MEA Electric Vehicle Market Outlook to 2030

Region:Middle East

Author(s):Shubham Kashyap

Product Code:KROD3935

December 2024

86

About the Report

MEA Electric Vehicle Market Overview

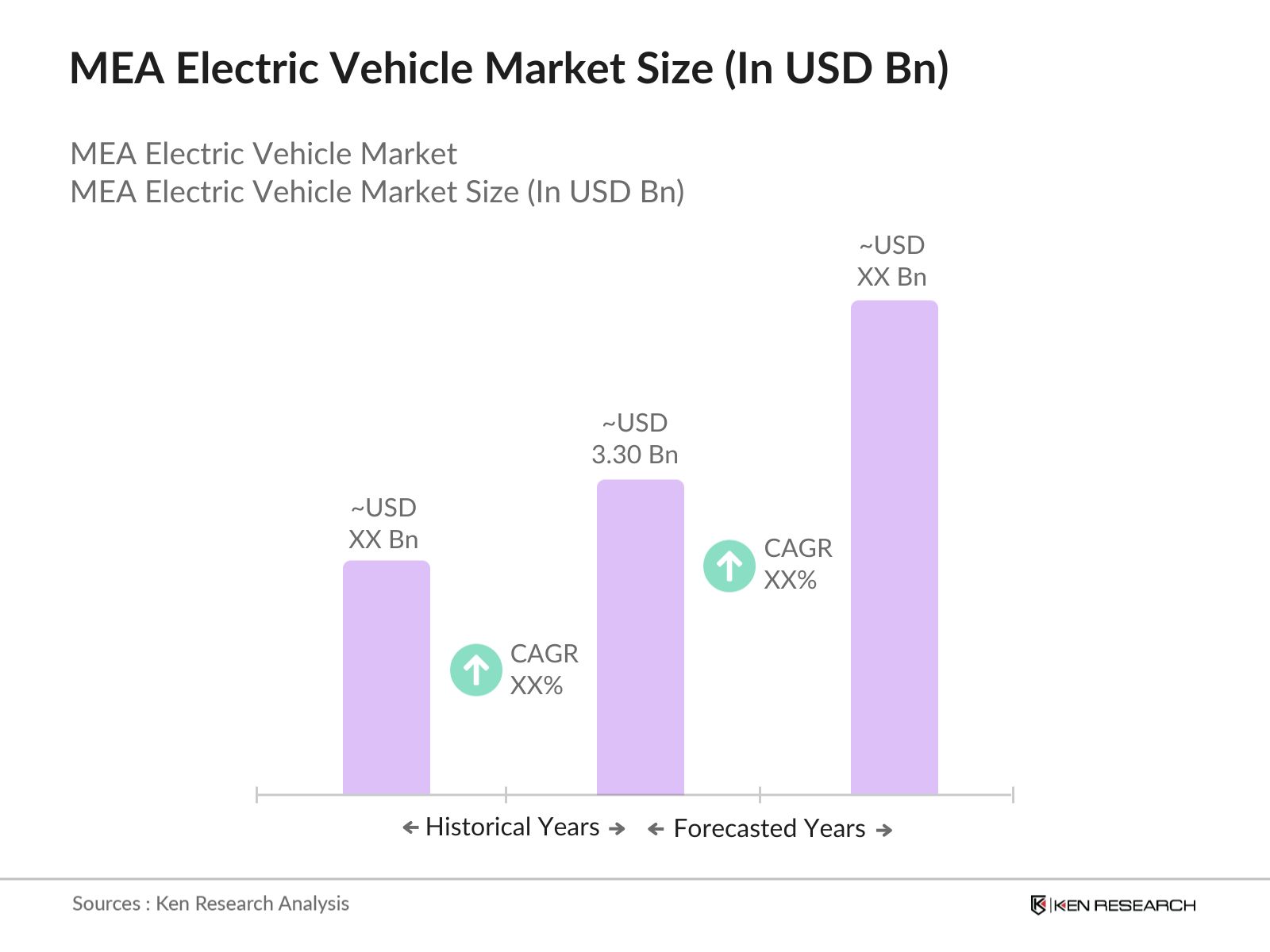

- The MEA Electric Vehicle (EV) market has exhibited substantial growth in recent years, currently valued at USD 3.30 Bn, driven by increasing environmental concerns, government initiatives to reduce carbon emissions, and rising fuel costs. Key markets such as the UAE, Saudi Arabia, and South Africa have been leading the charge in adopting electric vehicles, supported by a growing EV infrastructure network, including public charging stations and incentives for EV purchases.

