KSA PV Inverter Market Outlook to 2030

Region:Middle East

Author(s):Sanjeev

Product Code:KROD4558

December 2024

88

About the Report

KSA PV Inverter Market Overview

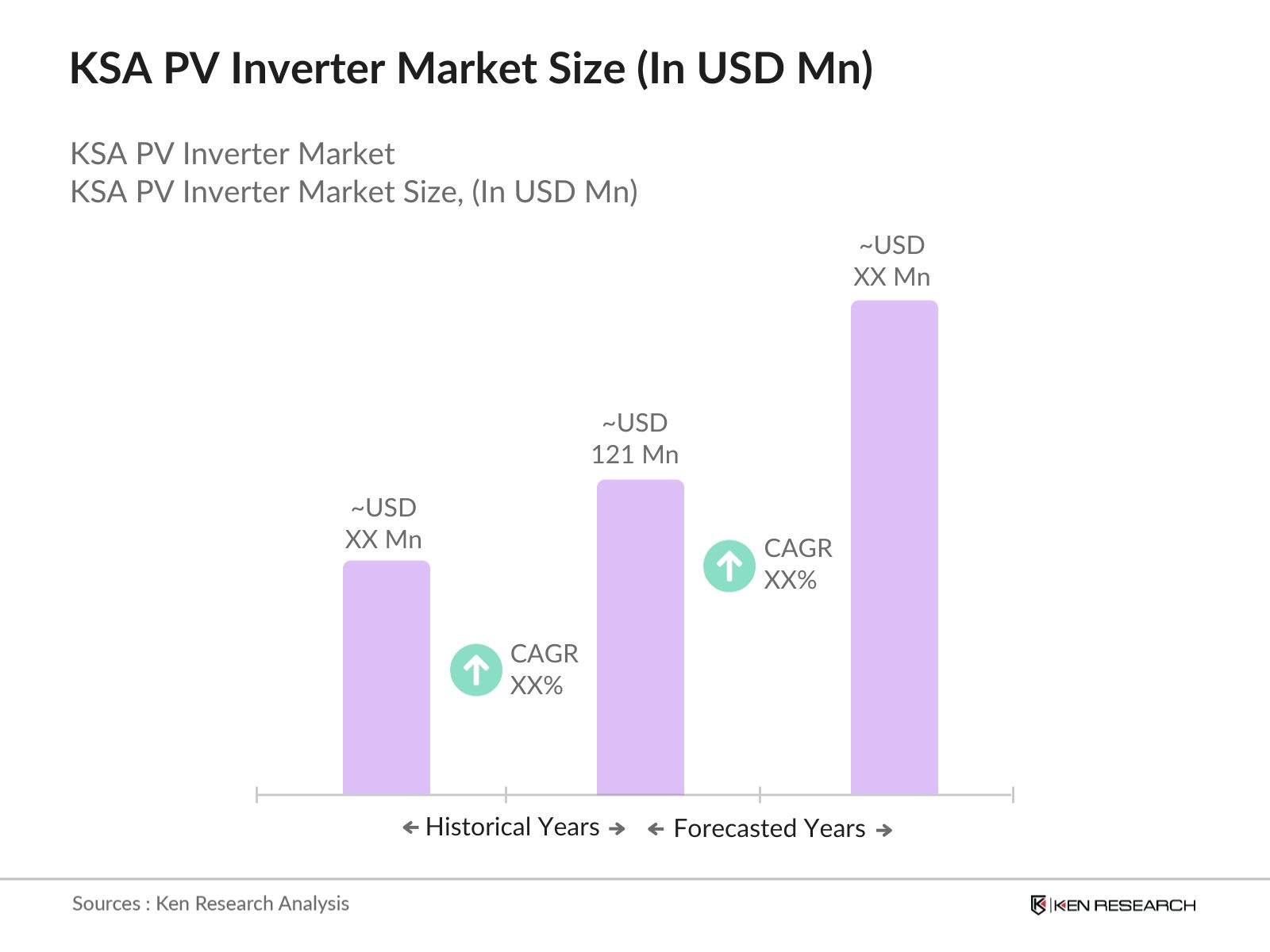

- The KSA PV inverter market is valued at USD 121 million, driven by the Kingdoms aggressive push towards renewable energy, particularly solar power as part of Vision 2030. The market has seen growth due to government policies encouraging solar energy adoption across residential, commercial, and utility sectors. This growth is also fueled by cost reductions in solar technology and increasing awareness of clean energy benefits.

