KSA Paper & Paperboard Packaging Market Outlook to 2030

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD4907

December 2024

80

About the Report

KSA Paper & Paperboard Packaging Market Overview

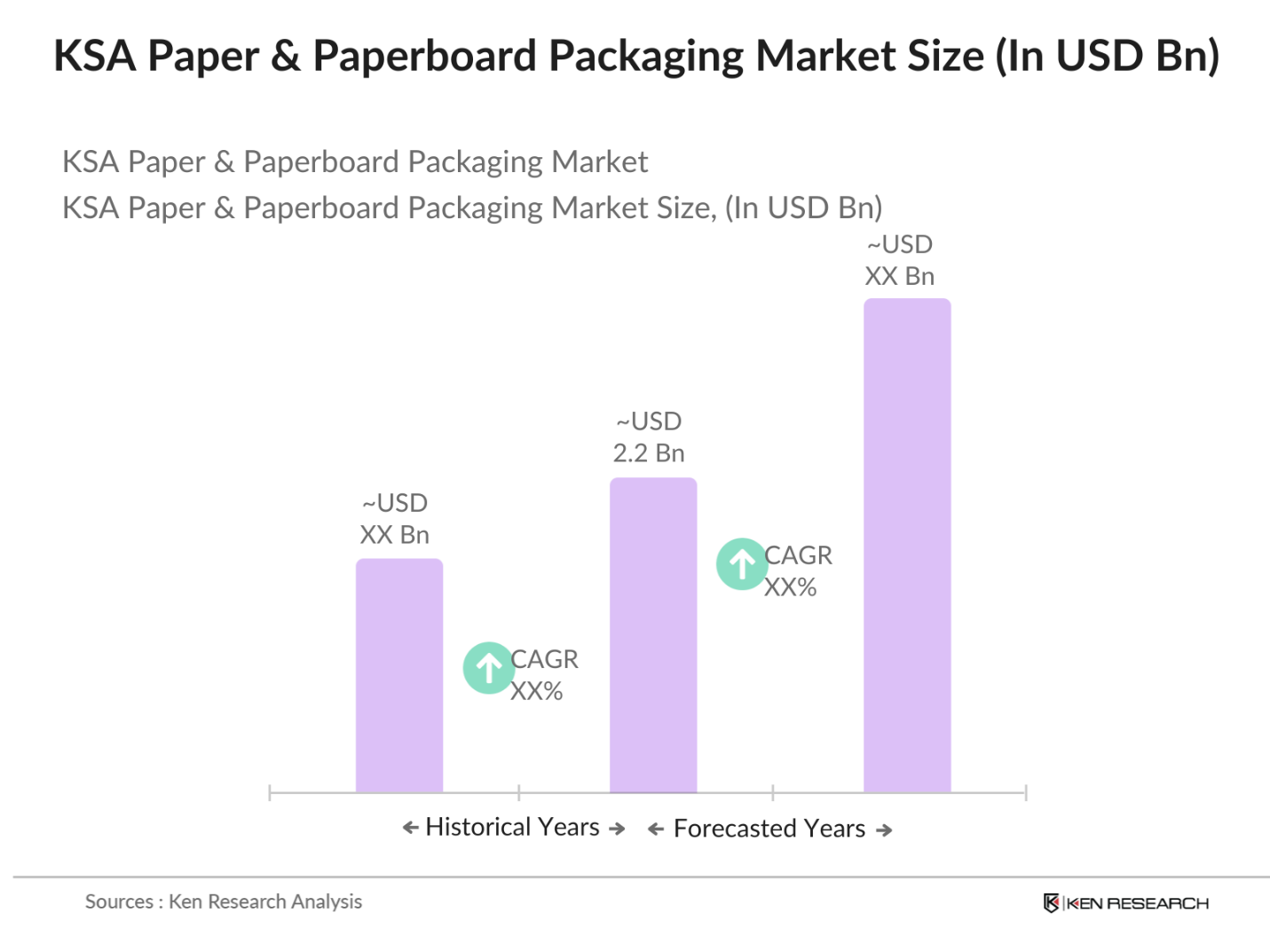

- The KSA paper and paperboard packaging market is valued at USD 2.2 billion, based on a five-year historical analysis. It is driven by the rising demand for sustainable packaging solutions in industries such as food & beverages, pharmaceuticals, and consumer goods. With Saudi Arabia's increasing focus on sustainable and recyclable materials in packaging, the market has witnessed significant growth. Additionally, the development of the e-commerce sector has also fueled the demand for paper and paperboard packaging as it is an eco-friendly option.

- Key cities in Saudi Arabia, such as Riyadh, Jeddah, and Dammam, dominate the market due to their large-scale industrial activities and robust supply chains. These cities host many manufacturers and industries that are adopting sustainable packaging solutions. Furthermore, Riyadhs role as the capital and economic hub ensures a concentration of packaging industries, while Dammam, with its proximity to the port, supports exports and trade.

- The Saudi government has implemented strict environmental packaging standards to regulate waste management and promote recycling. In 2023, the National Center for Waste Management mandated that packaging materials must meet at least 20% recycled content for large industries, encouraging the use of paperboard over plastic alternatives. These regulations are part of broader national efforts to achieve a 35% recycling rate by 2025, particularly in urban areas like Riyadh and Jeddah, where the majority of packaging waste is generated. Compliance with these mandates has significantly boosted the use of sustainable packaging materials.

