MEA Sea Salt Market Outlook to 2030

Region:Global

Author(s):Meenakshi Bisht

Product Code:KROD5426

Region:Global

Author(s):Meenakshi Bisht

Product Code:KROD5426

December 2024

91

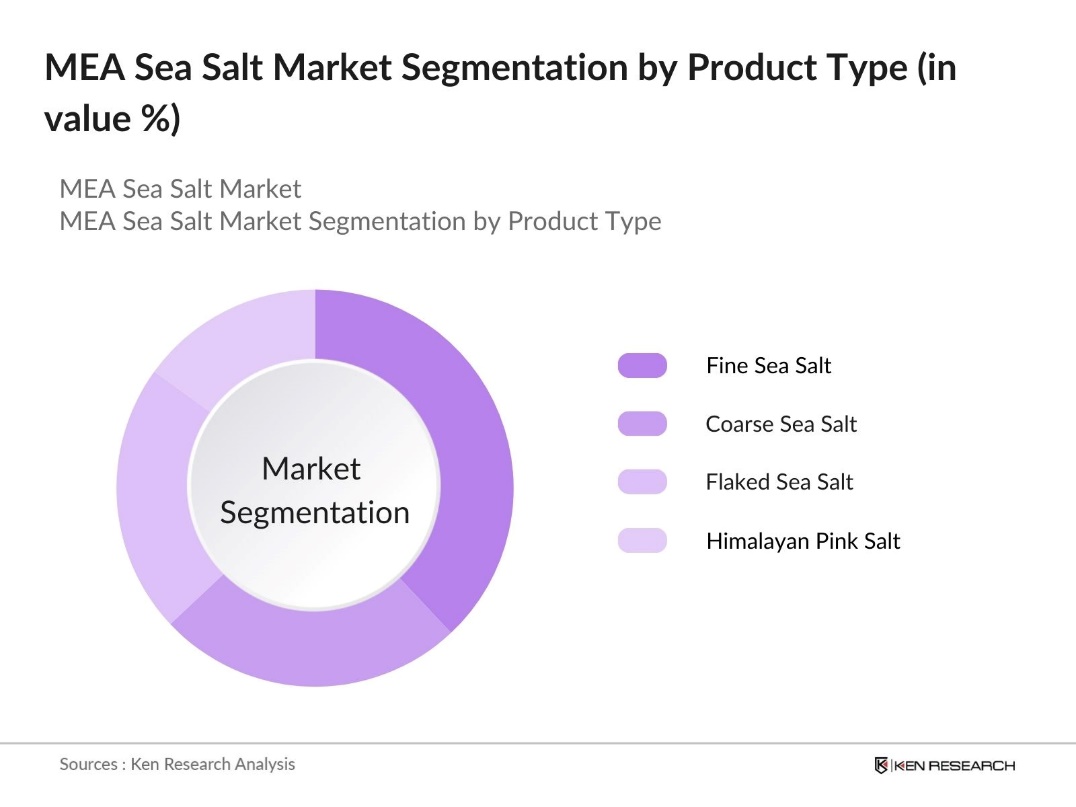

By Product Type: The MEA Sea Salt Market is segmented by product type into fine sea salt, coarse sea salt, flaked sea salt, and Himalayan pink salt. Fine sea salt currently holds the dominant share in this segmentation due to its wide application in food processing industries, especially in baked goods and snacks. Its smooth texture allows it to dissolve quickly, which is a critical requirement in industrial food preparation. Moreover, fine sea salt is preferred by consumers for daily use, further driving its dominance in the market. This segments growth is also supported by the increasing demand for sea salt-based seasoning blends and health-oriented products.

