MEA ECU Automotive Market Outlook to 2030

Region:Middle East

Author(s):Shreya Garg

Product Code:KROD2400

December 2024

97

About the Report

MEA ECU Automotive Market Overview

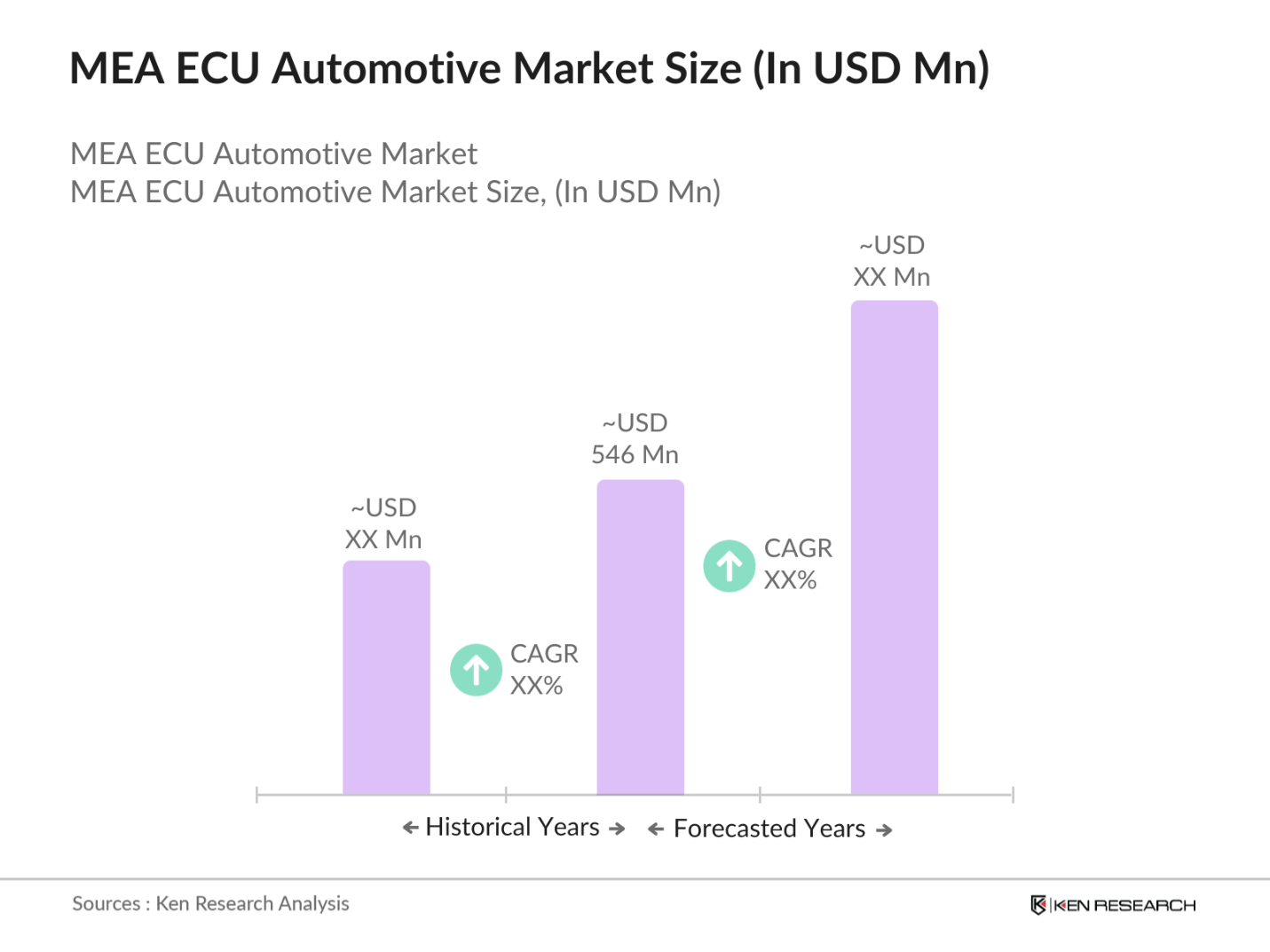

- The MEA ECU (Electronic Control Unit) Automotive market is valued at USD 546 Million based on a comprehensive analysis of the automotive sector in the region. The market's growth is primarily driven by the increasing adoption of advanced technologies such as electric vehicles (EVs) and autonomous driving systems. Key growth drivers include government regulations mandating emission control, the rise in demand for safety systems, and the integration of infotainment systems in vehicles. The evolution of powertrain ECUs in hybrid and electric vehicles further fuels the market growth.

- The market is predominantly dominated by cities and countries like Dubai (UAE), Johannesburg (South Africa), and Saudi Arabia. The dominance of these regions stems from their economic prosperity, infrastructural development, and substantial investments in advanced automotive technologies. Additionally, government policies promoting electric vehicles and stringent emissions standards in these countries have led to increased demand for sophisticated ECU systems, thus bolstering their prominence in the market.

- Several countries in the MEA region are aligning their emission regulations with international standards such as EURO 6 and the UN Vehicle Regulations. In 2023, Saudi Arabia and Egypt introduced new vehicle emission regulations aimed at reducing air pollution. The World Bank reported that compliance with these regulations is expected to cut vehicle-related CO2 emissions by 15 million metric tons annually in the region. The stricter regulations have driven automakers to enhance ECU systems for better emission control.

