KSA Waste-to-Energy (WTE) Market Outlook to 2030

Region:Middle East

Author(s):Vijay Kumar

Product Code:KROD4797

December 2024

88

About the Report

KSA Waste-to-Energy (WTE) Market Overview

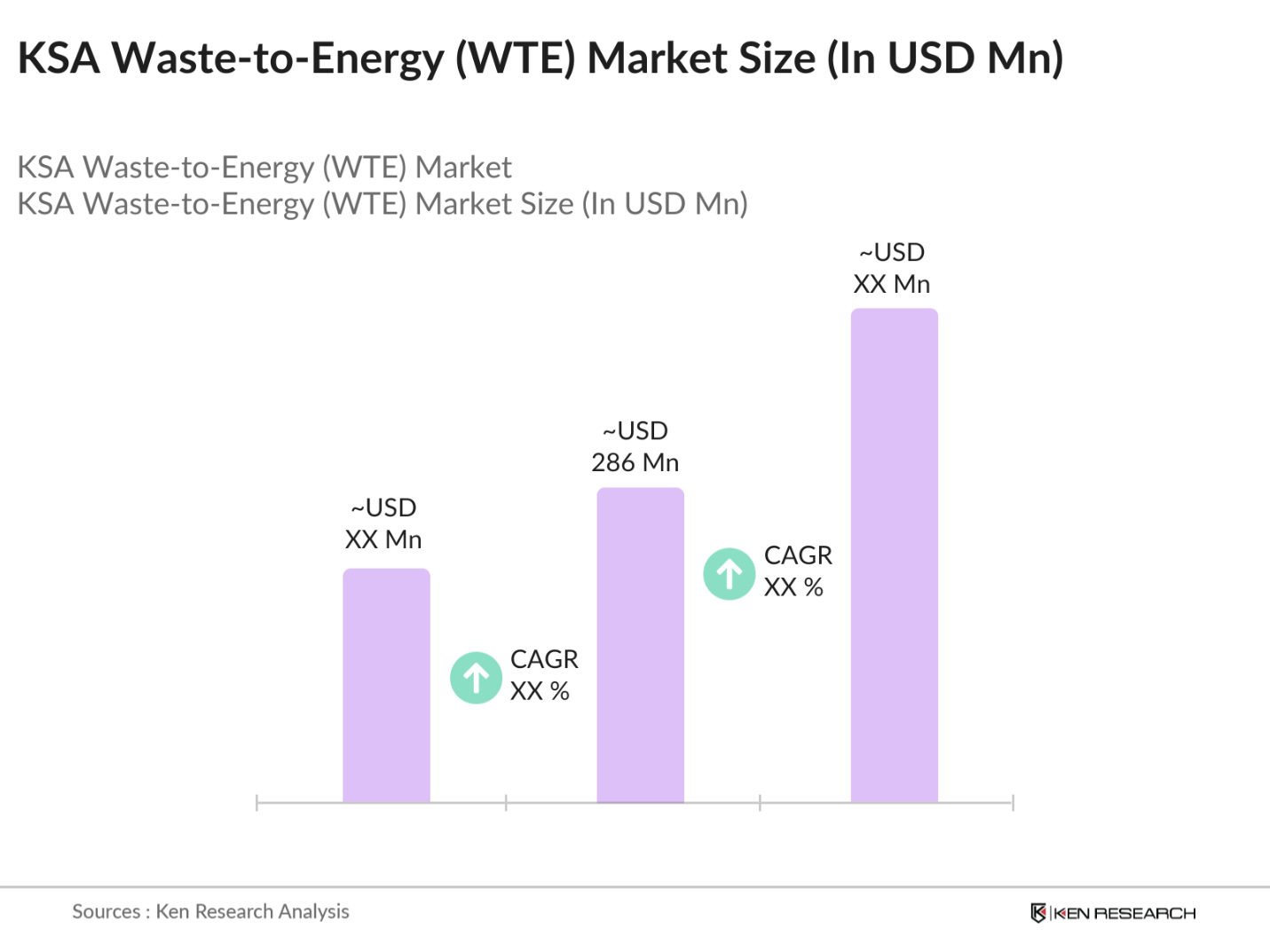

- The KSA Waste-to-Energy market is valued at USD 286 million, based on a five-year historical analysis. The markets growth is primarily driven by increasing waste generation in the country and the governments strategic initiatives under Saudi Vision 2030 to promote renewable energy projects. With the rising demand for sustainable energy solutions, WTE technologies have become a critical focus area. The expansion of municipal solid waste management systems in urban centers like Riyadh and Jeddah further fuels market growth, as these cities generate the highest volumes of waste, making them ideal locations for WTE facilities.

- Key cities such as Riyadh and Jeddah dominate the WTE market due to their large population size, high waste generation rates, and the presence of well-developed infrastructure. The centralization of waste collection and disposal facilities in these cities makes them attractive locations for WTE projects. Additionally, Riyadh's strategic plan to achieve zero waste to landfill and Jeddahs high commercial activity levels contribute significantly to the dominance of these areas in the market.

- The Saudi governments National Waste Management Strategy, under Vision 2030, outlines a clear roadmap for reducing landfill waste, enhancing recycling, and promoting WTE projects. The strategy supports the construction of new WTE plants, backed by strong regulatory frameworks and incentives for private sector participation. These initiatives are crucial for meeting the Kingdoms waste reduction and energy diversification targets.

