KSA Sports Drinks Market Outlook to 2030

Region:Saudi Arabia

Author(s):Sanjna Verma

Product Code:KROD6684

Region:Saudi Arabia

Author(s):Sanjna Verma

Product Code:KROD6684

December 2024

97

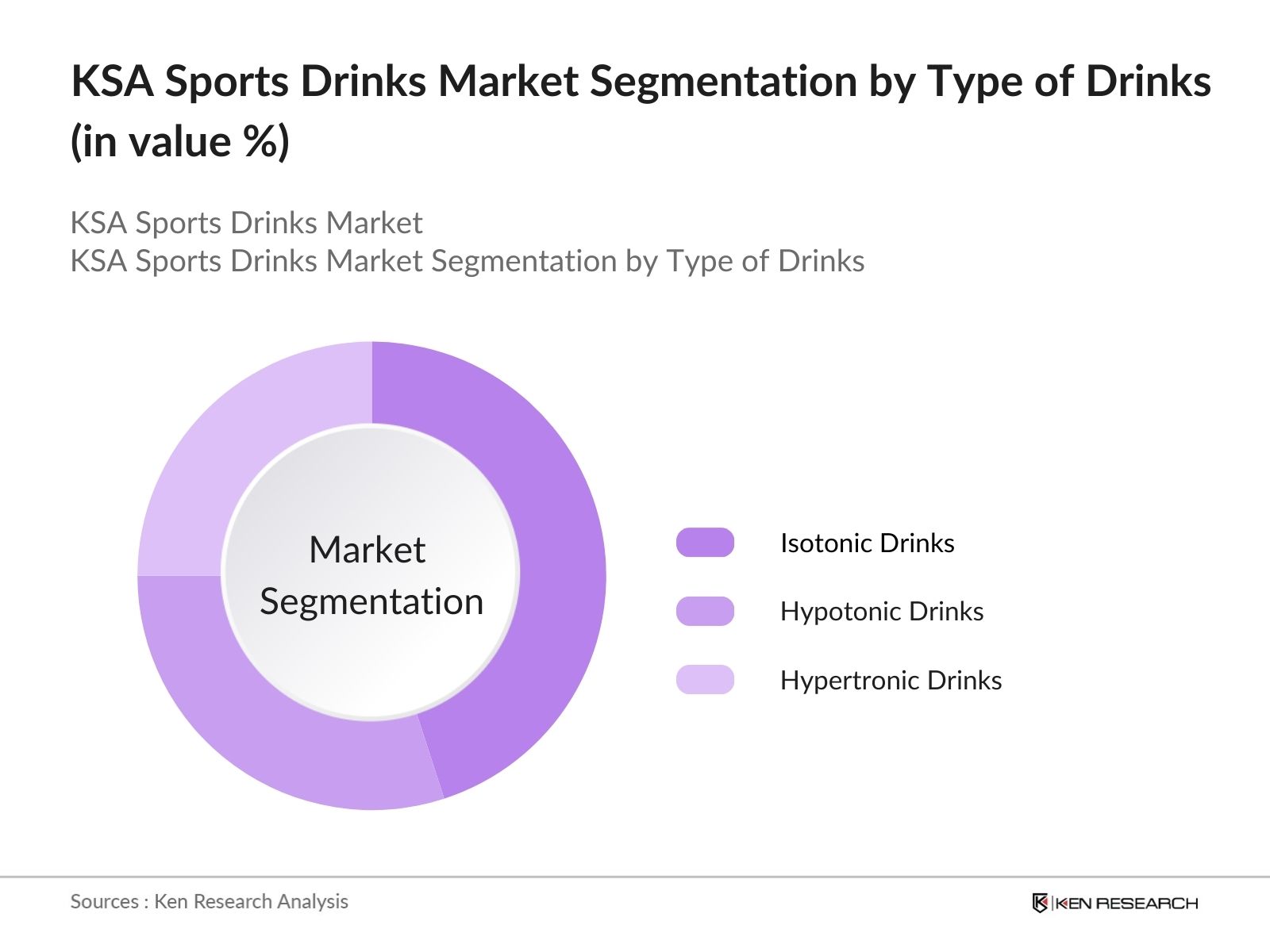

By Type of Drink: The KSA sports drinks market is segmented by drink type into isotonic drinks, hypotonic drinks, and hypertonic drinks. Currently, isotonic drinks dominate the market share due to their balanced formulation that helps in both hydration and energy replenishment. These drinks are popular among both professional athletes and fitness enthusiasts as they provide an optimal balance of electrolytes and carbohydrates, making them effective for longer-duration physical activities. The demand for isotonic drinks is further amplified by the wide variety of flavors and marketing campaigns from leading brands.

