MEA Industrial Automation Market Outlook to 2030

Region:Global

Author(s):Meenakshi

Product Code:KROD4835

November 2024

93

About the Report

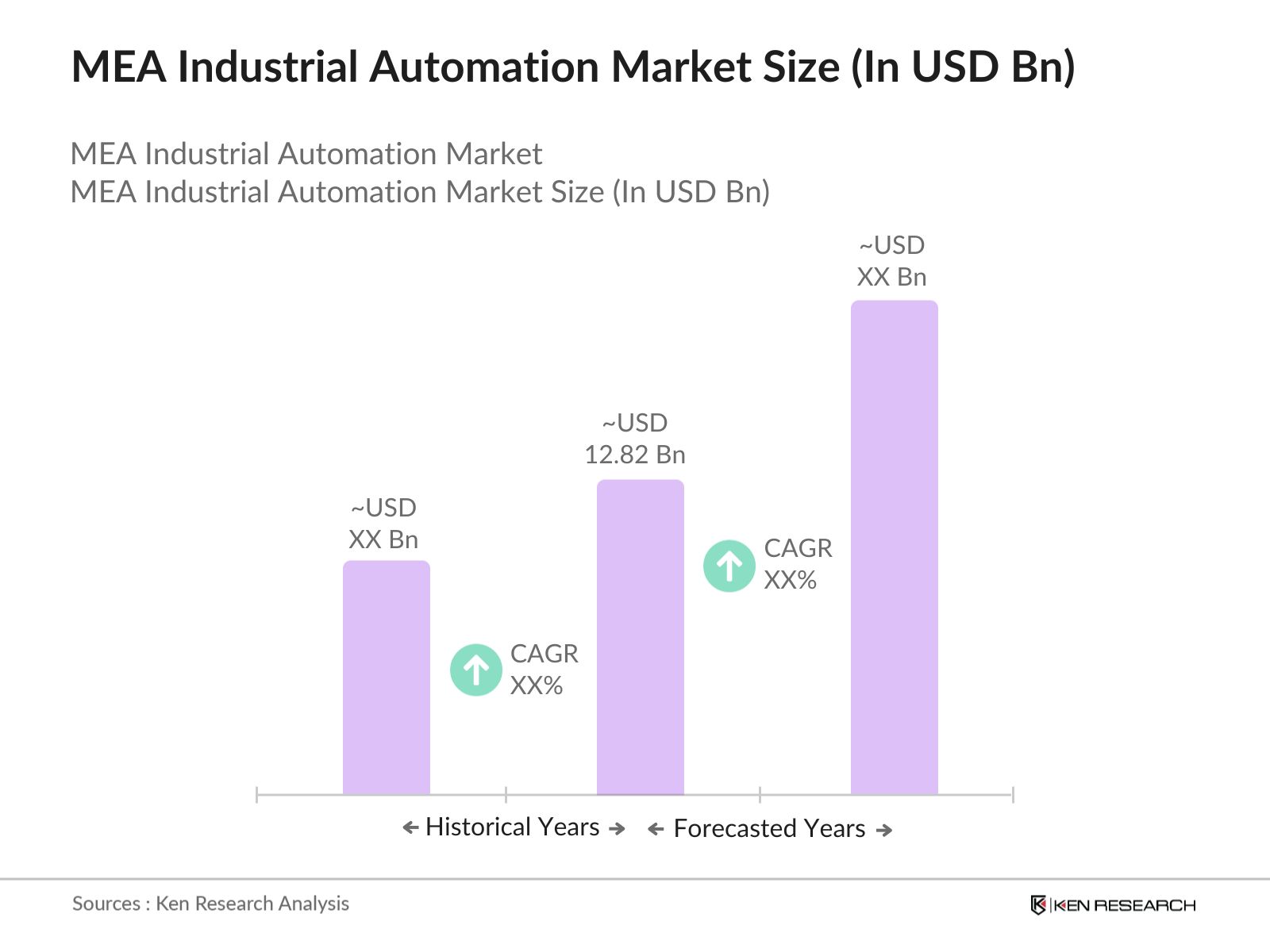

MEA Industrial Automation Market Overview

- The Middle East and Africa (MEA) industrial automation market is currently valued at USD 12.82 billion. This market is primarily driven by the increasing need for operational efficiency across industries, particularly within oil & gas, energy, and manufacturing sectors. Companies in the region are rapidly adopting automation technologies like Industrial Internet of Things (IIoT), robotics, and artificial intelligence (AI) to enhance productivity and reduce operational costs.

