KSA Prosthetics Market Outlook to 2030

Region:Middle East

Author(s):Sanjna

Product Code:KROD6824

November 2024

81

About the Report

KSA Prosthetics Market Overview

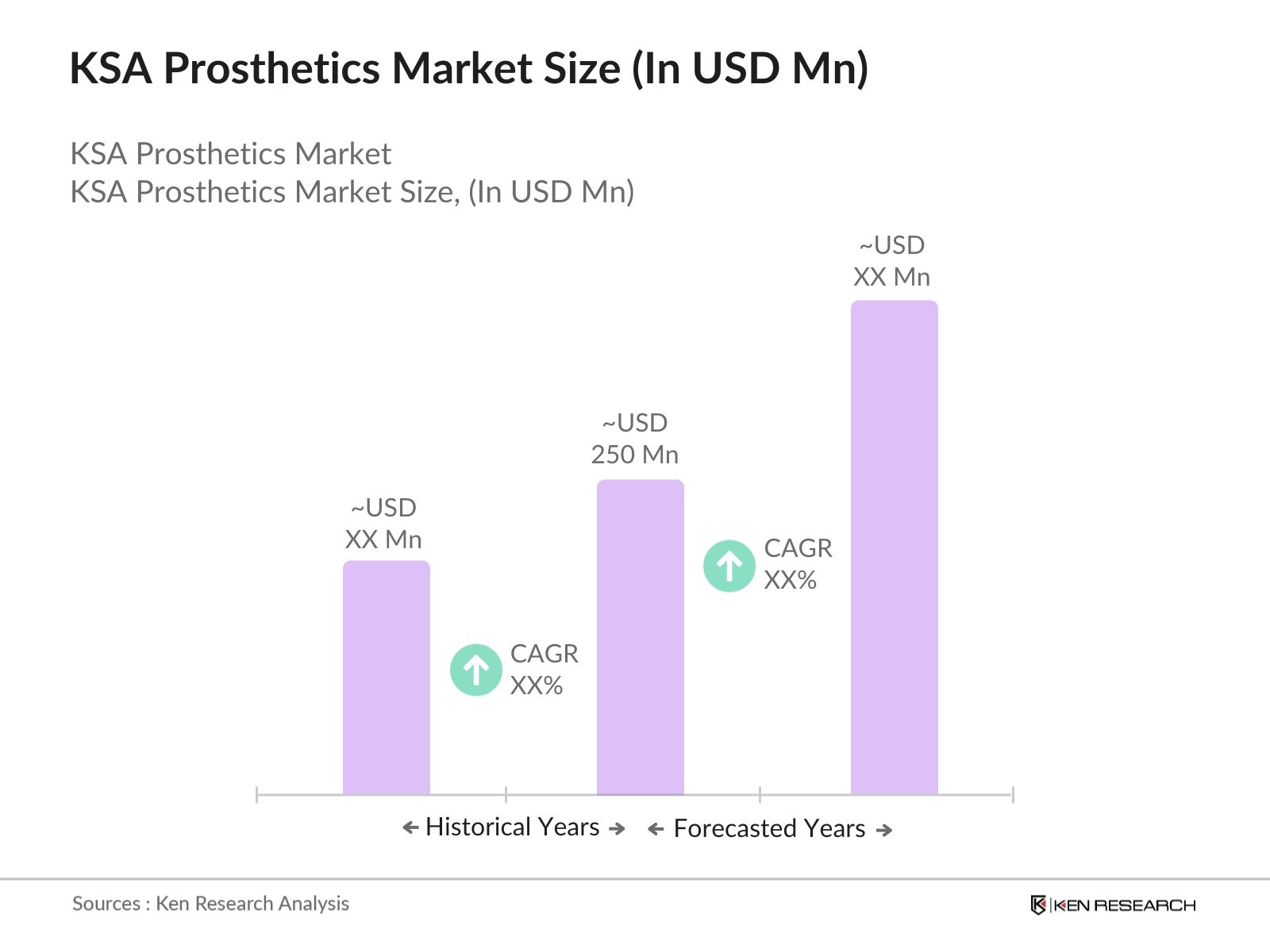

- The KSA prosthetics market, driven by rapid advancements in medical technology and increased healthcare funding, is valued at USD 250 million based on a five-year historical analysis. The surge in demand for prosthetic devices stems from the growing incidence of limb loss due to chronic diseases such as diabetes, as well as accidents and trauma-related amputations.

