MEA Polyolefin Market Outlook to 2030

Region:Africa

Author(s):Shreya

Product Code:KROD3048

Region:Africa

Author(s):Shreya

Product Code:KROD3048

November 2024

90

The MEA Polyolefin market is dominated by a few major players, including global and regional companies such as SABIC, Borouge, and LyondellBasell. These companies are well-established within the region, and their extensive production capabilities, along with a focus on sustainability and innovation, allow them to maintain significant market shares. The competitive landscape is shaped by major petrochemical companies that have vertical integration and access to key raw materials, thus ensuring cost-effective production.

|

Company |

Year of Establishment |

Headquarters |

Revenue (USD Bn) |

Production Capacity (Tons) |

Geographic Reach |

R&D Investment (USD Mn) |

Sustainability Initiatives |

Strategic Partnerships |

Product Innovation |

|---|---|---|---|---|---|---|---|---|---|

|

SABIC |

1976 |

Riyadh, Saudi Arabia |

|||||||

|

Borouge |

1998 |

Abu Dhabi, UAE |

|||||||

|

LyondellBasell |

1985 |

Houston, USA |

|||||||

|

ExxonMobil Corporation |

1870 |

Irving, USA |

|||||||

|

Dow Inc. |

1897 |

Midland, USA |

Increasing Demand for Packaging: The polyolefin market in the MEA region is driven by the growing demand for sustainable packaging solutions. As of 2024, global demand for eco-friendly packaging materials is at 62 million tons, with the MEA region contributing around 7 million tons to this figure. Consumer goods packaging is a key driver, supported by a significant increase in e-commerce, which saw 2.1 billion packages shipped in the region in 2023. Governments in the UAE and Saudi Arabia are introducing stricter regulations on single-use plastics, further pushing demand for sustainable packaging.

Volatility in Crude Oil Prices: Polyolefin production relies heavily on crude oil, and the MEA market faces challenges due to fluctuating oil prices. In 2023, crude oil prices ranged between 75 to 95 USD per barrel, making raw material costs for polyolefin production highly volatile. This price instability impacts profit margins and supply chain reliability for polyolefin manufacturers, particularly in countries like Saudi Arabia and the UAE, where oil contributes to a significant portion of the economy. This ongoing volatility poses a critical challenge for the growth of the polyolefin market in the region.

Over the next five years, the MEA Polyolefin market is expected to experience substantial growth, driven by rising demand for sustainable packaging solutions, technological advancements in production, and an increase in automotive manufacturing across the region. In addition, the construction sector in key markets like Saudi Arabia and the UAE will continue to drive demand for polyolefins in pipes and insulation applications. The focus on recycling and sustainability will also push companies to innovate in the production of eco-friendly and circular polyolefins, creating significant growth opportunities.

