MENA Fitness Equipment Market Outlook to 2029

Region:Global

Author(s):Khushi Khatreja

Product Code:KR1461

December 2024

90

About the Report

MENA Fitness Equipment Market Overview

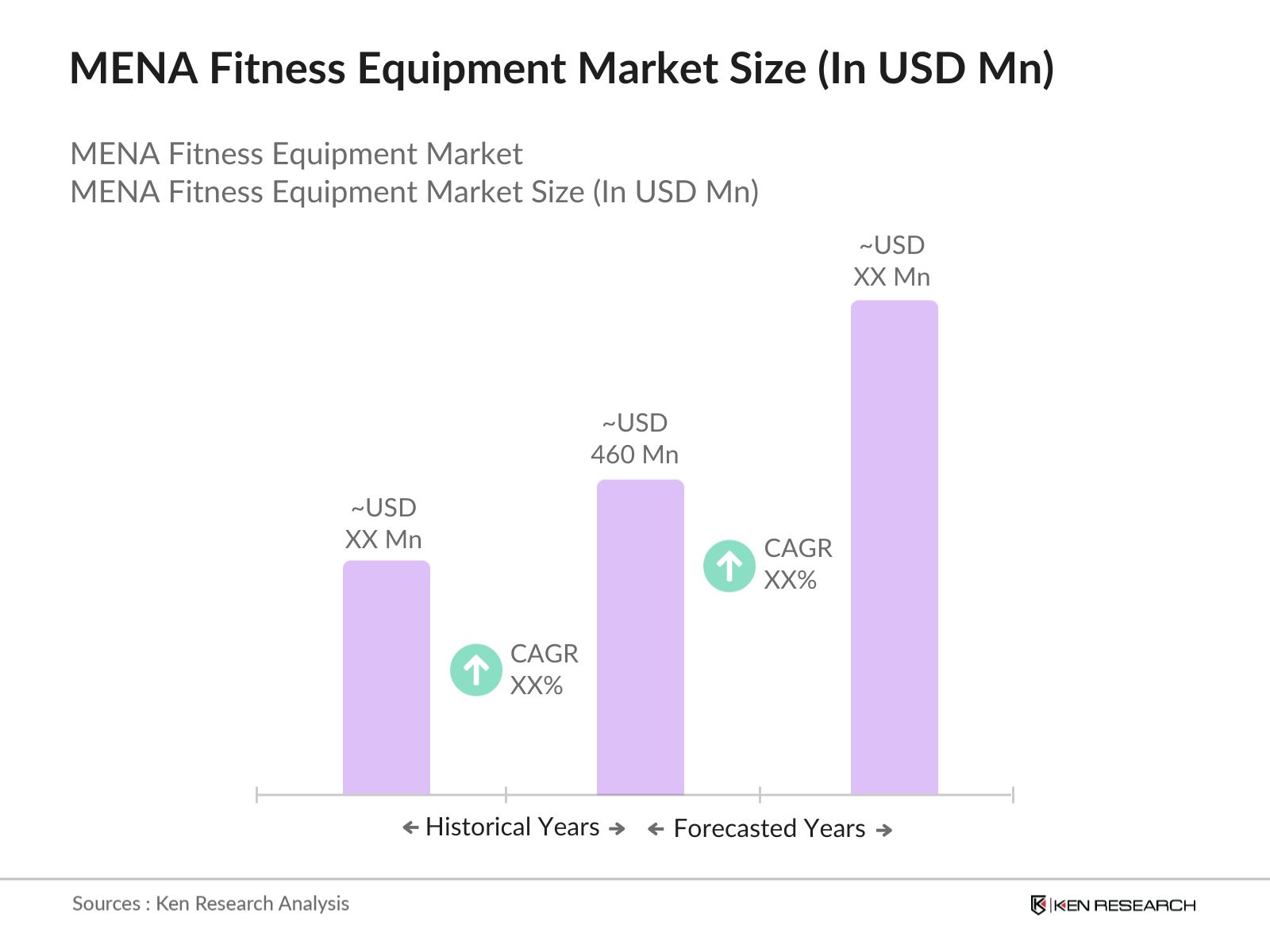

- The MENA fitness equipment market is valued at USD 460 million based on a five-year historical analysis. This market is primarily driven by increasing health awareness among consumers, government initiatives promoting healthy lifestyles, and the expansion of fitness centers and gym chains across the region. Rising adoption of home fitness equipment and integration of IoT in fitness devices have further propelled growth.