MEA ECU Automotive Market Segmentation

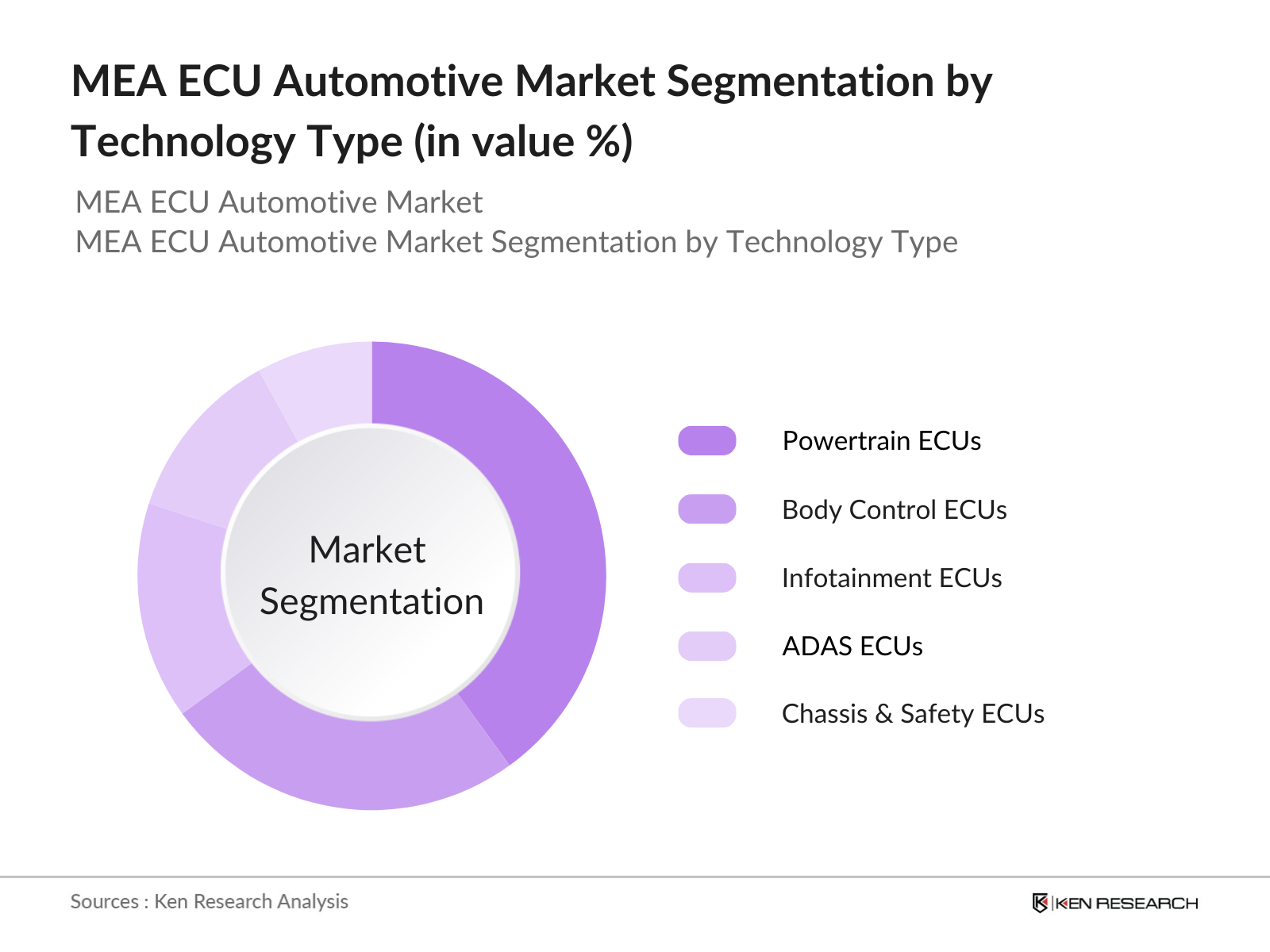

By Technology Type: The MEA ECU automotive market is segmented by technology type into powertrain ECUs, body control ECUs, infotainment ECUs, ADAS ECUs, and chassis and safety ECUs. Powertrain ECUs have a dominant market share in the region due to their critical role in optimizing fuel efficiency and meeting emission standards, especially with the growing emphasis on electric and hybrid vehicles. As the need for efficient fuel consumption and emission control becomes paramount, powertrain ECUs remain essential for vehicle performance, making them the leading segment.

