MEA Telecom Market Outlook to 2030

Region:Middle East

Author(s):Shubham Kashyap

Product Code:KROD9460

December 2024

87

About the Report

MEA Telecom Market Overview

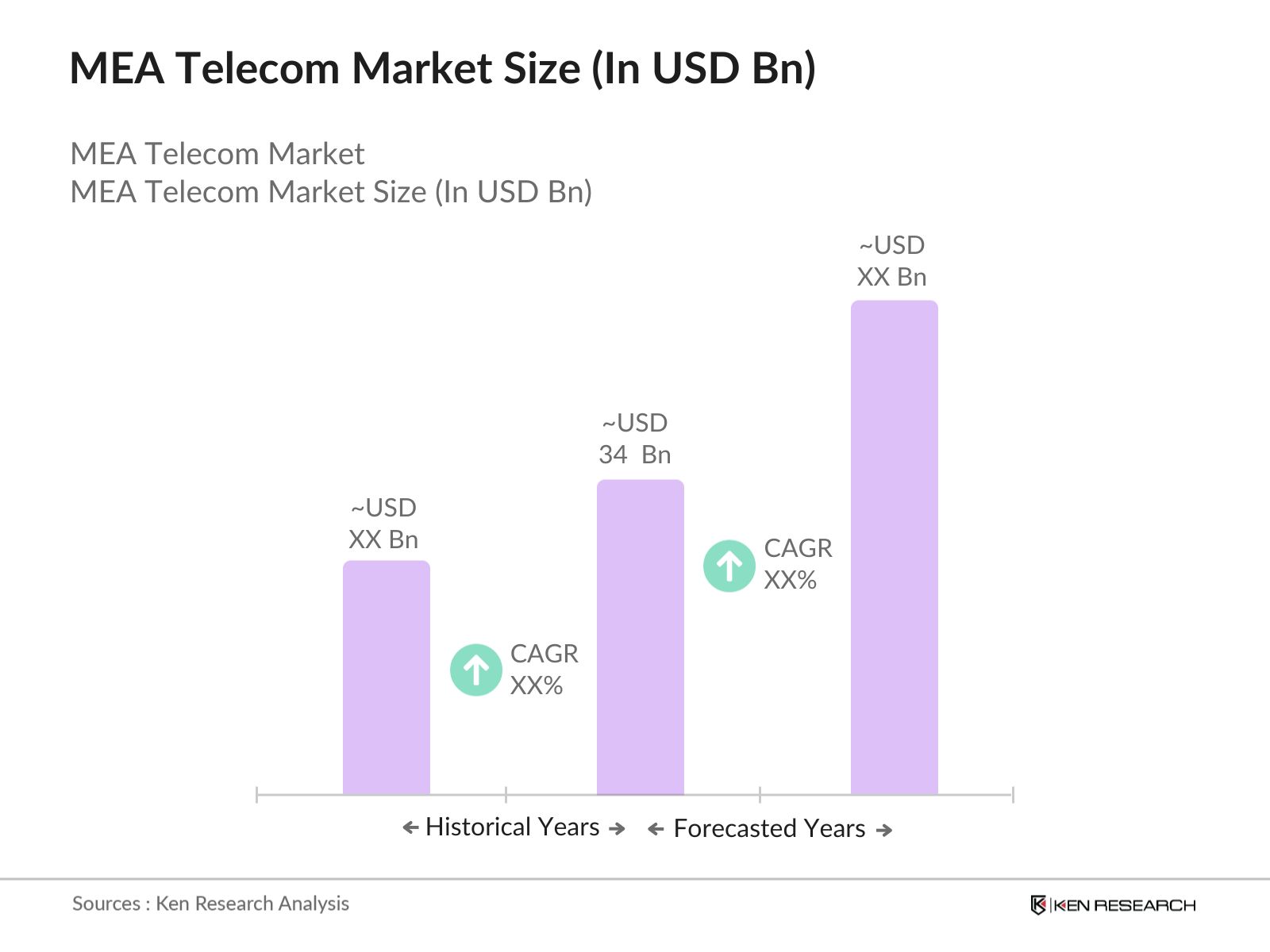

- The MEA Telecom market is valued at USD 34 billion, driven primarily by the increasing demand for connectivity, expansion of mobile networks, and adoption of digital transformation initiatives. Key factors include the widespread adoption of smartphones, the surge in broadband connections, and advancements in telecom infrastructure. Moreover, the proliferation of 4G and 5G services is enhancing the demand for faster and more reliable connectivity, establishing MEA as a robust market for telecom solutions on a global scale.

- The major demand centers for telecom services in the MEA region include Saudi Arabia, the United Arab Emirates (UAE), and South Africa. These countries dominate due to high mobile penetration rates, substantial government investment in telecom infrastructure, and strategic policies to promote digitalization. For instance, Saudi Arabia's Vision 2030 and UAE's Smart Dubai initiatives are accelerating the digital economy by prioritizing telecom advancements, strengthening these nations' positions in the regional market.

- Government policies on spectrum allocation play a crucial role in shaping the telecom landscape in MEA. Countries like Egypt and Kenya have recently reallocated spectrums to enhance 4G and 5G coverage. These allocations are critical for telecom operators to meet growing data demands, especially in urban areas. Inconsistencies in spectrum allocation, however, can slow down telecom expansions and affect service quality.