- In terms of dominance, Riyadh and the Eastern Province lead the market. These regions are pivotal due to their high levels of urbanization, strong industrial bases, and a high concentration of energy projects. The proximity of these regions to major infrastructure and grid networks makes them favorable for large-scale solar power installations, positioning them as key drivers of the markets expansion.

- Saudi Arabias Renewable Energy Law, implemented in 2022, has established a clear legal framework for renewable energy investments, setting specific guidelines for PV installations and equipment standards. This law encourages foreign investments in the solar sector, leading to an influx of projects, including the requirement for certified PV inverters that comply with the nation's renewable energy regulations. These legal frameworks have enhanced market transparency and regulatory certainty, benefiting the PV inverter industry.

KSA PV Inverter Market Segmentation

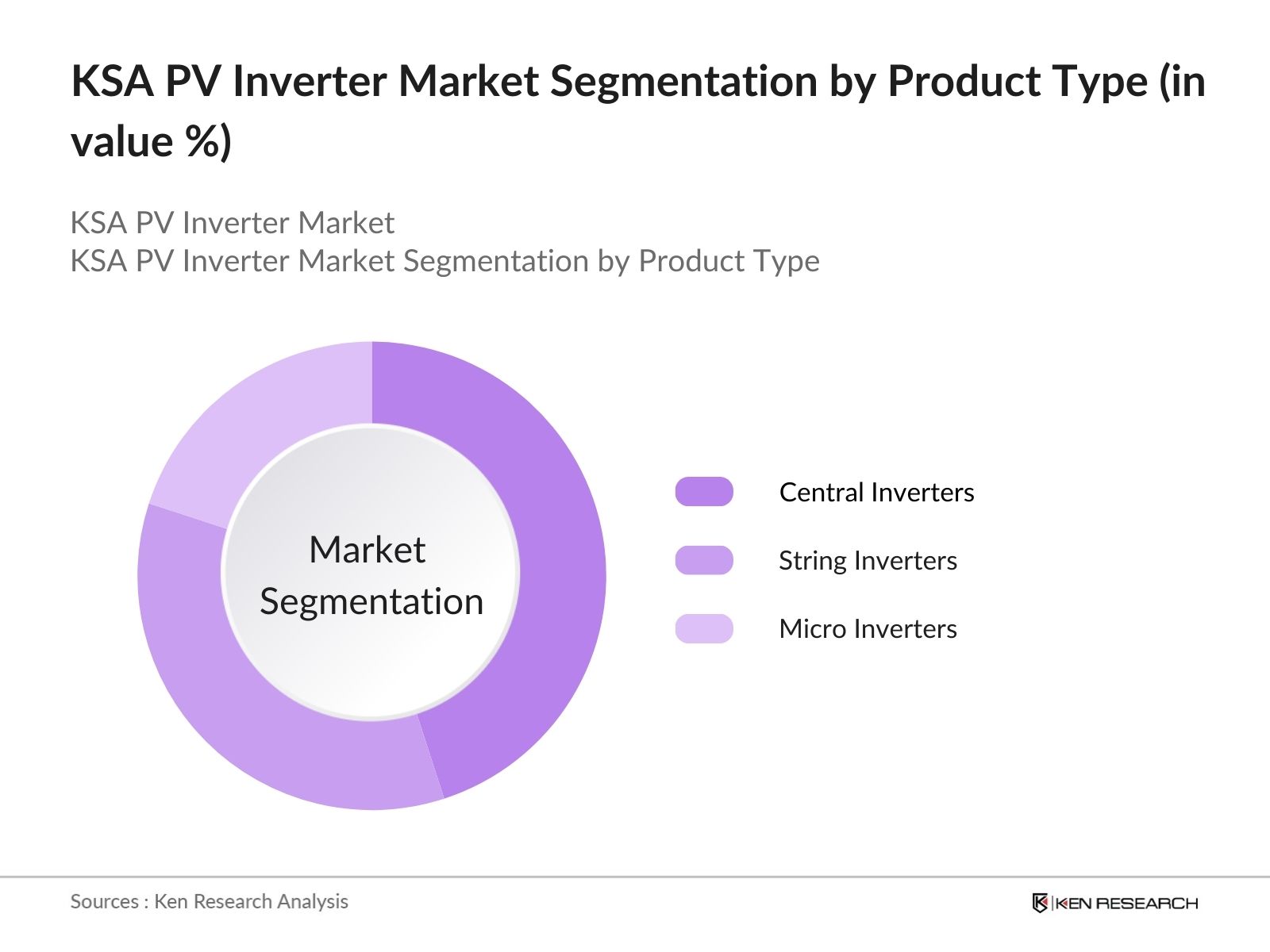

