KSA Pulp and Paper Market Outlook to 2030

Region:Saudi Arabia

Author(s):Meenakshi Bisht

Product Code:KROD5496

Region:Saudi Arabia

Author(s):Meenakshi Bisht

Product Code:KROD5496

December 2024

85

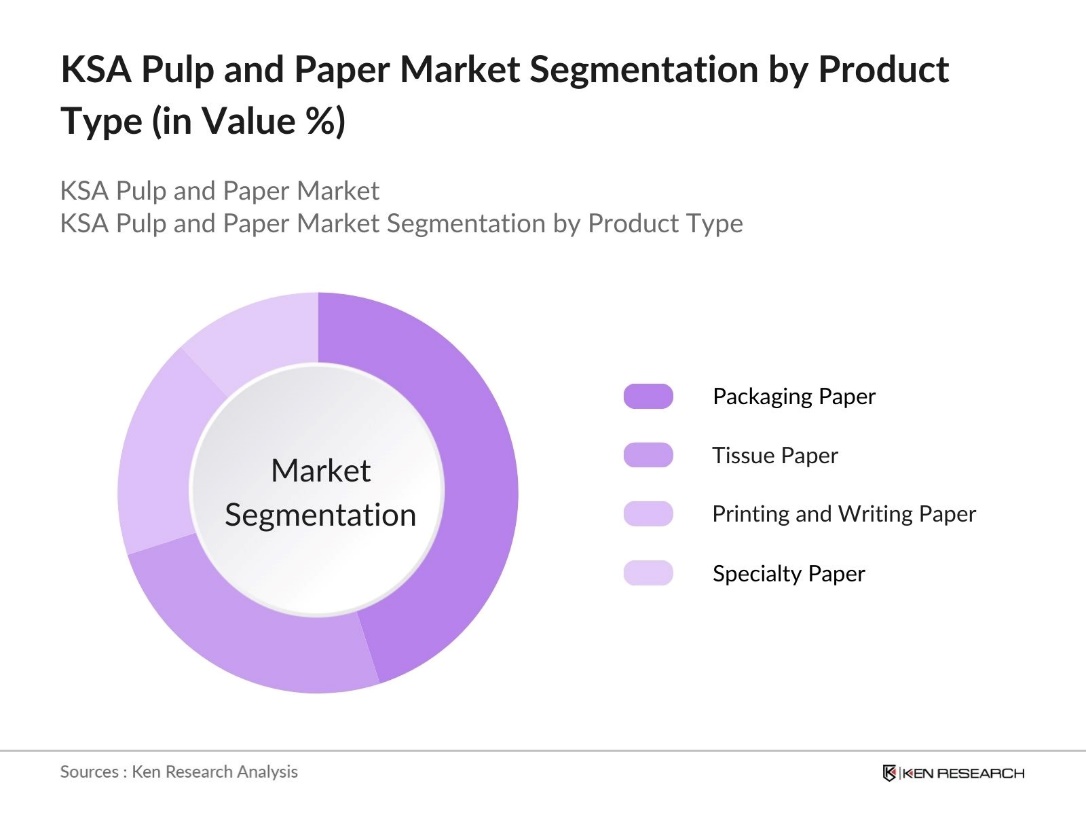

By Product Type: The KSA Pulp and Paper market is segmented by product type into packaging paper, tissue paper, printing and writing paper, and specialty paper. Among these, packaging paper holds the largest market share in the product type segment due to the growing demand for corrugated boxes, cartons, and flexible packaging. This demand is largely attributed to the expanding e-commerce sector, industrial growth, and food packaging needs in Saudi Arabia. Sustainable packaging has further enhanced the dominance of this sub-segment, as industries shift towards eco-friendly solutions.