|

Segment |

Sub-segments |

|---|---|

|

Type |

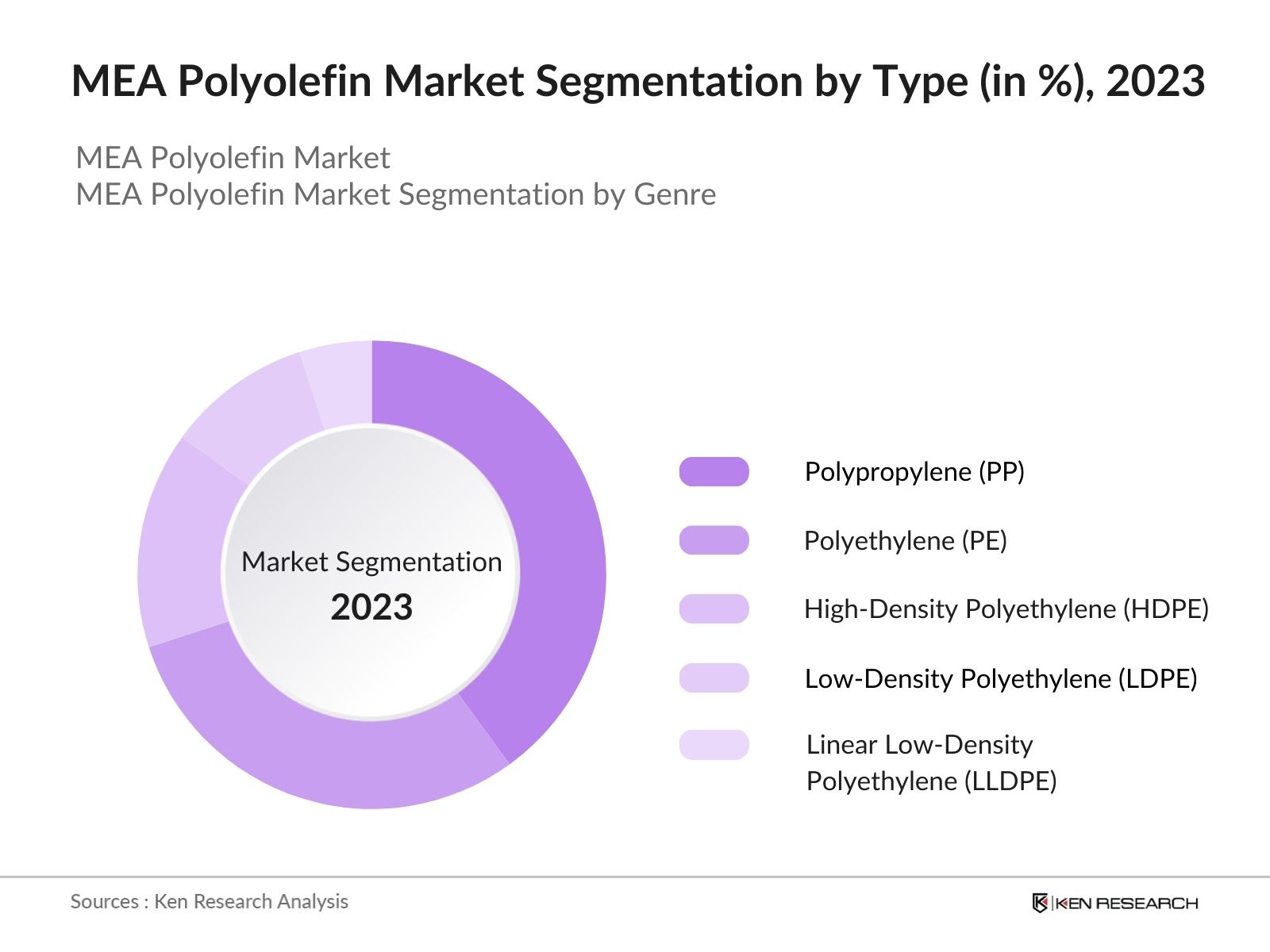

Polyethylene (PE) Polypropylene (PP) LLDPE HDPE LDPE |

|

Application |

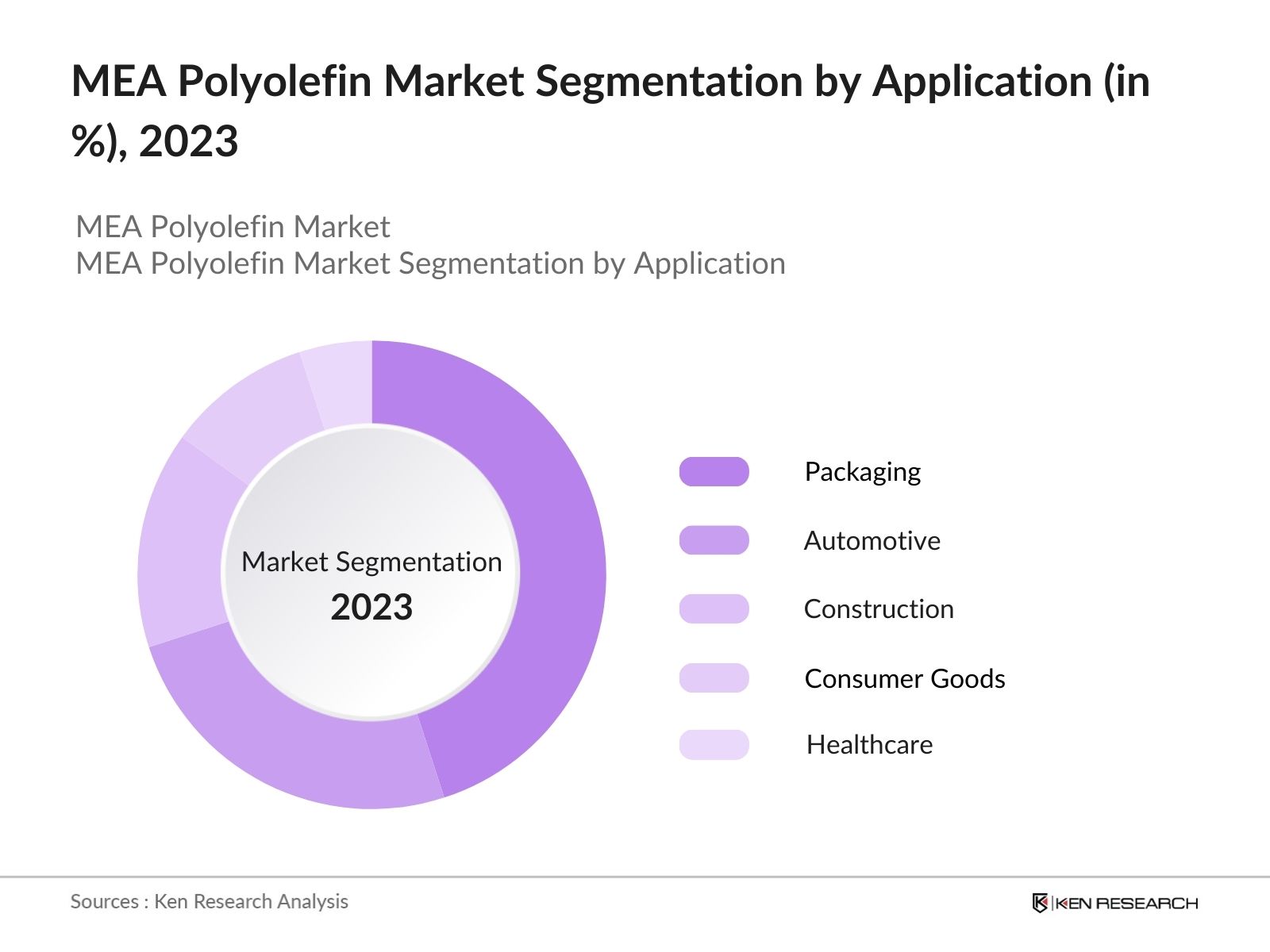

Packaging Automotive Construction Consumer Goods Healthcare |

|

End-User Industry |

Industrial Residential Commercial |

|

Processing Technology |

Injection Molding Blow Molding Extrusion Film Processing |

|

Region |

GCC Countries North Africa Sub-Saharan Africa Levant |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Polyethylene, Polypropylene, Linear Low-Density Polyethylene)

1.4. Market Segmentation Overview (By Type, By Application, By End-User)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis (Volume, Value)

2.3. Key Market Developments and Milestones (Raw Material Supply, Production Capacity)

3.1. Growth Drivers

3.1.1. Increasing Demand for Packaging (Sustainability, Consumer Goods)

3.1.2. Construction Sector Expansion (Pipes, Insulation)

3.1.3. Automotive Industry Growth (Lightweighting, Fuel Efficiency)

3.1.4. Government Infrastructure Projects

3.2. Market Challenges

3.2.1. Volatility in Crude Oil Prices

3.2.2. Environmental Regulations (Plastic Waste Management)

3.2.3. Competition from Biodegradable Alternatives

3.2.4. Limited Recycling Infrastructure

3.3. Opportunities

3.3.1. Technological Advancements in Production Processes

3.3.2. Rising Adoption of Sustainable Packaging Solutions

3.3.3. Expansion of Manufacturing Capacity in Emerging Markets

3.3.4. Development of New Applications in Agriculture and Healthcare

3.4. Trends

3.4.1. Increasing Use of Recycled Polyolefins

3.4.2. Integration of Digital Technology in Production (Automation, AI)

3.4.3. Growth of Polyolefin Composites

3.4.4. Innovation in High-Performance Polyolefin Grades

3.5. Government Regulation

3.5.1. Regional Environmental Laws (Plastic Waste, Emission Norms)

3.5.2. Incentives for Sustainable Packaging Solutions

3.5.3. Import/Export Tariffs and Trade Policies

3.5.4. Energy Efficiency Standards for Manufacturing

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Type (In Value %)