- In the MEA region, the United Arab Emirates (UAE), Saudi Arabia, and South Africa are key players in driving the industrial automation market. The UAE and Saudi Arabia dominate due to large-scale investments in smart cities and industrial diversification initiatives, particularly under the UAE Vision 2030 and Saudi Vision 2030.

- As industrial automation systems become more data-driven, data security and regulatory compliance have become critical issues. Governments in the MEA region are strengthening data protection laws, with countries like the UAE enforcing the Federal Decree Law No. 45 of 2021 on the Protection of Personal Data, which impacts how data is managed within automated systems.

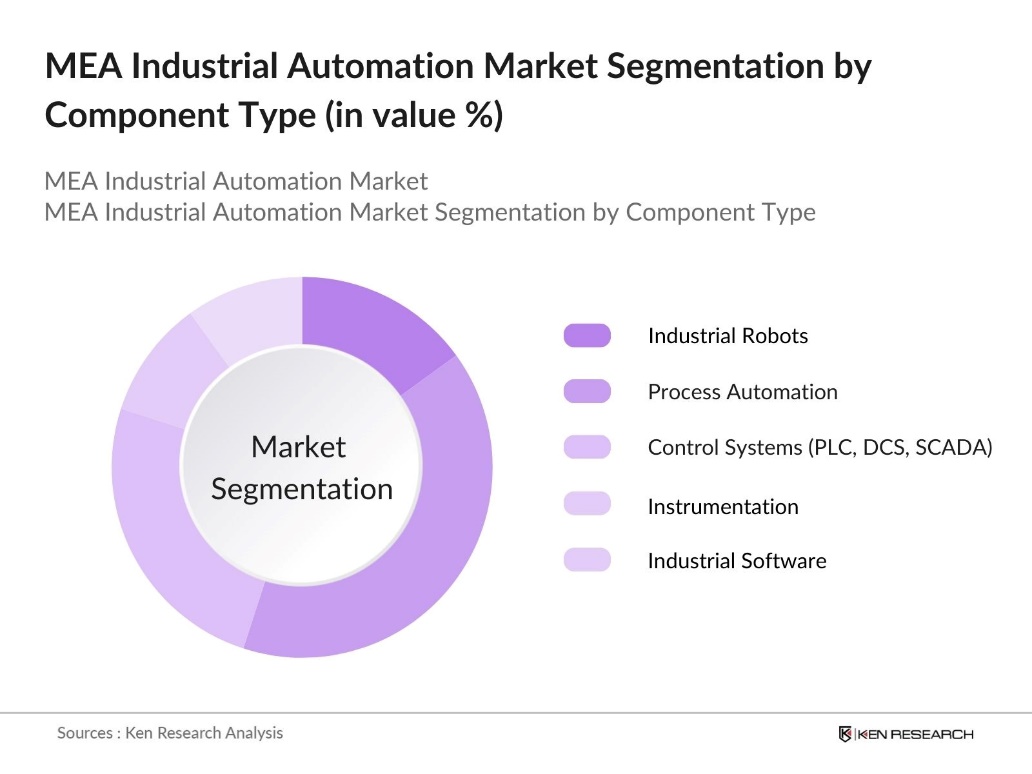

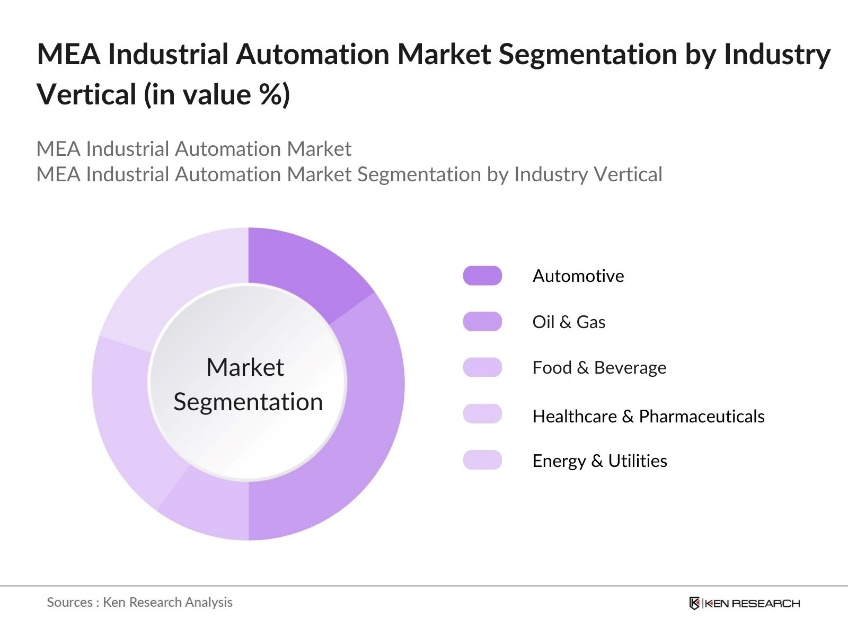

MEA Industrial Automation Market Segmentation

By Component Type: The market is segmented by component type into industrial robots, process automation solutions, control systems, instrumentation, and industrial software. Among these, process automation solutions hold a dominant market share. The demand for process automation is growing due to its ability to integrate and streamline operations across various industries, particularly in oil & gas and manufacturing, where continuous processes benefit significantly from automation.

By Industry Vertical: The market is segmented by industry vertical into automotive, oil & gas, food & beverage, healthcare & pharmaceuticals, and energy & utilities. The oil & gas sector holds the largest market share, largely due to the high demand for automation in offshore drilling, refining, and processing operations. Automation reduces human error and improves operational safety, which is critical in high-risk environments like oil platforms.

MEA Industrial Automation Market Competitive Landscape

he MEA industrial automation market is dominated by both global giants and regional players, leading to a competitive landscape marked by the integration of cutting-edge technology and strategic partnerships. Major players such as Siemens AG, Schneider Electric, and ABB Ltd have a strong foothold in the region due to their extensive product portfolios and robust service networks. The market is also seeing increasing competition from local companies in sectors like oil & gas, who are capitalizing on their deep understanding of regional needs.

MEA Industrial Automation Industry Analysis

Growth Drivers