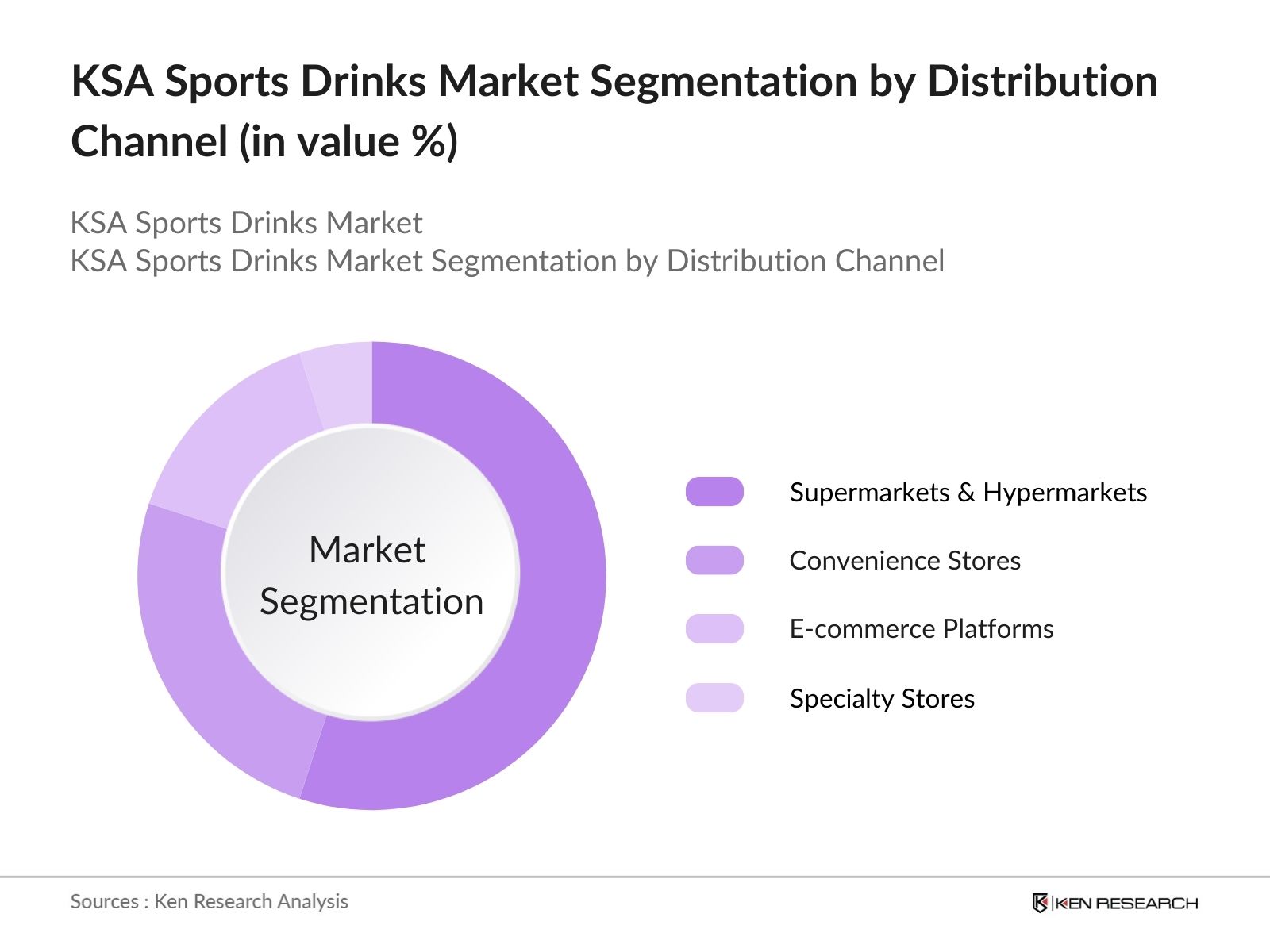

By Distribution Channel: The sports drinks market in KSA is segmented by distribution channels into supermarkets and hypermarkets, convenience stores, e-commerce platforms, and specialty stores. Supermarkets and hypermarkets hold the largest market share due to their widespread availability and the convenience of purchasing sports drinks along with other daily needs. These stores also offer a variety of product options and frequent discounts, which appeal to price-sensitive consumers. The growing trend of e-commerce has also expanded the reach of sports drinks to more remote regions in the kingdom, though its market share is still growing.

The KSA sports drinks market is dominated by both local and international brands, with significant consolidation seen in the hands of a few key players. The competitive landscape is driven by brand loyalty, strong distribution networks, and aggressive marketing campaigns targeting sports and fitness enthusiasts. Additionally, companies are introducing healthier and sugar-free variants to cater to the increasing demand for functional yet low-calorie beverages.

|

Company Name |

Establishment Year |

Headquarters |

No. of Products |

Revenue (USD) |

R&D Expenditure |

Regional Presence |

Sustainability Initiatives |

Strategic Partnerships |

|

PepsiCo, Inc. (Gatorade) |

1965 |

New York, USA |

- |

- |

- |

- |

- |

- |

|

Coca-Cola Company (Powerade) |

1892 |

Atlanta, USA |

- |

- |

- |

- |

- |

- |

|

Monster Beverage Corporation |

1935 |

California, USA |

- |

- |

- |

- |

- |

- |

|

Red Bull GmbH |

1987 |

Fuschl, Austria |

- |

- |

- |

- |

- |

- |

|

BioSteel Sports Nutrition |

2009 |

Toronto, Canada |

- |

- |

- |

- |

- |

- |

The KSA sports drinks market is expected to experience substantial growth driven by a rising focus on fitness, government initiatives promoting physical activities, and technological advancements in beverage formulations. The growing preference for healthier drink alternatives and increasing awareness of hydration's role in athletic performance are anticipated to further fuel the demand for sports drinks. Additionally, the expansion of e-commerce platforms will make these products more accessible, especially in less urbanized regions.