4.1.1. Polyethylene (PE)

4.1.2. Polypropylene (PP)

4.1.3. Linear Low-Density Polyethylene (LLDPE)

4.1.4. High-Density Polyethylene (HDPE)

4.1.5. Low-Density Polyethylene (LDPE)

4.2. By Application (In Value %)

4.2.1. Packaging

4.2.2. Automotive

4.2.3. Construction

4.2.4. Consumer Goods

4.2.5. Healthcare

4.3. By End-User Industry (In Value %)

4.3.1. Industrial

4.3.2. Residential

4.3.3. Commercial

4.4. By Processing Technology (In Value %)

4.4.1. Injection Molding

4.4.2. Blow Molding

4.4.3. Extrusion

4.4.4. Film Processing

4.5. By Region (In Value %)

4.5.1. GCC Countries

4.5.2. North Africa

4.5.3. Sub-Saharan Africa

4.5.4. Levant Region

5.1. Detailed Profiles of Major Companies

5.1.1. Saudi Basic Industries Corporation (SABIC)

5.1.2. Borouge

5.1.3. LyondellBasell Industries

5.1.4. Reliance Industries Limited

5.1.5. TotalEnergies

5.1.6. ExxonMobil Corporation

5.1.7. INEOS Group Holdings S.A.

5.1.8. Dow Inc.

5.1.9. Braskem

5.1.10. Sasol Limited

5.1.11. Chevron Phillips Chemical Company

5.1.12. Mitsubishi Chemical Holdings

5.1.13. Formosa Plastics Corporation

5.1.14. China Petroleum & Chemical Corporation (Sinopec)

5.1.15. LG Chem

5.2. Cross Comparison Parameters (Revenue, Production Capacity, Geographic Presence, Sustainability Initiatives, Number of Patents, Product Innovation, Strategic Partnerships, R&D Investment)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards for Plastic Waste

6.2. Compliance Requirements for Packaging Materials

6.3. Certification Processes for Polyolefin Products

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Innovation, Investment, Policy Changes)

8.1. By Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User Industry (In Value %)

8.4. By Processing Technology (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The research began by constructing an ecosystem map of the MEA Polyolefin market, covering all major stakeholders. Extensive desk research was undertaken to gather industry-level data using secondary sources and proprietary databases. The aim was to define key variables influencing the market, such as demand drivers and supply constraints.

Historical data for the MEA Polyolefin market was compiled, focusing on market penetration and industry growth across key sectors like automotive, construction, and packaging. Market revenue was analyzed to ensure reliability in data points.

Key market hypotheses were formulated and validated through telephone interviews with industry experts, including executives from leading polyolefin manufacturers. These insights helped refine the market data and provided operational perspectives on industry dynamics.

The final phase involved interactions with key polyolefin manufacturers and suppliers to verify product performance and consumer trends. This bottom-up approach helped ensure comprehensive and accurate analysis of the MEA Polyolefin market, validated by direct market participants.

