MEA Self Tanning Products Market Outlook to 2030

Region:Global

Author(s):Shambhavi

Product Code:KROD4549

December 2024

81

About the Report

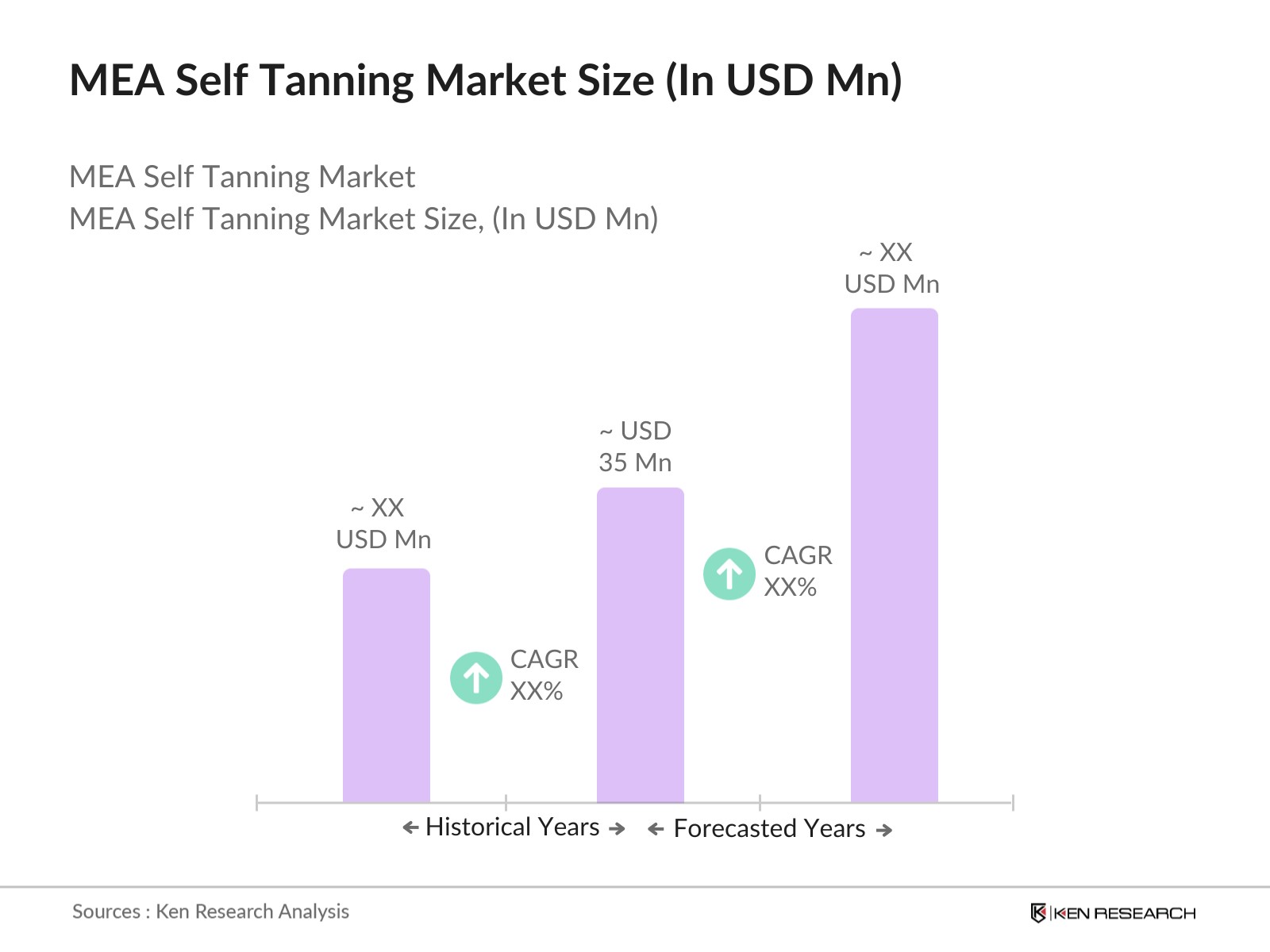

MEA Self Tanning Products Market Overview

- The MEA Self Tanning Products market is valued at USD 35 million, based on a comprehensive five-year historical analysis. This market size is driven by the increasing awareness of skin safety, particularly the adverse effects of UV rays on skin health. Consumers are shifting towards non-UV tanning alternatives, such as self-tanning lotions and sprays, due to growing beauty standards and health-conscious decisions. Additionally, the rising preference for organic and natural ingredients is fueling demand across the Middle East and Africa.