- Increased Adoption of Smart Technologies (IIoT, AI): The integration of Industrial Internet of Things (IIoT) and Artificial Intelligence (AI) is transforming the MEA industrial automation market. According to the IBM Global AI Adoption Index 2023, 42% of businesses in the UAE are actively using AI in their operations, enhancing operational efficiency and predictive maintenance. Across the region, IIoT implementations are expected to contribute to reduced operational downtime and optimizing energy consumption and equipment life cycles.

- Expansion of Energy and Utility Sectors: The energy and utility sectors in the MEA region are pivotal in driving the demand for industrial automation solutions. Countries like Qatar and the UAE have invested billions in smart grids and automation technologies to enhance energy distribution efficiency. The Qatar General Electricity and Water Corporation (Kahramaa) has initiated projects to install 600,000 smart meters by the end of 2023. Moreover, the UAEs push toward renewable energy sources has led to significant investment in automation systems for solar and wind power plants.

- Rise in Manufacturing Investments: Manufacturing investments in the Middle East and Africa (MEA) have surged, driven by government-led initiatives to enhance industrial productivity and economic diversification. Programs like Saudi Arabia's Vision 2030 and the UAE's Operation 300bn focus on integrating automation to boost efficiency and reduce import reliance. Additionally, foreign direct investment is helping accelerate industrial growth, especially in countries like South Africa and Egypt.

Market Challenges

- High Capital Expenditure (CAPEX): One of the primary challenges in the MEA industrial automation market is the high upfront cost of implementing automation systems. Technologies like robotics and AI-driven machinery require significant capital investment, which can be a major hurdle, particularly for small and medium-sized enterprises (SMEs). Limited access to financing further exacerbates the issue, making it difficult for these businesses to adopt automation solutions and enhance productivity.

- Interoperability and Integration Issues: In the MEA region, the lack of standardized protocols for automation systems leads to interoperability challenges, especially when integrating new technologies with existing infrastructure. These integration issues can cause operational disruptions, resulting in inefficiencies and increased costs for industries such as petrochemicals and automotive manufacturing, where seamless system integration is crucial for maintaining productivity.

