MEA Armored Vehicle Market Outlook to 2030

Region:Middle East

Author(s):Shubham

Product Code:KROD5531

November 2024

86

About the Report

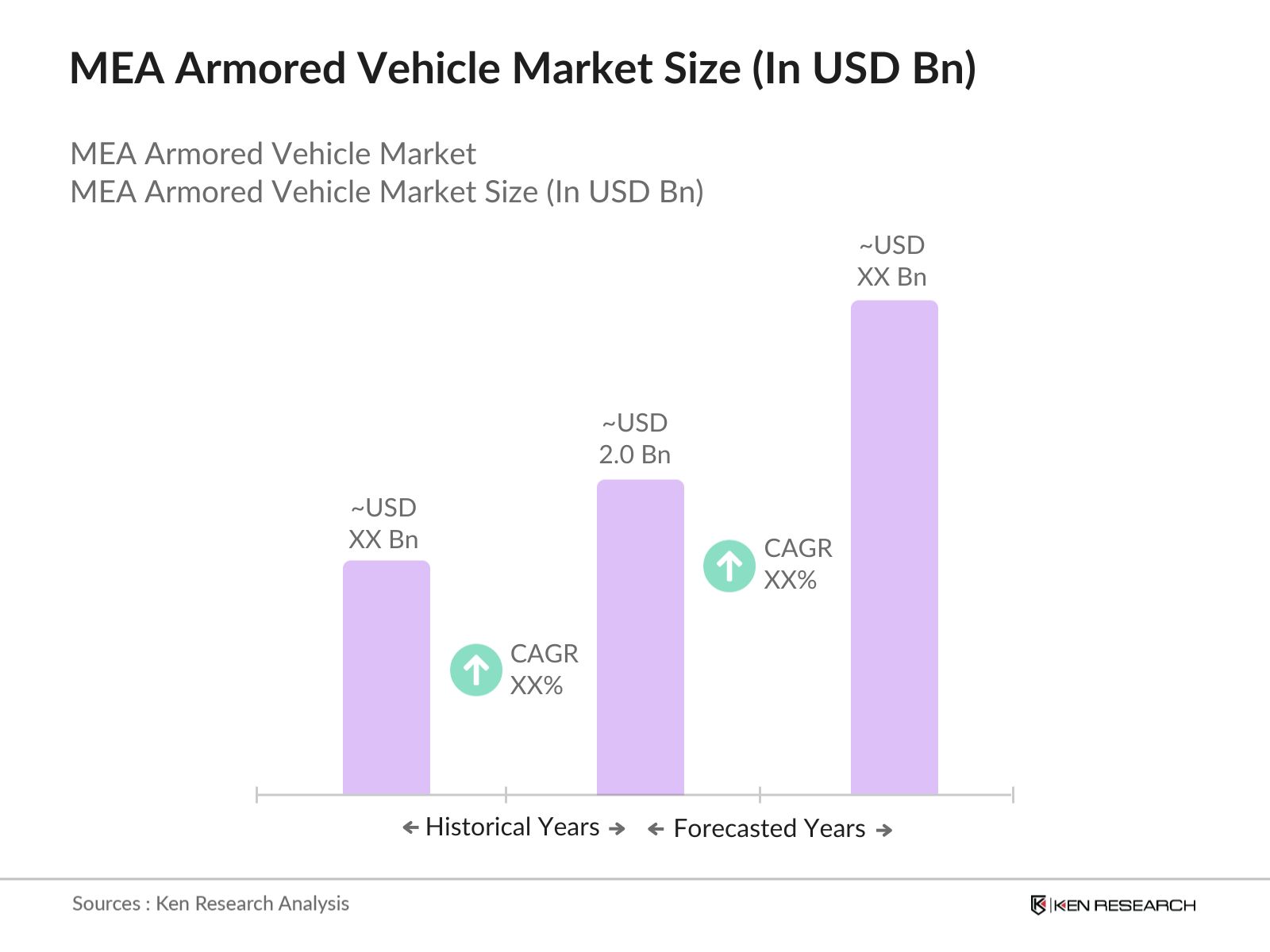

MEA Armored Vehicle Market Overview

The MEA Armored Vehicle market has shown robust growth in recent years, currently valued at USD 2.0 billion, driven by escalating geopolitical tensions, rising defense budgets, and increasing investments in military modernization programs. Countries like Saudi Arabia, the UAE, and South Africa are at the forefront of armored vehicle procurement, motivated by both domestic security needs and regional conflicts. These nations are heavily investing in next-generation armored vehicles, including mine-resistant and advanced infantry fighting vehicles.  Major demand hubs for armored vehicles in the MEA region include Saudi Arabia, the UAE, Egypt, and South Africa. These countries dominate the market due to their strategic geopolitical positions, high defense expenditures, and commitments to enhancing their military capabilities. For example, Saudi Arabia has intensified its defense spending as part of its Vision 2030 initiative, which emphasizes military modernization and self-sufficiency. Meanwhile, the UAEs involvement in regional peacekeeping and counterterrorism operations has spurred the need for technologically advanced armored vehicles.MEA governments have implemented stringent defense acquisition regulations to streamline procurement processes and ensure transparency. In 2024, Saudi Arabia introduced a new defense procurement framework aimed at reducing delays and increasing local content in defense acquisitions. Similarly, Egypt and the UAE have updated their defense procurement policies to align with international standards, fostering greater collaboration between local and foreign defense contractors.

Major demand hubs for armored vehicles in the MEA region include Saudi Arabia, the UAE, Egypt, and South Africa. These countries dominate the market due to their strategic geopolitical positions, high defense expenditures, and commitments to enhancing their military capabilities. For example, Saudi Arabia has intensified its defense spending as part of its Vision 2030 initiative, which emphasizes military modernization and self-sufficiency. Meanwhile, the UAEs involvement in regional peacekeeping and counterterrorism operations has spurred the need for technologically advanced armored vehicles.MEA governments have implemented stringent defense acquisition regulations to streamline procurement processes and ensure transparency. In 2024, Saudi Arabia introduced a new defense procurement framework aimed at reducing delays and increasing local content in defense acquisitions. Similarly, Egypt and the UAE have updated their defense procurement policies to align with international standards, fostering greater collaboration between local and foreign defense contractors.