- The prosthetics market in Saudi Arabia is dominated by Riyadh, Jeddah, and Dammam. These cities have seen substantial healthcare infrastructure investments, creating favorable conditions for prosthetic manufacturing and distribution. Riyadh, being the capital and a medical hub, hosts several specialized clinics, rehabilitation centers, and leading hospitals that cater to amputees and individuals requiring prosthetic care. Jeddah and Dammam have also benefited from their proximity to international markets and high-income populations, further driving the demand for advanced prosthetic solutions.

- The Saudi government launched the National Prosthetics Program in 2022, aiming to provide comprehensive prosthetic care to individuals with limb loss. Under this program, government hospitals and rehabilitation centers are mandated to offer free or subsidized prosthetic devices to citizens. The initiative also includes provisions for advanced prosthetic technologies, such as robotic limbs, ensuring that the latest innovations are accessible to the public. As of 2023, over 3,000 individuals had benefited from the program, with plans to expand the initiative further by 2025.

KSA Prosthetics Market Segmentation

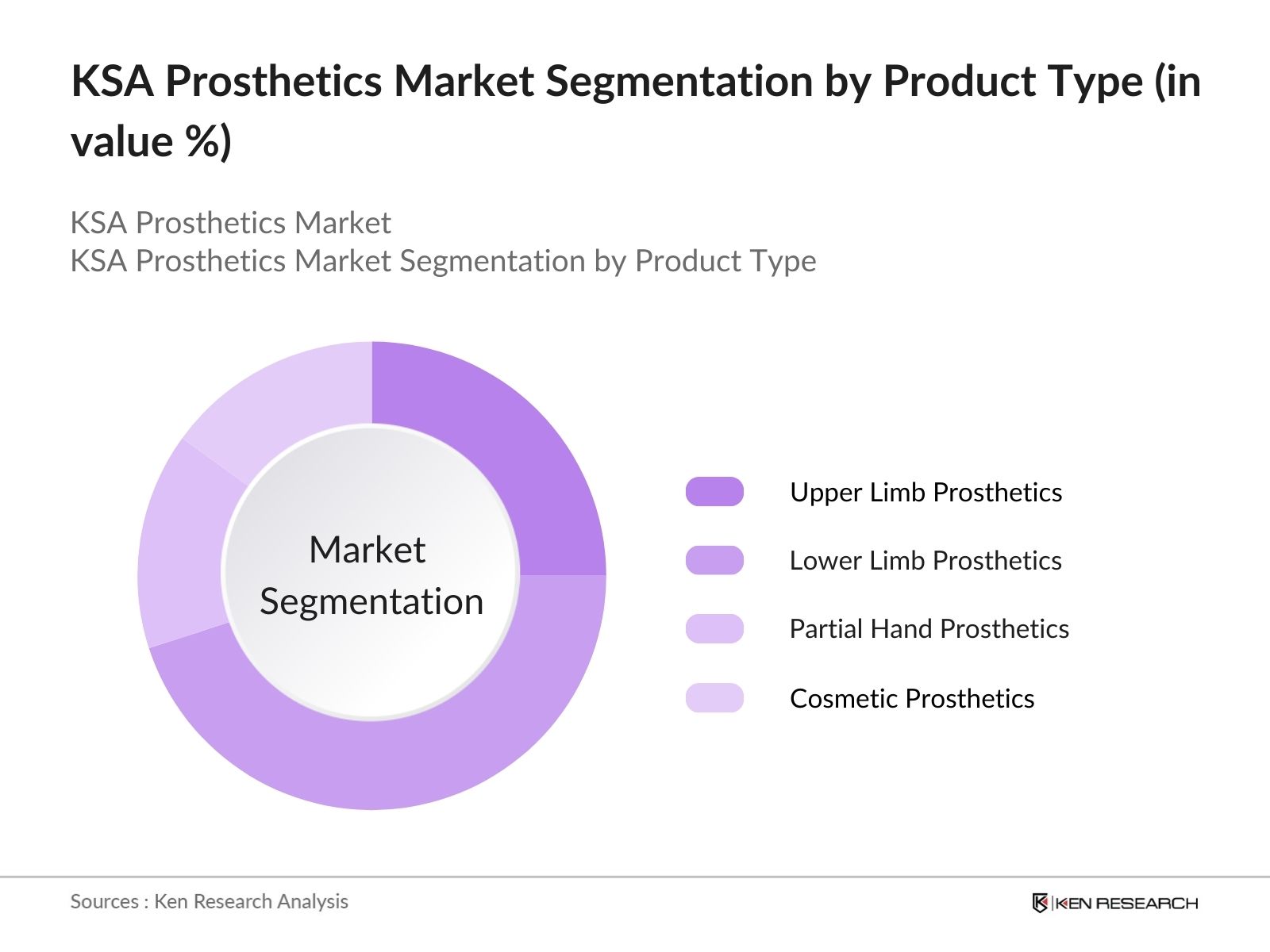

By Product Type: The KSA prosthetics market is segmented by product type into upper limb prosthetics, lower limb prosthetics, partial hand prosthetics, and cosmetic prosthetics. Recently, lower limb prosthetics have dominated the market under the product type segmentation, driven by the high prevalence of diabetes-related amputations. With diabetes being one of the leading causes of limb loss in Saudi Arabia, the demand for lower limb prosthetics has surged, particularly for advanced bionic and myoelectric solutions that offer improved mobility and quality of life for patients.