MEA Industrial Automation Market Future Outlook

Over the coming years, the MEA industrial automation market is anticipated to experience robust growth, driven by increasing investments in smart infrastructure, government support for Industry 4.0 initiatives, and the adoption of energy-efficient automation technologies. This growth will be further propelled by advancements in robotics, artificial intelligence, and IIoT, which will enable companies to achieve significant operational efficiency while reducing downtime and labor costs.

Market Opportunities

- Growing Demand for Energy-Efficient Solutions: As energy costs rise, industries in the MEA region are increasingly adopting energy-efficient automation technologies to reduce operational expenses and comply with emerging regulations. Governments are encouraging investments in energy-saving solutions such as automated systems for heating, ventilation, and air conditioning (HVAC) and smart lighting. These technologies are becoming essential for companies aiming to enhance sustainability and lower energy consumption in their industrial processes.

- Emergence of Robotics and Automation in SMEs: Small and medium-sized enterprises (SMEs) in the MEA region are gradually embracing robotics and automation to boost efficiency and competitiveness. Traditionally dominated by large industries, automation is now being integrated into SMEs, particularly in sectors like textiles, plastics, and food processing. Support from government programs and training initiatives has helped these businesses adopt basic robotic solutions, improving their overall productivity and operational capabilities.

Scope of the Report

|

Component Type |

Industrial Robots Process Automation Solutions Control Systems (PLC, DCS, SCADA) Instrumentation (Sensors, Actuators, Valves) Industrial Software (MES, HMI) |

|

Industry Vertical |

Automotive Oil & Gas Food & Beverage Healthcare and Pharmaceuticals Energy and Utilities |

|

Technology |

Industrial Internet of Things (IIoT) Machine Vision Systems Human-Machine Interface (HMI) Industrial Cloud Platforms |

|

Solution Type |

Hardware Software Services (Installation, Maintenance, Training) |

|

Region |

Gulf Cooperation Council (GCC) North Sub-Saharan East |

Products

Key Target Audience

Oil & Gas Companies

Manufacturing Companies

Healthcare and Pharmaceutical Companies

Logistics and Supply Chain Firms

Government and Regulatory Bodies (e.g., UAE Ministry of Industry, Saudi Industrial Development Fund)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Siemens AG

Schneider Electric

ABB Ltd

Emerson Electric Co.

Mitsubishi Electric Corporation

Honeywell International Inc.

Rockwell Automation

Yokogawa Electric Corporation

Fanuc Corporation

Bosch Rexroth

Table of Contents

1. MEA Industrial Automation Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. MEA Industrial Automation Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. MEA Industrial Automation Market Analysis

3.1. Growth Drivers

3.1.1. Rise in Manufacturing Investments

3.1.2. Increased Adoption of Smart Technologies (IIoT, AI)

3.1.3. Government Policies Promoting Industry 4.0

3.1.4. Expansion of Energy and Utility Sectors

3.2. Market Challenges

3.2.1. High Capital Expenditure (CAPEX)

3.2.2. Interoperability and Integration Issues

3.2.3. Lack of Skilled Workforce for Automation

3.3. Opportunities

3.3.1. Growing Demand for Energy-Efficient Solutions

3.3.2. Emergence of Robotics and Automation in SMEs

3.3.3. Government Funding for Digital Transformation

3.4. Trends

3.4.1. Increasing Use of Artificial Intelligence and Machine Learning

3.4.2. Shift to Decentralized Manufacturing Systems

3.4.3. Advanced Robotics and Automation in Logistics

3.5. Government Regulation

3.5.1. Industry 4.0 Initiatives (National and Regional Programs)

3.5.2. Energy Efficiency Regulations for Automation Technologies

3.5.3. Data Security and Compliance in Automation Systems

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. MEA Industrial Automation Market Segmentation