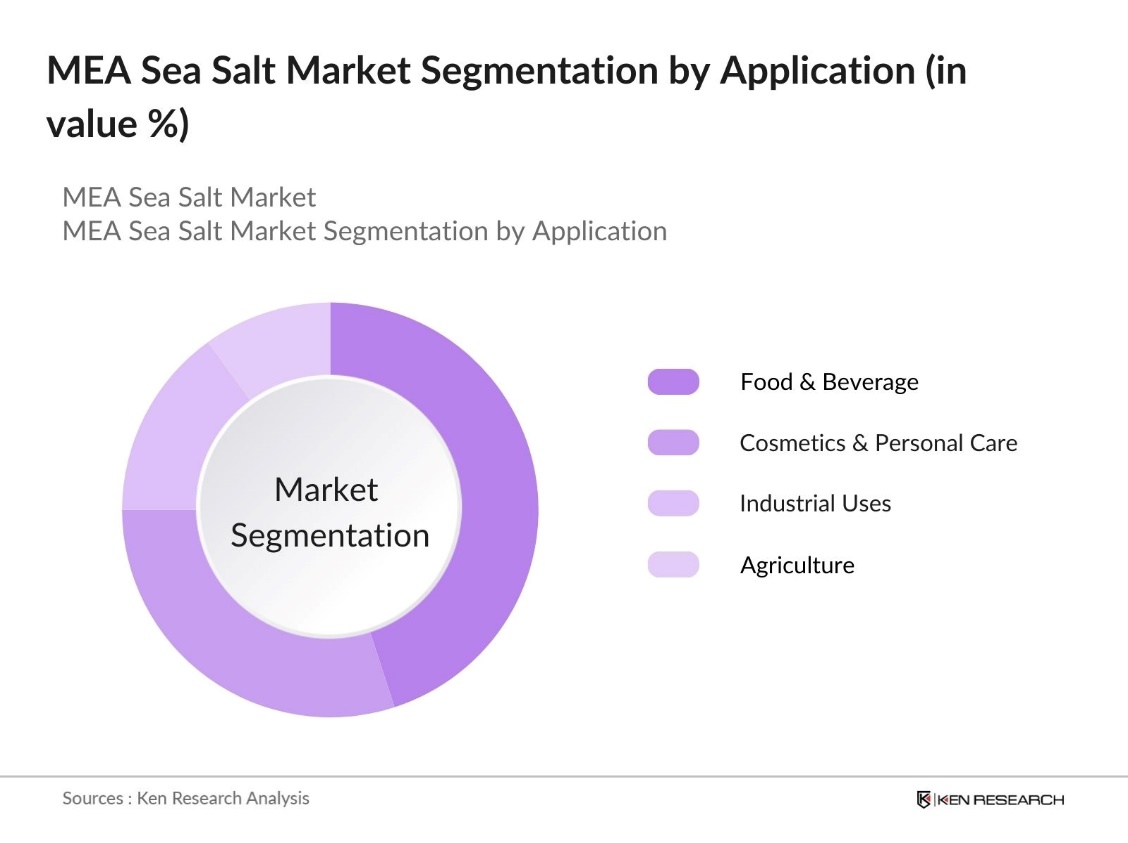

By Application: The MEA Sea Salt Market is segmented by application into food & beverage, cosmetics & personal care, industrial uses, and agriculture. The food & beverage sector leads this segment due to the rising popularity of sea salt in gourmet food products and natural food trends. Restaurants and food manufacturers are increasingly opting for sea salt as a healthier alternative to regular salt, and this shift is evident in product labels and menu items. Additionally, the demand for sea salt-based seasoning in snacks and ready-to-eat meals has contributed to the substantial market share in the food industry. As consumer preferences lean towards natural and unprocessed food ingredients, this segment continues to expand.

The market is led by global players like Cargill and Morton Salt, alongside local and artisanal brands such as Selina Naturally and Maldon Salt Company. These companies dominate the market due to their expansive distribution networks, sustainable harvesting techniques, and strong brand loyalty. The emphasis on eco-friendly and artisanal production methods has given some smaller players a competitive edge in niche markets, particularly in the gourmet and organic food sectors.

