KSA Payments Market Outlook to 2030

Region:Middle East

Author(s):Yogita Sahu

Product Code:KROD4426

Region:Middle East

Author(s):Yogita Sahu

Product Code:KROD4426

October 2024

81

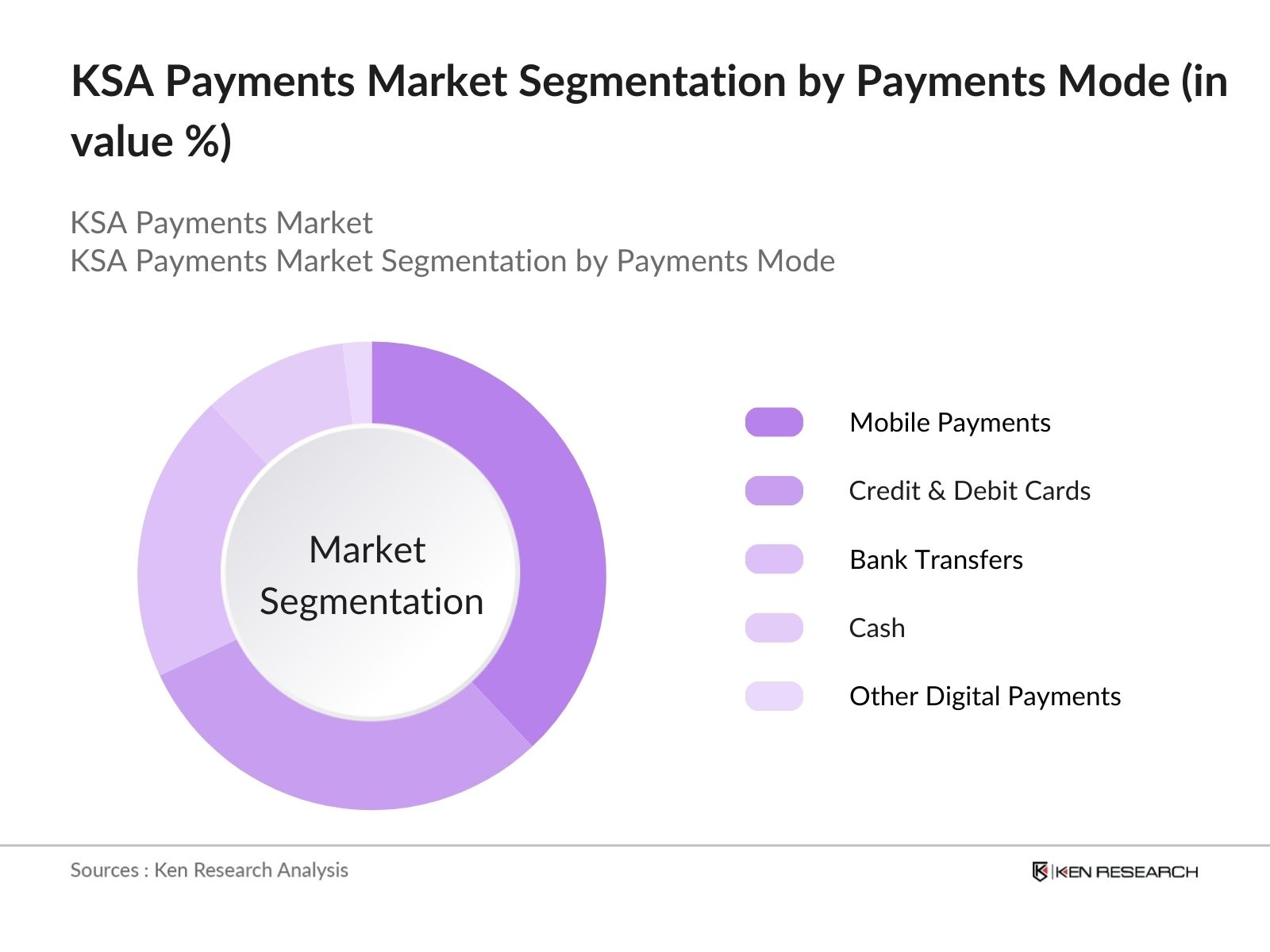

By Payment Mode: The market is segmented by payment mode into mobile payments, credit & debit cards, bank transfers, cash, and other digital payments. Recently, mobile payments have gained a dominant market share in the Kingdom, primarily due to the widespread use of smartphones and the introduction of apps like STC Pay and Apple Pay. These services have allowed consumers to make seamless transactions, including bill payments, money transfers, and retail purchases, without relying on cash or physical cards.