KSA Paper & Paperboard Packaging Market Segmentation

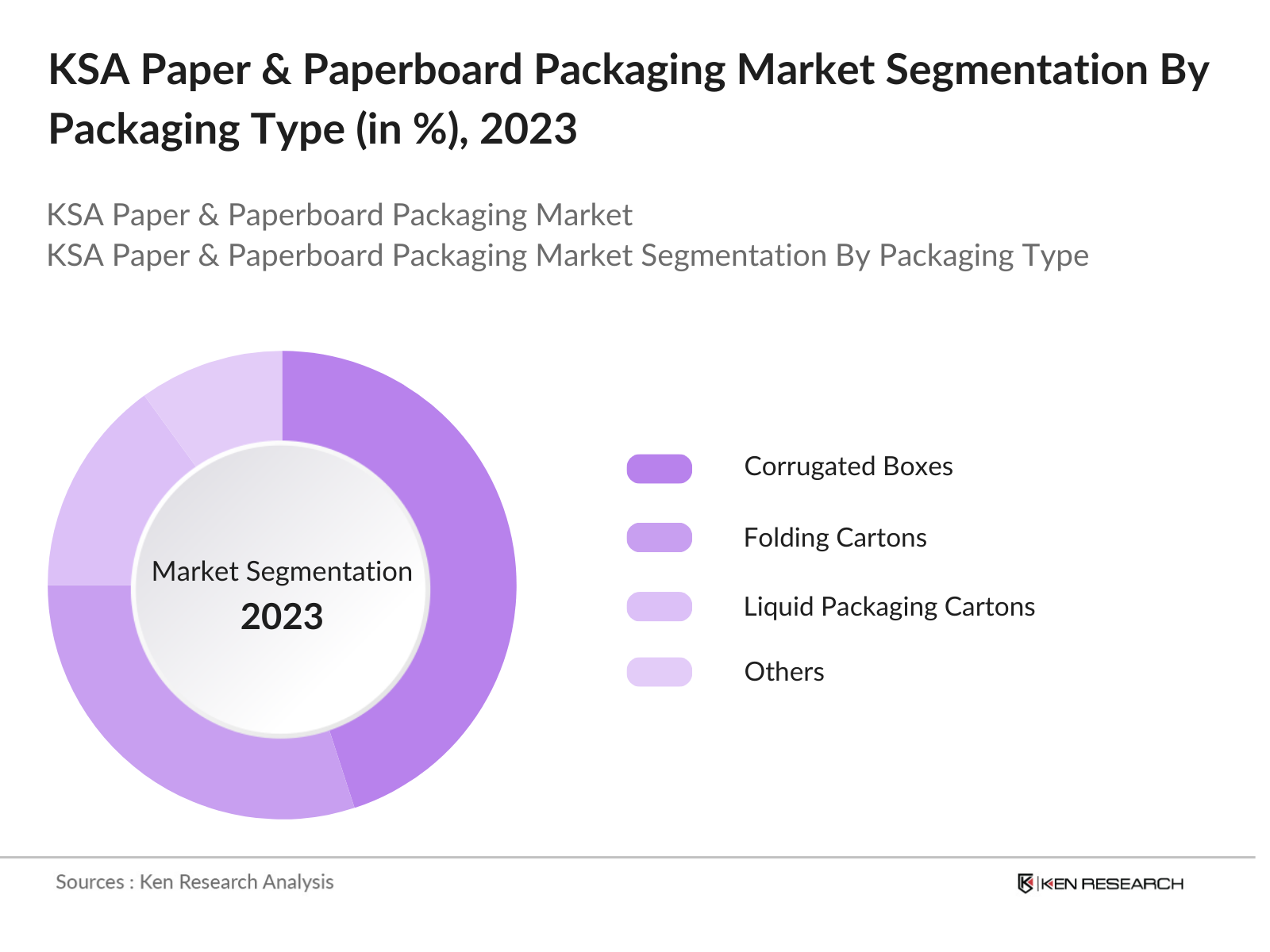

By Packaging Type: The KSA paper and paperboard packaging market is segmented by packaging type into corrugated boxes, folding cartons, liquid packaging cartons, and others (e.g., flexible paper, wrapping paper). Among these, corrugated boxes hold the dominant market share due to their widespread use in shipping and e-commerce applications. Their durability, lightweight nature, and recyclability make them the preferred choice for logistics and warehousing. E-commerce growth, accelerated by the pandemic, has further reinforced the demand for corrugated boxes as they protect products during transit.