- Major demand hubs for EVs in the MEA region include Dubai, Abu Dhabi, Riyadh, and Johannesburg, where urbanization, government policies promoting sustainable transportation, and rising disposable income levels are encouraging consumers and businesses to transition to electric mobility. In 2023, the UAE government introduced incentives, such as tax exemptions and free public parking for EVs, further boosting market adoption. Additionally, Saudi Arabia's Vision 2030 initiative has placed a strong emphasis on sustainability, driving demand for EVs across the kingdom.

- The regulatory landscape in the MEA region is evolving rapidly, with governments introducing stringent emission standards and policies favoring the adoption of electric vehicles. Organizations such as the Gulf Standardization Organization (GSO) and the Saudi Standards, Metrology, and Quality Organization (SASO) have been actively involved in shaping regulations to support the transition to EVs. These regulations ensure that EVs entering the market meet international safety and environmental standards, promoting market growth.

MEA Electric Vehicle Market Segmentation

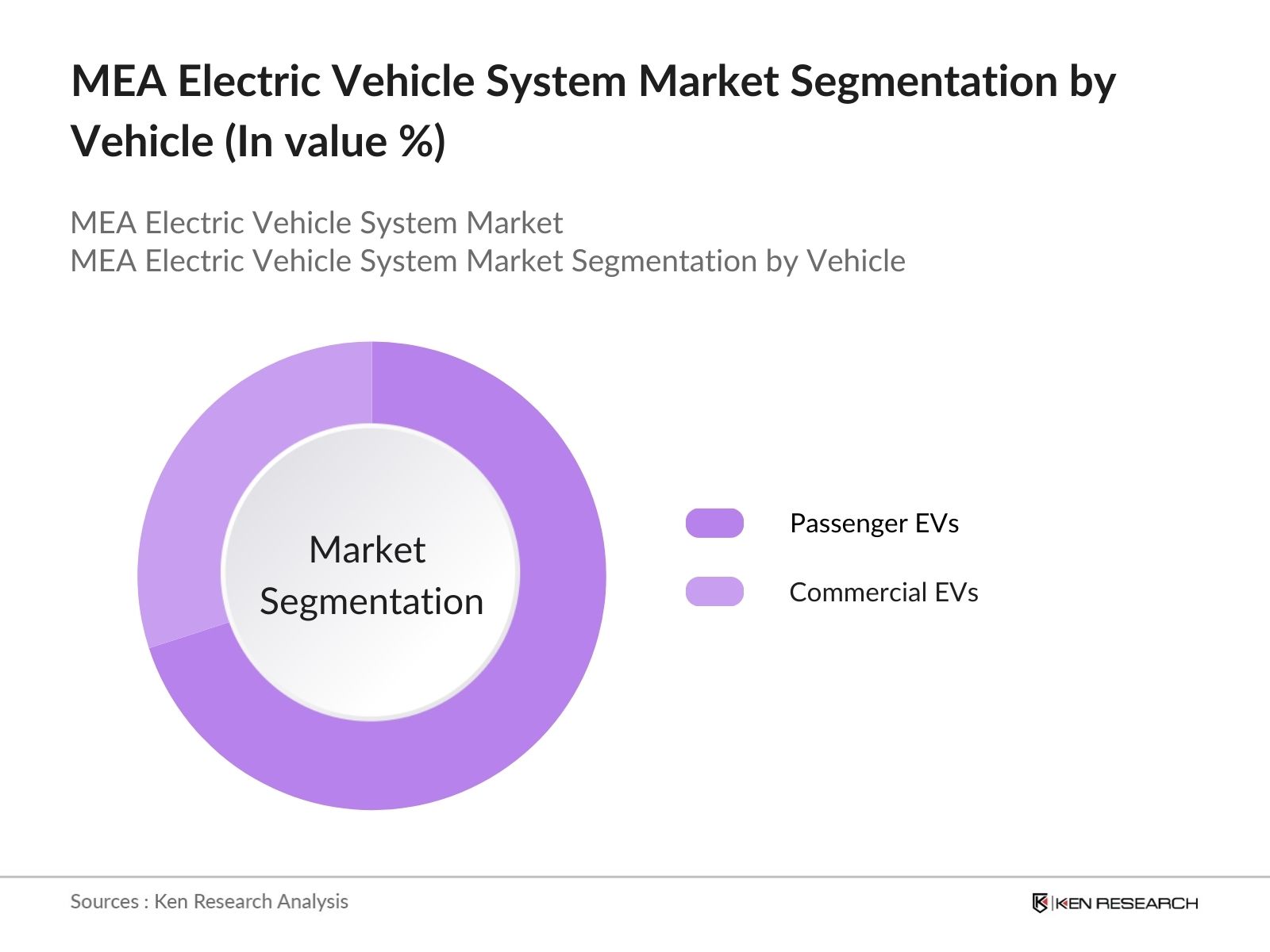

- By Vehicle Type: The market can be segmented into passenger vehicles and commercial vehicles. Passenger vehicles dominate the market, accounting for majority of the total EV sales in 2023. This segment is primarily driven by consumer demand for environmentally friendly transportation options, particularly in urban areas. In contrast, the commercial vehicle segment, which includes electric buses, vans, and trucks, is gaining traction, supported by government initiatives to electrify public transportation systems. The UAE and Saudi Arabia are leading the region in adopting electric buses, with both countries launching major EV bus projects in 2023 to reduce carbon emissions in urban areas.

