MEA Pet Food Market Outlook to 2030

Region:Global

Author(s):Shreya Garg

Product Code:KROD9094

December 2024

90

About the Report

MEA Pet Food Market Overview

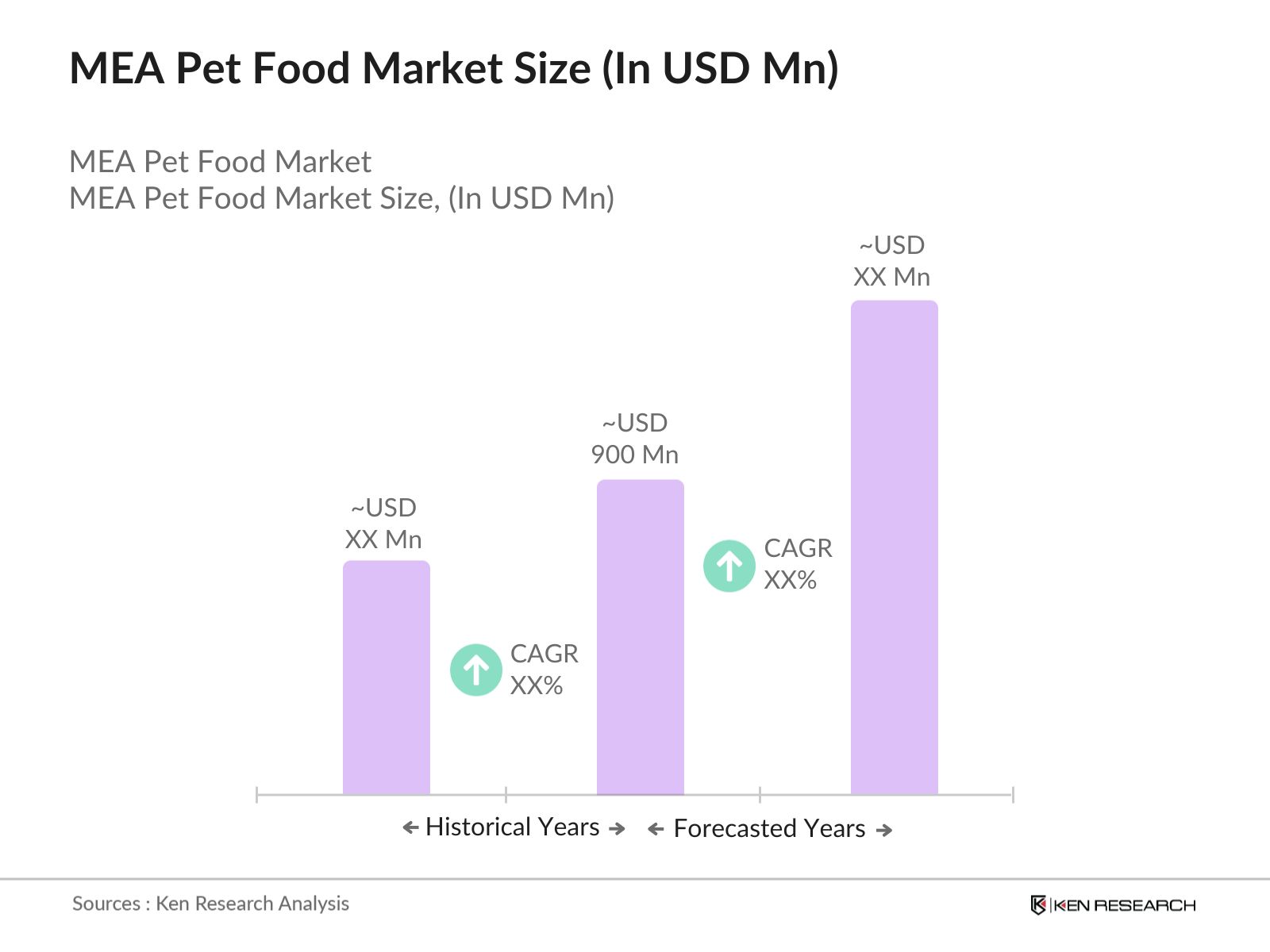

- The MEA pet food market is valued at USD 900 million based on a five-year historical analysis. The growth in the pet food market is primarily driven by the increasing pet ownership across urban regions and a growing middle-class population. There is a notable rise in consumer spending on premium pet food, including organic and grain-free products, due to heightened awareness about pet nutrition. The availability of specialized pet products through both traditional and e-commerce channels further enhances market demand.

- The MEA pet food market is primarily dominated by countries like the UAE and Saudi Arabia in the GCC region, and South Africa in Sub-Saharan Africa. The dominance of these regions is largely attributed to high pet ownership rates, a growing urban population, and higher disposable incomes. Additionally, strong import networks in these regions facilitate easy access to international pet food brands, contributing to their market dominance. Saudi Arabia and the UAE also benefit from a well-established retail infrastructure and strong e-commerce penetration.

- The MEA pet food market is influenced by various trade agreements and tariffs that affect the import and export of pet food products. For instance, the African Continental Free Trade Area (AfCFTA), implemented in 2021, aims to reduce tariffs between African countries, facilitating easier trade of pet food products across borders. However, countries like Egypt and Kenya still impose import tariffs on pet food, which affect the cost and availability of products. Such agreements and regulations play a key role in shaping the market, impacting how companies navigate cross-border trade.