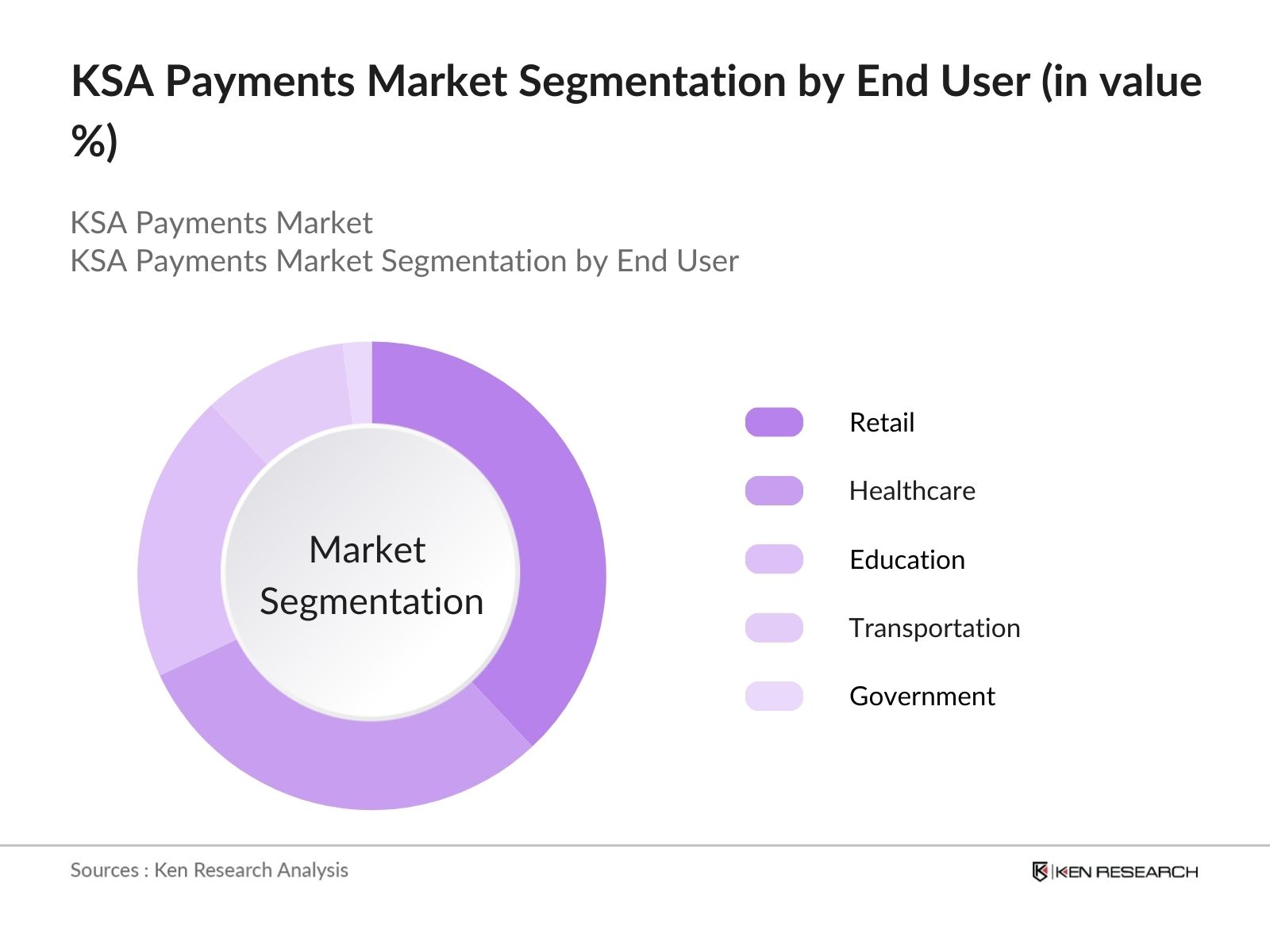

By End User: The market is also segmented by end user into retail, healthcare, education, transportation, and government. the retail sector is the largest contributor to the market due to the significant shift towards online shopping and digital payments. The growing popularity of e-commerce platforms such as Noon and Amazon KSA, coupled with the increasing use of mobile wallets and contactless payment options in physical stores, has resulted in the retail segment being the top end-user for digital transactions.