- By Product Type: The market is segmented by product type into central inverters, string inverters, and micro inverters. Recently, central inverters have dominated the market due to their suitability for large-scale utility projects. Their high capacity and efficiency make them a preferred choice for utility-scale solar farms, particularly in regions like Riyadh, where large commercial projects are more common. Central inverters provide better grid stability and lower maintenance costs, further enhancing their dominance in the market.

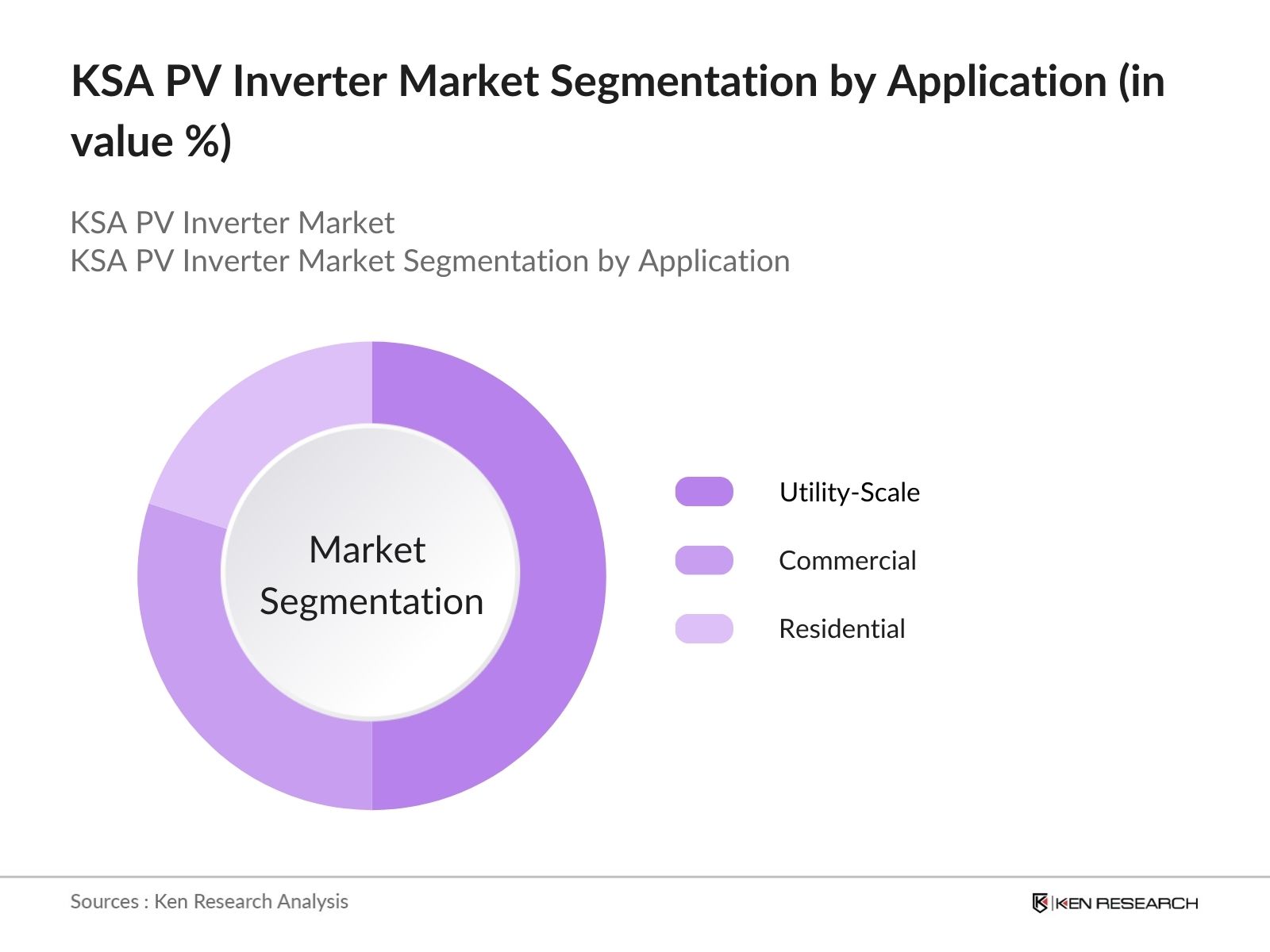

- By Application: The market is segmented by application into residential, commercial, and utility-scale projects. Utility-scale projects hold a dominant market share due to government-sponsored large solar farms aimed at meeting energy demand and diversifying the energy mix. These large installations are often supported by central inverters, which align with the governments renewable energy targets.