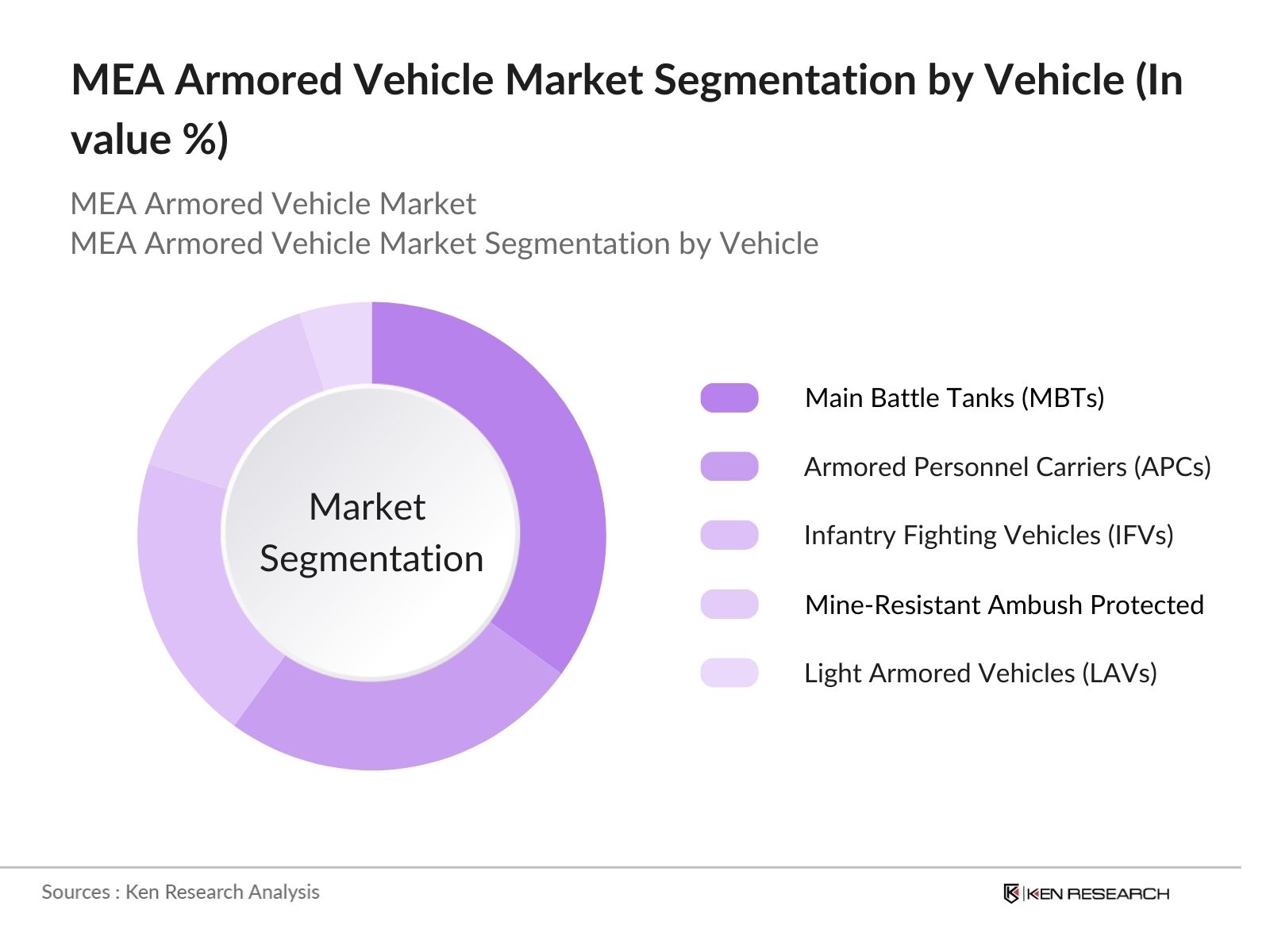

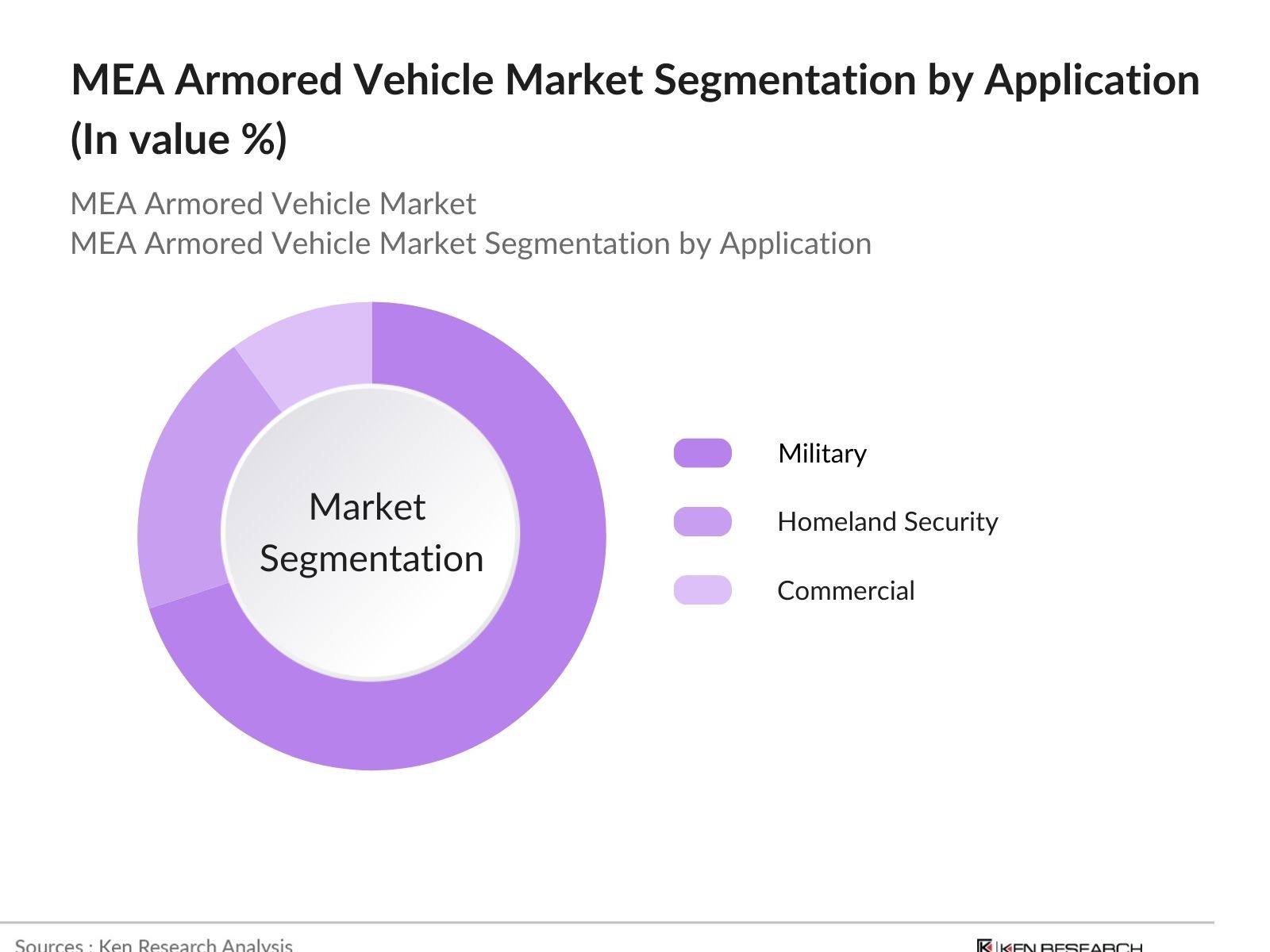

MEA Armored Vehicle Market Segmentation

- By Vehicle Type: The market can be segmented into Main Battle Tanks (MBTs), Armored Personnel Carriers (APCs), Infantry Fighting Vehicles (IFVs), Mine-Resistant Ambush Protected Vehicles (MRAPs), and Light Armored Vehicles (LAVs). Among these, MBTs dominate the market, accounting for the majority of the total armored vehicle sales in 2023. This segment is primarily driven by the increasing demand for advanced combat vehicles with superior firepower and protection. Saudi Arabia and the UAE lead the region in MBT procurement, driven by their need for modern ground forces capable of countering both conventional and asymmetric threats.

- By Application: The market is further segmented by application into military, homeland security, and commercial. The military segment holds a dominant market share, as governments across the MEA region focus on bolstering their defense capabilities. Military forces in Saudi Arabia, Egypt, and South Africa are increasing their armored vehicle fleets to enhance border security and counterterrorism operations. Homeland security is the second-largest application, driven by growing concerns over internal security, terrorism, and insurgency threats.

MEA Armored Vehicle Market Competitive Landscape

The MEA Armored Vehicle market is moderately competitive, with a mix of global and regional players competing for contracts and market share. Global defense contractors such as BAE Systems, Rheinmetall AG, and General Dynamics dominate the market, offering a wide range of armored vehicles, including MBTs, IFVs, and APCs. These companies focus on innovation, durability, and partnerships with regional governments to expand their market presence.