- The United Arab Emirates and Saudi Arabia dominate the MENA fitness equipment market due to high disposable incomes, the popularity of luxury fitness clubs, and government-backed health initiatives such as Saudi Vision 2030. These countries have seen a surge in fitness centers and gyms catering to a growing population of health-conscious individuals, alongside a robust demand for home fitness equipment.

- In 2023, several MENA countries have implemented subsidies and incentives aimed at bolstering domestic production of fitness equipment, which is reshaping the competitive landscape of the market. These policies are particularly evident in countries like Saudi Arabia and the United Arab Emirates (UAE), where government support is fostering local manufacturing and reducing reliance on imports. As part of its Vision 2030 initiative, Saudi Arabia has introduced financial incentives for local manufacturers of fitness equipment. This includes tax breaks and grants aimed at encouraging investments in production facilities.

MENA Fitness Equipment Market Segmentation

The MENA Fitness Equipment Market is segmented by Type of Institution, Type of Club, region, etc.

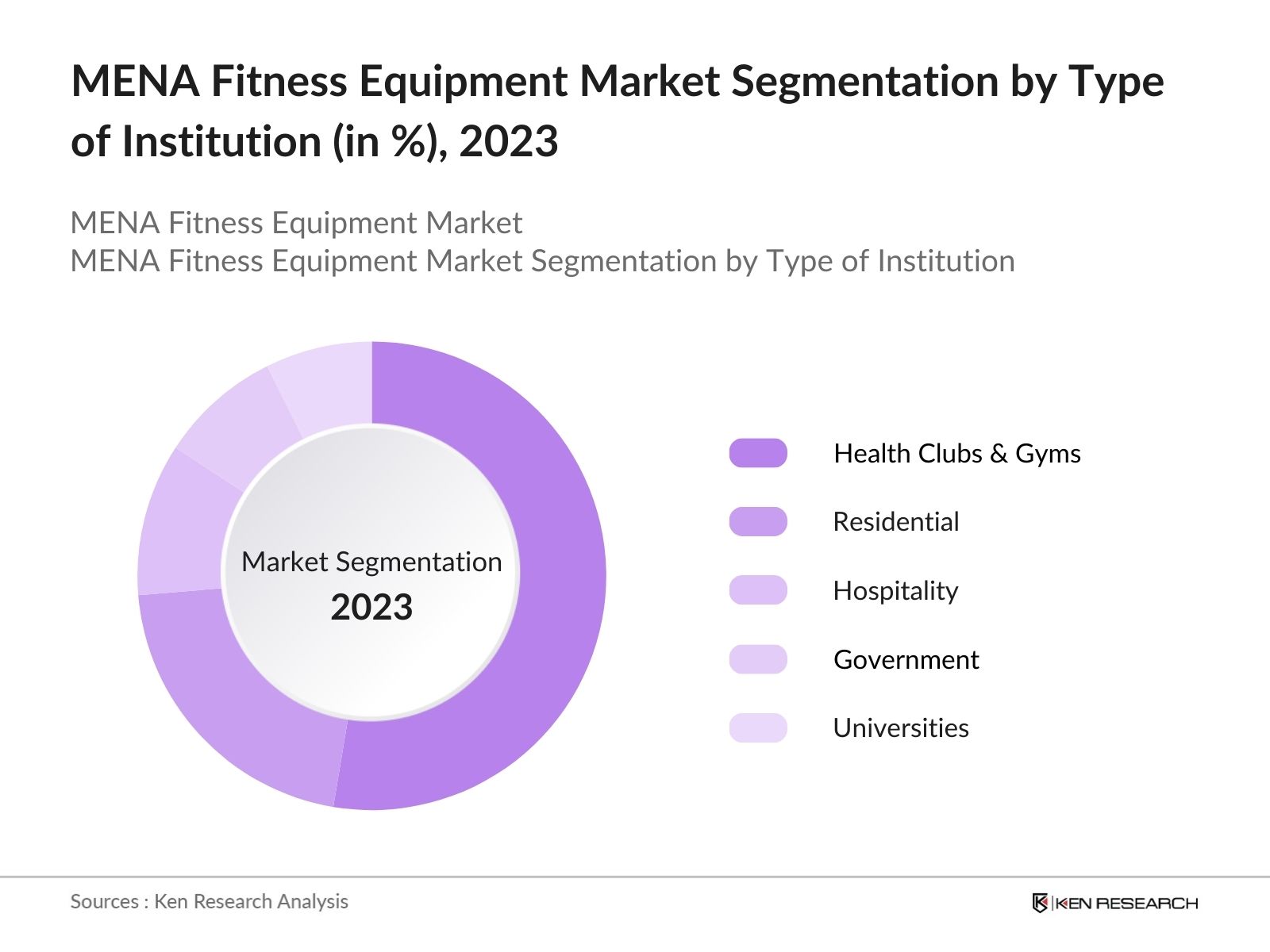

- By Type of Institution: The MENA Fitness Equipment Market is segmented by type of institution into Health Clubs & Gyms, Residential, Hospitality, Government, Universities, and Corporate Parks. Health clubs and gyms hold the largest market share. This dominance is attributed to the increasing number of fitness centers and gyms across the region, driven by rising health consciousness and disposable incomes. The expansion of international gym chains and the popularity of group fitness classes have further bolstered this segment's prominence.