MEA Pet Food Market Segmentation

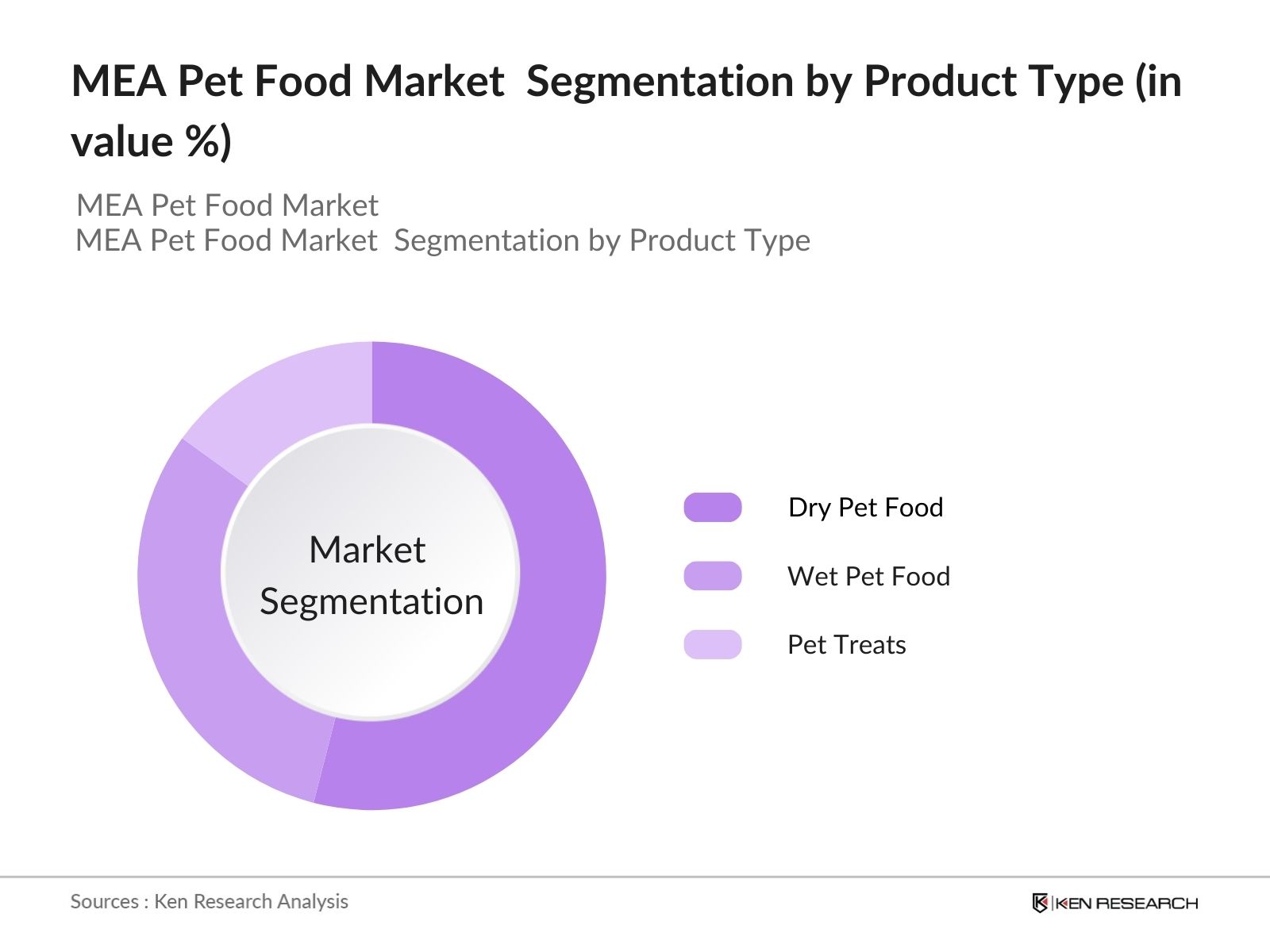

By Product Type: The market is segmented by product type into dry pet food, wet pet food, and pet treats. Recently, dry pet food has a dominant market share under the product type segment. This dominance is due to the long shelf life, convenience of storage, and cost-effectiveness of dry food products. Many consumers in the region prefer dry food for its affordability and ease of distribution, particularly in countries where large quantities are consumed.