|

By Type of Drink |

Isotonic Drinks Hypotonic Drinks Hypertonic Drinks |

|

By Distribution Channel |

Supermarkets and Hypermarkets Convenience Stores E-commerce Platforms Specialty Stores |

|

By End User |

Professional Athletes Fitness Enthusiasts Recreational Users |

|

By Ingredient |

Electrolytes Proteins and Amino Acids Carbohydrates Vitamins and Minerals |

|

By Packaging |

Bottles Cans Tetra Packs |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Growing Health Consciousness Among Consumers

3.1.2. Increasing Sports Participation and Fitness Trends

3.1.3. Rising Demand for Functional Beverages

3.1.4. Government Initiatives to Promote Sports and Fitness (Government Support)

3.2. Market Challenges

3.2.1. High Competition from Other Beverage Categories (Market Saturation)

3.2.2. Price Sensitivity of Consumers

3.2.3. Regulatory and Labeling Requirements (Regulatory Barriers)

3.3. Opportunities

3.3.1. Development of Sugar-Free and Natural Ingredient Sports Drinks

3.3.2. Growth of E-Commerce Channels for Beverage Sales (Online Expansion)

3.3.3. Sponsorships and Endorsements in Major Sports Events

3.4. Trends

3.4.1. Adoption of Clean Label Sports Drinks

3.4.2. Customization for Endurance and Recovery Products

3.4.3. Premiumization of Sports Drinks

3.4.4. Growth of Ready-to-Drink (RTD) Sports Beverages

3.5. Government Regulation

3.5.1. Halal Certification Requirements

3.5.2. KSA Nutritional and Health Claim Regulations

3.5.3. Subsidies and Tax Policies for the Beverage Industry

3.5.4. Import and Export Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Distributors, Retailers, End-Consumers)

3.8. Porters Five Forces Analysis (Supplier Power, Buyer Power, Competitive Rivalry, Threat of Substitutes, Threat of New Entrants)