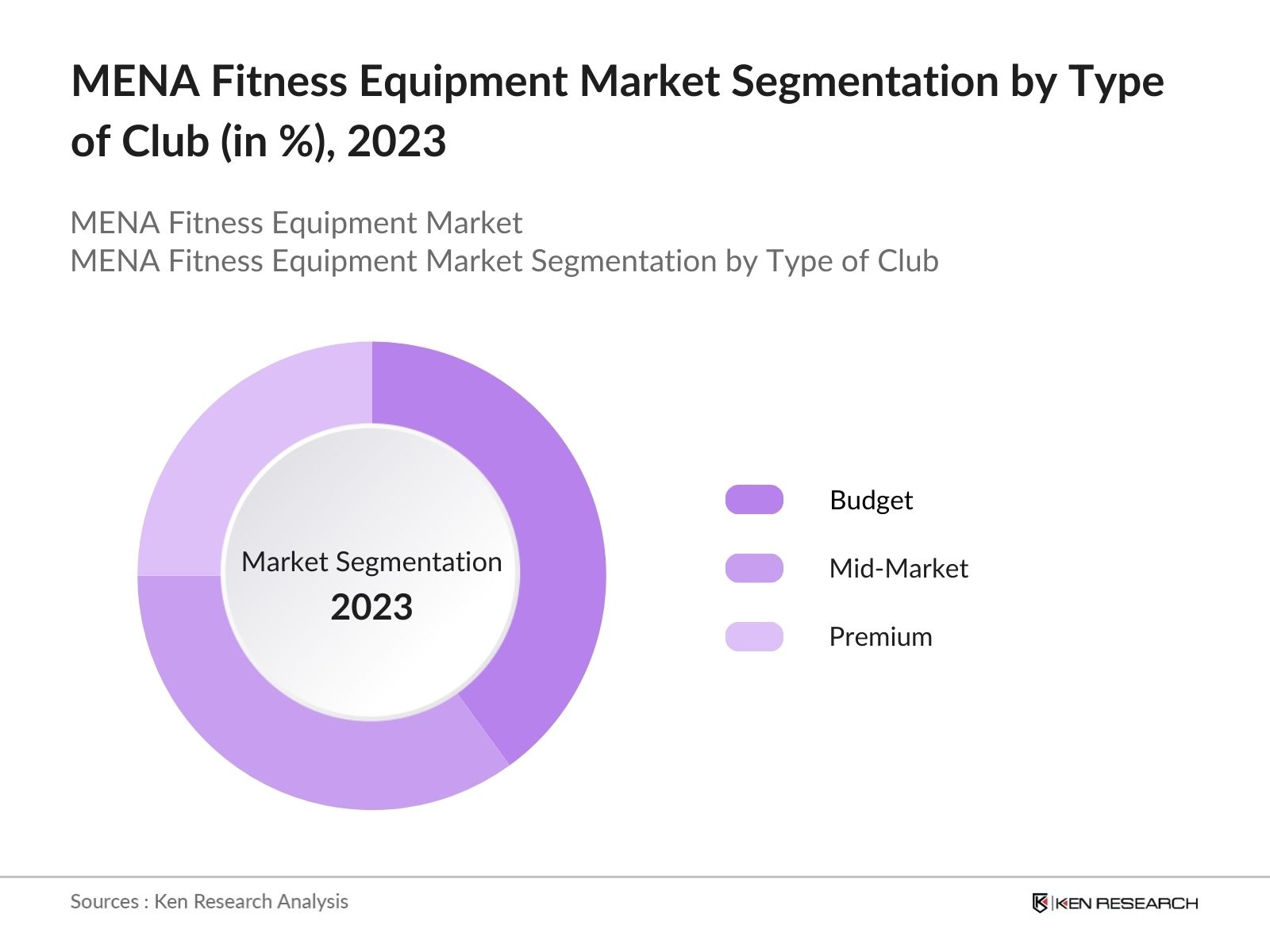

- By Type of Club: The MENA Fitness Equipment Market is segmented by type of club into Budget, Mid-Market, and Premium. Budget clubs lead the market appealing to a broad demographic seeking affordable fitness solutions. Their cost-effective membership plans and widespread accessibility make them attractive to price-sensitive consumers, contributing to their significant market presence.

- By Region: The MENA Fitness Equipment Market is segmented by region into the United Arab Emirates (UAE), Saudi Arabia (KSA), Egypt, Qatar, and Kuwait. The UAE holds the largest regional market share driven by high disposable incomes, a strong expatriate population, and government initiatives promoting health and fitness. The proliferation of luxury fitness centers and wellness programs further cements its leading position in the MENA fitness equipment market.

MENA Fitness Equipment Market Competitive Landscape

The fitness industry in the MENA region is characterized by a diverse range of fitness centers, each catering to specific market segments and offering unique services. This diversity reflects the varying preferences, lifestyles, and health needs of the population across different countries.

MENA Fitness Equipment Industry Analysis

Market Growth Drivers

-

Virtual Reality (VR) and Augmented Reality (AR) Workouts: VR and AR technologies are transforming traditional workout experiences by providing immersive environments that enhance user engagement. For instance, users can participate in virtual classes or simulate outdoor activities from their homes, making workouts more enjoyable and less monotonous. The global VR fitness market is witnessing strong growth, with rising adoption across the MENA region as fitness centers embrace these technologies to attract tech-savvy consumers.

- AI-Powered Personal Training: AI-driven solutions allow for highly personalized workout plans that adapt in real time based on user performance and preferences. This technology analyzes data from wearables and fitness apps to provide tailored feedback, ensuring users achieve their fitness goals more efficiently.

- Integrated Health Data Platforms: Integrated health data platforms enable users to track various health metrics (such as heart rate, activity levels, and nutrition) in one place. This comprehensive approach encourages users to take a proactive role in their health management.

Market Challenges

-

High Import Costs: The MENA region heavily relies on imported fitness equipment due to a lack of extensive local manufacturing capabilities. High tariffs and shipping costs can significantly increase the retail prices of fitness equipment. For example, the average price of imported gym machines can be inflated by up to 30% due to these additional costs, making them less accessible for average consumers and small gyms.

