KSA Over the Counter (OTC)Drugs Market Outlook to 2030

Region:Middle East

Author(s):Abhinav kumar

Product Code:KROD1349

December 2024

92

About the Report

KSA Over the Counter (OTC)Drugs Market Overview

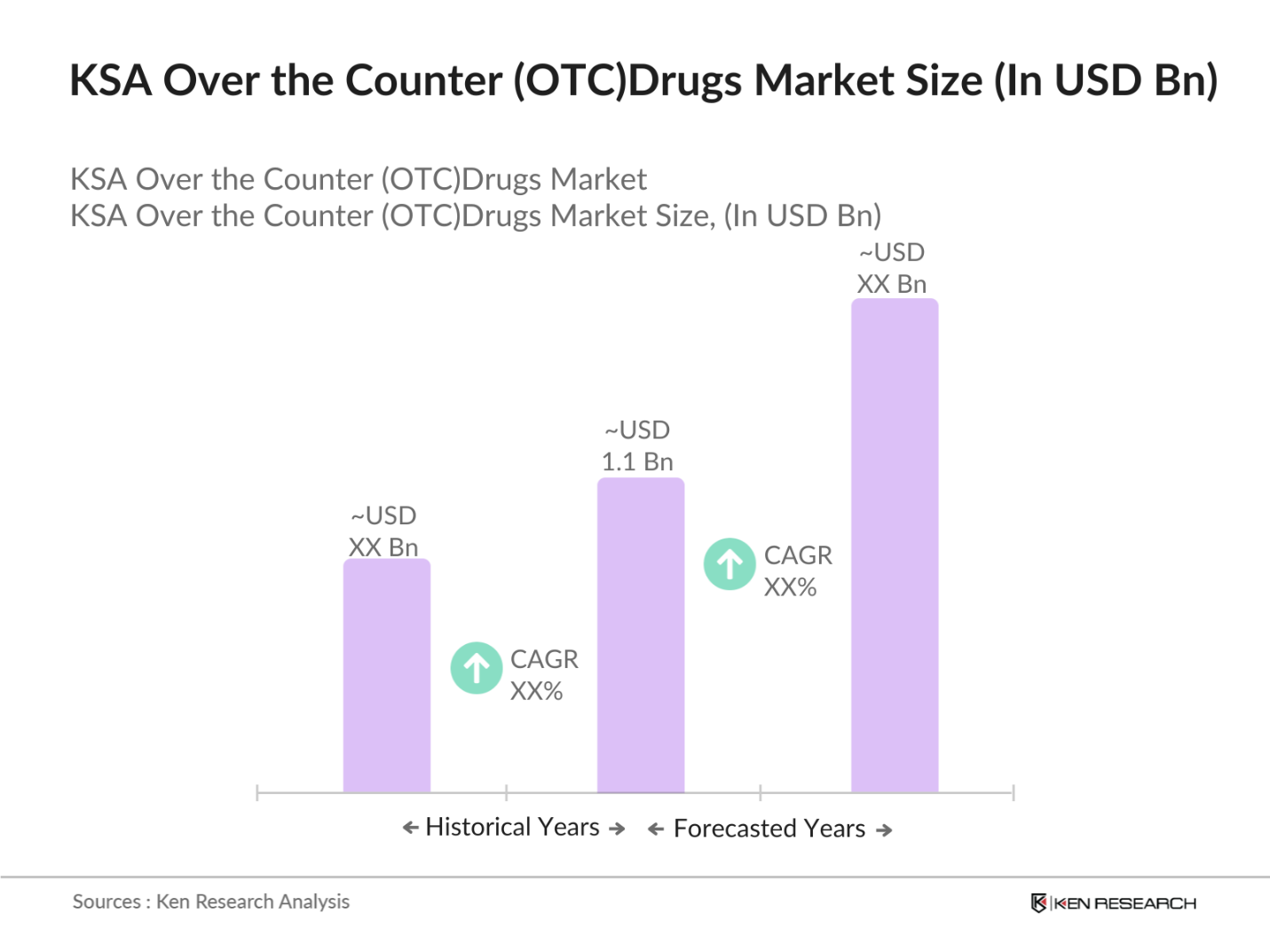

- The KSA Over the Counter (OTC)Drugs Market has shown steady growth, driven by rising cases of benign prostatic hyperplasia (BPH) and other prostate-related conditions among the aging male population. The market is valued at USD 1.1 billion, based on a five-year historical analysis. The market growth is largely influenced by the increasing preference for self-medication among men for mild to moderate symptoms of prostate enlargement, along with easier accessibility of OTC drugs through both physical and online pharmacies.