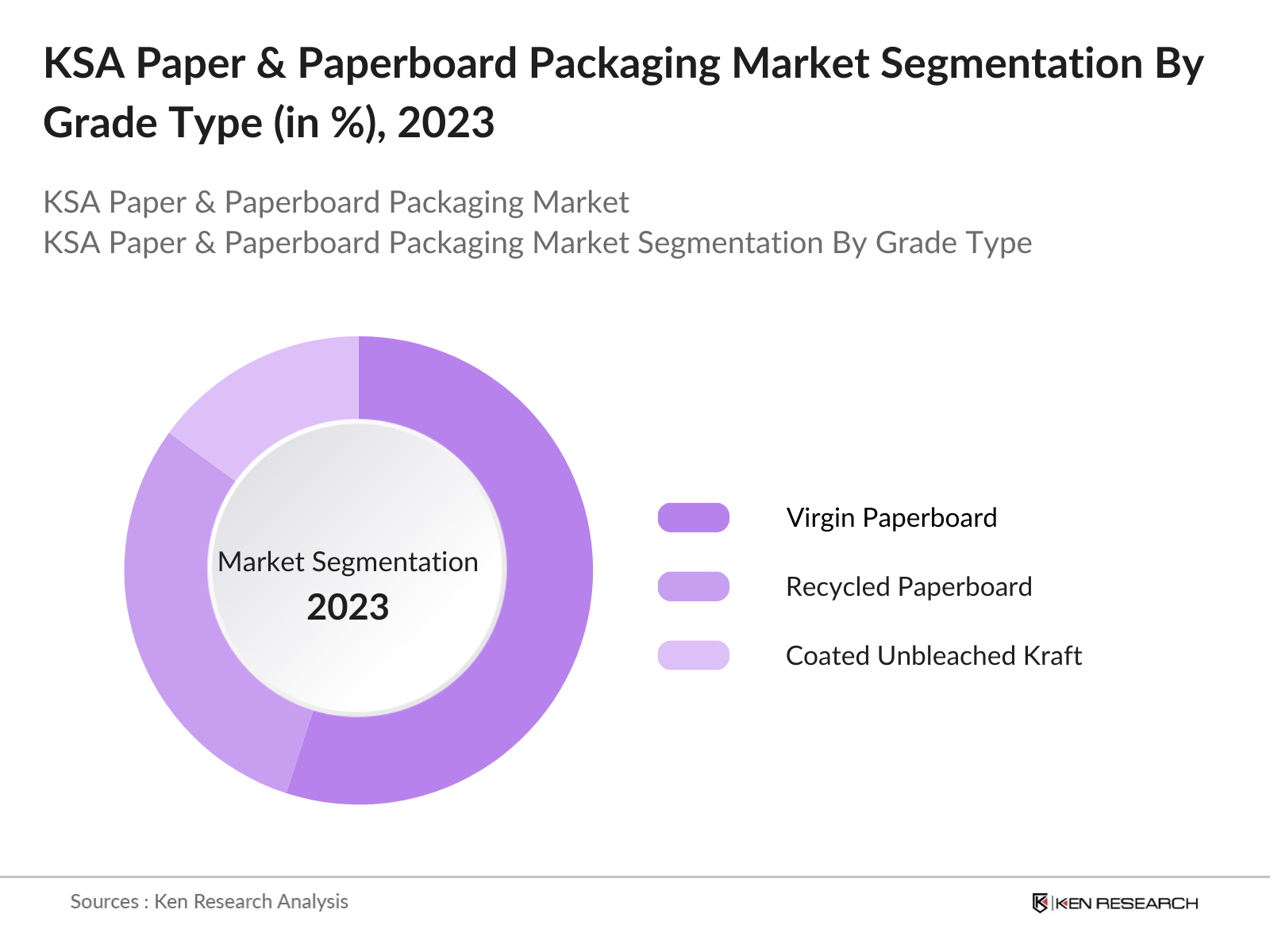

By Grade: The market is also segmented by grade into virgin paperboard, recycled paperboard, and coated unbleached kraft paperboard. Virgin paperboard dominates this segment, as it is preferred for high-quality packaging in industries such as food and beverages, pharmaceuticals, and cosmetics. The smooth surface and hygiene factor of virgin paperboard make it an ideal material for packaging premium products. Recycled paperboard, however, is gaining traction, driven by the growing emphasis on environmental sustainability and government initiatives supporting recycling.

KSA Paper & Paperboard Packaging Market Competitive Landscape

The KSA paper and paperboard packaging market is characterized by the presence of both domestic and international players. The competitive landscape is shaped by key companies that have established strong supply chains and invested in technology upgrades to enhance their production capabilities. Domestic players benefit from local resources and regulatory policies, while international players leverage advanced technologies and larger production scales.

|

Company Name |

Year Established |

Headquarters |

Production Capacity |

Sustainability Initiatives |