KSA Waste-to-Energy (WTE) Market Segmentation

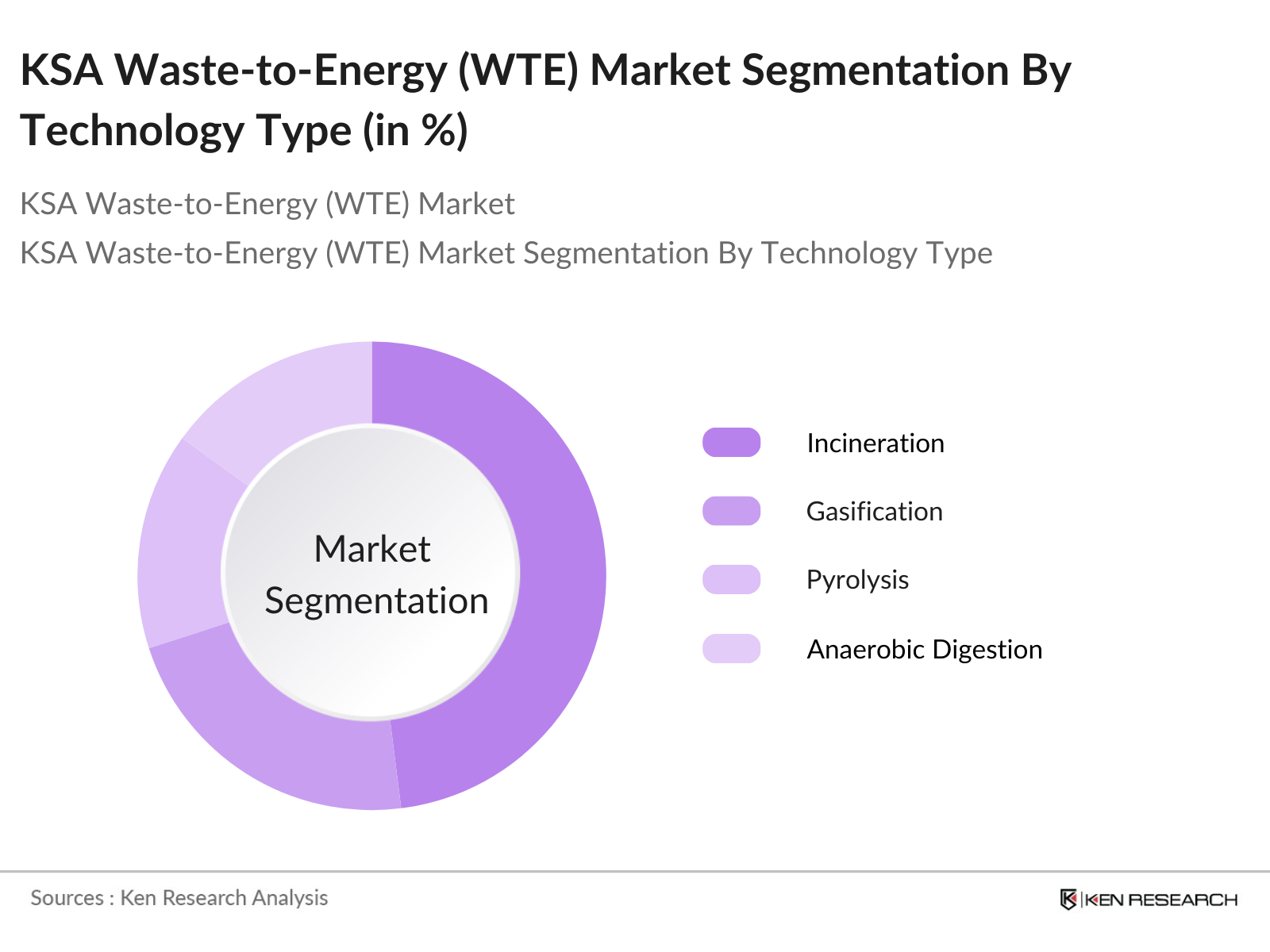

By Technology Type: The KSA Waste-to-Energy market is segmented by technology type into incineration, gasification, pyrolysis, and anaerobic digestion. Among these, incineration has a dominant market share in Saudi Arabia due to its ability to handle large quantities of waste and generate consistent energy output. This segments dominance is attributed to the lower operational complexities and reduced land usage compared to other technologies.