- The market is dominated by major cities such as Riyadh, Jeddah, and Dammam, where higher healthcare awareness and better access to healthcare facilities drive demand. Riyadh, in particular, stands out due to its advanced healthcare infrastructure and a higher concentration of the geriatric population, which makes it a key region for prostate health-related OTC products. Furthermore, the increasing disposable income in urban areas encourages consumers to purchase OTC drugs for self-treatment rather than visiting physicians.

- The adoption of digital marketing and telemedicine platforms has surged in Saudi Arabia, providing new avenues for promoting OTC prostate drugs. In 2023, the Communications and Information Technology Commission reported that 82% of the population had internet access, enabling widespread use of telemedicine services. These platforms are becoming crucial for patient education and the online purchase of OTC drugs.

KSA Over the Counter (OTC)Drugs Market Segmentation

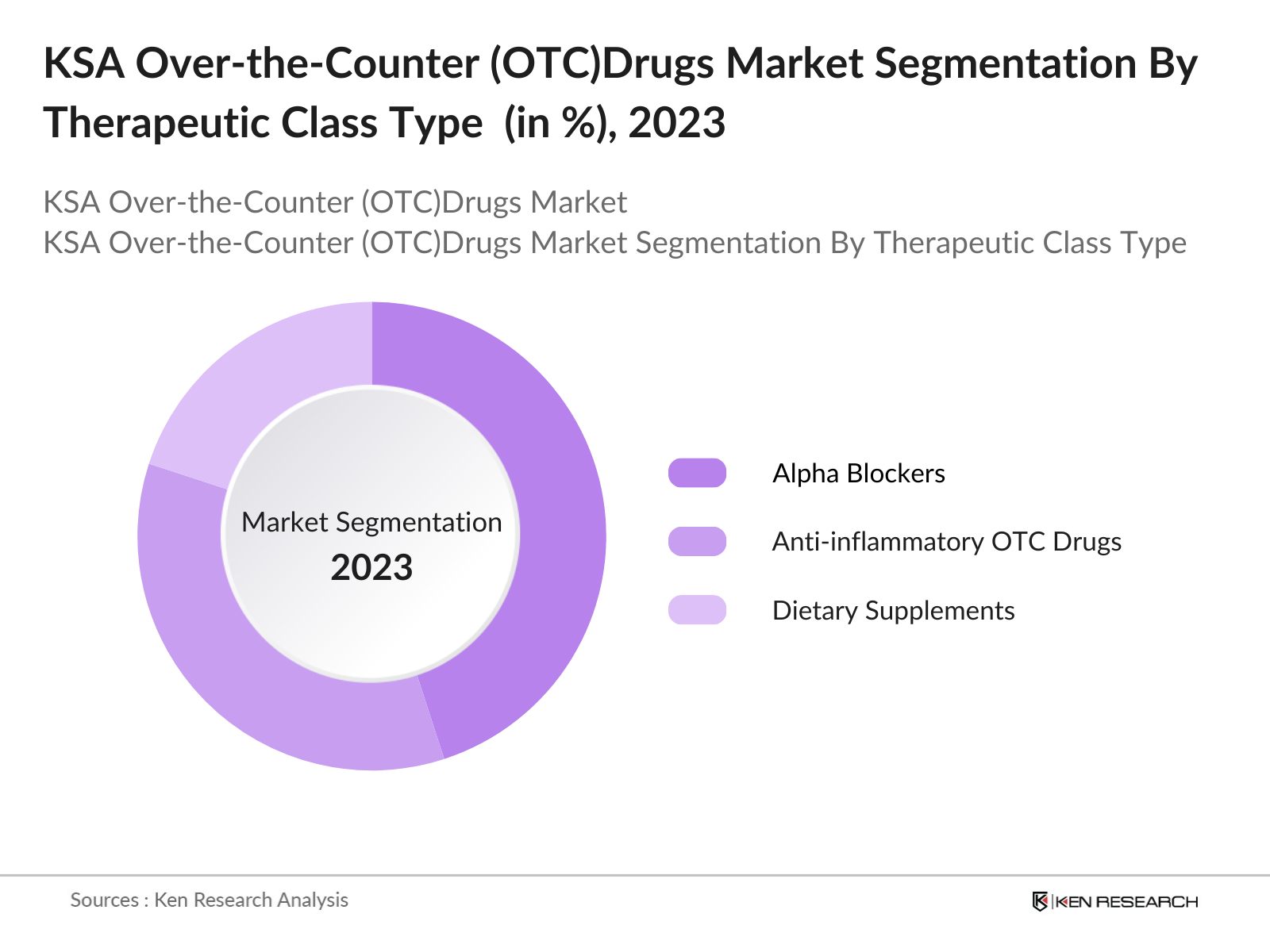

By Therapeutic Class: The KSA Over the Counter (OTC)Drugs Market is segmented by therapeutic class into alpha blockers, anti-inflammatory OTC drugs, and dietary supplements for prostate health. Recently, alpha blockers have maintained a dominant position due to their effectiveness in reducing the symptoms of BPH, such as urinary frequency and urgency. Consumers often prefer these drugs as they offer quick relief from symptoms, making them a popular choice among older men who seek non-prescription solutions for prostate issues.