- Countries like the UAE, Saudi Arabia, and South Africa dominate the market due to high consumer spending on beauty and personal care products. The UAE and Saudi Arabia are characterized by high disposable incomes, significant urban populations, and a strong beauty-conscious culture. South Africa leads in product penetration, particularly in urban areas where consumer awareness and accessibility to international brands are higher. These factors create a strong demand for self-tanning products in these regions.

- Governments in the MEA region have introduced stricter cosmetic product safety standards to ensure consumer protection. In 2024, the Saudi Food and Drug Authority (SFDA) reviewed over 500 cosmetic products, including self-tanning products, to enforce safety standards that limit harmful chemicals like parabens. Approximately 30% of self-tanning products failed to meet these criteria, leading to regulatory actions and product recalls across the region. These standards have increased consumer confidence and are driving the demand for safer, regulated products.

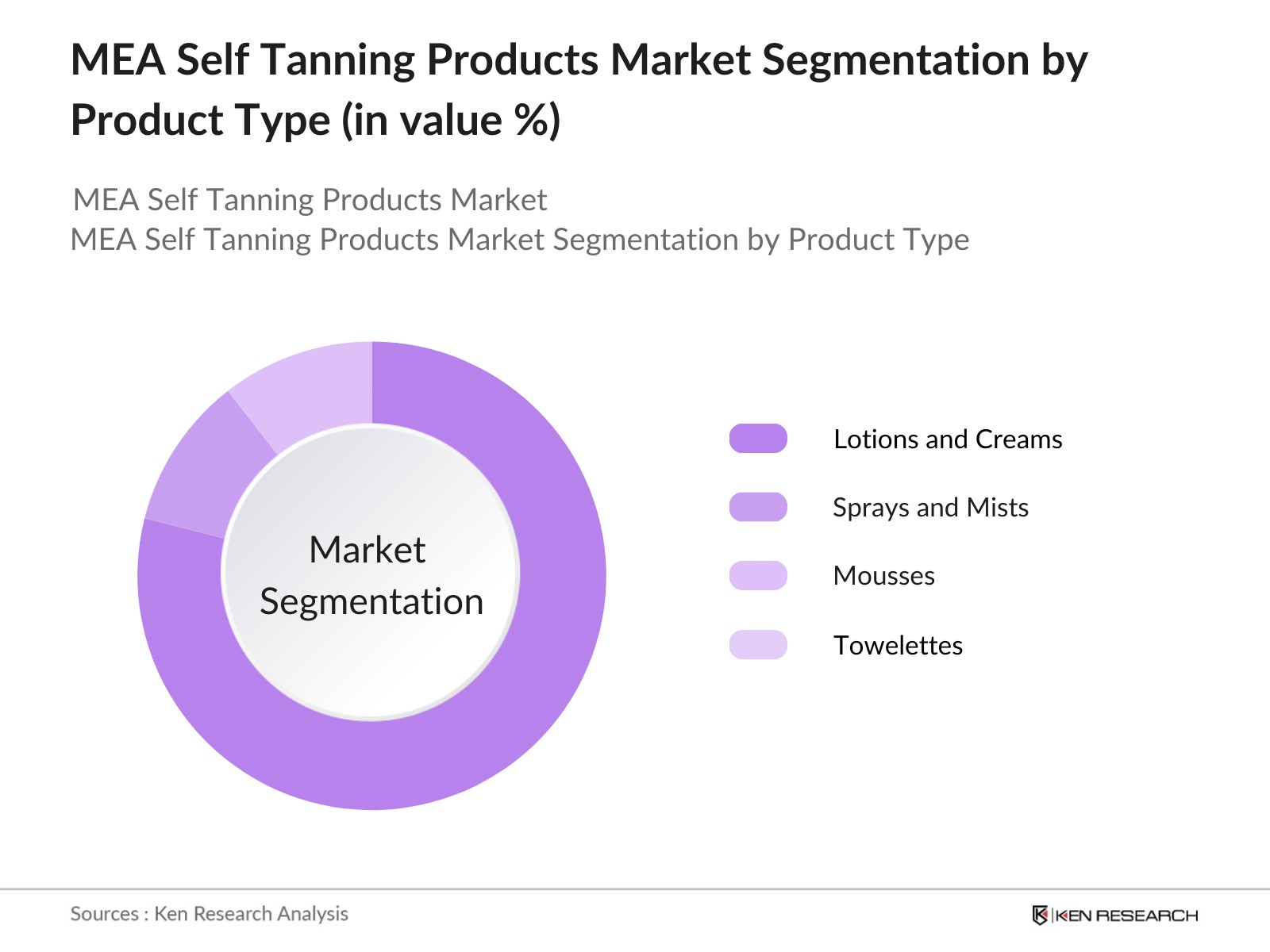

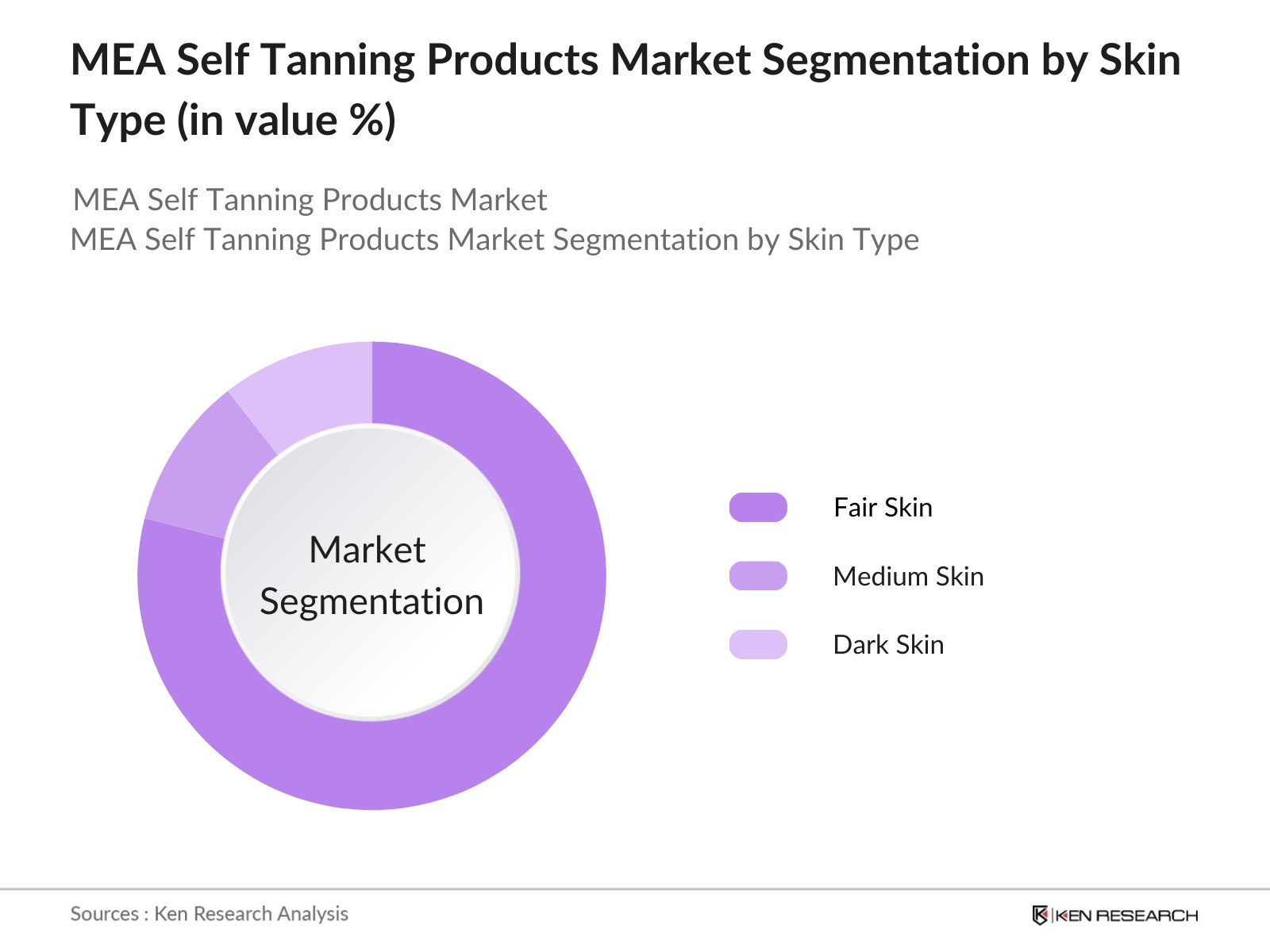

MEA Self Tanning Products Market Segmentation

By Product Type: The MEA Self Tanning Products market is segmented by product type into lotions and creams, sprays and mists, mousses, towelettes, and gels. Lotions and creams currently dominate the market, driven by their ease of application and longstanding consumer trust. Lotions provide a more even application and are less likely to cause streaking compared to other forms like sprays or mousses. Moreover, the inclusion of additional skincare benefits, such as moisturizing ingredients in lotions, makes them highly appealing to consumers.