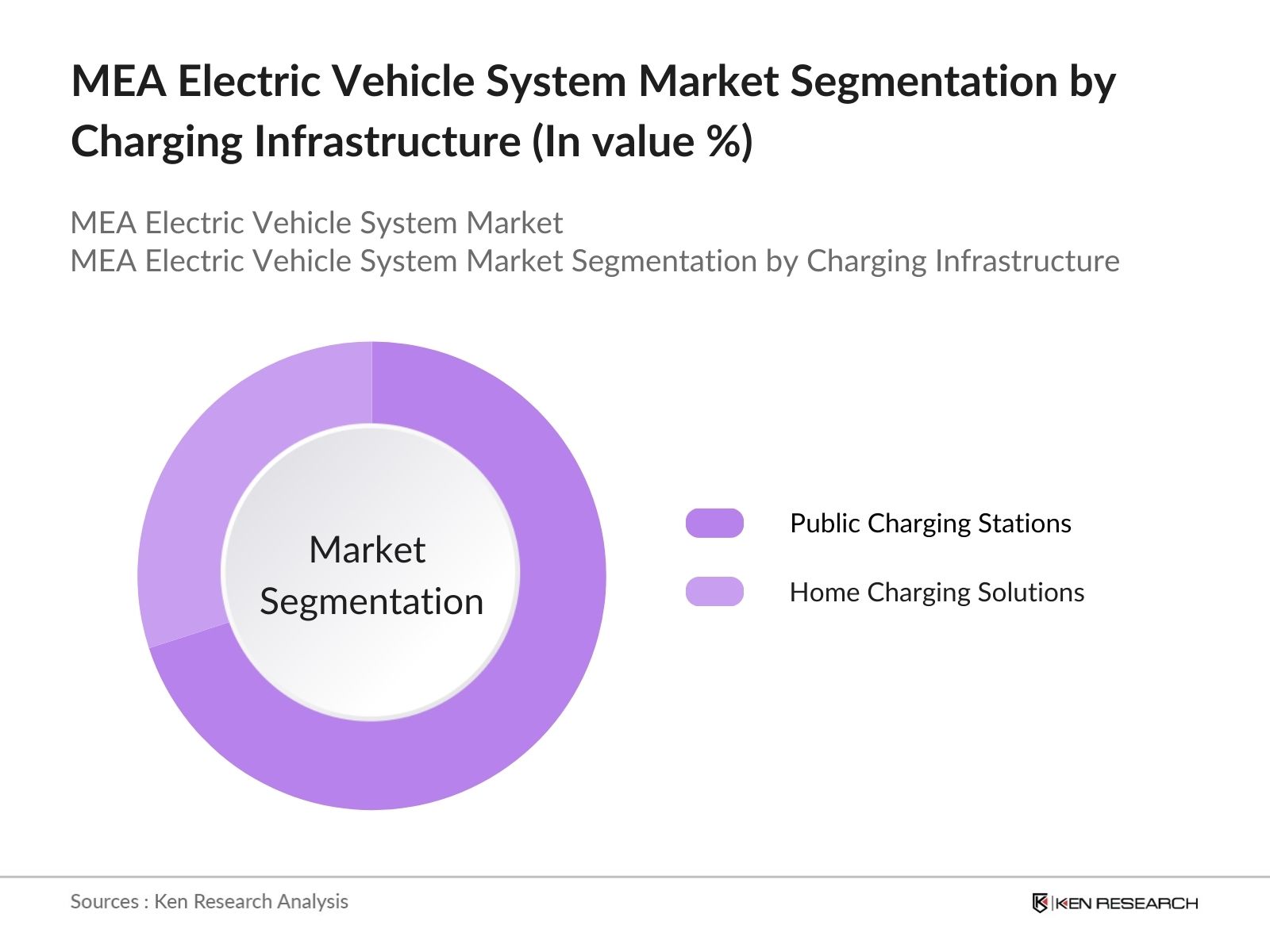

- By Charging Infrastructure: The market is further segmented by charging infrastructure, including public charging stations and home charging solutions. Public charging stations are gaining importance as governments and private players invest in expanding the EV charging network. In 2023, the UAE government installed hundreds of public charging stations nationwide, supporting the growing number of EVs on the road. Home charging solutions are also witnessing increased adoption, particularly among high-end consumers who prefer the convenience of charging their EVs at home. As the number of EVs grows, both public and private charging solutions will continue to expand to meet the rising demand for efficient and reliable charging options.

MEA Electric Vehicle Market Competitive Landscape

The MEA Electric Vehicle market is moderately competitive, with a mix of global and regional players vying for market share. Global automotive giants such as Tesla, Nissan, and BMW dominate the passenger EV segment, offering a range of electric sedans, SUVs, and hatchbacks. These companies focus on product innovation, battery technology advancements, and expanding their charging infrastructure to enhance their competitive positioning.

In the commercial vehicle segment, companies such as BYD, Tesla, and local manufacturers like Al-Futtaim Motors are actively expanding their presence. BYD, in particular, has secured multiple contracts to supply electric buses for public transportation projects in Saudi Arabia and the UAE. The competitive landscape is further influenced by collaborations between global automakers and regional distributors, which help adapt electric vehicle offerings to local market needs.

|

Company |

Establishment Year |

Headquarters |

EV Production Capacity (Units/Year) |

Revenue (2023) |

Key Products |

Market Penetration |

Sustainability Initiatives |

R&D Expenditure |

Distribution Network |

|

Tesla, Inc. |

2003 |

USA |

|||||||

|

Nissan Motor Co., Ltd. |

1933 |

Japan |

|||||||

|

BMW Group |

1916 |

Germany |

|||||||

|

Al-Futtaim Motors |

1955 |

UAE |

|||||||

|

BYD Co. Ltd. |

1995 |

China |

MEA Electric Vehicle Industry Analysis

Growth Drivers

-