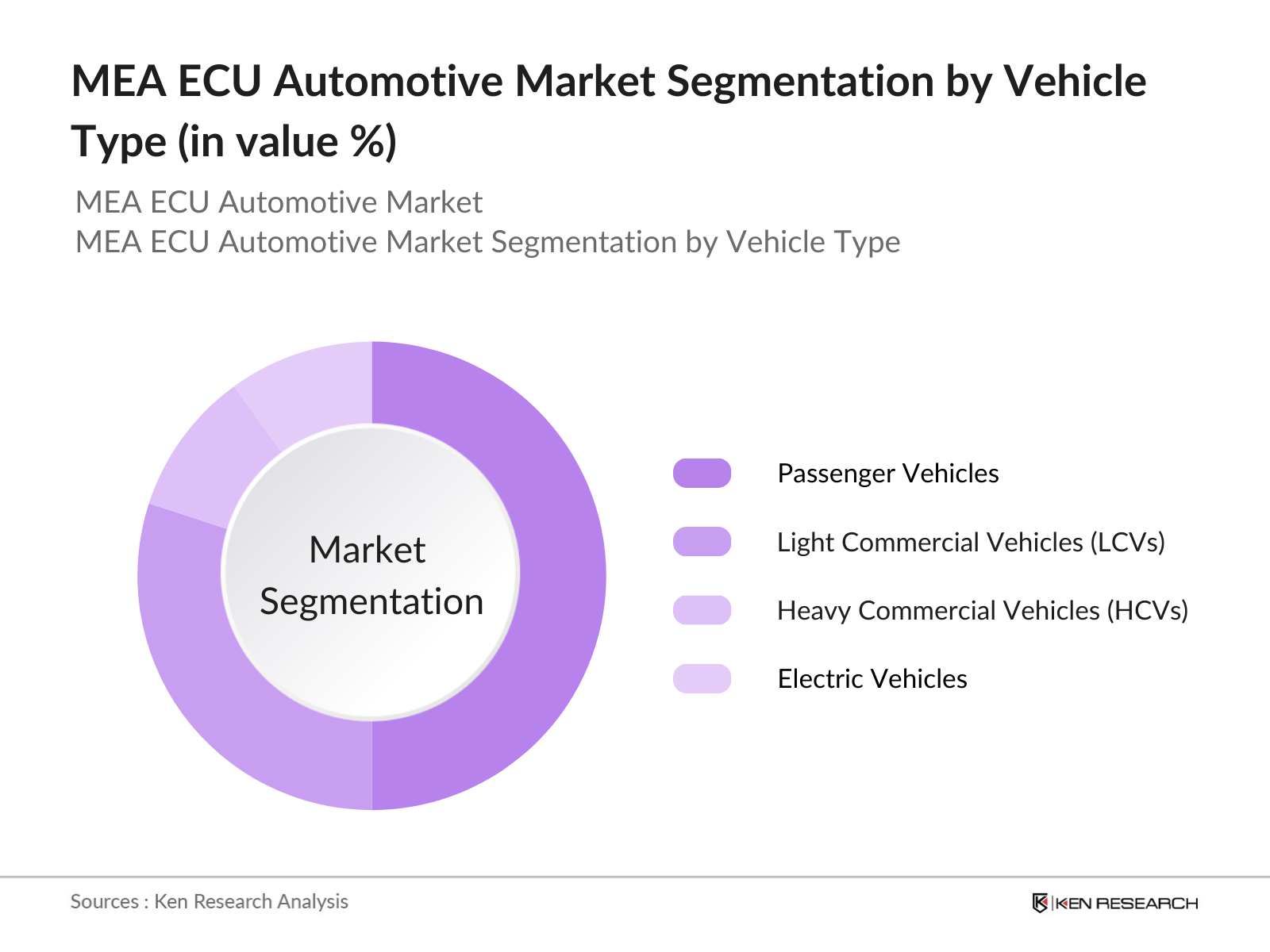

By Vehicle Type: The market is segmented by vehicle type into passenger vehicles, light commercial vehicles (LCVs), heavy commercial vehicles (HCVs), and electric vehicles (EVs). Electric vehicles dominate the market in terms of market share due to increasing government incentives, supportive policies for green energy, and a shift toward reducing carbon emissions. Electric vehicles require a higher number of advanced ECUs, such as those for power management and battery monitoring, leading to their significant share in the market.

MEA ECU Automotive Market Competitive Landscape

The MEA ECU automotive market is dominated by several global and regional players, who focus on product innovation, partnerships, and expansion strategies to maintain a competitive edge. The market shows a high level of consolidation, with a few players controlling a significant portion of the market. These key players are investing heavily in R&D to improve ECU functionality, ensuring compliance with emission standards and safety regulations, while also integrating advanced technologies such as artificial intelligence and IoT into their systems.

|

Company |

Establishment Year |

Headquarters |

Technology Focus |

R&D Expenditure |

Geographical Presence |

Product Portfolio |

Revenue (USD Mn) |

|---|---|---|---|---|---|---|---|

|

Continental AG |

1871 |

Germany |

|||||

|

Robert Bosch GmbH |

1886 |

Germany |

|||||

|

Denso Corporation |

1949 |

Japan |

|||||

|

ZF Friedrichshafen AG |

1915 |

Germany |

|||||

|

Mitsubishi Electric Corp. |

1921 |

Japan |

MEA ECU Automotive Industry Analysis

Growth Drivers

- Rise in Automotive Electrification: The electrification of the automotive sector in the MEA region has surged due to increased governmental push towards reducing emissions. In 2023, several countries such as the UAE and South Africa saw substantial EV penetration, with over 7,000 electric vehicles registered across the region. Additionally, hybrid electric vehicles (HEVs) have gained momentum, further driving the demand for electronic control units (ECUs) tailored for these systems. The World Bank has reported that investments in electric vehicle infrastructure in the region exceeded $3 billion in 2023, propelling ECU demand to accommodate advanced functionalities in EVs.