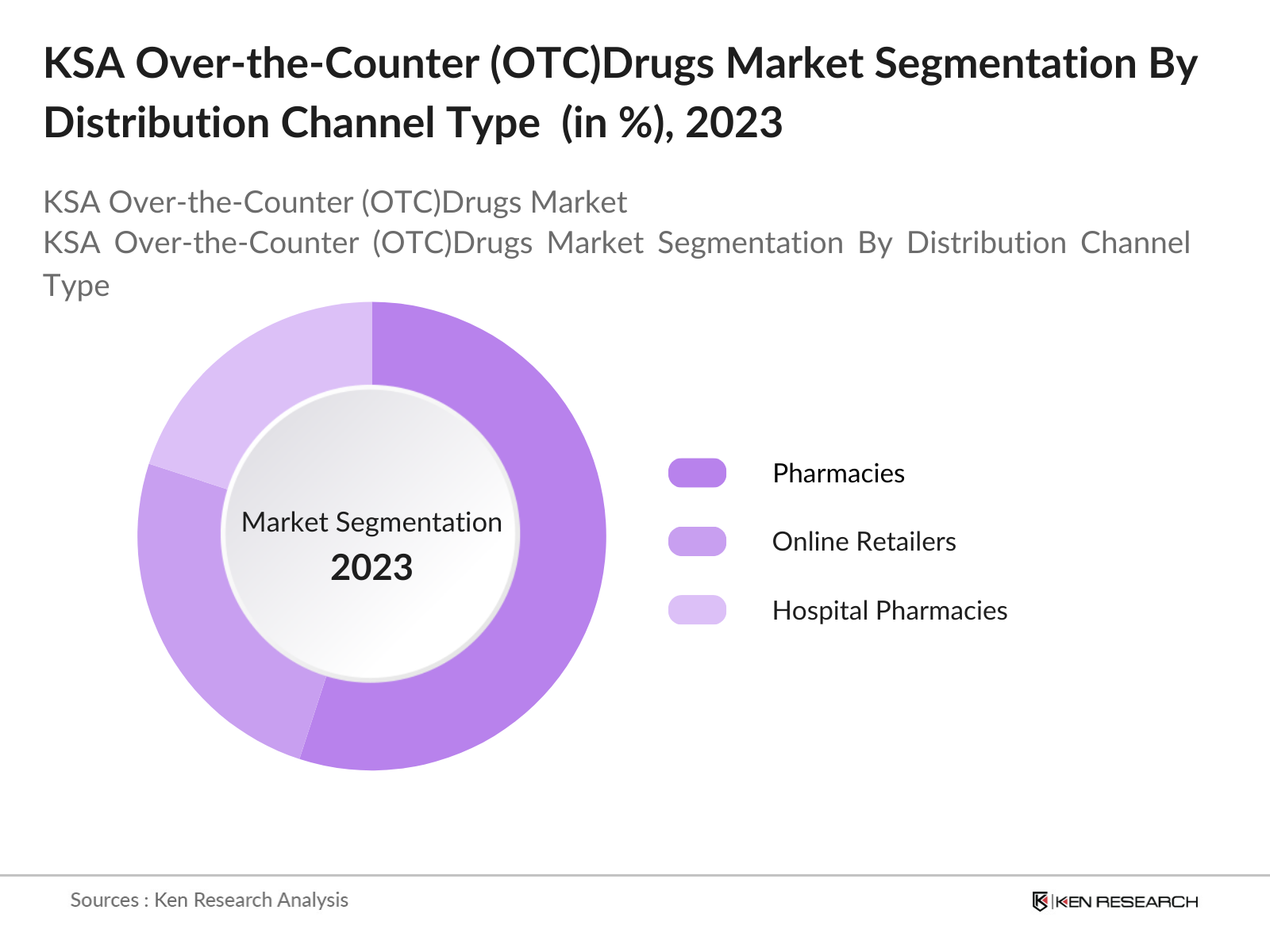

By Distribution Channel: The market is segmented by distribution channel into pharmacies, online retailers, and hospital pharmacies. Pharmacies hold the largest market share, driven by consumer trust in pharmacists for product recommendations and easy access to over-the-counter medications. The convenience of picking up prostate health products from pharmacies, along with the personalized guidance provided by pharmacists, makes this segment particularly strong.

KSA Over the Counter (OTC)Drugs Competitive Landscape

The KSA Over the Counter (OTC)Drugs Market is dominated by several global and local pharmaceutical companies. The market exhibits moderate consolidation, with a few key players holding significant market influence. Companies like Bayer AG and Pfizer Inc. have established strong footholds in the market due to their diverse product portfolios and trusted brand names. In addition to international firms, local manufacturers such as Jamjoom Pharma have emerged as prominent players due to their focus on regional healthcare needs.

|

Company |

Establishment Year |

Headquarters |

Product Portfolio |

R&D Expenditure |

Market Penetration |

Sales Revenue |

Manufacturing Locations |

Online Presence |

Marketing Strategy |

|

Bayer AG |

1863 |

Leverkusen, DE |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Pfizer Inc. |

1849 |

New York, USA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

GlaxoSmithKline PLC |

2000 |

Brentford, UK |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Jamjoom Pharma |

1994 |

Jeddah, KSA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Sanofi S.A. |

1973 |

Paris, FR |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

KSA Over the Counter (OTC)Drugs Industry Analysis

Growth Drivers

- Rising Prevalence of Prostate Conditions: The rising prevalence of prostate conditions, such as benign prostatic hyperplasia (BPH), is a significant driver of the demand for OTC drugs in Saudi Arabia. In 2023, the Saudi Ministry of Health reported that over 2 million men in the country are affected by prostate-related issues. The aging male population is a key factor contributing to this rise, with around 5 million men over the age of 40 by 2024. This increase directly correlates with growing demand for convenient, non-prescription treatment options.