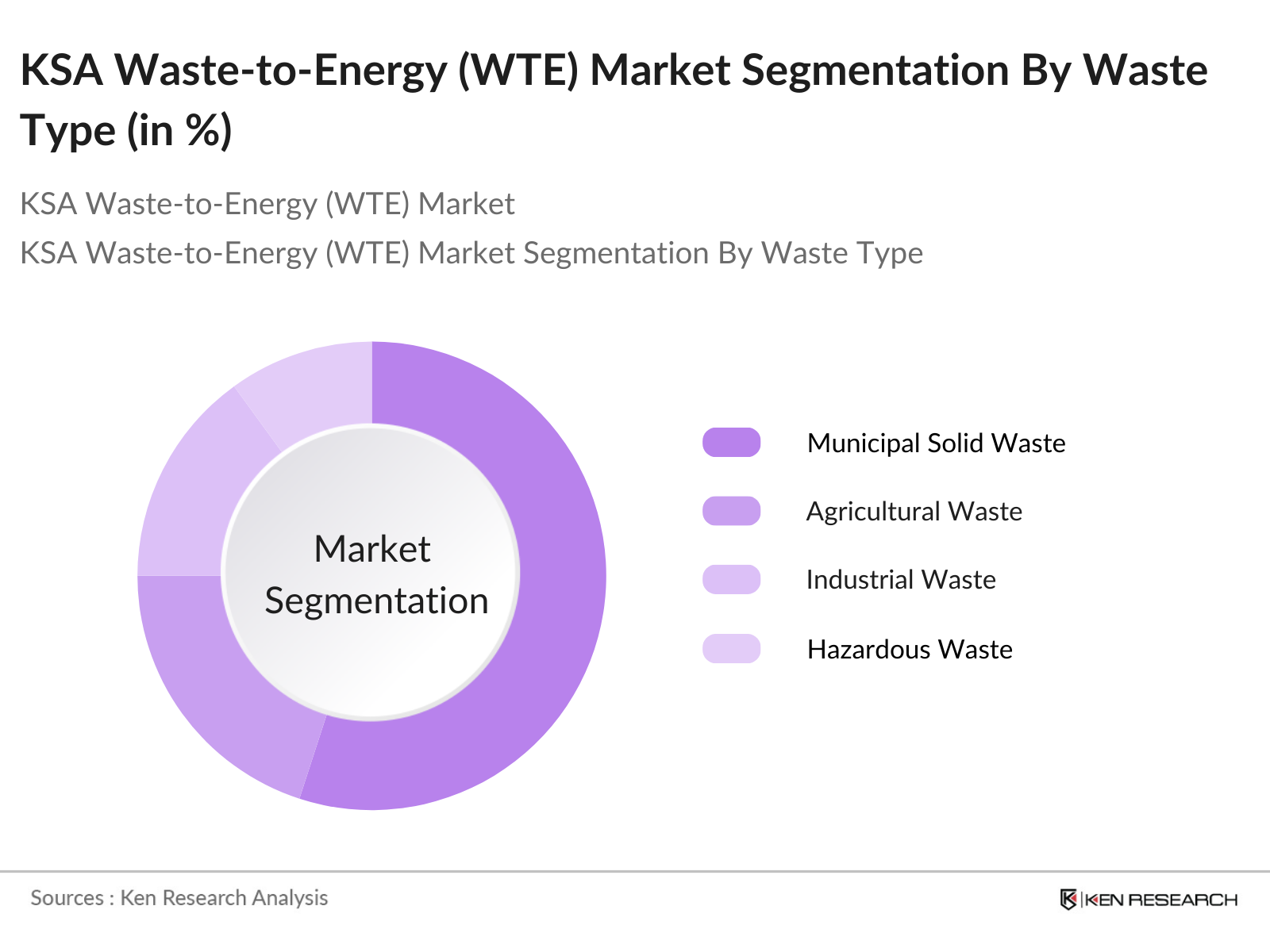

By Waste Type: The market is also segmented by waste type, including municipal solid waste, agricultural waste, industrial waste, and hazardous waste. The municipal solid waste sub-segment holds the largest market share due to the high population density in urban centers and extensive waste collection systems in place. The rising urbanization and increased commercial activities in cities like Riyadh have led to a surge in waste generation, driving the growth of this segment.

KSA Waste-to-Energy (WTE) Market Competitive Landscape

The KSA Waste-to-Energy market is dominated by a few key players with significant regional and global presence. This market consolidation reflects the influence of international and local companies in establishing strategic partnerships and collaborations to meet the growing demand for sustainable waste management solutions. The competitive landscape is influenced by a mix of established international players and regional champions, all of whom are investing in expanding their technological capabilities and project portfolios to enhance their market position.

KSA Waste-to-Energy (WTE) Industry Analysis

Growth Drivers

- Increasing Waste Generation (Municipal Solid Waste, Hazardous Waste): Saudi Arabia produces approximately 15 million tons of municipal solid waste annually, driven by rapid urbanization and a population of over 32 million in 2024. This surge is accompanied by an increase in industrial waste, further straining existing landfill capacities and creating an urgent need for alternative waste management solutions.

- Rising Demand for Sustainable Energy Solutions: Saudi Arabias push towards sustainability is underscored by the launch of the Saudi Green Initiative, which aims to generate 50% of the countrys energy from renewable sources by 2030. This includes integrating WTE as a viable renewable source, with 17 renewable energy projects in development contributing to 13.76 GW of additional capacity.

- Government Initiatives & Policies Supporting Renewable Energy Adoption: The Saudi governments Vision 2030 outlines a comprehensive strategy to support renewable energy adoption, including public-private partnerships (PPP) to stimulate investment in the WTE sector. In 2024, the Kingdom allocated over $186 billion to sustainability projects, which include waste management reforms and emissions reduction targets to ensure environmental compliance.