|

Company |

Establishment Year |

Headquarters |

Production Capacity |

Product Range |

Harvesting Techniques |

Distribution Channels |

Sustainability Initiatives |

Geographical Reach |

|

Cargill, Inc. |

1865 |

Minneapolis, USA |

||||||

|

Morton Salt |

1848 |

Chicago, USA |

||||||

|

Selina Naturally |

1984 |

USA |

||||||

|

Maldon Salt Company |

1882 |

UK |

||||||

|

SaltWorks, Inc. |

2001 |

USA |

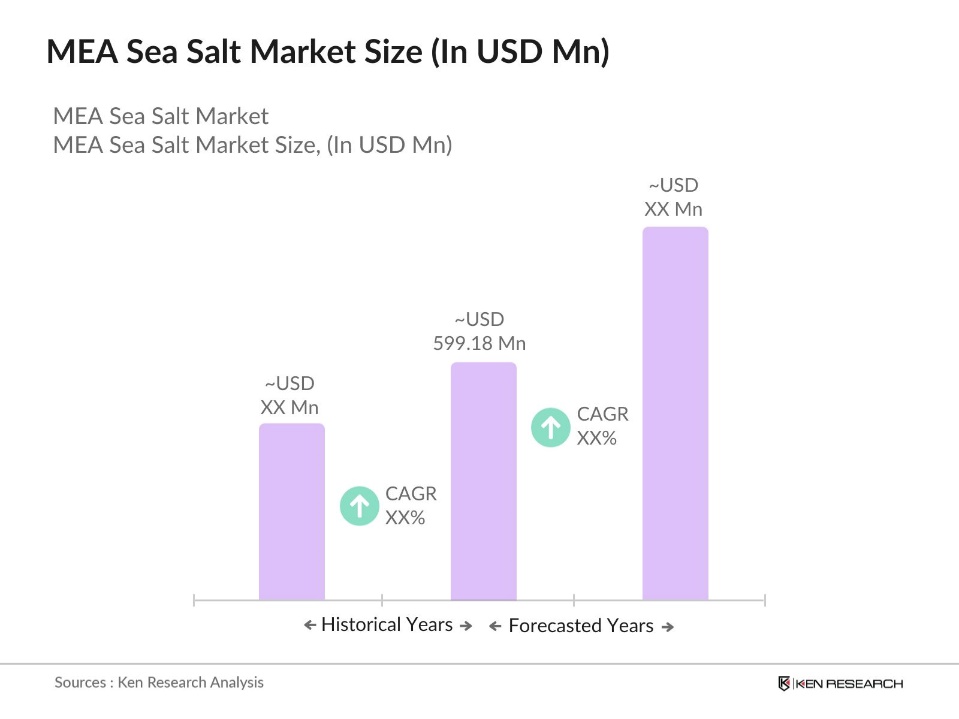

Over the next five years, the MEA Sea Salt Market is expected to witness substantial growth driven by expanding applications in the food and beverage industry and increasing consumer preference for organic and natural ingredients. With the region's significant export capabilities, particularly from countries like Saudi Arabia and Egypt, the market is poised to cater to growing demand in Europe and Asia.

|

By Product Type |

Fine Sea Salt Coarse Sea Salt Flaked Sea Salt Himalayan Pink Salt |

|

By Application |

Food & Beverage Cosmetics & Personal Care Industrial Agriculture |

|

By Distribution Channel |

Direct Sales (B2B) Supermarkets & Hypermarkets Specialty Stores Online Retail |

|

By End-User Industry |

Food Industry Pharmaceutical Industry Cosmetics Industry Industrial Uses |

|

By Region |

Middle East Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Demand for Natural Ingredients (Regional Consumer Preferences)