R&D Investment |

Key Products |

Market Presence |

Employee Strength |

|

International Paper |

1898 |

Memphis, USA |

_ |

_ |

_ |

_ |

_ |

_ |

|

Mondi Group |

1967 |

Vienna, Austria |

_ |

_ |

_ |

_ |

_ |

_ |

|

Saudi Paper Manufacturing Co. |

1989 |

Dammam, KSA |

_ |

_ |

_ |

_ |

_ |

_ |

|

Smurfit Kappa |

1934 |

Dublin, Ireland |

_ |

_ |

_ |

_ |

_ |

_ |

|

Gulf Carton Factory Co. |

1990 |

Riyadh, KSA |

_ |

_ |

_ |

_ |

_ |

_ |

KSA Paper & Paperboard Packaging Industry Analysis

Growth Drivers

- Expanding E-commerce Sector: The growing e-commerce sector in Saudi Arabia has significantly driven demand for paper and paperboard packaging, particularly in corrugated boxes. In 2023, Saudi Arabias e-commerce market was valued at $12.5 billion, with more than 47 million parcels delivered annually. This surge in e-commerce is pushing demand for sustainable and efficient packaging solutions, making paperboard packaging essential. The high volume of shipping activities requires lightweight, strong packaging to protect goods in transit. The focus on sustainability has also aligned with Vision 2030, encouraging more businesses to switch to recyclable materials for packaging.