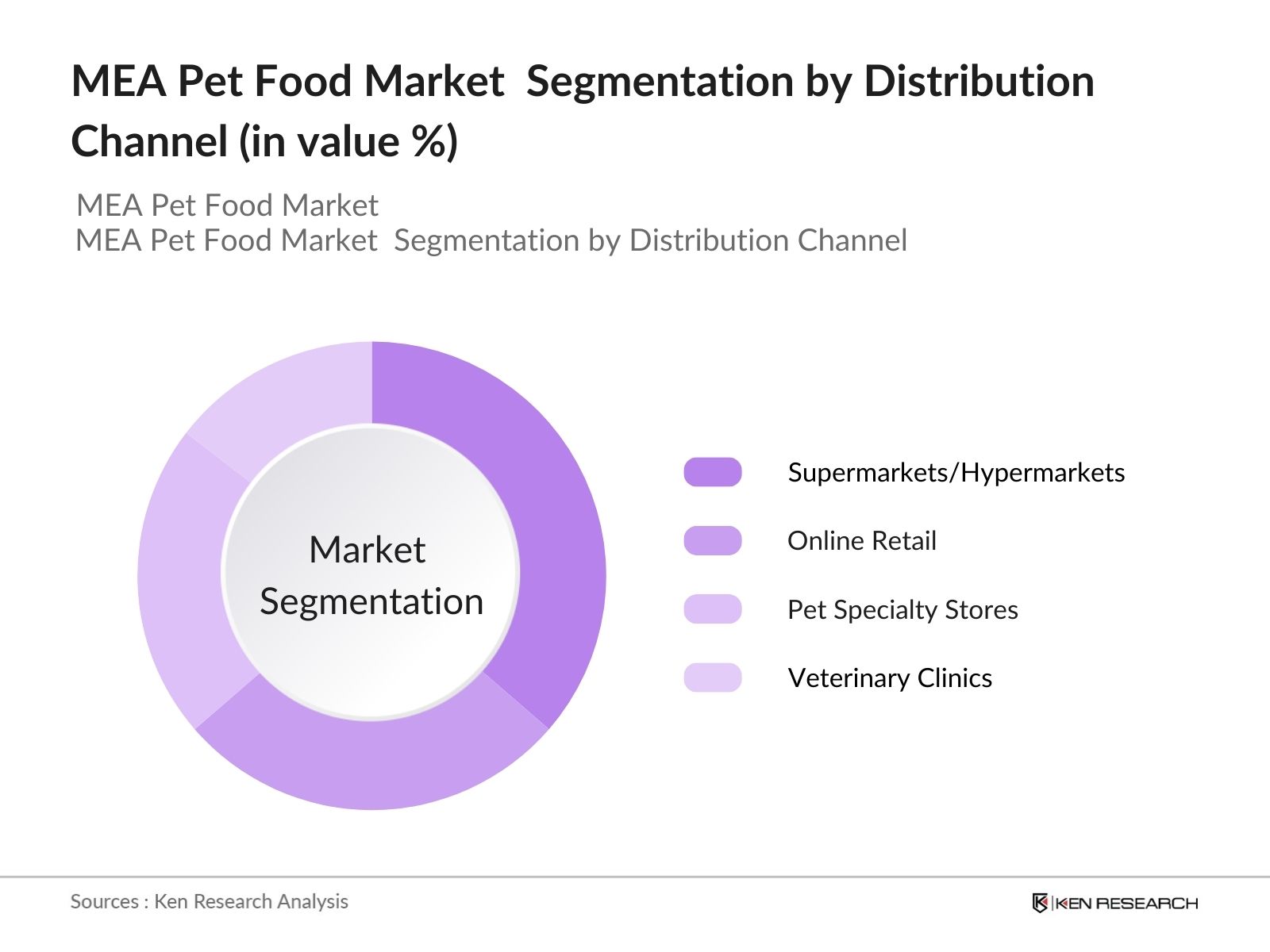

By Distribution Channel: The market is also segmented by distribution channels into supermarkets/hypermarkets, online retail, pet specialty stores, and veterinary clinics. Supermarkets and hypermarkets hold a dominant position in the market. This is due to their widespread presence across urban and semi-urban areas, providing consumers with convenient access to a variety of pet food options. These stores also offer promotions and discounts, making them popular choices among budget-conscious consumers.

MEA Pet Food Market Competitive Landscape

The MEA pet food market is dominated by both local manufacturers and international players. The market is characterized by the strong presence of established brands that have built customer loyalty through high-quality products. Local manufacturers are increasingly competing by offering region-specific products, while international players dominate premium segments. The rising trend of organic and natural pet food is also seeing several small niche brands gaining market share.

|

Company |

Establishment Year |

Headquarters |

No. of Employees |

Revenue (USD) |

Product Range |

Distribution Channels |

R&D Focus |

Market Share |

|

Mars, Inc. |

1911 |

McLean, USA |

||||||

|

Nestl Purina PetCare |

1894 |

Vevey, Switzerland |

||||||

|

Hill's Pet Nutrition |

1907 |

Topeka, USA |

||||||

|

Royal Canin |

1968 |

Aimargues, France |

||||||

|

Farmina Pet Foods |

1965 |

Naples, Italy |

MEA Pet Food Industry Analysis

Growth Drivers

- Increasing Pet Adoption Rates: The Middle East and Africa (MEA) region has seen a notable rise in pet ownership, particularly in urban centers. For example, Saudi Arabia and the UAE have witnessed a significant increase in households owning pets, with the UAE pet ownership rate rising to approximately 14% in urban areas in 2023. South Africa, one of the largest markets in the region, reported more than 9 million households owning pets by 2022. This increase in pet adoption contributes to the rising demand for pet food, stimulating the markets growth. As per World Bank, the urban population in the Middle East has also surged, creating further opportunities in urban areas for the pet food industry.