MEA Telecom Market Segmentation

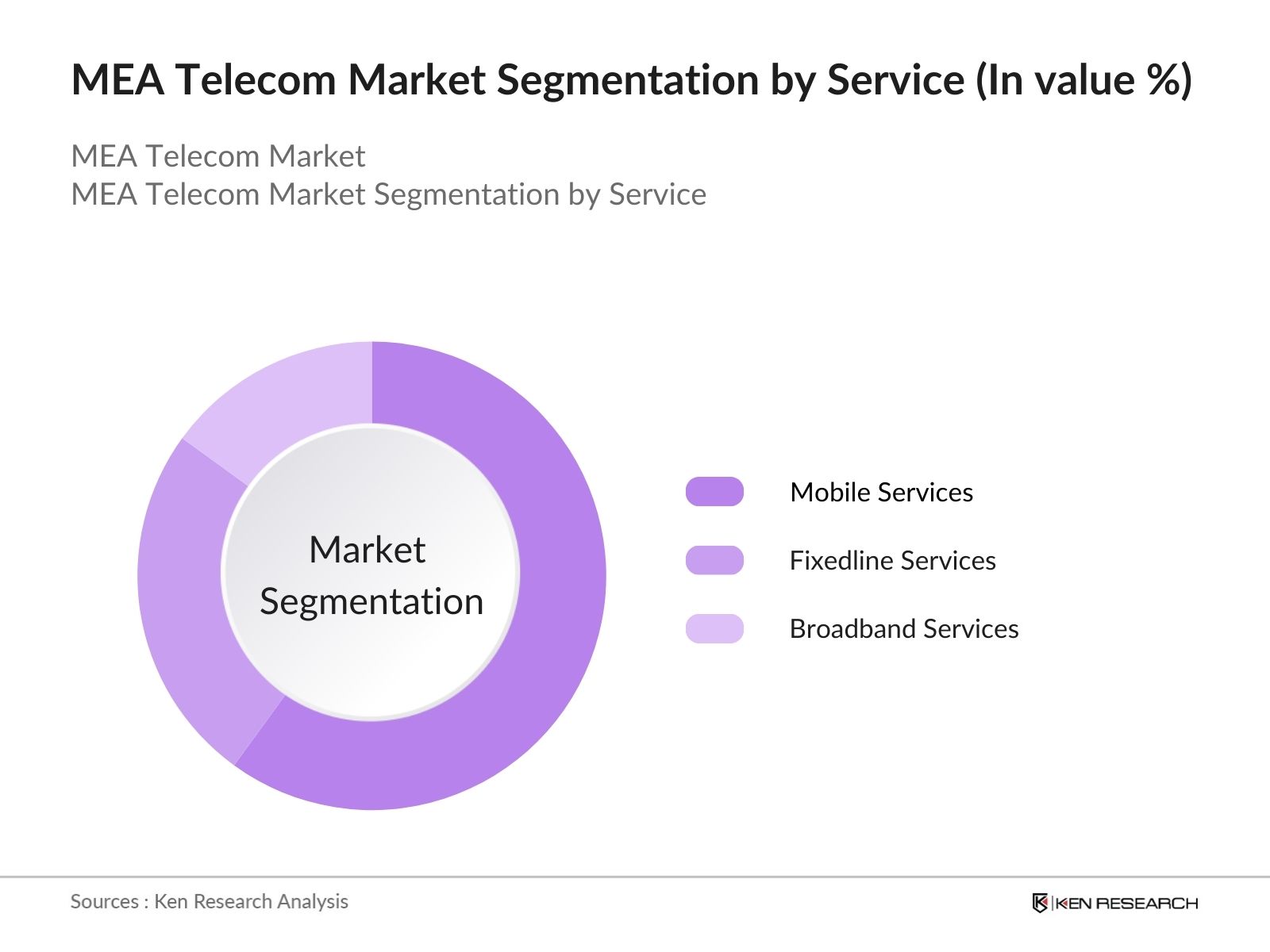

- By Service Type: The MEA telecom market is segmented by service type into mobile services, fixedline services, and broadband services. Mobile Services dominate this segment within the MEA telecom market. This is due to the accessibility and affordability of mobile devices, extensive mobile network coverage, and growing consumer preference for mobile connectivity. The mobile services sector also benefits from the high demand for data services, especially with the increasing use of smartphones for social media, streaming, and digital payments. With telecom operators expanding their offerings and improving network quality, mobile services continue to lead in market share.