- Industrial Packaging Demand: The Kingdom's industrial growth, particularly in FMCG, pharmaceuticals, and construction, has created a substantial demand for robust packaging solutions. In 2023, the Saudi FMCG sector generated revenue of $30.2 billion, with the pharmaceuticals market reaching $9.7 billion. These industries increasingly require durable and flexible packaging to support their extensive logistics networks. Paper and paperboard packaging, especially multi-layered corrugated boards, cater to the sector's needs for strength and sustainability. The construction industry, with projects worth over $1 trillion under Saudi Vision 2030, is also driving demand for industrial packaging for raw materials and components.

- Sustainability and Environmental Policies: Saudi Arabia's government regulations focusing on environmental sustainability, as part of its Vision 2030, are a key driver for the paper and paperboard packaging market. The Saudi government has set a goal of achieving 35% waste recycling by 2025. Policies promoting eco-friendly practices are encouraging manufacturers to adopt recyclable and biodegradable materials in packaging. Paper-based packaging, being recyclable and less harmful to the environment, is benefiting from these regulations. Companies in the region are adopting greener packaging solutions to comply with governmental mandates, resulting in an increase in demand for sustainable paperboard products.

Market Challenges

- Raw Material Volatility: One of the significant challenges in the paper and paperboard packaging market is the fluctuation in raw material prices, particularly pulp and recycled paper. In 2023, global pulp prices averaged $1,020 per ton, but Saudi Arabia experienced price increases due to regional supply chain constraints and rising energy costs. With Saudi Arabia importing a large proportion of its pulp, market players face heightened cost pressures. Additionally, fluctuating availability of recycled paper affects production cycles and profit margins. This price volatility impacts the profitability and competitiveness of local manufacturers.

- High Competition and Price Pressure: The paper and paperboard packaging market in Saudi Arabia is highly competitive, with a large number of domestic and international players. This intense competition exerts downward pressure on prices, impacting the profitability of companies. In 2022, there were over 150 active packaging manufacturers in the Kingdom, with most operating on thin margins. Moreover, companies must continually innovate and improve production efficiencies to remain competitive, leading to increased operational costs. Import tariffs and global market conditions further contribute to price pressure, especially when companies rely on imported raw materials.

KSA Paper & Paperboard Packaging Market Future Outlook

Over the next five years, the KSA paper and paperboard packaging market is expected to witness significant growth driven by increasing government regulations promoting sustainability, rising consumer demand for eco-friendly packaging, and technological advancements in packaging materials. The push towards Vision 2030, which emphasizes environmental sustainability and circular economies, will likely continue to spur investments in the recycling and manufacturing of paper and paperboard products. The market will also benefit from the expansion of key industries such as food and beverages, healthcare, and e-commerce, all of which have strong ties to packaging demand. The transition to smart and biodegradable packaging solutions, coupled with innovations in design and material use, will be key growth drivers.

Opportunities

- Circular Economy Initiatives: Saudi Arabia is increasingly adopting circular economy principles, offering a significant opportunity for the paper and paperboard packaging market. In 2024, the government launched a $1.5 billion fund dedicated to promoting sustainable waste management practices, including recycling initiatives in the packaging sector. This shift towards resource efficiency and recycling creates opportunities for packaging manufacturers to produce paperboard products using recycled materials. Furthermore, public and private investments in infrastructure to support recycling are expected to enhance the supply of sustainable raw materials, thus promoting the use of eco-friendly packaging solutions.