- Shifting Consumer Preferences Towards Premium Products: In the MEA region, consumer preferences are shifting toward premium pet food products. As of 2023, there has been growing demand for grain-free and organic pet foods, driven by increasing disposable income and awareness of healthier pet food options. Premium products now make up a substantial portion of the pet food market in affluent regions like the UAE, where consumer spending on pet care has risen alongside GDP growth rates. Organic pet food options have become particularly popular, with over 5% of pet food sales in Saudi Arabia being organic or grain-free, according to local reports.

- Rising Awareness on Pet Nutrition: There is a growing awareness among pet owners in MEA regarding pet nutrition, with more focus on the nutritional composition of pet food products. Governments are playing a significant role by implementing regulatory standards that require companies to meet specific nutritional content guidelines. For instance, in South Africa, the regulatory requirements under the Fertilizers, Farm Feeds, Agricultural Remedies and Stock Remedies Act (Act 36 of 1947) mandate that pet foods meet certain nutritional and quality standards. This increasing focus on proper pet nutrition has spurred the demand for nutritionally enhanced products. Source.

Market Challenges

- Low Penetration of Specialized Pet Products: Although pet ownership is increasing, the per capita consumption of specialized pet products remains relatively low in the MEA region. For example, pet food consumption per capita in countries like Morocco and Nigeria is significantly lower compared to Western markets, averaging only around 5 kg per year, according to recent industry reports. Consumers are still primarily focused on basic pet food, with limited adoption of specialized or premium products. This is compounded by lower awareness and purchasing power in many parts of Africa.

- Stringent Import and Quality Regulations: The importation of pet food products in the MEA region faces stringent regulatory hurdles. Many countries have implemented strict quality and safety standards to ensure that imported products meet local health regulations. For instance, in South Africa, pet food imports must comply with the Fertilizers, Farm Feeds, Agricultural Remedies and Stock Remedies Act, which adds additional costs for manufacturers to meet local guidelines. Similarly, Saudi Arabia's Saudi Food and Drug Authority (SFDA) requires rigorous testing and certification for imported pet foods, creating barriers for new entrants in the market.

MEA Pet Food Market Future Outlook

The MEA pet food market is expected to show significant growth driven by increasing pet ownership rates, urbanization, and rising awareness about pet nutrition. The growing availability of premium, organic, and natural pet food products is expected to drive higher consumer spending in the market. Additionally, the rise of online retail and direct-to-consumer sales models will provide further growth opportunities, especially for niche brands targeting health-conscious pet owners. The ongoing shift toward sustainability, with brands adopting eco-friendly packaging and sourcing ingredients ethically, will further shape the market's development.

Future Market Opportunities

Expansion into Untapped Regions: The MEA region offers untapped opportunities, particularly in sub-Saharan Africa and rural areas of the Middle East. For instance, Nigeria and Ethiopia, with large populations and increasing urbanization, represent emerging markets for pet food products. As of 2023, Nigeria alone is home to over 220 million people, many of whom are migrating to cities, leading to a growth in pet ownership and a corresponding rise in pet food demand. The African Development Banks reports on economic expansion in these regions highlight growing consumer markets that international pet food companies can explore.

Growth in E-Commerce Distribution: The rise of e-commerce platforms in the MEA region has created new distribution channels for pet food products. In 2024, more than 60% of consumers in urban centers like Dubai and Johannesburg now prefer to purchase pet food online, utilizing platforms such as Jumia and Amazons regional sites. These digital marketplaces provide opportunities for pet food companies to reach a broader audience without the need for physical stores. Additionally, subscription-based services for pet food, which guarantee monthly deliveries, are growing in popularity, particularly among affluent households in cities like Riyadh.