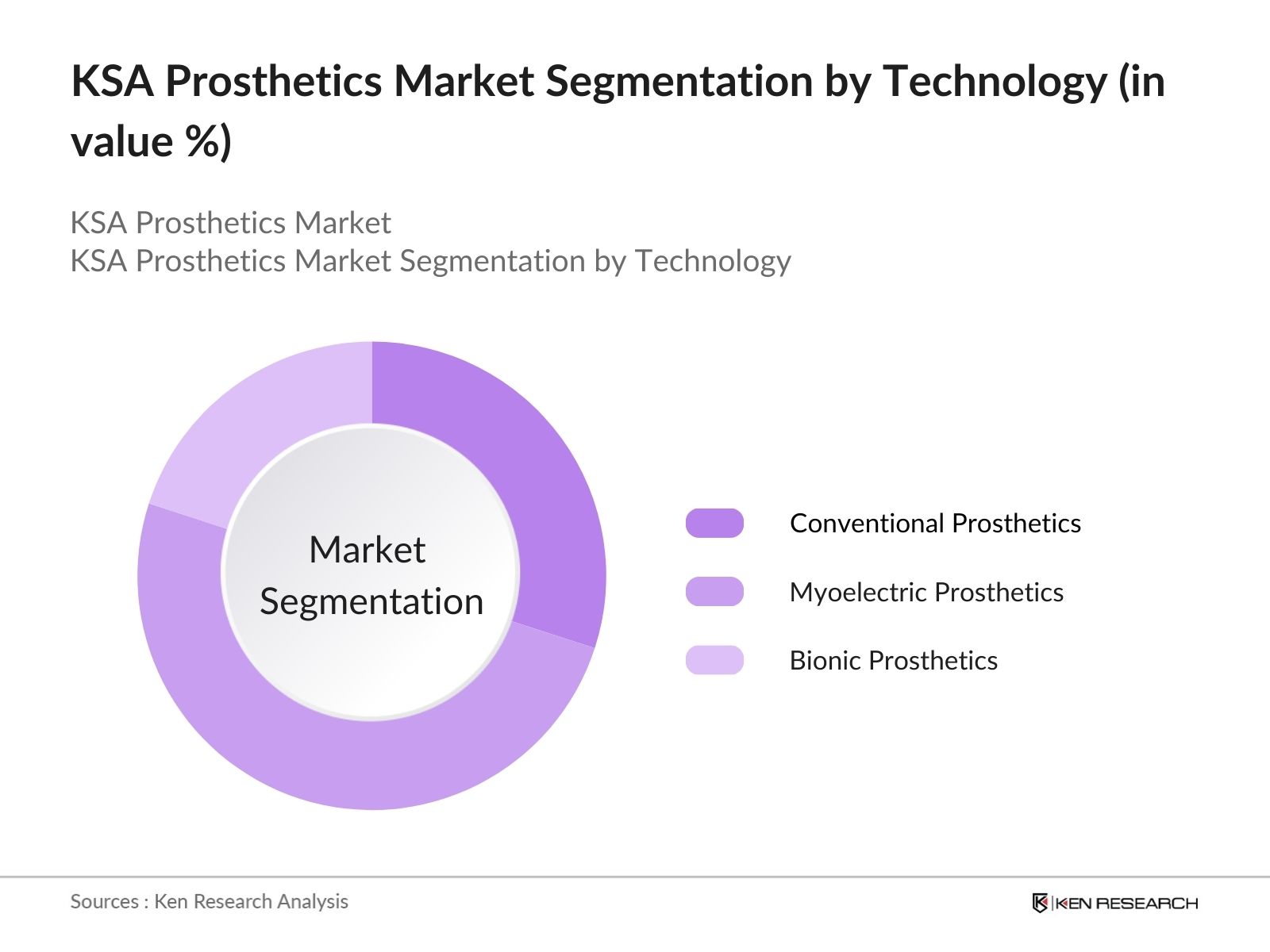

By Technology: The market is segmented by technology into conventional prosthetics, myoelectric prosthetics, and bionic prosthetics. Myoelectric prosthetics currently hold a dominant share in this segment due to their advanced functionality. These devices use electrical signals generated by muscle movements to control the prosthetic limb, offering patients more precision and control compared to conventional options. With a growing preference for high-tech solutions, particularly among younger amputees, the myoelectric prosthetics segment is expected to continue its growth trajectory.

By Technology: The market is segmented by technology into conventional prosthetics, myoelectric prosthetics, and bionic prosthetics. Myoelectric prosthetics currently hold a dominant share in this segment due to their advanced functionality. These devices use electrical signals generated by muscle movements to control the prosthetic limb, offering patients more precision and control compared to conventional options. With a growing preference for high-tech solutions, particularly among younger amputees, the myoelectric prosthetics segment is expected to continue its growth trajectory.

KSA Prosthetics Market Competitive Landscape

KSA Prosthetics Market Competitive Landscape

The KSA prosthetics market is characterized by a mix of global leaders and regional players, all competing for a share of the growing demand. The market is dominated by established companies that have introduced innovative products tailored to meet the specific needs of local consumers, especially in terms of durability and adaptability to the Saudi climate. The competitive landscape of the KSA prosthetics market shows a concentration of well-established global manufacturers with a strong presence in the Middle East, such as ssur and Ottobock.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD) |

Employees |

R&D Investments (USD) |

Product Range |

Partnerships |

Technological Innovations |

Geographic Presence |

|

ssur |

1971 |

Reykjavik, Iceland |

- |

- |

- |

- |

- |

- |

- |

|

Ottobock |

1919 |

Duderstadt, Germany |

- |

- |

- |

- |

- |

- |

- |

|

Blatchford Group |

1890 |

Basingstoke, UK |

- |

- |

- |

- |

- |

- |

- |

|

Fillauer |

1914 |