EV Infrastructure Expansion: The Middle East and Africa (MEA) region is seeing significant investments in electric vehicle (EV) infrastructure, driven by governmental push towards sustainable transport. Saudi Arabia has announced plans to build 100 EV charging stations by the end of 2025. The UAE, with its Vision 2030, aims to install 10,000 charging points. The African Development Bank has allocated $10 million for electric mobility projects across sub-Saharan Africa in 2023. These efforts reflect a broader global push towards EV adoption to reduce reliance on fossil fuels. These developments are supported by macroeconomic policies aimed at reducing carbon emissions.

- Increasing Fuel Prices and Environmental Awareness: The ongoing volatility in global oil prices has prompted both governments and consumers in the MEA region to seek alternatives to conventional fossil-fuel-based transport. In 2023, Brent crude prices averaged around USD 82.49 per barrel, which significantly impacted fuel costs across the region. South Africa recorded a rise in fuel prices of USD 1.34 per liter in 2023, which has accelerated EV adoption. Environmental concerns also play a major role as many MEA countries like Morocco and Egypt are facing increasing pressure to reduce greenhouse gas emissions.

- Government Incentives and Policies Promoting EVs: Governments in the MEA region are introducing tax breaks, subsidies, and incentives to promote EV adoption. In 2022, the UAE government waived import duties on electric vehicles, while Egypt announced a USD 200 million fund to support green transport initiatives. Saudi Arabia, in line with Vision 2030, is aiming for 30% of vehicles in Riyadh to be electric by 2030. These policies are a response to international pressures to reduce emissions, further driving the market for electric mobility.

Market Challenges

-

High Initial Investment and Battery Costs: Despite the growth potential, high upfront costs remain a significant barrier to EV adoption in the MEA region. The cost of electric vehicles is still beyond reach for most consumers in developing markets such as Kenya and Ghana. Additionally, battery manufacturing in the region is limited, leading to higher import costs. Lithium-ion batteries, which account for a significant portion of an EVs cost, continue to pose a challenge despite global price reductions. This high initial investment deters widespread EV adoption in emerging economies, where affordability remains a primary concern.