Scope of the Report

|

By Product Type |

Dry Pet Food Wet Pet Food Treats and Snacks Raw/Freeze-Dried Pet Food |

|

By Animal Type |

Dogs Cats Birds Others (Fish, Small Mammals) |

|

By Ingredient Type |

Animal-Based Plant-Based Grain-Free Organic Ingredients |

|

By Distribution Channel |

Online Retail Supermarkets/Hypermarkets Pet Specialty Stores Veterinary Clinics |

|

By Region |

GCC North Africa Sub-Saharan Africa Levant |

Products

Key Target Audience

Pet Food Manufacturers

Pet Specialty Retailers

Veterinary Clinics

Pet Owners Associations

Logistics and Supply Chain Providers

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (Saudi Food and Drug Authority, UAE Ministry of Climate Change and Environment)

E-Commerce Platforms

Companies

Major Players

Mars, Inc.

Nestl Purina PetCare

Hill's Pet Nutrition

Royal Canin

Farmina Pet Foods

Blue Buffalo

The J.M. Smucker Company

Champion Petfoods

Affinity Petcare

Orijen

Spectrum Brands

Monge & C. S.p.A

Pet Line S.A.E.

Petco

ZuPreem

Table of Contents

1. MEA Pet Food Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. MEA Pet Food Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

2.4. Market Share by Major Players (Revenue, Product Mix)

3. MEA Pet Food Market Analysis

3.1. Growth Drivers

Increasing Pet Adoption Rates (Region-Specific Pet Ownership Statistics)

Shifting Consumer Preferences Towards Premium Products (Organic, Grain-Free, etc.)

Rising Awareness on Pet Nutrition (Nutritional Composition, Regulatory Requirements)

3.2. Market Challenges

High Import Costs of Raw Materials (Supply Chain Issues, Logistics Costs)

Low Penetration of Specialized Pet Products (Per Capita Pet Food Consumption, Consumer Behavior)

Stringent Import and Quality Regulations (Local Regulatory Standards)

3.3. Opportunities

Expansion into Untapped Regions (Geographic Opportunities in Africa & Middle East)

Growth in E-Commerce Distribution (Digital Marketplaces, Pet Food Subscriptions)

Customization and Personalized Pet Nutrition (Market for Tailored Diets)

3.4. Trends

Growing Popularity of Natural and Organic Pet Food (Consumer Health Consciousness, Ingredient Preferences)

Rise of Pet Treats and Functional Foods (Nutraceutical Trends in Pet Food)

Sustainable Packaging Initiatives (Market Push Towards Eco-Friendly Materials)

3.5. Government Regulations

Food Safety and Animal Feed Standards (Regulatory Bodies, Certification Processes)

Veterinary and Health Certification for Pet Food (Regulatory Compliance for Imports)

Trade Agreements Affecting Pet Food Import/Export (Tariffs and Bilateral Agreements)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Distributors, Pet Specialty Retailers)

3.8. Porters Five Forces Analysis (Supplier Power, Buyer Power, Threat of Substitutes, etc.)

3.9. Competitive Ecosystem (Local vs. International Players)

4. MEA Pet Food Market Segmentation

4.1. By Product Type (In Value %)

Dry Pet Food

Wet Pet Food

Treats and Snacks

Raw/Freeze-Dried Pet Food

4.2. By Animal Type (In Value %)

Dogs

Cats

Birds

Others (Fish, Small Mammals)

4.3. By Ingredient Type (In Value %)

Animal-Based

Plant-Based

Grain-Free

Organic Ingredients

4.4. By Distribution Channel (In Value %)

Online Retail

Supermarkets/Hypermarkets

Pet Specialty Stores

Veterinary Clinics

4.5. By Region (In Value %)

GCC

North Africa

Sub-Saharan Africa

Levant

5. MEA Pet Food Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

Mars, Inc.