By Skin Type: This market is further segmented by skin type into fair skin, medium skin, and dark skin. Products for medium skin types dominate the market as the MEA region has a majority of consumers with medium-toned skin, making self-tanning products for this skin tone highly sought after. Additionally, medium skin tones often require products that provide gradual tanning effects, making them ideal for consumers looking for a subtle yet noticeable change.

MEA Self Tanning Products Market Competitive Landscape

The MEA Self Tanning Products market is dominated by several key players who have established a strong foothold in the region. These companies leverage their extensive distribution networks, brand reputation, and innovation in product formulation to capture a significant market share. The market remains moderately fragmented with both global and regional players contributing to its competitive dynamics. The market is led by companies like L'Oral, Unilever, and Johnson & Johnson, who are known for their diverse product portfolios. These firms dominate through their robust marketing strategies, heavy investment in research and development (R&D), and focus on organic and sustainable product offerings.

|

Company |

Establishment Year |

Headquarters |

R&D Expenditure |

Product Portfolio |

Distribution Network |

Sustainability Initiatives |

Digital Marketing Strategies |

|

L'Oral S.A. |

1909 |

France |

- |

- |

- |

- |

- |

|

Unilever PLC |

1930 |

UK/Netherlands |

- |

- |

- |

- |

- |

|

Johnson & Johnson |

1886 |

USA |

- |

- |

- |

- |

- |

|

PZ Cussons Plc |

1879 |

UK |

- |

- |

- |

- |

- |

|

Beiersdorf AG |

1882 |

Germany |

- |

- |

- |

- |

- |

MEA Self Tanning Products Industry Analysis

Growth Drivers

- Rising Beauty Consciousness: In 2024, the beauty industry in the MEA region has seen increased interest from consumers, particularly in aesthetic appearances. The growing beauty consciousness, especially in urban centers such as Dubai, Riyadh, and Cairo, has led to a heightened demand for beauty products, including self-tanning solutions. With a population exceeding 450 million in MEA, approximately 60 million individuals in urban areas have shown increasing interest in enhancing their aesthetic appearance, pushing the demand for safe and effective non-UV tanning products. According to IMF's regional outlook, consumer spending on personal care in these regions reached USD 9.8 billion by 2024.

- Increasing Popularity of Non-UV Tanning Methods: In the Middle East, particularly in UAE and Saudi Arabia, where harsh sunlight often necessitates indoor living, non-UV tanning products have gained widespread popularity. The suns harmful UV rays have driven consumers toward safer alternatives. A report from WHO in 2024 highlighted that approximately 300,000 skin cancer cases in MEA were linked to overexposure to UV rays, encouraging a shift toward non-UV methods. This has bolstered the market for self-tanning products, with DHA-based formulations becoming a preferred choice for about 25 million users across the region.

- Availability of Easy-to-Use Self Tanning Products: Self-tanning products have gained traction due to their ease of use and convenience. Retailers and e-commerce platforms report increased penetration of these products in urban areas of countries like South Africa and Egypt. With 2024 seeing e-commerce sales in MEA rise to USD 50 billion, over 15% of that figure pertains to personal care and cosmetics products. The availability of easy-to-use self-tanning lotions and sprays has penetrated markets with over 30 million active consumers across key urban markets in the region.

Market Challenges

- High Competition from Traditional Sun-Tanning Products: Despite the growing trend of self-tanning products, traditional sun-tanning methods still hold significant market share in coastal countries like Morocco and Egypt, where tourism and beach lifestyles prevail. According to 2024 government tourism data, about 25 million tourists visit these regions annually, contributing to a sustained demand for sun-tanning products. These traditional products continue to pose competition to non-UV alternatives, making market penetration for self-tanning products slower in these areas.