Chattanooga, USA |

- |

- |

- |

- |

- |

- |

- |

|

Steeper Group |

1921 |

Leeds, UK |

- |

- |

- |

- |

- |

- |

- |

KSA Prosthetics Market Analysis

Growth Drivers

- Increased Prevalence of Limb Loss: Limb amputations due to trauma and diseases such as diabetes are on the rise in Saudi Arabia. In 2022, over 1,500 amputations were reported annually, primarily linked to diabetes and traffic accidents, which is a significant concern given the high prevalence of diabetes (18% of the adult population) and road traffic injuries. This growing rate of amputations is expected to create increased demand for prosthetic devices in the KSA market, as healthcare providers respond to this public health issue.

- Government Initiatives for Healthcare Improvement: Under Saudi Arabia's Vision 2030, the government is focused on enhancing the quality and accessibility of healthcare, which includes initiatives aimed at improving prosthetic care and coverage. As of 2023, more than USD 39.93 billion has been allocated to healthcare infrastructure projects, including the development of rehabilitation centers that support prosthetic services. Expanding insurance coverage for medical devices and procedures, including prosthetics, has become a priority, leading to more widespread access to these essential devices.

- Technological Advancements in Prosthetic Design: Saudi Arabia has seen significant progress in prosthetic technology, with an increasing focus on 3D printing and AI-integrated prosthetic limbs. As of 2024, hospitals in major cities like Riyadh and Jeddah have begun adopting 3D printing technology to create custom-fit prosthetics that reduce manufacturing time and costs. AI-powered prosthetics, capable of mimicking natural limb movement, are also gaining traction, providing better mobility to amputees.

Challenges

- High Costs of Advanced Prosthetics: While Saudi Arabia is making strides in improving access to prosthetics, advanced prosthetic devices remain expensive, with costs ranging between USD 7,989 to USD 26,630, depending on the complexity. For example, robotic prosthetic limbs are particularly costly, often out of reach for many consumers. In addition, insurance coverage for advanced prosthetic devices is not comprehensive, with many insurers only covering basic models.