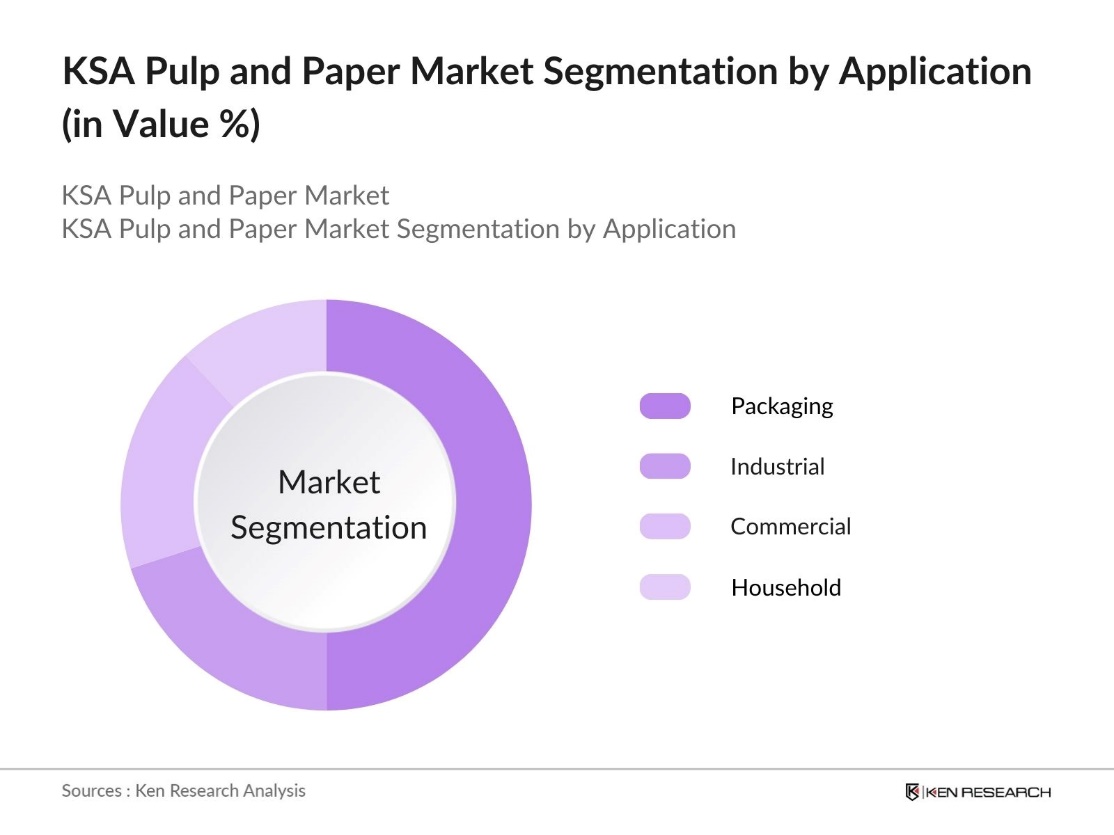

By Application: The KSA Pulp and Paper market is also segmented by application into industrial, commercial, household, and packaging. The packaging segment is dominant due to the increased focus on both consumer and industrial packaging, driven by the food and beverage industry, logistics, and retail sectors. Packaging applications are gaining traction due to sustainability efforts, particularly in single-use and recyclable packaging, which are supported by government policies promoting environmental protection.

The market is dominated by several major companies that have established strong local manufacturing capabilities and distribution networks. The competitive landscape reflects a blend of local manufacturers and international players, highlighting significant investments in technology and sustainable production.

|

Company |

Establishment Year |

Headquarters |

Production Capacity (tons) |

No. of Employees |

Export Capability |

Technological Integration |

Sustainability Certifications |

|

Saudi Paper Manufacturing Co. |

1989 |

Dammam |

|||||

|

Al-Jazira Paper Factory |

1986 |

Riyadh |

|||||

|

United Carton Industries Co. |

1990 |

Jeddah |

|||||

|

Waraq Paper Manufacturing Co. |

1979 |

Riyadh |

|||||

|

Napco National |

1956 |

Al Khobar |

The KSA Pulp and Paper market is expected to experience significant growth over the next five years, driven by the expanding industrial base, rapid urbanization, and a growing focus on sustainable packaging solutions. Government regulations aimed at promoting environmental sustainability and the increased adoption of recycling technologies will further contribute to the industry's upward trajectory. Additionally, technological advancements such as digital printing and automation in paper production processes are likely to enhance operational efficiencies and reduce costs.

|

Product Type |

Printing and Writing Paper Packaging Paper and Board Specialty Paper Tissue Paper |

|

Application |

Industrial Commercial Household Packaging |

|

Raw Material |

Wood Pulp Recycled Paper Non-Wood Fiber (Bagasse, Bamboo) |

|

Manufacturing Process |

Mechanical Pulping Chemical Pulping Recycled Fiber Pulping |

|

Region |

Riyadh Jeddah Dammam Makkah |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Industry Expansion Rate, Key Market Trends)