KSA PV Inverter Industry Competitive Landscape

The KSA PV inverter market is dominated by a few global players who have a presence due to their technology and capacity to support large solar projects. Companies like Huawei and SMA Solar Technology dominate due to their expertise in central inverters and their ability to meet the large demand from utility-scale projects. Local companies have also started entering the market but face stiff competition from established international players.

|

Company Name |

Year of Establishment |

Headquarters |

Product Portfolio |

Revenue (USD Mn) |

Inverter Efficiency |

Global Market Presence |

Key Projects in KSA |

|

Huawei Technologies Co. |

1987 |

Shenzhen, China |

|||||

|

SMA Solar Technology AG |

1981 |

Niestetal, Germany |

|||||

|

ABB Ltd. |

1988 |

Zurich, Switzerland |

|||||

|

Sungrow Power Supply Co. |

1997 |

Hefei, China |

|||||

|

Fronius International GmbH |

1945 |

Pettenbach, Austria |

KSA PV Inverter Industry Analysis

Growth Drivers

- Vision 2030 Renewable Energy Initiatives: Saudi Arabia's Vision 2030 sets a target of generating 58.7 GW of renewable energy by 2030, with solar energy contributing 40 GW. As of 2023, the Kingdom's solar capacity stands at 2.1 GW, reflecting strong momentum in solar projects across the nation. The development of projects like the Sudair Solar PV plant, which will have an installed capacity of 1.5 GW, highlights Saudi Arabia's aggressive push toward solar energy adoption, which directly increases demand for PV inverters. This policy-driven expansion of renewable energy significantly supports the PV inverter market.

- Increasing Demand for Clean Energy: The rising demand for clean energy in Saudi Arabia stems from the Kingdom's goal of reducing oil dependency, and transitioning to renewable sources is critical. By 2023, over 3.2 million MWh of electricity was generated from solar energy, contributing significantly to the energy mix. This shift has increased the adoption of solar PV systems, boosting the demand for PV inverters, particularly in the commercial and utility sectors. The push towards meeting the Vision 2030 targets continues to drive this demand upwards, indicating sustained market growth.

- Reductions in PV Inverter Costs: PV inverter prices have dropped considerably over the last decade, largely due to technological advancements and increased production scale. By 2024, the cost of PV inverters is expected to be 15% lower than in 2019, making solar energy systems more accessible to a wider range of consumers. This cost reduction allows commercial and utility-scale solar projects to benefit from enhanced return on investment, thereby fostering greater adoption. The decrease in capital expenditure has been a key growth driver for solar installations, benefiting the PV inverter market.

Market Challenges

- High Initial Capital Requirements: Despite the reduction in inverter costs, the initial capital investment for solar projects remains high in Saudi Arabia. A large commercial solar project in 2023 required an estimated $120 million for infrastructure, which includes PV inverters and related components. This high upfront cost has posed challenges for smaller enterprises and residential consumers in accessing solar solutions, thus limiting the market's growth potential. Financial support mechanisms remain essential for the broader adoption of solar technologies.

- Technical Integration Issues with Grid: Grid integration remains a challenge for solar power in Saudi Arabia, particularly for PV systems at the utility scale. In 2023, technical issues during the integration of 1 GW of solar power into the grid led to inefficiencies and downtime, impacting electricity distribution. These challenges arise from mismatches in energy storage capabilities, voltage regulation, and grid stability, all of which require advanced PV inverters capable of managing variability in power output.

KSA PV Inverter Market Future Outlook

Over the next five years, the KSA PV inverter market is expected to show significant growth driven by government initiatives such as Vision 2030, technological advancements in solar inverters, and increasing investment in large-scale utility projects. The rise of smart inverters integrated with energy storage systems will further drive the market, alongside local manufacturing efforts to reduce dependency on imports.