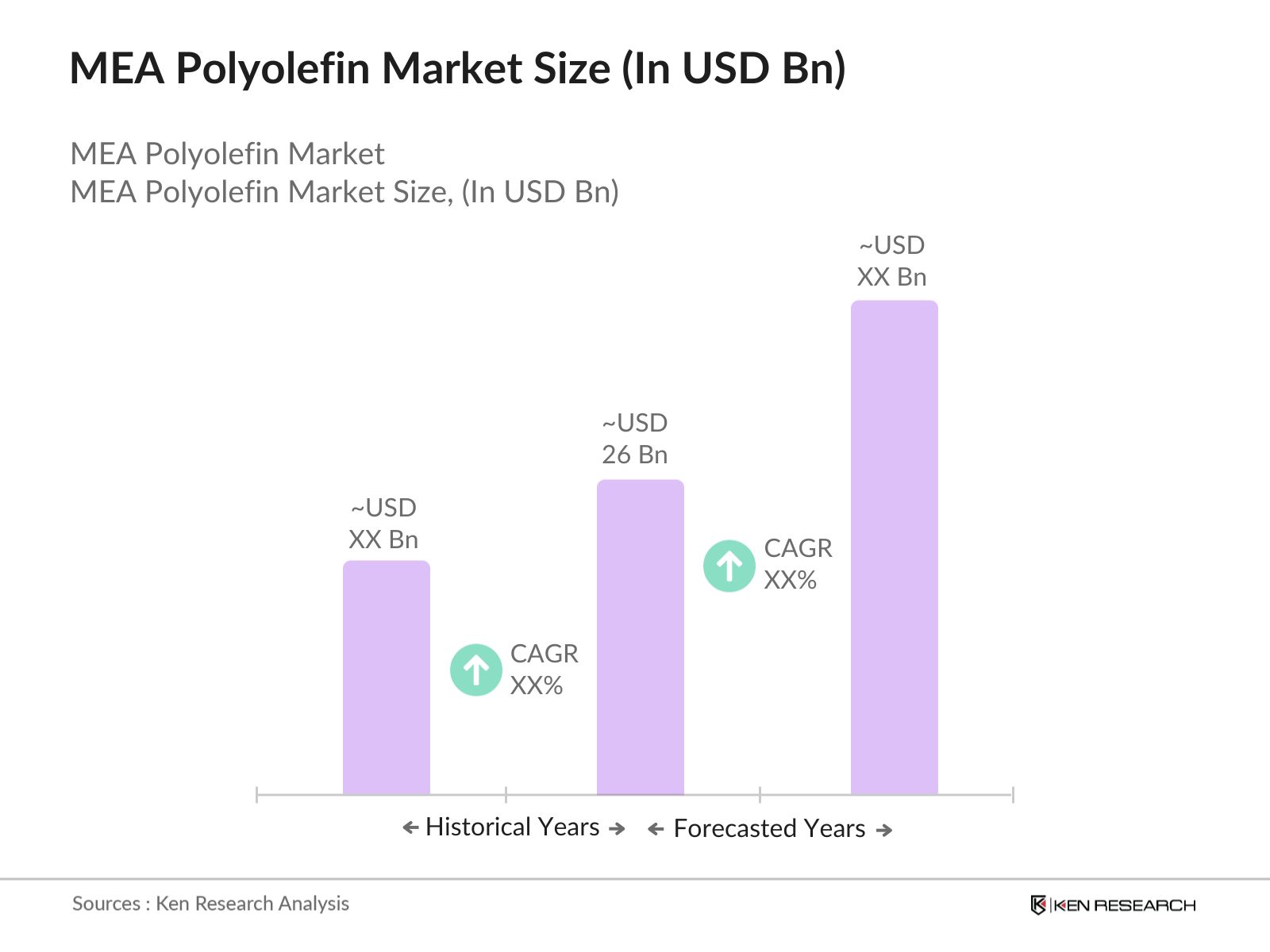

The MEA Polyolefin market is valued at USD 26 billion, driven by demand in packaging, automotive, and construction sectors.

Key challenges in the MEA Polyolefin market include fluctuating raw material prices, environmental regulations concerning plastic waste, and limited recycling infrastructure.

Major players in the MEA Polyolefin market include Saudi Basic Industries Corporation (SABIC), Borouge, LyondellBasell, Dow Inc., and ExxonMobil, dominating through extensive production capabilities and strategic investments.

The MEA Polyolefin market is driven by increased demand for lightweight materials in automotive production, growth in packaging for consumer goods, and government investment in infrastructure.

Key trends in the MEA Polyolefin market include the rising use of recycled polyolefins, advancements in digital production technologies, and innovations in high-performance polyolefin grades for various industrial applications.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.