3.1.2. Rising Health Awareness (Demand for Organic Sea Salt)

3.1.3. Expansion of Processed Food Industry (Use of Sea Salt in Packaged Foods)

3.1.4. Growth in Cosmetic Applications (Sea Salt in Skincare)

3.2. Market Challenges

3.2.1. High Costs of Extraction (Labor and Equipment)

3.2.2. Environmental Regulations (Impact of Salt Production on Coastal Ecosystems)

3.2.3. Competition from Synthetic Alternatives (Table Salt vs. Sea Salt)

3.2.4. Seasonality of Production (Impact of Climate on Harvesting)

3.3. Opportunities

3.3.1. Increasing Demand for Gourmet Food Products (Artisanal Salt Brands)

3.3.2. Technological Innovations in Salt Harvesting

3.3.3. Expansion of International Export Markets (Middle Eastern Export Channels)

3.3.4. Growing Interest in Eco-Friendly Packaging

3.4. Trends

3.4.1. Organic and Clean Labeling in Food Products

3.4.2. Rising Popularity of Bath Salts and Spa Products (Wellness Industry)

3.4.3. Demand for Premium-Grade Sea Salt (Foodservice and Retail)

3.4.4. Salt Flakes vs. Fine Sea Salt (Regional Preferences)

3.5. Government Regulation

3.5.1. Environmental Protection Regulations

3.5.2. Import and Export Guidelines for Sea Salt

3.5.3. Quality Certifications (Organic, Eco-Friendly Production Standards)

3.5.4. Food Safety Regulations (Edible Sea Salt Certification)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Fine Sea Salt

4.1.2. Coarse Sea Salt

4.1.3. Flaked Sea Salt

4.1.4. Himalayan Pink Salt

4.2. By Application (In Value %)

4.2.1. Food & Beverage (Culinary Use, Food Processing)

4.2.2. Cosmetics & Personal Care (Skincare, Bath Products)

4.2.3. Industrial (Water Treatment, Chemical Manufacturing)

4.2.4. Agriculture (Animal Feed, Soil Conditioning)

4.3. By Distribution Channel (In Value %)

4.3.1. Direct Sales (B2B)

4.3.2. Supermarkets & Hypermarkets

4.3.3. Specialty Stores (Gourmet Stores)

4.3.4. Online Retail (E-commerce)

4.4. By End-User Industry (In Value %)

4.4.1. Food Industry

4.4.2. Pharmaceutical Industry

4.4.3. Cosmetics Industry

4.4.4. Industrial Uses

4.5. By Region (In Value %)

4.5.1. Middle East (GCC, North Africa, Egypt)

4.5.2. Africa (South Africa, East Africa, Nigeria)

5.1. Detailed Profiles of Major Companies

5.1.1. Cargill, Inc.

5.1.2. Morton Salt

5.1.3. Selina Naturally

5.1.4. Maldon Salt Company

5.1.5. Pacific Salt Pty Ltd.

5.1.6. SAN FRANCISCO SALT COMPANY

5.1.7. SaltWorks, Inc.

5.1.8. Celtic Sea Salt

5.1.9. Pyramid Salt Pty Ltd.

5.1.10. The Cornish Sea Salt Company

5.1.11. K+S AG

5.1.12. Salt of the Earth Ltd.

5.1.13. Hubei Salt Group

5.1.14. Iran Salt Co.

5.1.15. Salins Group

5.2. Cross Comparison Parameters (Production Capacity, Harvesting Techniques, Pricing, Sustainability Initiatives, Product Range, Regional Dominance, Export Market Share, Brand Reputation)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

6.4. Food Safety Regulations (Edible Sea Salt)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe first step involved constructing an ecosystem map, identifying all significant stakeholders in the MEA Sea Salt Market. Through extensive desk research using industry reports and government databases, we defined the critical variables influencing the market, including production processes, demand trends, and regulatory frameworks.

In this phase, we analyzed historical data, focusing on market penetration, supply chains, and revenue generation for the market. Additionally, we assessed product distribution across various application sectors, particularly food & beverage, to gauge overall market health and growth.

We engaged industry experts through structured interviews and surveys to validate the initial findings. Insights from salt producers, traders, and government agencies helped in refining the data and forecasting market trends based on actual production and trade data.

Finally, we synthesized all gathered information, ensuring that it aligns with market realities and industry expectations. This step involved cross-referencing all data with trade reports and government publications, ensuring accuracy and reliability.

The MEA Sea Salt Market is valued at USD 599.18 million, driven by the increasing demand for natural food products and expanding applications in the food and cosmetics industries.

Key challenges in MEA Sea Salt Market include the high costs of extraction, environmental regulations surrounding coastal salt production, and competition from lower-cost alternatives like table salt.

The MEA Sea Salt Market is dominated by companies such as Cargill, Morton Salt, Selina Naturally, and SaltWorks, Inc., which have established strong distribution networks and focus on sustainable production methods.

The MEA Sea Salt Market growth is driven by the rising consumer preference for natural and organic products, increasing demand from the food and beverage sector, and the growing popularity of sea salt in cosmetic applications.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.