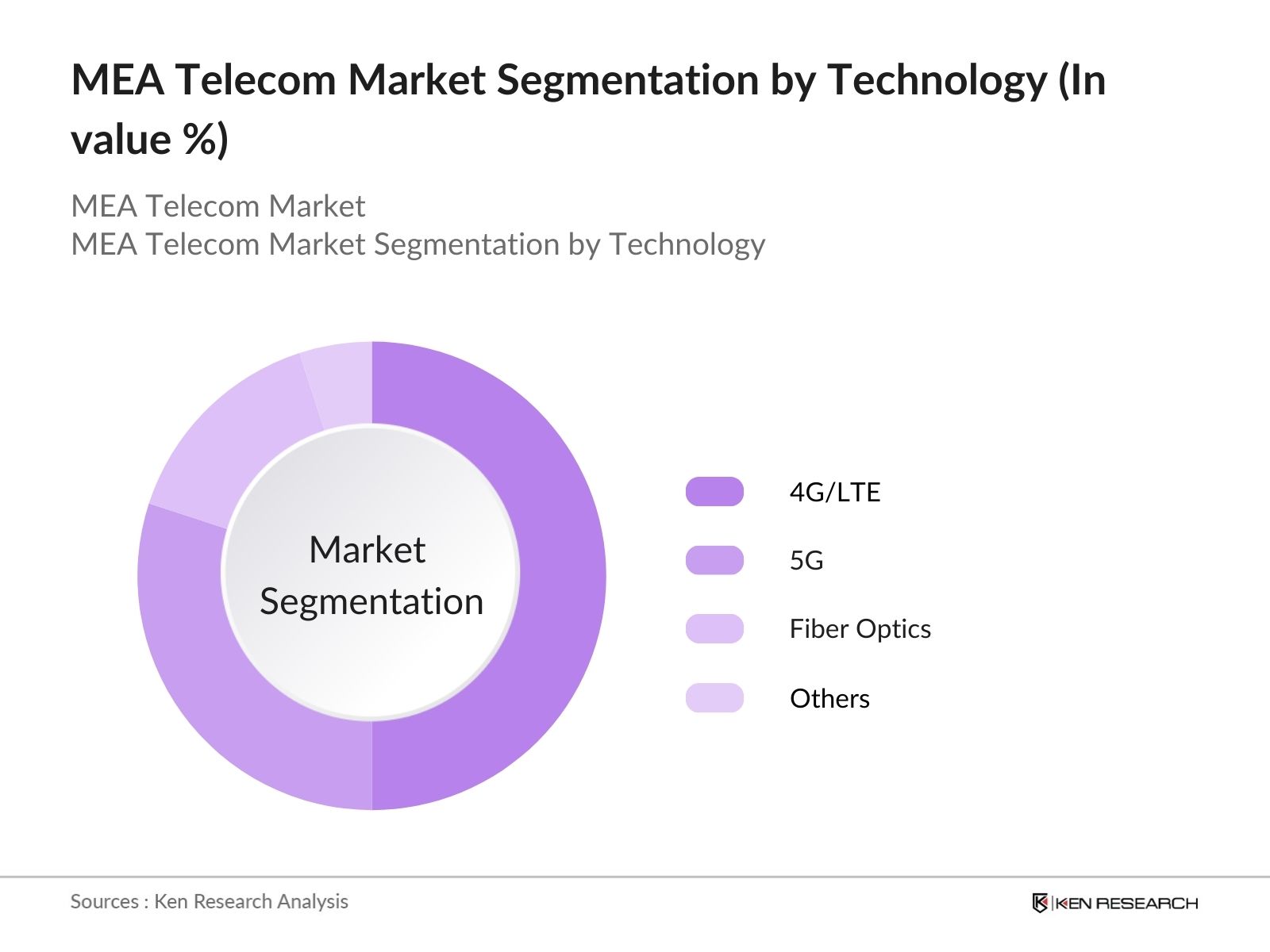

- By Technology: The MEA telecom market is also segmented by technology into 4G/LTE, 5G, fiber optics, and others. 4G/LTE Technology holds the largest market share within the technology segmentation. Its dominance is attributed to the widespread availability of 4G infrastructure across the region, providing reliable highspeed internet for mobile users. Additionally, the affordability of 4Genabled devices and the high demand for digital services have solidified 4G/LTEs leading position. Although 5G technology is gaining traction, 4G remains the preferred choice due to its accessibility and coverage.

MEA Telecom Market Competitive Landscape

The MEA telecom market is characterized by the presence of several key players who leverage their infrastructure investments, innovative service portfolios, and strategic partnerships to establish and maintain a strong market position.

The MEA telecom market is dominated by a few major players, including Saudi Telecom Company (STC), Etisalat Group, MTN Group, Vodafone Egypt, and Ooredoo Group. This consolidation highlights the significant influence of these key companies in shaping the region's telecommunications landscape.

MEA Telecom Market Analysis

Growth Drivers

- Increasing Mobile Penetration: The MEA region has experienced a substantial increase in mobile penetration, with over 1.2 billion mobile subscriptions recorded in 2023, according to the International Telecommunication Union (ITU). This growth reflects a sharp increase in smartphone ownership, particularly in populous nations like Nigeria and Egypt, where 75% and 65% of the population, respectively, now have access to mobile devices. With rapid population growth across MEA projected to exceed 1.5 billion by 2025, demand for mobile connectivity is set to increase further, fostering growth within the telecom sector.

- Expansion of Broadband Services: MEA's broadband subscriptions have expanded by 22 million from 2022 to 2024, with a significant rise in fiber optic installations across urban and rural areas. Nations like the United Arab Emirates (UAE) and Saudi Arabia have achieved broadband connectivity rates above 95%, supported by governmental initiatives and subsidies aimed at expanding digital accessibility. This broadband infrastructure growth has positively influenced e-commerce, online education, and telemedicine in these regions, thereby enhancing the telecom markets growth potential.