- Limited Charging Stations in Emerging Markets: Charging infrastructure remains a significant bottleneck in many African countries. The limited number of charging stations creates challenges for mass EV adoption, as consumers are concerned about the accessibility of charging points. The lack of infrastructure investments in rural and suburban areas further exacerbates this problem, limiting the market to urban regions. The expansion of charging infrastructure is essential, and public-private partnerships are seen as a potential solution to accelerate the development of this critical infrastructure.

MEA Electric Vehicle Market Future Outlook

The MEA Electric Vehicle market is poised for substantial growth over the next five years, driven by increasing government support, growing environmental consciousness, and rising fuel costs. Countries such as the UAE and Saudi Arabia will continue to lead the market, with strong growth expected in both the passenger and commercial vehicle segments. Additionally, the expansion of charging infrastructure and the localization of EV production in some markets will further support market growth.

Future Market Opportunities

-

Emerging Market Demand for Low-Emission Vehicles: Several emerging economies within the MEA region are witnessing a growing demand for low-emission vehicles as part of their green economy transition. In 2023, Egypt saw a 30% year-on-year increase in EV sales, driven by government incentives and rising fuel prices. Additionally, Moroccos National Energy Strategy aims for 52% of energy production to come from renewable sources by 2030, supporting the demand for electric mobility. These shifts are creating opportunities for local and international automakers to meet this growing demand.

- Integration of Renewable Energy with EV Charging Stations: In 2023, Kenyas Energy and Petroleum Regulatory Authority (EPRA) approved the integration of solar-powered charging stations in major urban areas. This integration of renewable energy sources with EV infrastructure presents a significant opportunity to promote sustainable energy use. For instance, Dubais Sustainable City has already installed solar-powered EV charging stations, allowing the use of clean energy for mobility. These developments not only promote EV adoption but also reduce dependence on the grid

Scope of the Report

|

By Vehicle Type |

Passenger Vehicles Commercial Vehicles |

|

By Charging Infrastructure |

Public Charging Stations Home Charging Solutions |

|

By Propulsion Type |

Battery Electric Vehicles (BEVs) Plug-in Hybrid Electric Vehicles (PHEVs) |

|

By End-User |

Private Consumers Government Fleet Commercial Fleet |

|

By Country |

GCC North Africa Sub-Saharan Africa |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (UAE Ministry of Energy and Industry, Saudi Ministry of Transport)

Electric Vehicle Manufacturers

EV Charging Infrastructure Providers

Automotive Distributors and Dealers

Fleet Operators

Public Transportation Authorities

Renewable Energy Companies

Banks and Financial Institutions

Companies

Major Players Mentioned in the Report

Tesla Motors

Nissan Motor Corporation

BMW Group

BYD Auto

Volkswagen Group

Renault Group

Ford Motor Company

General Motors

Rivian

Hyundai Motor Company

Al-Futtaim Motors

Geely Auto

Tata Motors

Chery Automobile Co. Ltd.

Lucid Motors

Table of Contents

1. MEA Electric Vehicle Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. MEA Electric Vehicle Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. MEA Electric Vehicle Market Analysis