Future Market Opportunities

- Increase in Energy Storage Systems Integration: The integration of energy storage systems (ESS) with solar PV installations has become a crucial opportunity for the PV inverter market. In 2023, the total energy storage capacity tied to solar systems in Saudi Arabia reached 150 MWh, a significant increase from 90 MWh in 2022. The demand for hybrid inverters, which combine solar PV with energy storage capabilities, is expected to rise as more grid operators adopt ESS to stabilize electricity supply, thus providing an additional growth avenue for PV inverter manufacturers.

- Rise of Hybrid Inverter Systems: Hybrid inverters, which allow for both grid and battery storage connections, are seeing growing demand in Saudi Arabia. In 2023, over 25% of newly installed PV systems in commercial projects incorporated hybrid inverters, reflecting an increasing trend toward decentralized energy systems. These inverters provide flexibility in managing energy loads and optimizing power usage, making them attractive for both residential and commercial installations. This shift presents a lucrative opportunity for companies manufacturing advanced inverter solutions.

Scope of the Report

| By Product Type | Central Inverters String Inverters Micro Inverters |

| By Application | Residential Commercial Utility-Scale |

| By Technology | On-Grid Inverters Off-Grid Inverters Hybrid Inverters |

| By Phase | Single-Phase Three-Phase |

| By Region | North East West South |

Products

Key Target Audience

Solar PV Installation Companies

Renewable Energy Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Saudi Ministry of Energy, SASO)

Utility Providers and Energy Distributors

Banks and Financial Institutes

Solar Component Manufacturers

Engineering, Procurement, and Construction (EPC) Contractors

Residential and Commercial Property Developers

Solar Energy Consultants and Project Managers

Companies

List of Major Players in the KSA PV Inverter Market

Huawei Technologies Co.

SMA Solar Technology AG

ABB Ltd.

Sungrow Power Supply Co., Ltd.

Fronius International GmbH

Delta Electronics, Inc.

Schneider Electric SE

Fimer S.p.A.

Solis Inverters

GoodWe Power Supply Technology Co., Ltd.

Power Electronics S.L.

TBEA Sunoasis Co., Ltd.

Kaco New Energy GmbH

Enphase Energy

Ginlong Technologies Co., Ltd.

Table of Contents

1. KSA PV Inverter Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy (Types of PV Inverters, Installation Modes)

1.3. Market Growth Rate (MW Capacity Installed, Percentage Growth)

1.4. Market Segmentation Overview (Residential, Commercial, Utility-Scale)

2. KSA PV Inverter Market Size (In SAR Mn)

2.1. Historical Market Size (Installation Capacity and Revenue)

2.2. Year-On-Year Growth Analysis (MW and SAR Mn)

2.3. Key Market Developments and Milestones (Installation Capacity in Key Regions)

3. KSA PV Inverter Market Analysis

3.1. Growth Drivers (Solar Capacity Expansion Targets, Government Energy Policies)

3.1.1. Vision 2030 Renewable Energy Initiatives

3.1.2. Increasing Demand for Clean Energy

3.1.3. Reductions in PV Inverter Costs

3.1.4. Expansion in Commercial and Utility Sectors

3.2. Market Challenges (Grid Integration, Supply Chain Disruptions)

3.2.1. High Initial Capital Requirements

3.2.2. Technical Integration Issues with Grid

3.2.3. Lack of Domestic Manufacturing

3.3. Opportunities (Technological Innovations, Local Production Incentives)

3.3.1. Increase in Energy Storage Systems Integration

3.3.2. Rise of Hybrid Inverter Systems

3.3.3. Expansion of Solar Rooftop Installations in Residential Sectors

3.4. Trends (Hybrid Inverters, Smart PV Systems)

3.4.1. Rise of AI-Driven Energy Management Systems

3.4.2. Growth in Demand for Three-Phase Inverters for Utility Projects

3.4.3. Integration with IoT for Enhanced Monitoring

3.5. Government Regulation (Government Tenders, Local Content Requirements)

3.5.1. Renewable Energy Law

3.5.2. Saudi Arabian Standards Organization (SASO) PV Inverter Standards

3.5.3. Energy Efficiency Initiatives in PV Inverters

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Manufacturers, Distributors, EPCs)