Regional players like Paramount Group and Otokar are also gaining traction, offering cost-effective solutions tailored to the specific needs of MEA countries. For instance, Paramount Groups Marauder and Mbombe series of armored vehicles have gained widespread adoption due to their rugged design and adaptability to different terrains.

MEA Armored Vehicle Industry Analysis

Growth Drivers

- Rising Defense Budgets: The MEA region's defense spending has been steadily increasing, driven by military modernization and security demands. In 2024, Saudi Arabia allocated over USD 75 billion to defense, positioning it among the top global defense spenders. Similarly, the UAE's defense budget reached USD 24 billion, reflecting heightened regional security concerns and military advancements. These investments are essential for bolstering border security and upgrading military infrastructure in response to emerging threats. The World Bank indicates that rising defense allocations across the MEA region are fueling the demand for armored vehicles and related military technologies.

- Increasing Threat Perceptions: The geopolitical landscape in the MEA region remains volatile, with ongoing conflicts and political instability in nations such as Syria, Yemen, and Libya. These conditions have heightened the region's defense and security needs, prompting increased procurement of advanced military equipment, including armored vehicles. In 2024, ongoing tensions with militant groups and cross-border conflicts have spurred an increased demand for improved defense systems, with MEA countries investing in upgraded military capabilities to address both conventional and asymmetrical threats. These factors underscore the strategic importance of armored vehicle acquisitions across the region.

- Government Initiatives on Military Procurement: Governments across the MEA region are actively working to modernize their military capabilities, with several nations launching procurement programs aimed at acquiring state-of-the-art armored vehicles. Saudi Arabia's Vision 2030 includes initiatives to localize military production, with plans to ensure that 50% of its defense equipment is manufactured domestically by 2030. This push for local manufacturing is accompanied by procurement of advanced technologies to enhance national defense. Additionally, the UAE has invested heavily in domestic defense production, with joint ventures aimed at advancing its armored vehicle fleet.

Market Challenges

- High Development Costs: Developing advanced armored vehicles comes with substantial costs, particularly in the MEA region where local manufacturing capabilities are limited. The cost of integrating new technologies, such as autonomous systems and advanced armor, has escalated in recent years, with the production of a single state-of-the-art armored vehicle reaching over USD 5 million. These high development costs present challenges for MEA nations, particularly those with smaller defense budgets, hindering widespread procurement and forcing reliance on foreign manufacturers for cutting-edge technology.

- Delays in Procurement Processes: Delays in military procurement processes are common in the MEA region due to bureaucratic hurdles, regulatory approvals, and geopolitical complexities. For example, a 2023 report on regional defense procurement highlighted that some MEA countries experience delays of up to two years in acquiring advanced defense technologies, including armored vehicles. These delays can be attributed to complex defense acquisition policies, slow government approvals, and changing political landscapes. As a result, defense forces may face outdated equipment, affecting operational readiness in conflict zones.

MEA Armored Vehicle Market Future Outlook

The MEA Armored Vehicle market is expected to continue its growth trajectory over the next five years, driven by increasing defense budgets, geopolitical tensions, and the need for advanced military capabilities. Countries like Saudi Arabia, the UAE, and Egypt will continue to dominate the market, while emerging markets in North Africa and sub-Saharan Africa may also see increased demand for armored vehicles as they modernize their military forces.

Future Market Opportunities

- Joint Ventures Between OEMs and Local Defense Companies: Joint ventures between original equipment manufacturers (OEMs) and local defense companies present a significant growth opportunity in the MEA armored vehicle market. For example, Saudi Arabia has signed several joint venture agreements with international defense contractors such as Lockheed Martin to co-develop and manufacture armored vehicles domestically. These collaborations not only foster technology transfer but also create a skilled workforce in the region. In 2024, such partnerships are expected to increase, with countries like the UAE and Qatar also investing heavily in joint ventures to strengthen their defense sectors.