The market is dominated by a combination of local and international players, including payment platforms, banks, and fintech companies. Companies like STC Pay, Mada, and Al Rajhi Bank lead the market, benefitting from strong government backing and well-established financial infrastructures.

|

Company |

Establishment Year |

Headquarters |

Revenue |

No. of Employees |

Transaction Volume |

Technology Integration |

Market Presence |

Key Partnerships |

|

STC Pay |

2018 |

Riyadh |

||||||

|

Mada (Saudi Payments) |

1990 |

Riyadh |

||||||

|

Al Rajhi Bank |

1957 |

Riyadh |

||||||

|

PayTabs |

2014 |

Dammam |

||||||

|

HyperPay |

2014 |

Riyadh |

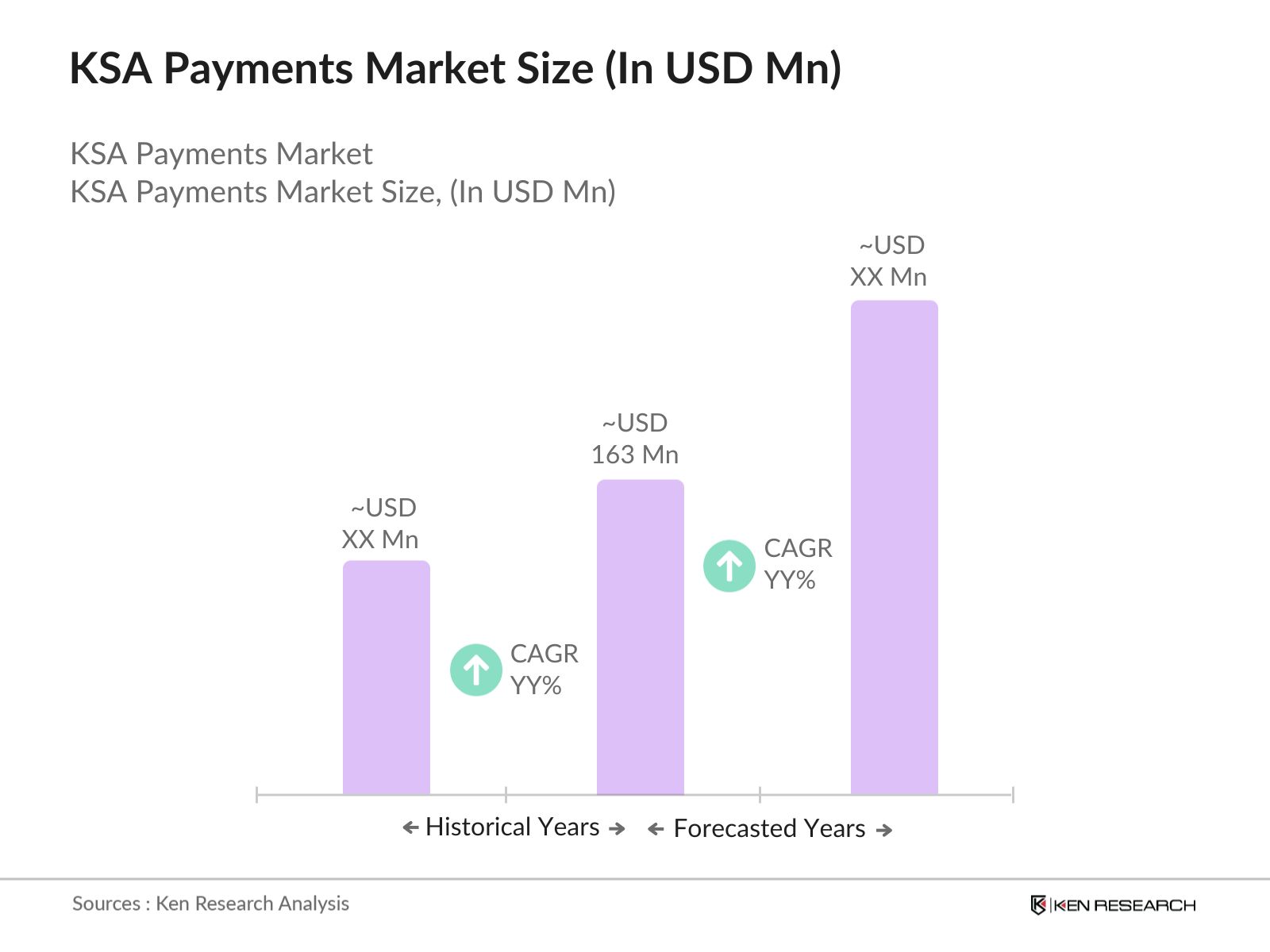

Over the next few years, the KSA payments industry is expected to show growth driven by continuous government support for digital transformation, advancements in payment technologies such as blockchain and AI, and increasing consumer demand for contactless and mobile payments. Furthermore, with Vision 2030 emphasizing the reduction of cash-based transactions and fostering financial inclusion, the payments ecosystem is set to evolve rapidly.

|

Payment Mode |

Mobile Payments Credit & Debit Cards Bank Transfers Cash Other Digital Payments |

|

End User |

Retail Healthcare Education Transportation Government |

|

Transaction Type |

B2B Payments B2C Payments C2C Payments G2P Payments |

|

Technology |

NFC QR Code Payments Blockchain-Based Payments Cloud-Based Payment Systems |

|

Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Government Initiatives (Vision 2030, Digital Transformation)