- Increasing Demand for OTC Treatments: The shift toward over-the-counter (OTC) drugs in the Kingdom is evident, with rising demand fueled by increased self-medication practices. In 2024, the Saudi Arabian General Investment Authority highlighted a surge in OTC medication sales, especially for prostate health treatments, largely driven by a robust e-commerce sector with sales exceeding SAR 13 billion. This growth is linked to a population increasingly seeking quick, cost-effective solutions for managing mild to moderate prostate conditions.

- Growing Geriatric Population: The Kingdoms population is rapidly aging, with over 2.4 million individuals above the age of 65 in 2023, according to the General Authority for Statistics. This demographic shift is directly tied to a higher prevalence of prostate conditions, pushing the need for accessible OTC solutions. The Ministry of Health expects this figure to surpass 3 million by 2025, reinforcing the demand for non-prescription treatments tailored to prostate health.

Market Challenges

- Limited Awareness Among Patients: Despite the growing availability of OTC prostate drugs, there remains a significant gap in awareness. The Saudi Ministry of Health estimates that up to 60% of men with mild prostate symptoms in 2023 are unaware of available OTC treatments. This gap in knowledge creates a barrier to the market's full potential, as many patients still rely on prescription medication or remain untreated.

- Competition from Prescription Drugs: Prescription medications continue to dominate the prostate treatment market in Saudi Arabia. Data from the Saudi Food and Drug Authority indicates that prescription drugs still account for more than 70% of prostate-related treatments in 2023. While OTC alternatives are growing in popularity, the robust presence of prescribed drugs creates a competitive challenge for OTC drug manufacturers.