- Advanced Driver Assistance Systems: The MEA region is witnessing increasing integration of advanced driver assistance systems (ADAS) in vehicles, which requires sophisticated ECUs for real-time data processing and sensor fusion. In 2023, around 55% of new cars in the UAE and Saudi Arabia featured ADAS technology, driving up demand for multi-domain ECUs that manage safety features like lane assistance and collision avoidance. With significant investments from governments, including over $1 billion dedicated to smart road systems in the UAE, the growth in ADAS applications will further fuel the ECU market.

- Government Emission Regulations: Several MEA countries are adopting stringent emission regulations akin to the EURO 6 standards. In 2022, Saudi Arabia implemented stricter vehicle emission laws aimed at reducing nitrogen oxide and carbon monoxide emissions. This regulatory push is driving automotive manufacturers to invest in ECU systems capable of optimizing engine performance and reducing emissions. The IMF reported that investments in green automotive technology exceeded $1.5 billion in the MEA region, signaling further growth for ECUs designed to meet these emission standards.

Market Challenges

- High Initial Costs of ECU Systems: The high costs associated with advanced ECU systems remain a significant barrier for manufacturers in the MEA region. Automotive companies need to invest heavily in research, development, and production, which increases the cost of the vehicles equipped with these systems. In 2023, it was estimated that the inclusion of advanced ECUs in mid-sized cars added an average of $2,000 to the vehicle's cost, which limited adoption, especially in lower-income markets within the region.

- Lack of Standardization Across MEA Region: The absence of uniform standards for automotive ECUs across the MEA region has created challenges for manufacturers. Countries like Egypt, Saudi Arabia, and South Africa each have distinct regulations regarding vehicle components, making it difficult for manufacturers to streamline ECU production for the region. According to a 2023 report by the World Bank, this fragmentation costs automotive companies approximately $200 million annually in additional compliance expenses, highlighting the need for more cohesive regional standards.

MEA ECU Automotive Market Future Outlook

Over the next five years, the MEA ECU automotive market is expected to witness significant growth due to increasing adoption of electric vehicles, advancements in autonomous driving technologies, and the rising integration of smart safety systems in vehicles. Governments across the region are introducing policies and incentives aimed at reducing carbon emissions, further driving demand for advanced ECUs, particularly in electric and hybrid vehicles. Additionally, the growing demand for connected cars and infotainment systems is likely to fuel the expansion of the ECU market.

Future Market Opportunities

- Growing Aftermarket for ECU Upgrades: The aftermarket for ECU upgrades in the MEA region is expanding rapidly, driven by a growing customer base interested in improving vehicle performance and integrating advanced functionalities. In 2023, the UAEs automotive aftermarket value exceeded $3.4 billion, with a notable portion allocated to ECU upgrades, especially for luxury vehicles and performance cars. The World Bank's data reflects increased disposable income in the region, further boosting demand for aftermarket ECU solutions.

- Expansion of Local Manufacturing Facilities: With governments in the MEA region actively promoting local manufacturing, several automotive components manufacturing plants, including ECU production facilities, are being established. In 2023, Saudi Arabia invested over $2 billion to establish local automotive component factories, fostering a favorable environment for ECU production. This localized manufacturing helps reduce reliance on imports, thereby decreasing lead times and production costs, and supports the development of a self-sustaining ECU ecosystem.

Scope of the Report

|

Technology Type |

Powertrain ECUs |

|

Application |

Passenger Vehicles |

|

Vehicle Type |

Light Commercial Vehicles |

|

Distribution Channel |

OEMs |

|

Region |

GCC |

Products

Key Target Audience

Automotive OEMs

Automotive Component Manufacturers

Government and Regulatory Bodies (e.g., Saudi Standards, Metrology, and Quality Organization)