1.4. Market Segmentation Overview (by Type, Application, End-Use, and Region)

2.1. Historical Market Size (by Volume and Value)

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Industry Shifts, Technological Innovations, and Key Stakeholder Initiatives)

3.1. Growth Drivers

3.1.1. Demand for Sustainable Packaging

3.1.2. Government Initiatives for Environmental Sustainability

3.1.3. Rising Paper Recycling Efforts

3.1.4. Expanding Industrial Applications (Construction, Printing, Packaging)

3.2. Market Challenges

3.2.1. High Raw Material Costs (Wood Pulp, Recycled Paper)

3.2.2. Water Usage Regulations

3.2.3. Competition from Digital Media (Reduced Paper Demand in Publishing)

3.2.4. Supply Chain Bottlenecks

3.3. Opportunities

3.3.1. Expansion of Corrugated Packaging in E-commerce

3.3.2. Growth in Tissue Paper Products (Increased Hygiene Awareness)

3.3.3. Increased Export Opportunities (Rising Global Demand for Packaging Materials)

3.4. Trends

3.4.1. Adoption of Digital Printing Technologies

3.4.2. Growing Use of Biodegradable and Recycled Paper Products

3.4.3. Automation in Manufacturing Processes (Reducing Production Costs)

3.4.4. Shift Towards Lightweight Paper Grades (Energy Conservation)

3.5. Government Regulation

3.5.1. Environmental Protection Laws (Water Usage, Emission Standards)

3.5.2. National Recycling Programs

3.5.3. Import Tariffs on Pulp and Paper Materials

3.5.4. Support for Local Manufacturers (Subsidies, Tax Incentives)

3.6. SWOT Analysis

3.6.1. Strengths (Local Production Capacity, Government Support)

3.6.2. Weaknesses (Dependence on Imported Raw Materials)

3.6.3. Opportunities (Regional Trade Agreements, Technological Advancements)

3.6.4. Threats (Global Market Volatility, Environmental Pressures)

3.7. Stakeholder Ecosystem (Suppliers, Manufacturers, Distributors, End-users)

3.8. Porters Five Forces Analysis (Bargaining Power of Suppliers, Buyers, Competitive Rivalry, etc.)

3.9. Competition Ecosystem (Market Share Distribution, Key Players Positioning)

4.1. By Product Type (In Value %)

4.1.1. Printing and Writing Paper

4.1.2. Packaging Paper and Board

4.1.3. Specialty Paper

4.1.4. Tissue Paper

4.2. By Application (In Value %)

4.2.1. Industrial

4.2.2. Commercial

4.2.3. Household

4.2.4. Packaging

4.3. By Raw Material (In Value %)

4.3.1. Wood Pulp

4.3.2. Recycled Paper

4.3.3. Non-Wood Fiber (Bagasse, Bamboo)

4.4. By Manufacturing Process (In Value %)

4.4.1. Mechanical Pulping

4.4.2. Chemical Pulping

4.4.3. Recycled Fiber Pulping

4.5. By Region (In Value %)

4.5.1. Riyadh

4.5.2. Jeddah

4.5.3. Dammam

4.5.4. Makkah

5.1. Detailed Profiles of Major Companies

5.1.1. Saudi Paper Manufacturing Co.

5.1.2. Al-Jazira Paper Factory

5.1.3. United Carton Industries Co.

5.1.4. Waraq Paper Manufacturing Co.

5.1.5. Middle East Paper Co. (MEPCO)

5.1.6. Obeikan Paper Industries

5.1.7. Fipco

5.1.8. Napco National

5.1.9. Gulf Carton Factory

5.1.10. Green Pulp Paper Industry

5.1.11. Gulf Packaging Industries

5.1.12. GPC Group

5.1.13. Zamil Paper Industries

5.1.14. Hotpack Global

5.1.15. Al Suwaidi Paper Co.

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Revenue, Production Capacity, Raw Material Usage, Market Penetration, Technological Integration, Environmental Certifications)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Sustainability Initiatives, R&D Investments, Digitalization Strategies)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Local and International Investments in the Industry)