- Limited Local Manufacturing: Saudi Arabia heavily depends on imported prosthetic devices, with 100% prosthetics coming from international markets as of 2023. This dependency increases costs due to import taxes and currency fluctuations. Moreover, regulatory hurdles make it challenging for local manufacturers to scale domestic production. Although there are initiatives to encourage local manufacturing through tax breaks and subsidies, the lack of established local manufacturers hinders the countrys ability to meet growing demand at an affordable cost.

KSA Prosthetics Market Future Outlook

The KSA prosthetics market is set to experience significant growth in the coming years, driven by advancements in prosthetic technology and increased healthcare funding from the government. As part of Vision 2030, the Kingdom aims to improve healthcare access and quality, which includes the development of specialized rehabilitation centers equipped with the latest prosthetic technologies. This, combined with the growing demand for personalized and custom-fit prosthetics, will likely fuel the markets expansion.

Market Opportunities

- Rising Healthcare Infrastructure Investments: Saudi Arabia has significantly increased investments in healthcare infrastructure as part of Vision 2030, with over USD 133 billion earmarked for hospital expansions and the development of specialized healthcare centers. This includes new rehabilitation centers that cater specifically to individuals in need of prosthetic services. By the end of 2023, at least 10 new rehabilitation centers were planned across major cities, improving access to advanced prosthetics and aftercare services.

- Emerging Markets for Low-Cost Prosthetics: As part of its healthcare reforms, Saudi Arabia is investing in localized manufacturing of low-cost prosthetics to meet growing demand. In 2023, the government announced new subsidies and tax incentives for local manufacturers to produce affordable prosthetic devices, targeting low-income patients. The rise of local production could decrease the dependency on costly imports while ensuring wider availability of prosthetics.

Scope of the Report

|

Segments |

Sub-Segments |

|

By Product Type |

Upper Limb Prosthetics Lower Limb Prosthetics Partial Hand Prosthetics Cosmetic Prosthetics |

|

By Technology |

Conventional Prosthetics Myoelectric Prosthetics Bionic Prosthetics |

|

By Material |

Carbon Fiber Plastic Metal Alloys Silicone |

|

By Application |

Trauma Congenital Conditions Disease-Related Amputations |

|

By End-User |

Hospitals Rehabilitation Centers Prosthetic Clinics |

Products

Key Target Audience

Hospitals and healthcare institutions

Rehabilitation centers

Prosthetic manufacturers and suppliers

Insurance providers

Disability support organizations

Investors and venture capitalist firms

Government and regulatory bodies (Saudi Food and Drug Authority)

Companies

Players Mentioned in the Report

ssur

Ottobock

Blatchford Group

Fillauer

Steeper Group

Touch Bionics (A part of ssur)

WillowWood Global LLC

Advanced Arm Dynamics

Proteor

RSLSteeper

Table of Contents

1. KSA Prosthetics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. KSA Prosthetics Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. KSA Prosthetics Market Analysis

3.1. Growth Drivers

3.1.1. Increased prevalence of limb loss (Amputation rates, Trauma and disease-related amputations)

3.1.2. Government initiatives for healthcare improvement (Health Insurance expansions, Vision 2030 health objectives)

3.1.3. Technological advancements in prosthetic design (3D printing, AI-based smart prosthetics)

3.1.4. Growing awareness of prosthetic devices (Public awareness campaigns, Disability support initiatives)

3.2. Market Challenges

3.2.1. High costs of advanced prosthetics (Cost barriers for consumers, Lack of insurance coverage)

3.2.2. Limited local manufacturing (Dependency on imports, Regulatory challenges for domestic production)

3.2.3. Technical skill gap in prosthetic fitting and customization (Need for trained professionals, Underdeveloped rehabilitation services)