- Technological Advancements in Armor and Weapon Systems: Technological advancements in armor and weapon systems are rapidly transforming the armored vehicle landscape. In 2024, the MEA region has witnessed the development of new lightweight armor materials that improve vehicle mobility without compromising protection. Additionally, advancements in active protection systems (APS) and remote weapon stations have been integrated into next-generation vehicles. These innovations enhance the operational capabilities of military forces, particularly in asymmetric warfare scenarios. Countries like Egypt and the UAE are actively adopting these technologies to modernize their armored fleets.

Scope of the Report

|

By Type |

Main Battle Tanks Armored Personnel Carriers Infantry Fighting Vehicles MRAPs Light Armored Vehicles |

|

By Mobility |

Wheeled Tracked |

|

By Application |

Military Homeland Security Commercial |

|

By End-User |

Government Private Defense Companies |

|

By Region |

GCC Countries North Africa Sub-Saharan Africa East Africa West Africa |

Products

Key Target Audience

Ministries of Defense

Homeland Security Agencies

Armored Vehicle Manufacturers

International Defense Contractors

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Government and Regulatory Bodies (Ministries of Defense, Interior, and Homeland Security)

Private Security Firms

Companies

Players Mentioned in the Report

BAE Systems

General Dynamics

Rheinmetall AG

Oshkosh Defense

Paramount Group

Otokar

FNSS Defence Systems

Streit Group

Al Jasoor

Lenco Industries

INKAS Armored Vehicle Manufacturing

Textron Systems

KMW (Krauss-Maffei Wegmann)