Nestl Purina PetCare

Hill's Pet Nutrition

Royal Canin

Blue Buffalo

The J.M. Smucker Company

Champion Petfoods

Affinity Petcare

Orijen

Spectrum Brands

Monge & C. S.p.A

Farmina Pet Foods

Pet Line S.A.E.

Petco

ZuPreem

5.2. Cross Comparison Parameters (Product Portfolio, Manufacturing Locations, Distribution Network, Sustainability Initiatives, Product Certifications, Revenue, Market Penetration)

5.3. Market Share Analysis (Top Players, Local Brands)

5.4. Strategic Initiatives (Expansion Plans, Brand Partnerships, Product Launches)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital and Private Equity Investments

5.8. Government Support and Incentives (Subsidies, Grants for Local Manufacturers)

6. MEA Pet Food Market Regulatory Framework

6.1. Food Safety Standards (Regulatory Bodies, Compliance Levels)

6.2. Labeling Requirements (Nutritional Information, Ingredient Lists)

6.3. Import Tariffs and Trade Restrictions (By Region, Specific Ingredients)

7. MEA Pet Food Future Market Size (In USD Mn)

7.1. Market Size Projections

7.2. Key Factors Driving Future Market Growth

Urbanization and Rise in Pet Ownership

Innovations in Pet Food Formulation

8. MEA Pet Food Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Animal Type (In Value %)

8.3. By Ingredient Type (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. MEA Pet Food Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Cohort Analysis (Pet Ownership Segmentation, Buyer Personas)

9.3. Brand Positioning Strategy

9.4. White Space Opportunity Analysis (Product Innovation Areas)

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first step involved mapping the ecosystem of the MEA pet food market by identifying key stakeholders, including manufacturers, distributors, and consumers. This step was facilitated by in-depth desk research, analyzing existing reports, government publications, and industry white papers to collect relevant data on the market's key variables.

Step 2: Market Analysis and Construction

This step involved collecting and analyzing historical data on the MEA pet food market, including market penetration, sales volumes, and consumer preferences. This analysis also took into consideration market growth drivers such as urbanization, pet ownership rates, and changing consumer behavior towards pet health.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations were conducted with industry professionals from pet food manufacturing companies, distribution networks, and veterinary associations. These consultations provided qualitative insights and helped validate quantitative data, particularly on product demand and supply chain efficiencies.

Step 4: Research Synthesis and Final Output

The final step involved synthesizing the data collected from secondary and primary research to produce a comprehensive analysis of the MEA pet food market. This phase ensured that the market forecasts were accurate and reflective of the current market dynamics.

Frequently Asked Questions

01. How big is the MEA Pet Food Market?

The MEA pet food market is valued at USD 900 Mn, driven by increasing pet ownership rates and rising consumer awareness about pet nutrition across key countries like Saudi Arabia, UAE, and South Africa.

02. What are the challenges in the MEA Pet Food Market?

The main challenges in the MEA pet food market include high import costs of raw materials, 900 million regulatory compliance requirements, and the limited availability of specialized pet products in certain regions. Additionally, logistical challenges in certain parts of the region further complicate distribution.

03. Who are the major players in the MEA Pet Food Market?

Major players in the MEA pet food market include Mars, Inc., Nestl Purina PetCare, Hill's Pet Nutrition, Royal Canin, and Farmina Pet Foods. These companies dominate the market due to their strong product portfolios and extensive distribution networks.

04. What are the growth drivers of the MEA Pet Food Market?

The MEA pet food market is driven by increasing pet ownership, rising disposable incomes, and growing awareness of the nutritional needs of pets. Additionally, the expansion of e-commerce platforms offering a wide variety of pet food products has also contributed to market growth.

05. Which countries dominate the MEA Pet Food Market?

Countries like Saudi Arabia, UAE, and South Africa dominate the MEA pet food market due to high pet ownership rates, strong retail infrastructure, and consumer spending power. These countries have a well-developed import network that allows access to premium international pet food brands.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.