Market Challenges

- High Capital Investment: Setting up WTE plants requires significant capital investment due to the advanced technology and infrastructure needed. With estimated setup costs ranging between $50 million to $300 million depending on the capacity and technology, these initial expenses can pose a financial challenge. This has been identified as a barrier, especially in regions without strong financial backing, and is addressed through PPP models and foreign direct investment, which constituted 1.3% of GDP in 2024.

- Technological Complexities in Waste Segregation and Conversion: Waste segregation and conversion remain complex due to varying waste compositions. In 2024, less than 10% of municipal solid waste is recycled, complicating the conversion process. Advanced technologies such as gasification and pyrolysis are being explored to improve efficiency, but their implementation is hindered by technical expertise and high operational costs.

KSA Waste-to-Energy (WTE) Market Future Outlook

Over the next five years, the KSA Waste-to-Energy market is expected to show significant growth driven by continuous government support, increasing investments in renewable energy infrastructure, and rising awareness regarding sustainable waste management. The Saudi Vision 2030 initiative serves as a backbone for the markets growth, pushing for increased WTE capacity and the adoption of environmentally-friendly waste disposal practices.

Market Opportunities

- Technological Advancements in Gasification and Pyrolysis: Technological advancements in gasification and pyrolysis present significant opportunities for Saudi Arabias WTE market. These technologies offer more efficient waste-to-energy conversion rates and lower emissions, aligning with Saudi Arabias environmental goals. Research institutions and international technology providers are collaborating with local companies to pilot these technologies, thereby setting the stage for broader adoption in the Kingdoms industrial sectors.

- Potential Expansion into Industrial and Commercial Waste Management: With industrial production rising by 1% in August 2024, the expansion of WTE facilities to handle commercial and industrial waste is an untapped opportunity. The integration of WTE solutions into industrial zones is expected to reduce environmental impact and provide sustainable energy sources for manufacturing processes, supporting Saudi Arabias economic diversification efforts under Vision 2030.

Scope of the Report

|

Technology Type |

Incineration Gasification Pyrolysis Anaerobic Digestion |

|

Application |

Electricity Generation Heat Production Combined Heat and Power (CHP) Alternative Fuels (Biofuels, Syngas) |

|

Waste Type |

Municipal Solid Waste Agricultural Waste Industrial Waste Hazardous Waste |

|

End-User |

Industrial Residential Commercial |

|

Region |

Central Region (Riyadh) Western Region (Jeddah, Makkah) Eastern Region (Dammam, Khobar) |

Products

Key Target Audience

Waste Management Companies

Environmental Agencies (Saudi National Environmental Center)

Power Generation Companies

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (Ministry of Energy, Ministry of Environment, Water and Agriculture)

Public-Private Partnership (PPP) Entities

Industrial Waste Generators

Municipal Authorities

Companies

Players Mentioned in the Report

Veolia Environmental Services

SUEZ Group

Hitachi Zosen

Covanta Holding Corporation

ACWA Power

Babcock & Wilcox Enterprises, Inc.

Keppel Seghers

China Everbright International

C&G Environmental Protection Holdings

Ramboll Group

Table of Contents

1. KSA Waste-to-Energy Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. KSA Waste-to-Energy Market Size (In USD Mn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. KSA Waste-to-Energy Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Waste Generation (Municipal Solid Waste, Hazardous Waste)

3.1.2 Rising Demand for Sustainable Energy Solutions

3.1.3 Government Initiatives & Policies Supporting Renewable Energy Adoption

3.2 Market Challenges

3.2.1 High Capital Investment

3.2.2 Technological Complexities in Waste Segregation and Conversion

3.3 Opportunities

3.3.1 Technological Advancements in Gasification and Pyrolysis

3.3.2 Potential Expansion into Industrial and Commercial Waste Management

3.3.3 Strategic Collaborations with International Energy Corporations

3.4 Trends

3.4.1 Integration of WTE Plants with Circular Economy Models

3.4.2 Increasing Adoption of Advanced Emission Control Technologies

3.5 Government Regulation

3.5.1 National Waste Management Strategy (Saudi Vision 2030)

3.5.2 Environmental Protection and Waste Disposal Standards

3.5.3 Public-Private Partnerships (PPP) in Waste-to-Energy Projects

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Government Agencies, Private Waste Management Companies)