5.7. Venture Capital and Private Equity Investments

5.8. Government Grants and Subsidies

6.1. Environmental Standards (Water Usage, Emissions)

6.2. Compliance Requirements (Sustainability Certifications, Safety Protocols)

6.3. Certification Processes (ISO Certifications, Environmental Management Standards)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Urbanization, Export Demand, and Technological Advancements)

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Raw Material (In Value %)

8.4. By Manufacturing Process (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial stage involves defining key factors influencing the KSA Pulp and Paper market. Extensive research, utilizing industry reports, government publications, and proprietary data sources, is used to identify market drivers, challenges, and emerging trends. The objective is to map the entire market ecosystem comprehensively.

In this phase, historical market data is compiled and analyzed to assess the market's current state. This includes understanding key demand factors, price fluctuations, and technological adoption trends, ensuring a precise view of market dynamics.

Hypotheses regarding market trends, pricing, and consumption are validated through expert interviews and consultations. These interviews with industry professionals provide critical insights into operational practices, market challenges, and technological innovations, reinforcing the market analysis.

In the final stage, all findings are synthesized into a cohesive report, covering market size, growth projections, segmentation, and competitive analysis. A combination of top-down and bottom-up approaches ensures that the data is accurate and reflective of real-world market dynamics.

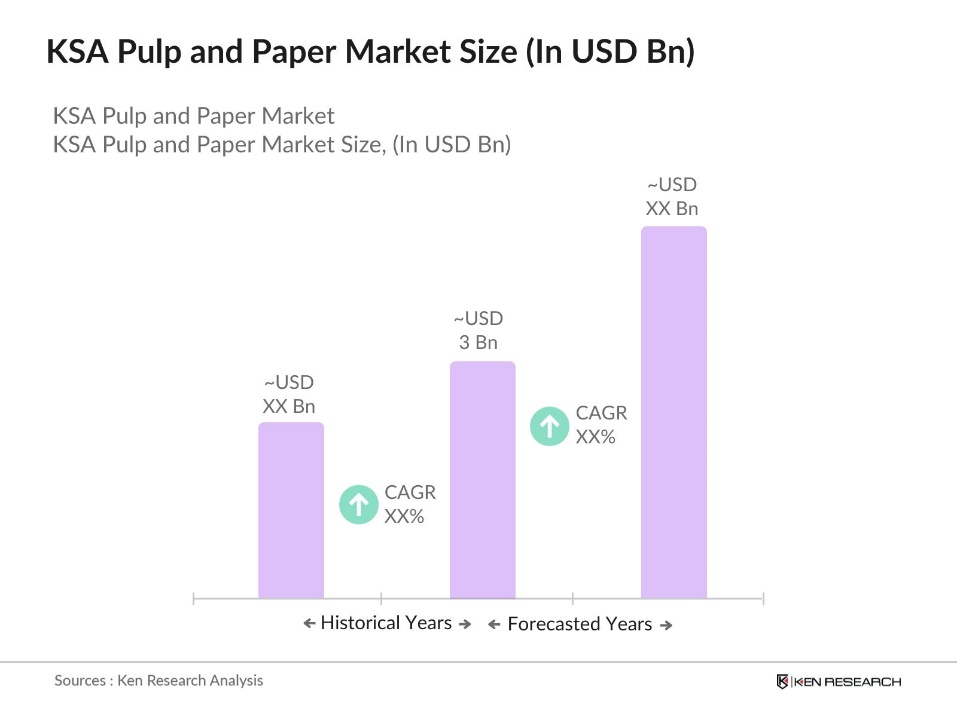

The KSA Pulp and Paper Market is valued at USD 3 billion, driven by rising demand in industrial packaging, consumer goods, and growing e-commerce activities.

Challenges in KSA Pulp and Paper Market include the rising cost of raw materials such as wood pulp, compliance with environmental regulations, and competition from alternative packaging materials like plastics and metals.

Key players in KSA Pulp and Paper Market include Saudi Paper Manufacturing Co., Al-Jazira Paper Factory, United Carton Industries Co., Waraq Paper Manufacturing Co., and Napco National, each contributing significantly to local and export markets.

The KSA Pulp and Paper Market is driven by factors such as increased industrialization, government support for sustainable packaging, and the growing use of recycled materials in the packaging industry.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.