KSA Over the Counter (OTC)Drugs Market Future Outlook

Over the next five years, the KSA Over the Counter (OTC)Drugs Market is expected to show consistent growth, driven by rising awareness of prostate health among men, increased preference for non-prescription treatments, and the growth of digital healthcare platforms. Government initiatives aimed at improving healthcare access and the increasing penetration of e-commerce will further boost market growth. Additionally, innovations in drug formulations, including herbal and natural supplements, are likely to gain traction among health-conscious consumers seeking safer and more sustainable treatment options.

Opportunities

- Expansion of E-commerce Distribution Channels: E-commerce is emerging as a critical distribution channel for OTC drugs in Saudi Arabia. In 2023, e-commerce sales of pharmaceuticals, including OTC prostate drugs, surpassed SAR 10 billion, according to the General Authority for Statistics. The expansion of e-commerce platforms provides manufacturers with direct access to consumers, especially in remote areas, fueling growth in OTC prostate treatments.

- Product Innovation: Innovation in drug formulations and delivery methods is driving the growth of the OTC prostate drug market in Saudi Arabia. For instance, sublingual and fast-dissolving tablets for prostate conditions are becoming increasingly popular. In 2023, the Saudi Industrial Development Fund reported that several local pharmaceutical companies have begun investing in new drug delivery technologies, aiming to improve patient compliance and treatment efficacy.

Scope of the Report

|

Therapeutic Class |

Alpha Blockers Anti-inflammatory OTC Drugs Dietary Supplements for Prostate Health |

|

Distribution Channel |

Pharmacies Online Retailers Hospital Pharmacies |

|

Product Form |

Tablets Capsules Liquids Powders |

|

Region |

Riyadh Eastern Province Makkah Jeddah Medina |

|

End-User |

Geriatric Population Adult Male Population |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Pharmaceutical Companies

Government and Regulatory Bodies (Saudi FDA)

Online Pharmacies Companies

Hospitals and Healthcare Industries

Pharmacies Industries

Investments and Venture Capitalist Firms

Companies

Players Mentioned in the Report:

Bayer AG

Pfizer Inc.

GlaxoSmithKline PLC

Sanofi S.A.

Jamjoom Pharma

Novartis AG

Johnson & Johnson

Himalaya Drug Company

Astellas Pharma Inc.

Zydus Wellness

Boehringer Ingelheim GmbH

Cipla Ltd.

Abbott Laboratories

Reckitt Benckiser Group PLC

Al-Dawaa Pharmacies

Table of Contents

1. KSA Over-the-Counter (OTC) Drugs Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. KSA Over-the-Counter (OTC) Drugs Market Size (In SAR Mn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. KSA Over-the-Counter (OTC) Drugs Market Analysis