- Presence of Harmful Chemicals in Self-Tanning Formulas: In 2024, regulatory agencies such as the Saudi Food and Drug Authority (SFDA) and the Egyptian Ministry of Health flagged concerns over certain self-tanning products containing harmful chemicals, such as parabens and phthalates. The SFDA inspected over 200 self-tanning products and found that 40% of them failed to meet safety standards due to the presence of toxic ingredients. This has created regulatory barriers for manufacturers to ensure compliance with stringent safety regulations, impacting the growth of the market.

MEA Self Planning Market Future Outlook

Over the next five years, the MEA Self Tanning Products market is expected to exhibit steady growth, driven by the increasing focus on skincare safety, rising disposable incomes, and growing consumer awareness of non-UV tanning alternatives. Continuous product innovation, especially in the organic and vegan-friendly product segment, will contribute to the market's positive trajectory. Moreover, the rise of e-commerce channels is likely to enhance product accessibility, fueling market expansion across both urban and rural regions in MEA.

Market Opportunities

- Demand for Organic and Natural Self Tanning Products: There is a growing consumer preference for organic and natural ingredients in personal care products across the MEA region, particularly in countries like the UAE and Israel, where consumers are increasingly health-conscious. In 2024, the World Health Organization reported that over 20 million consumers in MEA prefer organic skincare solutions. This trend presents an opportunity for self-tanning products that emphasize organic ingredients such as DHA derived from plant sources, positioning them as safer and more sustainable alternatives.

- Growing E-commerce and Online Sales Chain: In 2024, e-commerce in the MEA region experienced rapid growth, driven by a tech-savvy population. Digital sales penetration for personal care products grew by over 30% in countries like the UAE, where more than 70% of consumers purchase beauty products online. This trend has opened up significant market opportunities for self-tanning products through online channels, with approximately 12 million active users in MEA purchasing cosmetics through platforms like Amazon and Noon. The availability of global shipping options further supports the rapid expansion of these products across the region.

Scope of the Report

|

By Product Type |

Lotions and Creams Sprays and Mists Mousses Towelettes Gels |

|

By Skin Type |

Fair Skin Medium Skin Dark Skin |

|

By End-User |

Men Women |

|

By Distribution Channel |

Online Retail Specialty Stores Hypermarkets/Supermarkets Pharmacies |

|

By Region |

Gulf Cooperation Council (GCC) North Africa South Africa Levant Region |

Products

Key Target Audience

Beauty Product Manufacturers

Skincare Product Distributors

Online Retailers (e.g., Amazon, Noon)

Hypermarkets and Supermarkets

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (UAE Ministry of Health, South African Bureau of Standards)

Organic and Natural Product Brands

Retail Chains and Department Stores

Companies

Players Mentioned in the Report

L'Oral S.A.

Unilever PLC

Beiersdorf AG

Johnson & Johnson

PZ Cussons Plc

Kao Corporation

Clarins Group

St. Tropez (PZ Cussons)

Bondi Sands Pty Ltd.

Coty Inc.

The Este Lauder Companies Inc.

Tan-Luxe

Fake Bake

Vita Liberata

Isle of Paradise

Table of Contents

1. MEA Self Tanning Products Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Market Demand for Skin Care and Aesthetic Products)

1.4. Market Segmentation Overview

2. MEA Self Tanning Products Market Size (In USD Bn)

2.1. Historical Market Size (Skin Care Market Revenue)

2.2. Key Market Developments and Milestones (Product Launches and Innovations)

3. MEA Self Tanning Products Market Analysis

3.1. Growth Drivers

3.1.1. Rising Beauty Consciousness (Consumer Preferences for Aesthetic Appearance)

3.1.2. Increasing Popularity of Non-UV Tanning Methods

3.1.3. Availability of Easy-to-Use Self Tanning Products (Product Penetration)

3.2. Market Challenges

3.2.1. High Competition from Traditional Sun-Tanning Products

3.2.2. Presence of Harmful Chemicals in Self-Tanning Formulas (Regulatory Compliance)

3.2.3. Limited Consumer Awareness in Rural Areas

3.3. Opportunities

3.3.1. Demand for Organic and Natural Self Tanning Products

3.3.2. Growing E-commerce and Online Sales Channels (Digital Sales Penetration)

3.3.3. Market Expansion into Emerging MEA Economies

3.4. Trends

3.4.1. Increasing Use of DHA (Dihydroxyacetone) in Formulations

3.4.2. Vegan and Cruelty-Free Product Innovations (Sustainability)

3.4.3. Customizable Tanning Solutions for Different Skin Types

3.5. Government Regulation

3.5.1. MEA Cosmetic Product Safety Standards (Health and Safety Regulations)

3.5.2. Import Regulations for Self Tanning Products (Trade Barriers)

3.5.3. Labeling and Packaging Requirements (Consumer Information Regulations)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. MEA Self Tanning Products Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Lotions and Creams