3.1 Growth Drivers (Electric Mobility Transition, Government Policies, Infrastructure Development, Oil Price Volatility)

3.1.1 EV Infrastructure Expansion

3.1.2 Increasing Fuel Prices and Environmental Awareness

3.1.3 Government Incentives and Policies Promoting EVs

3.1.4 Rise of Sustainable Transportation Solutions

3.2 Market Challenges (High Purchase Costs, Charging Infrastructure Gaps, Energy Resource Challenges)

3.2.1 High Initial Investment and Battery Costs

3.2.2 Limited Charging Stations in Emerging Markets

3.2.3 Technological Gaps and Power Grid Dependency

3.2.4 Market Dependency on Imported Technology

3.3 Opportunities (EV Supply Chain Localization, Renewable Energy Integration, Urban Mobility Solutions)

3.3.1 Emerging Market Demand for Low-Emission Vehicles

3.3.2 Integration of Renewable Energy with EV Charging Stations

3.3.3 Rise of Urban E-Mobility Solutions

3.3.4 Investment in Advanced Battery Technology

3.4 Trends (Battery Technology Advances, Autonomous EVs, EV Adoption in Public Transport)

3.4.1 Shift Toward Solid-State Batteries

3.4.2 Autonomous EV Development in Key Markets

3.4.3 Expansion of Electric Buses in Public Transport

3.5 Government Regulation (EV Incentives, Emission Standards, Sustainable Development Goals)

3.5.1 EV Adoption Incentives and Tax Breaks

3.5.2 CO2 Emission Reduction Targets and Compliance

3.5.3 Public-Private Partnerships in Charging Infrastructure

3.5.4 SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.5.5 Stakeholder Ecosystem

3.5.6 Porters Five Forces

4. MEA Electric Vehicle Market Segmentation

4.1 By Vehicle Type (In Value %)

4.1.1 Passenger Electric Vehicles

4.1.2 Commercial Electric Vehicles (EV Buses, EV Trucks)

4.2 By Charging Infrastructure Type (In Value %)

4.2.1 Home Charging Solutions

4.2.2 Public Charging Stations (Fast Charging, Slow Charging)

4.3 By Drivetrain Type (In Value %)

4.3.1 Battery Electric Vehicles (BEVs)

4.3.2 Plug-In Hybrid Electric Vehicles (PHEVs)

4.4 By End-Use Sector (In Value %)

4.4.1 Private Transportation

4.4.2Commercial Fleets (Logistics, E-Commerce, Ride Hailing)

4.5 By Region (In Value %)

4.5.1 GCC (UAE, Saudi Arabia, Oman)

4.5.2 North Africa (Egypt, Morocco)

4.5.3 Sub-Saharan Africa (South Africa, Nigeria)

5. MEA Electric Vehicle Market Competitive Landscape

5.1 Detailed Profiles of Major Companies (Company Overview, Product Offerings, Market Presence, Strategic Initiatives)

Tesla Motors

Nissan Motor Corporation

BMW Group

BYD Auto

Volkswagen Group

Renault Group

Ford Motor Company

General Motors

Rivian

Hyundai Motor Company

Al-Futtaim Motors

Geely Auto

Tata Motors

Chery Automobile Co. Ltd.

Lucid Motors

5.1 Cross Comparison Parameters (Market Share, Revenue, Global Footprint, Strategic Initiatives, Charging Infrastructure Partnerships, R&D Focus, Sustainability Practices, Local Manufacturing Initiatives)

Market Share Analysis

Strategic Initiatives (Partnerships, Joint Ventures, Expansion Plans)

Mergers and Acquisitions

Investment Analysis

Venture Capital Funding

Government Grants and Incentives

Private Equity Investments

6. MEA Electric Vehicle Market Regulatory Framework

6.1 Emission Standards and EV Compliance

6.2 EV Certification Requirements

6.3 Renewable Energy Integration in EV Policies

6.4 Public Transport Electrification Policies

6.5 Government Infrastructure Development Programs

7. MEA Electric Vehicle Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. MEA Electric Vehicle Future Market Segmentation

8.1 By Vehicle Type (In Value %)

8.2 By Charging Infrastructure Type (In Value %)

8.3 By Drivetrain Type (In Value %)

8.4 By End-Use Sector (In Value %)

8.5 By Region (In Value %)

9. MEA Electric Vehicle Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 White Space Opportunity Analysis

9.4 Marketing and Sales Initiatives

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the MEA Electric Vehicle Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the MEA Electric Vehicle Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple electric vehicle manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the MEA Electric Vehicle Market.

Frequently Asked Questions

01. How big is the MEA Electric Vehicle Market?

The MEA Electric Vehicle market was valued at USD 3.30 billion and continues to grow due to government incentives, rising fuel costs, and the region's commitment to reducing its carbon footprint.

02. What are the challenges in the MEA Electric Vehicle Market?

Challenges in the MEA Electric Vehicle market include high initial costs for EVs, insufficient charging infrastructure in emerging markets, and a reliance on imported technology for vehicle components and batteries.

03. Who are the major players in the MEA Electric Vehicle Market?

Key players in the MEA Electric Vehicle market include Tesla, Nissan, BMW, BYD, and Al-Futtaim Motors, all of which dominate through innovation, regional partnerships, and an expanding presence across the region.

04. What are the growth drivers of the MEA Electric Vehicle Market?

The MEA Electric Vehicle market is propelled by government support, advancements in battery technology, and increasing consumer demand for sustainable transportation solutions. Urbanization and infrastructure development are also contributing to the market's rapid expansion.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.