3.1 Growth Drivers

3.1.1 Rising Health Awareness

3.1.2 Expansion of Retail Pharmacies

3.1.3 Growing E-commerce Penetration

3.2 Market Challenges

3.2.1 Regulatory Compliance

3.2.2 Price Sensitivity

3.2.3 Consumer Trust Issues

3.3 Opportunities

3.3.1 Growth of Herbal and Natural OTC Products

3.3.2 Digital Health Integration

3.3.3 Strategic Partnerships

3.4 Trends

3.4.1 Self-Medication Practices

3.4.2 Rise of Personalized OTC Products

3.4.3 Growth of Online Pharmacies

3.5 Government Regulation

3.5.1 SFDA Guidelines

3.5.2 OTC Drug Reclassification

3.5.3 Advertising Standards

3.5.4 Price Controls

3.6 SWOT Analysis

3.6.1 Strengths

3.6.2 Weaknesses

3.6.3 Opportunities

3.6.4 Threats

3.7 Stake Ecosystem

3.7.1 Manufacturers

3.7.2 Retailers

3.7.3 Regulatory Bodies

3.7.4 Consumers

3.8 Porter’s Five Forces

3.8.1 Bargaining Power of Suppliers

3.8.2 Bargaining Power of Buyers

3.8.3 Threat of New Entrants

3.8.4 Threat of Substitutes

3.8.5 Competitive Rivalry

3.9 Competition Ecosystem

3.9.1 Key Players

3.9.2 Competitive Intensity

3.9.3 Innovation Landscape

4. KSA Over-the-Counter (OTC) Drugs Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Pain Relievers

4.1.2 Cough, Cold, and Allergy Medicines

4.1.3 Digestive Health Products

4.1.4 Vitamins and Supplements

4.1.5 Topical Ointments

4.2 By Distribution Channel (In Value %)

4.2.1 Retail Pharmacies

4.2.2 E-commerce Platforms

4.2.3 Supermarkets and Hypermarkets

4.2.4 Convenience Stores

4.3 By End-User (In Value %)

4.3.1 Individual Consumers

4.3.2 Institutional Buyers

4.4 By Dosage Form (In Value %)

4.4.1 Tablets

4.4.2 Capsules

4.4.3 Liquids

4.4.4 Topicals

4.5 By Region (In Value %)

4.5.1 Central KSA

4.5.2 Western KSA

4.5.3 Eastern KSA

4.5.4 Northern KSA

5. KSA Over-the-Counter (OTC) Drugs Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 GlaxoSmithKline (GSK)

5.1.2 Johnson & Johnson

5.1.3 Bayer AG

5.1.4 Pfizer

5.1.5 Sanofi

5.1.6 Reckitt Benckiser

5.1.7 Novartis

5.1.8 Abbott Laboratories

5.1.9 Procter & Gamble

5.1.10 Taibah Pharma

5.1.11 Hikma Pharmaceuticals

5.1.12 Jamjoom Pharmaceuticals

5.1.13 SPIMACO

5.1.14 Julphar

5.1.15 Tabuk Pharmaceuticals

5.2 Cross Comparison Parameters

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Grants

5.8 Private Equity Investments

6. KSA Over-the-Counter (OTC) Drugs Market Regulatory Framework

6.1 SFDA Regulations

6.2 Licensing and Compliance Requirements

6.3 Advertising Standards

6.4 OTC Drug Classification Guidelines

7. KSA Over-the-Counter (OTC) Drugs Future Market Size (In SAR Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. KSA Over-the-Counter (OTC) Drugs Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Distribution Channel (In Value %)

8.3 By End-User (In Value %)

8.4 By Dosage Form (In Value %)

8.5 By Region (In Value %)

9. KSA Over-the-Counter (OTC) Drugs Market Analysts’ Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Consumer Persona Insights

9.3 Distribution Channel Optimization

9.4 Innovation Opportunities

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves creating a comprehensive ecosystem map of all stakeholders in the KSA Over the Counter (OTC)Drugs Market. Using desk research from secondary sources, industry databases, and proprietary market data, the primary objective was to identify critical factors that affect market dynamics, such as distribution channel performance and product innovation.

Step 2: Market Analysis and Construction

This phase includes analyzing historical data related to market size, product penetration, and revenue growth. A detailed evaluation of the prostate health drug market was conducted, focusing on key drivers like product formulation, consumer preferences, and distribution trends.

Step 3: Hypothesis Validation and Expert Consultation

We conducted interviews with industry experts, pharmacists, and drug manufacturers using computer-assisted telephone interviews (CATI) to validate the market hypotheses. These expert insights were crucial for refining our data and assumptions about the market.

Step 4: Research Synthesis and Final Output

Finally, data gathered from primary and secondary sources were synthesized to create a robust market model. Additional insights were obtained directly from OTC drug manufacturers, which helped verify the accuracy of the bottom-up data used to form this report.

Frequently Asked Questions

01. How big is the KSA Over the Counter (OTC)Drugs Market?

The KSA Over the Counter (OTC)Drugs Market is valued at USD USD 1.1 billion, supported by the growing number of men suffering from benign prostatic hyperplasia (BPH) and the rising trend of self-medication for prostate health.

02. What are the challenges in the KSA Over the Counter (OTC)Drugs Market?

Challenges include regulatory hurdles for OTC drugs, competition from prescription medications, and limited awareness about OTC solutions for prostate health among the population, particularly in rural areas.

03. Who are the major players in the KSA Over the Counter (OTC)Drugs Market?

Key players in the market include Bayer AG, Pfizer Inc., GlaxoSmithKline PLC, Sanofi S.A., and Jamjoom Pharma. These companies dominate due to their strong distribution networks and trusted product offerings.

04. What are the growth drivers of the KSA Over the Counter (OTC)Drugs Market?

The market is driven by the rising prevalence of prostate conditions, growing consumer preference for OTC solutions, and advancements in drug formulations. Increased awareness of prostate health also plays a significant

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.