4.1.2. Sprays and Mists

4.1.3. Mousses

4.1.4. Towelettes

4.1.5. Gels

4.2. By Skin Type (In Value %)

4.2.1. Fair Skin

4.2.2. Medium Skin

4.2.3. Dark Skin

4.3. By End-User (In Value %)

4.3.1. Men

4.3.2. Women

4.4. By Distribution Channel (In Value %)

4.4.1. Online Retail

4.4.2. Specialty Stores

4.4.3. Hypermarkets/Supermarkets

4.4.4. Pharmacies

4.5. By Region (In Value %)

4.5.1. Gulf Cooperation Council (GCC)

4.5.2. North Africa

4.5.3. South Africa

4.5.4. Levant Region

5. MEA Self Tanning Products Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. L'Oral S.A.

5.1.2. Unilever PLC

5.1.3. Beiersdorf AG

5.1.4. Johnson & Johnson

5.1.5. PZ Cussons Plc

5.1.6. Kao Corporation

5.1.7. Clarins Group

5.1.8. St. Tropez (PZ Cussons)

5.1.9. Bondi Sands Pty Ltd.

5.1.10. Coty Inc.

5.1.11. The Este Lauder Companies Inc.

5.1.12. Tan-Luxe

5.1.13. Fake Bake

5.1.14. Vita Liberata

5.1.15. Isle of Paradise

5.2. Cross Comparison Parameters (R&D Expenditure, Sustainability Initiatives, Product Portfolio, Distribution Network, Customer Base, Market Presence, Digital Marketing Strategies, Innovation Capabilities)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Collaborations)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Private Equity Investments

6. MEA Self Tanning Products Market Regulatory Framework

6.1. MEA Cosmetic Product Standards

6.2. Safety and Compliance Regulations

6.3. Certification Processes for Self Tanning Products

7. MEA Self Tanning Products Future Market Size (In USD Billion)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. MEA Self Tanning Products Future Market Segmentation

8.1 By Product Type

8.2 By Skin

8.3 By End-User

8.4 By Distribution Channel

8.5 By Region

9. MEA Self Tanning Products Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first phase involves mapping the stakeholder ecosystem within the MEA Self Tanning Products Market. Extensive desk research was conducted using proprietary databases and secondary research sources to gather critical information. The goal of this step is to identify the core variables affecting market growth and demand.

Step 2: Market Analysis and Construction

Historical data for the self-tanning products market was compiled and analyzed, with attention given to market penetration by product type and consumer demographics. Additional analysis of sales figures and revenue generation was undertaken to ensure accurate data representation.

Step 3: Hypothesis Validation and Expert Consultation

This stage involved validating initial hypotheses through interviews with key industry experts, including manufacturers and retailers. These consultations helped refine the market data, providing insights into sales trends and operational dynamics that influence market behavior.

Step 4: Research Synthesis and Final Output

In the final stage, engagement with multiple manufacturers helped refine product segment insights. This ensured comprehensive and accurate analysis, verified through a bottom-up approach to market data, ensuring the final output is a complete representation of the MEA Self Tanning Products Market.

Frequently Asked Questions

01. How big is the MEA Self Tanning Products Market?

The MEA Self Tanning Products market is valued at USD 35 miliion, driven by consumer preferences for safe, non-UV tanning alternatives and increasing demand for organic skincare solutions.

02. What are the key challenges in the MEA Self Tanning Products Market?

Challenges include competition from traditional sun-tanning products, regulatory compliance issues regarding product safety, and limited consumer awareness in rural areas.

03. Who are the major players in the MEA Self Tanning Products Market?

Key players include L'Oral S.A., Unilever PLC, Johnson & Johnson, PZ Cussons Plc, and Beiersdorf AG, dominating the market with diverse product portfolios and strong distribution networks.

04. What are the growth drivers of the MEA Self Tanning Products Market?

Growth is propelled by increasing awareness of skin damage caused by UV exposure, rising demand for organic and vegan-friendly tanning products, and expanding e-commerce sales channels.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.