3.1.2. Growing E-commerce and Online Retail

3.1.3. Rising Smartphone Penetration

3.1.4. Increase in Financial Inclusion and Cashless Economy

3.2. Market Challenges

3.2.1. Cybersecurity and Data Privacy Concerns

3.2.2. Regulatory Barriers

3.2.3. High Infrastructure Costs for Payment Gateways

3.3. Opportunities

3.3.1. Growth of Mobile Wallets and Digital Payments

3.3.2. International Payment Platforms Entering the Market

3.3.3. Partnerships Between Banks and Fintechs

3.4. Trends

3.4.1. Emergence of Contactless Payments (NFC, QR Codes)

3.4.2. Blockchain and Cryptocurrency Integration

3.4.3. Buy Now, Pay Later (BNPL) Adoption

3.5. Regulatory Framework

3.5.1. SAMA (Saudi Arabian Monetary Authority) Regulations

3.5.2. Anti-Money Laundering (AML) and KYC Compliance

3.5.3. Open Banking Regulations and APIs

3.5.4. Consumer Protection Laws for Digital Payments

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.7.1. Key Players: Banks, Fintechs, Payment Processors

3.7.2. Roles and Responsibilities

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Payment Mode (In Value %)

4.1.1. Mobile Payments

4.1.2. Credit & Debit Cards

4.1.3. Bank Transfers

4.1.4. Cash

4.1.5. Other Digital Payments

4.2. By End User (In Value %)

4.2.1. Retail

4.2.2. Healthcare

4.2.3. Education

4.2.4. Transportation

4.2.5. Government

4.3. By Transaction Type (In Value %)

4.3.1. B2B Payments

4.3.2. B2C Payments

4.3.3. C2C Payments

4.3.4. G2P (Government to Person) Payments

4.4. By Technology (In Value %)

4.4.1. Near Field Communication (NFC)

4.4.2. QR Code Payments

4.4.3. Blockchain-Based Payments

4.4.4. Cloud-Based Payment Systems

4.5. By Region (In Value %)

4.5.1. North

4.5.2. East

4.5.3. West

4.5.4. South

5.1. Detailed Profiles of Major Companies

5.1.1. STC Pay

5.1.2. Mada (Saudi Payments Network)

5.1.3. Al Rajhi Bank

5.1.4. PayTabs

5.1.5. HyperPay

5.1.6. SABB (Saudi British Bank)

5.1.7. Riyad Bank

5.1.8. Saudi Payments

5.1.9. National Commercial Bank (NCB)

5.1.10. Arab National Bank

5.1.11. QNB Alahli

5.1.12. American Express Saudi Arabia

5.1.13. Visa Saudi Arabia

5.1.14. Mastercard Saudi Arabia

5.1.15. Apple Pay

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Active Users, Transaction Volume, Technology Integration, Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Central Bank Policies

6.2. Payment System Regulations

6.3. Licensing and Compliance Requirements

6.4. Taxation Policies on Digital Transactions

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Payment Mode (In Value %)

8.2. By End User (In Value %)

8.3. By Transaction Type (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the KSA Payments Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

In this phase, we will compile and analyze historical data about the KSA Payments Market. This includes assessing market penetration, the ratio of payment service providers to consumers, and the resultant transaction volumes. Furthermore, an evaluation of service adoption statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Market hypotheses will be developed and subsequently validated through interviews with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

The final phase involves direct engagement with key stakeholders such as payment platforms, banks, and fintech companies to acquire detailed insights into transaction volumes, service offerings, and consumer behavior. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the KSA Payments market.

The KSA Payments Market, valued at USD 163 million, is driven by strong government support, increased smartphone penetration, and the widespread adoption of digital payment platforms across various sectors like retail and government services.

Challenges in the KSA payments market include cybersecurity concerns, regulatory hurdles related to fintech innovations, and the high costs of building and maintaining secure digital payment infrastructures.

Key players in the KSA payments market include STC Pay, Mada, Al Rajhi Bank, PayTabs, and HyperPay. These companies dominate due to their strong government backing, extensive infrastructure, and wide acceptance across industries.

Growth drivers in the KSA Payments Market include the push for digital transformation under Vision 2030, the increasing use of mobile payment solutions, and the expansion of the e-commerce industry, which has led to a surge in online transactions and contactless payments.

Key trends in the KSA payments market include the rise of contactless payment methods such as NFC and QR code payments, growing interest in blockchain-based transactions, and the emergence of buy-now-pay-later (BNPL) solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.