3.9. Competition Ecosystem

4.1. By Type of Drink (In Value %)

4.1.1. Isotonic Drinks

4.1.2. Hypotonic Drinks

4.1.3. Hypertonic Drinks

4.2. By Distribution Channel (In Value %)

4.2.1. Supermarkets and Hypermarkets

4.2.2. Convenience Stores

4.2.3. E-commerce Platforms

4.2.4. Specialty Stores

4.3. By End User (In Value %)

4.3.1. Professional Athletes

4.3.2. Fitness Enthusiasts

4.3.3. Recreational Consumers

4.4. By Ingredient (In Value %)

4.4.1. Electrolytes

4.4.2. Proteins and Amino Acids

4.4.3. Carbohydrates

4.4.4. Vitamins and Minerals

4.5. By Packaging (In Value %)

4.5.1. Bottles

4.5.2. Cans

4.5.3. Tetra Packs

5.1. Detailed Profiles of Major Companies

5.1.1. PepsiCo, Inc. (Gatorade)

5.1.2. The Coca-Cola Company (Powerade)

5.1.3. GlaxoSmithKline (Lucozade)

5.1.4. Danone SA

5.1.5. Monster Beverage Corporation

5.1.6. Bodyarmor SuperDrink

5.1.7. Abbott Laboratories

5.1.8. Red Bull GmbH

5.1.9. BioSteel Sports Nutrition

5.1.10. Pocari Sweat (Otsuka Pharmaceutical)

5.1.11. Nuun Hydration

5.1.12. Vitargo

5.1.13. Herbalife Nutrition Ltd.

5.1.14. PacificHealth Laboratories, Inc.

5.1.15. Staminade

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Market Share, Innovation, Regional Presence, Marketing Strategies, Sustainability Initiatives, Customer Base)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6.1. Labeling and Nutritional Claims

6.2. Sugar Content Regulations

6.3. Certification Requirements

6.4. Health Claims and Advertising Restrictions

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Rising Fitness Awareness, Product Innovation, E-commerce Expansion)

8.1. By Type of Drink (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By End User (In Value %)

8.4. By Ingredient (In Value %)

8.5. By Packaging (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

In the initial phase, an ecosystem map of the KSA sports drinks market was developed. Extensive secondary research was conducted using a mix of proprietary databases and credible third-party sources to define market dynamics. Key variables like consumer demand trends, regional distribution, and product innovation were identified.

Historical market data, including the penetration rate of sports drinks, distribution channel analysis, and regional sales performance, was compiled. The data was cross-referenced with industry benchmarks to ensure reliability and accuracy in the revenue estimates. Consumer preferences and product success rates were also evaluated.

Market hypotheses were formed based on the data gathered and then validated through expert interviews with industry professionals from major sports drink brands. These consultations provided deeper insights into operational strategies, growth prospects, and challenges, ensuring the accuracy of market projections.

The final stage involved synthesizing all the research data, expert feedback, and historical trends to create a cohesive and verified analysis of the KSA sports drinks market. This included verifying product segments, future market forecasts, and competitive dynamics using both top-down and bottom-up approaches.