3.8. Porters Five Forces (Competitive Rivalry, Supplier and Buyer Power, Substitution, New Entrants)

3.9. Competition Ecosystem (Local vs. International Competitors)

4. KSA PV Inverter Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Central Inverters

4.1.2. String Inverters

4.1.3. Micro Inverters

4.2. By Application (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Utility-Scale

4.3. By Technology (In Value %)

4.3.1. On-Grid Inverters

4.3.2. Off-Grid Inverters

4.3.3. Hybrid Inverters

4.4. By Phase (In Value %)

4.4.1. Single-Phase

4.4.2. Three-Phase

4.5. By Region (In Value %)

4.5.1. North

4.5.2. West

4.5.3. East

4.5.4. South

5. KSA PV Inverter Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. SMA Solar Technology AG

5.1.2. Huawei Technologies Co., Ltd.

5.1.3. ABB Ltd.

5.1.4. Sungrow Power Supply Co., Ltd.

5.1.5. Schneider Electric SE

5.1.6. Fronius International GmbH

5.1.7. Delta Electronics, Inc.

5.1.8. TBEA Sunoasis Co., Ltd.

5.1.9. Growatt New Energy Technology Co., Ltd.

5.1.10. Fimer S.p.A.

5.1.11. Solis Inverters

5.1.12. GoodWe Power Supply Technology Co., Ltd.

5.1.13. Power Electronics S.L.

5.1.14. Kaco New Energy GmbH

5.1.15. Enphase Energy

5.2 Cross Comparison Parameters (Revenue, Product Portfolio, Inverter Efficiency, Installed Capacity, Technological Advancements, Presence in Key Projects, After-Sales Support, Local Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7 Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. KSA PV Inverter Market Regulatory Framework

6.1. Solar PV Policies and Targets

6.2. Compliance with Energy Regulations

6.3. Certification and Testing Requirements

7. KSA PV Inverter Future Market Size (In SAR Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. KSA PV Inverter Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Phase (In Value %)

8.5. By Region (In Value %)

9. KSA PV Inverter Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In this initial step, we mapped the entire ecosystem of the KSA PV Inverter Market. This process involved extensive desk research using both secondary and proprietary databases to gather vital industry information. We identified and defined key variables such as inverter efficiency, technological advancements, and grid compatibility that influence market performance.

Step 2: Market Analysis and Construction

In this phase, historical data from the PV inverter market was collected and analyzed to assess the adoption rate in KSA. We measured market penetration rates for different inverter types, focusing on the distribution of utility, residential, and commercial applications. Additional analysis was performed on the efficiency and performance of central vs. string inverters to understand their respective market shares.

Step 3: Hypothesis Validation and Expert Consultation

We developed market hypotheses and validated them through consultations with industry experts using computer-assisted telephone interviews (CATIs). Experts from leading inverter manufacturers and solar energy firms provided insights into market challenges, such as grid integration and domestic manufacturing constraints.

Step 4: Research Synthesis and Final Output

This final stage involved synthesizing the data collected from manufacturers and EPC contractors. We focused on aligning the bottom-up data with broader industry trends, ensuring a validated and comprehensive view of the KSA PV Inverter markets current and future dynamics.

Frequently Asked Questions

01. How big is the KSA PV Inverter Market?

The KSA PV inverter market is valued at USD 121 million, driven by the countrys commitment to expanding its renewable energy capacity under Vision 2030. This valuation reflects the increasing investments in utility-scale solar projects and the governments favorable policies promoting clean energy.

02. What are the challenges in the KSA PV Inverter Market?

The KSA PV inverter market faces several challenges, including high initial capital requirements for solar projects, technical issues related to grid integration, and the lack of domestic manufacturing capacity. Supply chain disruptions, especially in the post-pandemic period, have also impacted project timelines.

03. Who are the major players in the KSA PV Inverter Market?

Key players in the KSA PV Inverter market include Huawei Technologies, SMA Solar Technology, ABB Ltd., Sungrow Power Supply, and Fronius International. These companies dominate due to their technological expertise, efficiency in inverter systems, and involvement in major solar projects.

04. What are the growth drivers of the KSA PV Inverter Market?

The market is driven by Saudi Arabias Vision 2030 initiative, which emphasizes the adoption of renewable energy, particularly solar power. The continuous cost reductions in solar PV technology and government incentives for clean energy projects are also key growth drivers.

05. What are the future trends in the KSA PV Inverter Market?

Future trends include the integration of smart inverters with energy storage systems, increasing demand for hybrid inverter systems, and the rise of AI-driven energy management platforms. Additionally, the push for local manufacturing of solar components is expected to play a crucial role in the markets evolution.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.