Roshel Defense Solutions

Iveco Defence Vehicles

Table of Contents

MEA Armored Vehicle Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

MEA Armored Vehicle Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

MEA Armored Vehicle Market Analysis

3.1 Growth Drivers (Military Modernization, Defense Spending, Border Security)

3.1.1 Rising Defense Budgets (In USD Bn)

3.1.2 Increasing Threat Perceptions

3.1.3 Government Initiatives on Military Procurement

3.1.4 Geopolitical Tensions in the Region

3.2 Market Challenges (Supply Chain, Technological Complexity)

3.2.1 High Development Costs

3.2.2 Delays in Procurement Processes

3.2.3 Regulatory Approvals and Export Restrictions

3.2.4 Limited Local Manufacturing Capabilities

3.3 Opportunities (Partnerships, Innovation, and R&D)

3.3.1 Joint Ventures Between OEMs and Local Defense Companies

3.3.2 Technological Advancements in Armor and Weapon Systems

3.3.3 Growth in Retrofitting and Upgrade Programs

3.3.4 Increasing Demand for Unmanned Armored Vehicles

3.4 Trends (Electrification, Autonomous Technology)

3.4.1 Shift Towards Hybrid and Electric-Powered Armored Vehicles

3.4.2 Adoption of AI and Autonomous Systems

3.4.3 Increased Use of Lighter and More Durable Composite Materials

3.4.4 Growing Focus on Cybersecurity of Military Vehicles

3.5 Government Regulation (Procurement Policies, Export Regulations)

3.5.1 National Defense Acquisition Regulations

3.5.2 Trade Compliance for Defense Exports

3.5.3 Collaboration Agreements between Government and Private Entities

3.5.4 MEA Region Defense Policies and Strategic Frameworks

MEA Armored Vehicle Market Segmentation

4.1 By Vehicle Type (In Value %)

4.1.1 Main Battle Tanks

4.1.2 Armored Personnel Carriers (APCs)

4.1.3 Infantry Fighting Vehicles (IFVs)

4.1.4 Light Armored Vehicles

4.1.5 Mine-Resistant Ambush-Protected (MRAP) Vehicles

4.2 By Application (In Value %)

4.2.1 Defense

4.2.2 Homeland Security

4.2.3 Special Forces

4.2.4 Commercial (Private Security Firms)

4.3 By Mobility Type (In Value %)

4.3.1 Wheeled Armored Vehicles

4.3.2 Tracked Armored Vehicles

4.4 By Component (In Value %)

4.4.1 Engines

4.4.2 Armor Systems

4.4.3 Communication Systems

4.4.4 Weaponry

4.5 By Region (In Value %)

4.5.1 GCC Countries

4.5.2 North Africa

4.5.3 Sub-Saharan Africa

4.5.4 Rest of MEA

MEA Armored Vehicle Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 BAE Systems

5.1.2 General Dynamics Corporation

5.1.3 Rheinmetall AG

5.1.4 Oshkosh Defense

5.1.5 Leonardo S.p.A.

5.1.6 Lockheed Martin Corporation

5.1.7 Denel Land Systems

5.1.8 FNSS Savunma Sistemleri A..

5.1.9 Streit Group

5.1.10 KMW (Krauss-Maffei Wegmann GmbH & Co. KG)

5.1.11 Paramount Group

5.1.12 IVECO Defence Vehicles

5.1.13 Thales Group

5.1.14 Textron Inc.

5.1.15 Elbit Systems Ltd.

5.2 Cross Comparison Parameters (Vehicle Manufacturing Capacity, Global Reach, Military Contracts, Technology Innovations, Revenue from Defense, Number of Armored Vehicle Models, Market Presence in MEA, Recent Acquisitions)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Partnerships, Technology Collaborations)

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Funding Programs

5.8 Private Equity and Venture Capital Investments

MEA Armored Vehicle Market Regulatory Framework

6.1 Export Control Regulations

6.2 National Defense Procurement Laws

6.3 Import Tariffs on Armored Vehicles

6.4 Regional Arms Trade Agreements

MEA Armored Vehicle Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

MEA Armored Vehicle Future Market Segmentation

8.1 By Vehicle Type (In Value %)

8.2 By Application (In Value %)

8.3 By Mobility Type (In Value %)

8.4 By Component (In Value %)

8.5 By Region (In Value %)

MEA Armored Vehicle Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 White Space Opportunity Analysis

9.3 Customer Segment Analysis

9.4 Strategic Marketing Initiatives

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the initial phase, we map out all key stakeholders in the MEA Armored Vehicle market, including defense ministries, manufacturers, and security agencies. Extensive desk research is conducted to collect data from both secondary sources and proprietary databases.

Step 2: Market Analysis and Construction

This step involves gathering and analyzing historical data on armored vehicle sales, production capacities, and defense budgets. The collected data is then used to segment the market based on vehicle type and application.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, including representatives from armored vehicle manufacturers and defense agencies, are consulted to validate market assumptions. These consultations provide insights into procurement trends, product preferences, and defense strategies.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing the data to produce actionable insights, which are then validated by comparing them with sales figures and government contracts. The output provides a comprehensive analysis of the MEA Armored Vehicle market.

Frequently Asked Questions

01. How big is the MEA Armored Vehicle Market?

The MEA Armored Vehicle market is valued at USD 2.0 billion, driven by rising defense budgets, regional conflicts, and increasing demand for military modernization across the region.

02. What are the challenges in the MEA Armored Vehicle Market?

The key challenges in the MEA Armored Vehicle market include high procurement and maintenance costs, regulatory restrictions on exports, and limited budgets for advanced military equipment in certain countries.

03. Who are the major players in the MEA Armored Vehicle Market?

Key players in the MEA Armored Vehicle market include BAE Systems, General Dynamics, Rheinmetall AG, Paramount Group, and Otokar, who dominate the market due to their advanced product offerings and strong government contracts.

04. What are the growth drivers of the MEA Armored Vehicle Market?

The MEA Armored Vehicle market is driven by increasing defense budgets, the need for military modernization, and rising geopolitical tensions across the MEA region.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.