- Government Initiatives for Digital Transformation: Governments in the MEA region are prioritizing digital transformation to diversify their economies. Initiatives like Saudi Vision 2030 and Smart Dubai focus on enhancing connectivity, infrastructure, and digital services. Such programs stimulate investments in telecom infrastructure, driving the adoption of advanced technologies like 5G and fiber optics. These transformations are projected to support substantial gains in telecom infrastructure and services, increasing market demand across multiple industries reliant on digital solutions.

Challenges

- Regulatory and Compliance Issues: The MEA telecom market faces challenges related to regulatory compliance. Regulations around spectrum allocation, data privacy, and security create barriers for telecom operators. Compliance costs can be high, and the varied regulatory environments across countries add complexity to operations. These regulatory differences often delay service rollouts and increase the administrative burden for telecom companies.

- Infrastructure Limitations in Rural Areas: While urban areas in MEA enjoy high connectivity, rural and remote areas face infrastructure gaps. Limited infrastructure in these regions hampers service expansion and creates a digital divide, challenging telecom operators to develop costeffective solutions for connectivity in these areas. This disparity in connectivity hinders equal access to digital services, impacting economic growth in rural regions.

MEA Telecom Market Future Outlook

The MEA telecom market is projected to experience robust growth, driven by expanding digital economies, 5G adoption, and increased investment in telecom infrastructure. Innovations in network technology, a surge in IoT applications, and governmentled digitalization initiatives will create new opportunities. Additionally, the focus on expanding rural connectivity will be instrumental in enhancing the markets reach across the region.

Future Market Opportunities

- Expansion of 5G Services: The ongoing rollout of 5G networks is set to transform the telecom landscape in the MEA region, creating new demand for services that rely on ultrafast, low-latency connectivity. 5G technology supports applications requiring high-speed, real-time data transfer, making it ideal for sectors such as manufacturing, healthcare, and retail. For instance, 5G enables advanced manufacturing automation, real-time patient monitoring in healthcare, and immersive experiences in retail through augmented reality.

- Growth in Fiber Optics Deployment: The deployment of fiber optic technology is opening significant opportunities within the MEA telecom market. With a growing demand for high-speed broadband connectivity, fiber optics offer a solution for delivering consistent and reliable internet access to both residential and commercial users. Fiber optic networks, known for their capacity to transmit data over long distances with minimal signal loss, are becoming crucial in meeting the needs of industries reliant on large data transfers, such as financial services, media, and cloud computing.

Scope of the Report

|

By Service Type |

Mobile Services |

|

By Technology |

4G/LTE |

|

By Application |

Residential |

|

By EndUser |

Individuals |

|

By Region |

Saudi Arabia |

Products

Key Target Audience

Telecom Operators

Network Equipment Manufacturers

Government and Regulatory Bodies (e.g., Communications and Information Technology Commission)

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Internet Service Providers (ISPs)

Mobile Virtual Network Operators (MVNOs)

Technology Solution Providers

Companies

Players Mentioned in the Report

Saudi Telecom Company (STC)