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem

4. KSA Waste-to-Energy Market Segmentation

4.1 By Technology Type (In Value %)

4.1.1 Incineration

4.1.2 Gasification

4.1.3 Pyrolysis

4.1.4 Anaerobic Digestion

4.2 By Application (In Value %)

4.2.1 Electricity Generation

4.2.2 Heat Production

4.2.3 Combined Heat and Power (CHP)

4.2.4 Alternative Fuels (Biofuels, Syngas)

4.3 By Waste Type (In Value %)

4.3.1 Municipal Solid Waste

4.3.2 Agricultural Waste

4.3.3 Industrial Waste

4.3.4 Hazardous Waste

4.4 By End-User (In Value %)

4.4.1 Industrial

4.4.2 Residential

4.4.3 Commercial

4.5 By Region (In Value %)

4.5.1 Central Region (Riyadh)

4.5.2 Western Region (Jeddah, Makkah)

4.5.3 Eastern Region (Dammam, Khobar)

5. KSA Waste-to-Energy Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Veolia Environmental Services (France)

5.1.2 SUEZ Group (France)

5.1.3 Hitachi Zosen (Japan)

5.1.4 Covanta Holding Corporation (US)

5.1.5 Abu Dhabi National Energy Company (UAE)

5.1.6 ACWA Power (Saudi Arabia)

5.1.7 Babcock & Wilcox Enterprises, Inc. (US)

5.1.8 Keppel Seghers (Singapore)

5.1.9 China Everbright International (China)

5.1.10 C&G Environmental Protection Holdings (China)

5.1.11 Ramboll Group (Denmark)

5.1.12 Waste Management Inc. (US)

5.1.13 Al-Qaryan Group (Saudi Arabia)

5.1.14 Bee'ah (UAE)

5.1.15 Masdar (UAE)

5.2 Cross Comparison Parameters (Number of Facilities, Capacity, Revenue, Key Technology, Regional Presence, Market Share, Partnerships, Strategic Initiatives)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. KSA Waste-to-Energy Market Regulatory Framework

6.1 National Environmental Standards

6.2 Compliance Requirements

6.3 Certification Processes

7. KSA Waste-to-Energy Future Market Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. KSA Waste-to-Energy Future Market Segmentation

8.1 By Technology Type (In Value %)

8.2 By Application (In Value %)

8.3 By Waste Type (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9. KSA Waste-to-Energy Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the KSA Waste-to-Energy Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the KSA Waste-to-Energy Market. This includes assessing market penetration, the ratio of waste management projects to energy output, and the resultant revenue generation. Furthermore, an evaluation of project performance statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple waste management companies to acquire detailed insights into project segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the KSA Waste-to-Energy market.

Frequently Asked Questions

1. How big is the KSA Waste-to-Energy Market?

The KSA Waste-to-Energy market is valued at USD 286 million, based on a five-year historical analysis. The markets growth is primarily driven by increasing waste generation in the country and the governments strategic initiatives under Saudi Vision 2030 to promote renewable energy projects.

2. What are the key growth drivers in the KSA Waste-to-Energy Market?

The market is propelled by factors such as the rise in municipal solid waste generation, supportive government policies, and advancements in waste management technologies. The Saudi Vision 2030 initiative further accelerates market growth by emphasizing renewable energy adoption.

3. Who are the major players in the KSA Waste-to-Energy Market?

Key players in the market include Veolia Environmental Services, SUEZ Group, Hitachi Zosen, Covanta Holding Corporation, and ACWA Power. These companies dominate due to their technological expertise, extensive project portfolios, and strategic partnerships in the region.

4. What challenges does the KSA Waste-to-Energy Market face?

Challenges include high capital investment requirements, technological complexities, and regulatory barriers in implementing new waste management projects. Additionally, the market faces competition from traditional energy sources.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.