4.1. By Component Type (In Value %)

4.1.1. Industrial Robots

4.1.2. Process Automation Solutions

4.1.3. Control Systems (PLC, DCS, SCADA

4.1.4. Instrumentation (Sensors, Actuators, Valves)

4.1.5. Industrial Software (MES, HMI)

4.2. By Industry Vertical (In Value %)

4.2.1. Automotive

4.2.2. Oil & Gas

4.2.3. Food & Beverage

4.2.4. Healthcare and Pharmaceuticals

4.2.5. Energy and Utilities

4.3. By Technology (In Value %)

4.3.1. Industrial Internet of Things (IIoT)

4.3.2. Machine Vision Systems

4.3.3. Human-Machine Interface (HMI)

4.3.4. Industrial Cloud Platforms

4.4. By Solution Type (In Value %)

4.4.1. Hardware

4.4.2. Software

4.4.3. Services (Installation, Maintenance, Training)

4.5. By Region (In Value %)

4.5.1. Gulf Cooperation Council (GCC)

4.5.2. North Africa

4.5.3. Sub-Saharan Africa

4.5.4. East Africa

5. MEA Industrial Automation Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Siemens AG

5.1.2. Schneider Electric

5.1.3. ABB Ltd.

5.1.4. Rockwell Automation

5.1.5. Honeywell International Inc.

5.1.6. Emerson Electric Co.

5.1.7. Mitsubishi Electric Corporation

5.1.8. Yokogawa Electric Corporation

5.1.9. Bosch Rexroth

5.1.10. Omron Corporation

5.1.11. Fanuc Corporation

5.1.12. GE Automation

5.1.13. ABB Robotics

5.1.14. Endress+Hauser Group

5.1.15. Danfoss Group

5.2. Cross Comparison Parameters (Automation Capabilities, Global Reach, Industrial Verticals Served, Innovation Index, Revenue, Workforce Strength, Headquarters, Market Penetration)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Alliances, and Joint Ventures)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital and Private Equity Funding

5.8. Government Grants and Subsidies

6. MEA Industrial Automation Market Regulatory Framework

6.1. Industrial Safety Standards (Occupational Safety Standards, Machine Safety)

6.2. Compliance Requirements (Automation System Compliance, Data Privacy Regulations)

6.3. Certification Processes (Automation Standards ISO/IEC 61508, IEC 61131)

7. MEA Industrial Automation Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. MEA Industrial Automation Future Market Segmentation

8.1. By Component Type (In Value %)

8.2. By Industry Vertical (In Value %)

8.3. By Technology (In Value %)

8.4. By Solution Type (In Value %)

8.5. By Region (In Value %)

9. MEA Industrial Automation Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Automation Integration Strategies

9.3. Market Expansion Tactics in Key Industry Verticals

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In this phase, an ecosystem map was constructed to identify all major stakeholders in the MEA industrial automation market. This involved detailed desk research utilizing various databases to define critical market variables and assess their influence on market dynamics.

Step 2: Market Analysis and Construction

Historical market data was compiled to evaluate the market penetration of automation technologies. The analysis focused on the rate of adoption across different verticals, revenue generation, and the quality of automation solutions being deployed in the region.

Step 3: Hypothesis Validation and Expert Consultation

Interviews were conducted with industry professionals and automation specialists to validate market hypotheses. This process provided operational and financial insights, refining our market forecasts and confirming the reliability of collected data.

Step 4: Research Synthesis and Final Output

In the final stage, key automation manufacturers and solution providers were consulted to provide detailed insights into product performance, market trends, and consumer preferences. This bottom-up approach ensured that the final report was comprehensive and accurately reflected the markets trajectory.

Frequently Asked Questions

01. How big is the MEA Industrial Automation Market?

The MEA industrial automation market is valued at approximately USD 12.82 billion, driven by significant investments in smart manufacturing and energy-efficient technologies, particularly in oil & gas, utilities, and manufacturing.

02. What are the key challenges in the MEA Industrial Automation Market?

Key challenges in MEA industrial automation market include high capital expenditure, a lack of skilled workforce, and interoperability issues between different automation systems. These factors can slow down the adoption of advanced automation technologies.

03. Who are the major players in the MEA Industrial Automation Market?

Key players in MEA industrial automation market include Siemens AG, Schneider Electric, ABB Ltd, Emerson Electric, and Mitsubishi Electric. These companies dominate the market due to their extensive portfolios and global service networks.

04. What is driving growth in the MEA Industrial Automation Market?

The MEA industrial automation market growth is driven by increasing demand for operational efficiency, the rise of Industry 4.0 initiatives, and government support for the digitization of industries, especially in the oil & gas and energy sectors.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.