Electric Vehicle Manufacturers

Tier-1 Automotive Suppliers

Technology Solution Providers

Investments and Venture Capitalist Firms

Aftermarket Service Providers

Companies

Major Players

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- ZF Friedrichshafen AG

- Hitachi Automotive Systems

- Aptiv PLC

- Valeo SA

- Mitsubishi Electric Corporation

- Magneti Marelli

- Lear Corporation

- Infineon Technologies AG

- NXP Semiconductors

- Texas Instruments

- Renesas Electronics Corporation

- Visteon Corporation

Table of Contents

1. MEA ECU Automotive Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Year-on-Year % Growth, Regional % Growth)

1.4. Market Segmentation Overview (Technology Type, Application, Vehicle Type)

2. MEA ECU Automotive Market Size (In USD Bn)

2.1. Historical Market Size (Market Value USD, Growth Rate %)

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (New Launches, Strategic Alliances, Major Product Innovations)

3. MEA ECU Automotive Market Analysis

3.1. Growth Drivers

3.1.1. Rise in Automotive Electrification (EV Adoption, Growth in HEVs)

3.1.2. Advanced Driver Assistance Systems (ADAS Integration)

3.1.3. Government Emission Regulations (EURO Emission Standards, MEA Country-Specific Regulations)

3.1.4. Rising Demand for Autonomous Vehicles

3.2. Market Challenges

3.2.1. High Initial Costs of ECU Systems

3.2.2. Lack of Standardization Across MEA Region

3.2.3. Impact of Global Chip Shortages

3.3. Opportunities

3.3.1. Growing Aftermarket for ECU Upgrades

3.3.2. Expansion of Local Manufacturing Facilities

3.3.3. Increased Focus on In-Vehicle Infotainment (Connected Car Technologies)

3.4. Trends

3.4.1. Rising Demand for Real-time Data Processing ECUs (AI and Machine Learning Integration)

3.4.2. Development of Multi-Domain ECUs (Combining ADAS, Infotainment, and Engine Control)

3.4.3. Adoption of OTA (Over-the-Air) Updates for ECU Systems

3.5. Government Regulations

3.5.1. Adoption of Emission Standards (EURO 6, UN Vehicle Regulations)

3.5.2. Mandatory Safety Features in Automotive ECU (Advanced Braking Systems, Crash Avoidance Technology)

3.5.3. Incentives for Electric Vehicles (EV Subsidies, Charging Infrastructure Development)

3.6. SWOT Analysis

3.7. Stake Ecosystem (Automotive Manufacturers, Suppliers, OEMs, Aftermarket)

3.8. Porters Five Forces (Bargaining Power of Suppliers, Threat of New Entrants, Intensity of Competitive Rivalry, etc.)

3.9. Competition Ecosystem (Key Market Competitors, Technological Advancements, Pricing Strategies)

4. MEA ECU Automotive Market Segmentation

4.1. By Technology Type (In Value %)

4.1.1. Powertrain ECUs

4.1.2. Body Control ECUs

4.1.3. Infotainment ECUs

4.1.4. ADAS ECUs

4.1.5. Chassis and Safety ECUs

4.2. By Application (In Value %)

4.2.1. Passenger Vehicles

4.2.2. Commercial Vehicles

4.2.3. Electric Vehicles

4.2.4. Hybrid Vehicles

4.3. By Vehicle Type (In Value %)

4.3.1. Light Commercial Vehicles (LCVs)

4.3.2. Heavy Commercial Vehicles (HCVs)

4.3.3. Passenger Cars (Hatchbacks, Sedans, SUVs)

4.4. By Distribution Channel (In Value %)

4.4.1. OEMs

4.4.2. Aftermarket

4.5. By Region (In Value %)

4.5.1. GCC

4.5.2. North Africa

4.5.3. Sub-Saharan Africa

4.5.4. South Africa

4.5.5. Levant Region

5. MEA ECU Automotive Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Continental AG

5.1.2. Robert Bosch GmbH

5.1.3. Denso Corporation

5.1.4. ZF Friedrichshafen AG

5.1.5. Mitsubishi Electric Corporation

5.1.6. Hitachi Automotive Systems

5.1.7. Aptiv PLC

5.1.8. Magneti Marelli

5.1.9. Valeo SA

5.1.10. Infineon Technologies AG

5.1.11. Texas Instruments

5.1.12. Renesas Electronics Corporation

5.1.13. NXP Semiconductors

5.1.14. Lear Corporation

5.1.15. Visteon Corporation

5.2. Cross Comparison Parameters (Revenue, Technology Adoption, Geographical Presence, R&D Investments, Number of Patents, Key Strategic Partnerships, Market Share %)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product Launches, Joint Ventures, Acquisitions)