- Rising Consumer Preference for Sustainable Packaging: Consumer awareness of environmental issues has led to a shift in demand towards sustainable packaging. In 2023, more than 60% of Saudi consumers expressed a preference for products with eco-friendly packaging. This trend aligns with global shifts in consumer behavior and is creating an opportunity for paper and paperboard packaging companies to capitalize on the growing demand for recyclable, biodegradable, and compostable packaging. Businesses across sectors such as food, beverages, and cosmetics are increasingly turning to paper-based alternatives to meet consumer expectations and comply with regulations.

Scope of the Report

|

By Packaging Type |

Corrugated Boxes |

|

By Grade |

Virgin Paperboard |

|

By End-Use Industry |

Food & Beverages |

|

By Region |

Central Region |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Companies of Paper and Paperboard Packaging Materials

Paper Recycling Companies

Food & Beverage Industry

Healthcare and Pharmaceuticals Industry

E-commerce and Retail Companies

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Saudi Standards, Metrology, and Quality Organization, Ministry of Industry and Mineral Resources)

Packaging Machinery Manufacturing Companies

Companies

Players Mentioned in the Report

International Paper

Mondi Group

Smurfit Kappa

Saudi Paper Manufacturing Co.

Al Jabr Paper & Packaging

Gulf Carton Factory Co.

Middle East Paper Co. (MEPCO)

Sealed Air Corporation

Tetra Pak Arabia

Huhtamaki Group

Table of Contents

1. KSA Paper & Paperboard Packaging Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (CAGR, Volume/Value Growth, GDP Contribution)

1.4. Market Segmentation Overview

2. KSA Paper & Paperboard Packaging Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis (In Volume & Value)

2.3. Key Market Developments and Milestones

3. KSA Paper & Paperboard Packaging Market Analysis

3.1. Growth Drivers

3.1.1. Expanding E-commerce Sector

3.1.2. Industrial Packaging Demand (FMCG, Pharmaceuticals, Construction)

3.1.3. Sustainability and Environmental Policies (Government Regulations)

3.1.4. Technological Advancements in Manufacturing and Recycling

3.2. Market Challenges

3.2.1. Raw Material Volatility (Pulp, Recycled Paper)

3.2.2. High Competition and Price Pressure

3.2.3. Lack of Advanced Recycling Infrastructure

3.3. Opportunities

3.3.1. Circular Economy Initiatives

3.3.2. Rising Consumer Preference for Sustainable Packaging

3.3.3. Growth in Packaged Food & Beverage Industry

3.4. Trends

3.4.1. Shift to Lightweight Packaging Materials

3.4.2. Increase in Usage of Recyclable and Biodegradable Paperboard

3.4.3. Demand for Smart Packaging Solutions

3.5. Government Regulations

3.5.1. Environmental Packaging Standards (Waste Management, Recycling Mandates)

3.5.2. National Sustainability Policies (Vision 2030, Green Initiatives)

3.5.3. Tariffs and Import/Export Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Suppliers, Distributors, Consumers)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. KSA Paper & Paperboard Packaging Market Segmentation