3.3. Opportunities

3.3.1. Rising healthcare infrastructure investments (Hospital expansions, New rehabilitation centers)

3.3.2. Emerging markets for low-cost prosthetics (Government subsidies, Localized manufacturing efforts)

3.3.3. Partnerships with global prosthetic manufacturers (International collaborations, Joint ventures)

3.4. Trends

3.4.1. Adoption of bionic prosthetics (Robotic limb technologies, AI-driven motion control)

3.4.2. Use of advanced materials (Carbon fiber, Lightweight alloys, Biodegradable prosthetics)

3.4.3. Customization and personalized prosthetics (3D-printed prosthetic limbs, Custom-fit designs)

3.5. Government Regulation

3.5.1. National Prosthetics Program

3.5.2. Medical Device Regulatory Framework

3.5.3. Import duties and taxation on medical devices

3.5.4. Public-Private Partnerships in the healthcare sector

3.6. SWOT Analysis

3.6.1. Strengths

3.6.2. Weaknesses

3.6.3. Opportunities

3.6.4. Threats

3.7. Stakeholder Ecosystem (Manufacturers, Distributors, Healthcare providers, Government entities)

3.8. Porters Five Forces

3.8.1. Supplier Power

3.8.2. Buyer Power

3.8.3. Threat of Substitutes

3.8.4. Threat of New Entrants

3.8.5. Industry Rivalry

3.9. Competition Ecosystem

4. KSA Prosthetics Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Upper Limb Prosthetics

4.1.2. Lower Limb Prosthetics

4.1.3. Partial Hand Prosthetics

4.1.4. Cosmetic Prosthetics

4.2. By Technology (In Value %)

4.2.1. Conventional Prosthetics

4.2.2. Myoelectric Prosthetics

4.2.3. Bionic Prosthetics

4.3. By Material (In Value %)

4.3.1. Carbon Fiber

4.3.2. Plastic

4.3.3. Metal Alloys

4.3.4. Silicone

4.4. By Application (In Value %)

4.4.1. Trauma

4.4.2. Congenital Conditions

4.4.3. Disease-Related Amputations (Diabetes, Vascular disease)

4.5. By End-User (In Value %)

4.5.1. Hospitals

4.5.2. Rehabilitation Centers

4.5.3. Prosthetic Clinics

5. KSA Prosthetics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. ssur

5.1.2. Ottobock

5.1.3. Blatchford Group

5.1.4. Fillauer

5.1.5. Steeper Group

5.1.6. Touch Bionics (A part of ssur)

5.1.7. WillowWood Global LLC

5.1.8. Advanced Arm Dynamics

5.1.9. Proteor

5.1.10. RSLSteeper

5.2. Cross Comparison Parameters (Revenue, R&D Investments, Product Portfolio, Technological Innovation, Geographic Presence, Manufacturing Capacity, Customer Base, Local Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6. KSA Prosthetics Market Regulatory Framework

6.1. Licensing Requirements

6.2. Compliance with Saudi FDA (Saudi Food and Drug Authority) Standards

6.3. Certification Processes

6.4. Import and Export Regulations

7. KSA Prosthetics Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. KSA Prosthetics Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Technology (In Value %)

8.3. By Material (In Value %)

8.4. By Application (In Value %)

8.5. By End-User (In Value %)

9. KSA Prosthetics Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase involves mapping all major stakeholders in the KSA prosthetics market through extensive desk research and the use of proprietary databases. The goal is to identify the key variables affecting the market, including healthcare spending, technological advancements, and government policies.

Step 2: Market Analysis and Construction

Historical data is compiled to analyze the market dynamics of the KSA prosthetics market, focusing on the ratio of amputees to service providers, and revenue generation in the prosthetic manufacturing sector. Service quality metrics are also evaluated to ensure the reliability of market data.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through interviews with industry experts, including prosthetists and healthcare providers, to gain insight into market trends and technological innovations. These consultations help refine the gathered data and ensure accuracy.

Step 4: Research Synthesis and Final Output

In the final stage, direct engagement with prosthetic manufacturers is conducted to obtain detailed insights into sales performance, customer preferences, and emerging technologies. This data, validated through the bottom-up approach, ensures a comprehensive understanding of the market.

Frequently Asked Questions

01. How big is the KSA Prosthetics Market?

The KSA prosthetics market is valued at USD 250 million, driven by increasing demand for advanced prosthetic solutions, particularly for lower limb amputations caused by diabetes and trauma-related injuries.

02. What are the challenges in the KSA Prosthetics Market?

Challenges in the KSA prosthetics market include high costs of advanced prosthetics, a lack of skilled professionals to fit and customize prosthetics, and limited local manufacturing capabilities, leading to a dependency on imported products.

03. Who are the major players in the KSA Prosthetics Market?

Key players in the KSA prosthetics market include global manufacturers such as ssur, Ottobock, Blatchford Group, Fillauer, and Steeper Group. These companies dominate the market due to their technological innovations and comprehensive product offerings.

04. What are the growth drivers of the KSA Prosthetics Market?

The KSA prosthetics market is driven by the increasing prevalence of chronic diseases like diabetes, which leads to amputations, and government healthcare initiatives that improve access to prosthetic devices. Technological advancements such as bionic and AI-powered prosthetics also contribute to market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.