5.5. Mergers And Acquisitions

5.6. Investment Analysis (Venture Capital, Private Equity)

5.7. R&D Expenditure Analysis

5.8. Government Grants and Subsidies

6. MEA ECU Automotive Market Regulatory Framework

6.1. Compliance with Emission Standards (EURO, MEA-Specific Regulations)

6.2. Safety Standards for ECU Integration (Crash Avoidance, ADAS Compliance)

6.3. Import Regulations for ECU Components

6.4. Certification Processes (Automotive ECU Standards, ISO Certifications)

7. MEA ECU Automotive Future Market Size (In USD Bn)

7.1. Future Market Size Projections (Growth Forecast, Technology Penetration Rate)

7.2. Key Factors Driving Future Market Growth (Increased EV Adoption, Government Incentives)

8. MEA ECU Automotive Future Market Segmentation

8.1. By Technology Type (In Value %)

8.2. By Application (In Value %)

8.3. By Vehicle Type (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. MEA ECU Automotive Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis (Total Addressable Market, Serviceable Available Market, Serviceable Obtainable Market)

9.2. Strategic Customer Cohort Analysis

9.3. Product Development Recommendations

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase focuses on mapping the entire ecosystem of the MEA ECU automotive market. This is achieved through in-depth desk research involving secondary sources such as government reports, industry databases, and proprietary datasets. The goal is to identify the key factors that impact market dynamics, including technological trends and regulatory frameworks.

Step 2: Market Analysis and Construction

In this phase, we gather and assess historical data for the MEA ECU automotive market, analyzing market penetration, revenue trends, and competitive intensity. We also review the presence of ECU suppliers and OEMs in key regions to ensure accurate market segmentation and forecast.

Step 3: Hypothesis Validation and Expert Consultation

We engage with industry experts through CATIs (computer-assisted telephone interviews) to validate our market hypotheses. These discussions provide insights from stakeholders across the supply chain, helping us refine our findings and ensure the accuracy of the data.

Step 4: Research Synthesis and Final Output

In the final stage, we compile data from manufacturers and suppliers to verify market forecasts. This involves direct engagement with ECU manufacturers, ensuring that all data points are validated and reflect the current industry landscape.

Frequently Asked Questions

01. How big is the MEA ECU Automotive Market?

The MEA ECU automotive market is valued at USD 2.7 billion, driven by the growing demand for electric and hybrid vehicles, alongside advancements in autonomous driving technologies.

02. What are the key challenges in the MEA ECU Automotive Market?

Challenges include the high cost of ECU systems, lack of standardization across the region, and the ongoing global semiconductor shortage, which affects the production of critical automotive components.

03. Who are the major players in the MEA ECU Automotive Market?

Key players include Continental AG, Robert Bosch GmbH, Denso Corporation, ZF Friedrichshafen AG, and Hitachi Automotive Systems, which dominate due to their advanced product offerings, extensive R&D investments, and strong market presence.

04. What are the growth drivers for the MEA ECU Automotive Market?

The market is propelled by factors such as the increasing adoption of electric vehicles, advancements in ADAS (Advanced Driver Assistance Systems), and government regulations enforcing emission standards.

05. What is the future outlook for the MEA ECU Automotive Market?

The market is expected to experience substantial growth, driven by the increasing integration of advanced ECUs in electric and hybrid vehicles, as well as growing demand for in-vehicle infotainment and connected car technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.