4.1. By Packaging Type (In Volume & Value %)

4.1.1. Corrugated Boxes

4.1.2. Folding Cartons

4.1.3. Liquid Packaging Cartons

4.1.4. Others (Flexible Paper, Wrapping Paper)

4.2. By Grade (In Volume & Value %)

4.2.1. Virgin Paperboard

4.2.2. Recycled Paperboard

4.2.3. Coated Unbleached Kraft Paperboard

4.3. By End-Use Industry (In Volume & Value %)

4.3.1. Food & Beverages

4.3.2. Healthcare & Pharmaceuticals

4.3.3. Consumer Goods

4.3.4. E-commerce

4.3.5. Industrial Applications

4.4. By Region (In Volume & Value %)

4.4.1. Central Region

4.4.2. Western Region

4.4.3. Eastern Region

4.4.4. Northern Region

4.4.5. Southern Region

5. KSA Paper & Paperboard Packaging Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. International Paper

5.1.2. Mondi Group

5.1.3. Smurfit Kappa

5.1.4. Saudi Paper Manufacturing Co.

5.1.5. Al Jabr Paper & Packaging

5.1.6. Gulf Carton Factory Co.

5.1.7. Middle East Paper Co. (MEPCO)

5.1.8. Sealed Air Corporation

5.1.9. Tetra Pak Arabia

5.1.10. Huhtamaki Group

5.1.11. RAK Ghani Glass

5.1.12. Georgia-Pacific LLC

5.1.13. DS Smith PLC

5.1.14. Nine Dragons Paper

5.1.15. Packaging Corporation of America (PCA)

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Sustainability Initiatives, Packaging Innovations, Market Presence, Production Capacity)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, New Product Launches, R&D Investment)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Capital Investment, Facility Expansion)

5.7 Venture Capital Funding in Packaging Startups

5.8. Government Incentives and Grants

5.9. Private Equity Investments

6. KSA Paper & Paperboard Packaging Market Regulatory Framework

6.1. Environmental Standards (Recycling and Waste Reduction Regulations)

6.2. Compliance Requirements (Packaging Material Composition, Safety Standards)

6.3. Certification Processes (ISO Certifications, FSC Certification)

7. KSA Paper & Paperboard Packaging Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. KSA Paper & Paperboard Packaging Future Market Segmentation

8.1. By Packaging Type (In Value %)

8.2. By Grade (In Value %)

8.3. By End-Use Industry (In Value %)

8.4. By Region (In Value %)

9. KSA Paper & Paperboard Packaging Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segmentation Analysis

9.3. White Space Opportunity Analysis

9.4. Strategic Marketing Recommendations

Research Methodology

Step 1: Identification of Key Variables

The initial phase involved identifying key variables affecting the KSA paper and paperboard packaging market, including raw material availability, industrial demand, and government policies promoting sustainability. Extensive desk research was carried out utilizing proprietary databases and secondary sources such as industry reports.

Step 2: Market Analysis and Construction

Historical data from 2018 to 2023 was analyzed to determine market penetration and growth. This included calculating market shares for different packaging types and grades while assessing overall industry trends and market demand for recycled and virgin paperboards.

Step 3: Hypothesis Validation and Expert Consultation

Key market hypotheses, such as the increasing role of sustainable packaging and growth in e-commerce, were validated through interviews with industry stakeholders, including manufacturers, distributors, and government agencies. This process helped refine the market estimates.

Step 4: Research Synthesis and Final Output

The final output involved consolidating quantitative data and insights from multiple primary and secondary sources. This allowed us to provide accurate market figures for 2023, identify key growth drivers, and validate the final market forecasts.

Frequently Asked Questions

01. How big is the KSA Paper & Paperboard Packaging Market?

The KSA paper and paperboard packaging market is valued at USD 2.2 billion, driven by demand for sustainable and eco-friendly packaging materials in sectors such as food and beverages, pharmaceuticals, and e-commerce.

02. What are the challenges in the KSA Paper & Paperboard Packaging Market?

Key challenges include fluctuations in raw material prices, limited recycling infrastructure, and increasing competition from alternative packaging materials such as plastics and bio-based packaging solutions.

03. Who are the major players in the KSA Paper & Paperboard Packaging Market?

Key players include International Paper, Mondi Group, Smurfit Kappa, Saudi Paper Manufacturing Co., and Gulf Carton Factory Co., all of whom are leaders in the market due to their large production capacities and focus on sustainability.

04. What are the growth drivers of the KSA Paper & Paperboard Packaging Market?

Growth is driven by the demand for sustainable packaging, supported by government regulations and Vision 2030 initiatives, the rise of e-commerce, and the growing need for packaged consumer goods and pharmaceuticals.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.