Etisalat Group

MTN Group

Vodafone Egypt

Ooredoo Group

Zain Group

Orange Egypt

Telecom Egypt

Maroc Telecom

Safaricom

Telkom Kenya

Airtel Africa

Vodacom Group

Omantel

Batelco

Table of Contents

1. MEA Telecom Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. MEA Telecom Market Size (In USD Million)

2.1 Historical Market Size

2.2 Year On Year Growth Analysis

2.3 Key Market Developments and Milestones

3. MEA Telecom Market Analysis

3.1 Growth Drivers

3.2 Increasing Mobile Penetration

3.3 Expansion of Broadband Services

3.4 Government Initiatives for Digital Transformation

3.5 Adoption of Advanced Technologies (e.g., 5G, Fiber Optics)

3.6 Market Challenges

3.7 Regulatory and Compliance Issues

3.8 Infrastructure Limitations

3.9 High Operational Costs

3.10 Opportunities

3.11 Emerging Markets within MEA

3.12 Technological Advancements

3.13 Strategic Partnerships and Collaborations

3.14 Trends

3.15 Rise of Mobile Virtual Network Operators (MVNOs)

3.16 Integration of Internet of Things (IoT) Solutions

3.17 Shift Towards CloudBased Services

3.18 Government Regulations

3.19 Spectrum Allocation Policies

3.20 Licensing Frameworks

3.21 Data Privacy and Security Regulations

3.22 SWOT Analysis

3.23 Stakeholder Ecosystem

3.24 Porters Five Forces Analysis

3.25 Competitive Landscape

4. MEA Telecom Market Segmentation

4.1 By Service Type (In Value %)

4.2 Mobile Services

4.3 FixedLine Services

4.4 Broadband Services

4.5 By Technology (In Value %)

4.6 4G/LTE

4.7 5G

4.8 Fiber Optics

4.9 Others

4.10 By Transmission (In Value %)

4.11 Wireless Transmission

4.12 Wireline Transmission

4.13 By EndUser (In Value %)

4.14 Residential

4.15 Commercial

4.16 Industrial

4.17 Government

4.18 By Region (In Value %)

4.19 South Africa

4.10 Saudi Arabia

4.11 Egypt

4.12 UAE

4.13 Israel

4.14 Rest of Middle East and Africa

5. MEA Telecom Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.2 Saudi Telecom Company

5.3 Etisalat Group

5.4 Ooredoo Group

5.5 Zain Group

5.6 Oman Telecommunications Company

5.7 Telecom Egypt

5.8 MTN Group

5.9 Vodacom Group

5.10 Orange Middle East and Africa

5.11 Airtel Africa

5.12 Maroc Telecom

5.13 Telkom SA

5.14 Cell C

5.15 Safaricom

5.16 Batelco

5.17 Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Market Share, Service Portfolio, Technological Capabilities, Regional Presence)

5.18 Market Share Analysis

5.19 Strategic Initiatives

5.20 Mergers and Acquisitions

5.21 Investment Analysis

5.22 Venture Capital Funding

5.23 Government Grants

5.24 Private Equity Investments

6. MEA Telecom Market Regulatory Framework

6.1 Telecommunications Regulatory Authorities

6.2 Licensing and Compliance Requirements

6.3 Spectrum Management Policies

6.4 Data Protection and Privacy Laws

7. MEA Telecom Future Market Size (In USD Million)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. MEA Telecom Future Market Segmentation

8.1 By Service Type (In Value %)

8.2 By Technology (In Value %)

8.3 By Transmission (In Value %)

8.4 By EndUser (In Value %)

8.5 By Region (In Value %)

9. MEA Telecom Market Analysts Recommendations

9.1Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the MEA Telecom Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industrylevel information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the MEA Telecom Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computerassisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple telecom operators to acquire detailed insights into service segments, network expansion, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the MEA Telecom market.

Frequently Asked Questions

1. How big is the MEA Telecom Market?

The MEA Telecom market is valued at around USD 34 billion, driven by increasing demand for connectivity and the expansion of mobile networks across the region.

2. What are the main growth drivers in the MEA Telecom Market?

Key growth drivers in the MEA Telecom market include rising mobile penetration, government initiatives for digital transformation, and the increasing adoption of 5G technology.

3. Who are the major players in the MEA Telecom Market?

Major players in the MEA Telecom market include Saudi Telecom Company (STC), Etisalat Group, MTN Group, and Vodafone Egypt, among others, all of which have a strong presence in the region.

4. What are the challenges faced by the MEA Telecom Market?

Challenges in the MEA Telecom market include regulatory compliance issues and infrastructure limitations in rural areas, which can hinder market expansion and service delivery.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.