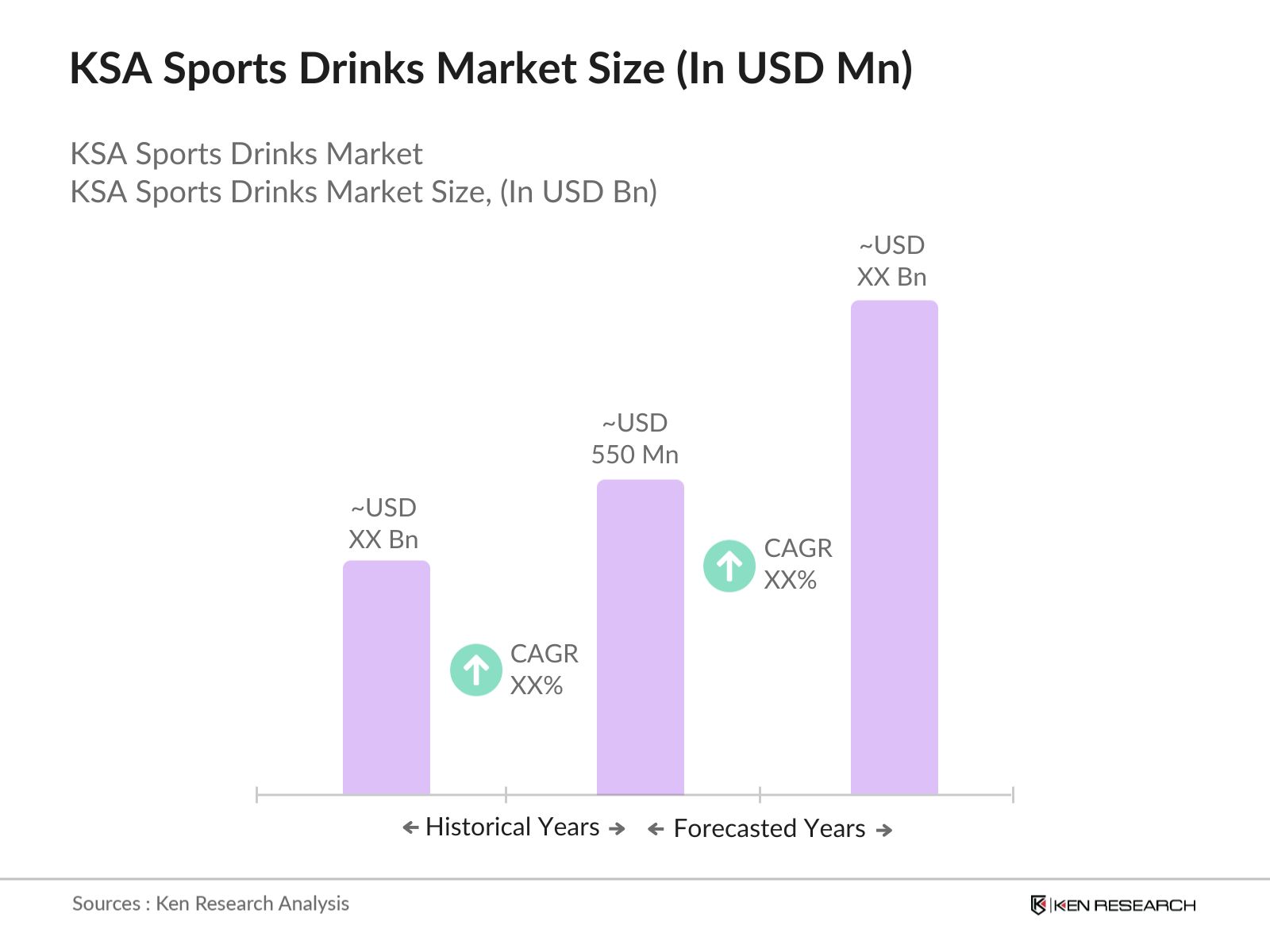

The KSA sports drinks market was valued at USD 730 million, driven by increasing fitness trends and rising health consciousness among the youth.

Key challenges of KSA Sports Drinks Market include high competition from other beverages, strict regulatory requirements on labeling and sugar content, and price sensitivity among consumers.

Major players in KSA Sports Drinks market include PepsiCo (Gatorade), Coca-Cola (Powerade), GlaxoSmithKline (Lucozade), Monster Beverage Corporation, and Red Bull GmbH.

KSA Sports Drinks Market is driven by increasing consumer awareness of health benefits, growing participation in sports and fitness activities, and rising demand for functional and hydrating beverages.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.