- Competition from Alternative Fitness Solutions: The rise of digital fitness solutions, such as mobile apps and online workout programs, presents competition for traditional fitness equipment sales. Consumers may opt for virtual classes or home workouts that require little to no equipment. As more people turn to home workouts facilitated by technology, traditional gym memberships, and large equipment purchases may decline.

MENA Fitness Equipment Future Market Outlook

The MENA fitness equipment market is on the brink of substantial growth including increasing health awareness, government initiatives promoting active lifestyles, and technological advancements in fitness solutions.

Market Opportunities

-

Growth of Health Clubs and Fitness Centers: The number of health clubs and fitness centers is on the rise as consumers increasingly seek to adopt healthier lifestyles. Major international fitness operators, such as Fitness First and Golds Gym, have expanded their presence in the region, indicating strong growth potential.

- Technological Innovations: The integration of technology into fitness equipmentsuch as AI-powered personal training apps and connected devicesoffers personalized workout experiences and real-time feedback. This innovation appeals particularly to tech-savvy consumers looking for efficiency and engagement in their fitness routines.

Scope of the Report

|

Segment |

Sub-Segments |

|

Type of Institution |

Health Clubs & Gyms Residential Hospitality Government Universities Corporate Parks |

|

Club Type |

Budget Mid-Market Premium |

|

Distribution Channel |

Offline Retail Online Retail |

|

Price Point |

Premium/Luxury Mass Market |

|

Country |

United Arab Emirates (UAE) Saudi Arabia (KSA) Egypt Qatar Kuwait |

Products

Key Target Audience

Fitness Equipment Manufacturers

Gym Chains and Health Clubs

Home Fitness Equipment Retailers

Corporate Wellness Program Providers

Sports and Fitness Technology Companies

Hospitality Chains and Luxury Hotels

Government and Regulatory Bodies (e.g., General Authority for Sports, UAE Ministry of Health)

Investor and Venture Capitalist Firms

Companies

Major Players mentioned in the report

Life Fitness

Technogym

Johnson Health Tech

Precor Incorporated

ICON Health & Fitness

Cybex International

Matrix Fitness

True Fitness Technology

Impulse (Qingdao) Health Tech

Body-Solid Inc.

Torque Fitness

Core Health & Fitness

Nautilus Inc.

Afton Fitness

Fitness World

Table of Contents

1. Product Taxonomy

2. MENA Fitness Equipment Market

2.1. Executive Summary MENA Fitness Equipment Market

2.2. Consumer Mindset for Fitness in MENA Region

2.3. Fitness Market Business Model

2.4. Stratification of Brand Positioning of Gyms in MENA Region

2.5. Technological Disruptions for Fitness Centers

2.6. Future Trends and Outlook for MENA Fitness Industry

3. UAE Fitness Equipment Market

3.1. Executive Summary UAE Fitness Equipment Market, 2018-2029

3.2. Ecosystem of UAE Fitness Equipment Market, 2023

3.3. Fitness Equipment Market Size in UAE, 2018-2029F

3.4. Segmentation of Establishments by End-User and Type, 2023 & 2029

3.5. Number of Health Clubs/Gym Chains in UAE and Segmentation by Club Type, 2018-2029

3.6. Cross Comparison for Budget, Mid-Market, and Premium Gyms in UAE, 2023

3.7. Average Spending Across Popular Regions in Each Club Type, 2023

3.8. Market Share of Fitness Equipment Distributors in UAE, 2023

3.9. Cross Comparison Between Key Gym Operators in UAE, 2023

4. KSA Fitness Equipment Market

4.1. Executive Summary KSA Fitness Equipment Market, 2018-2029

4.2. Ecosystem Supply Side of Fitness Equipment Market in KSA

4.3. Ecosystem Demand Side of Fitness Equipment Market in KSA

4.4. Fitness Equipment Market Size in KSA, 2018-2029

4.5. Number of Gym Establishments in KSA by Type of Institution, 2023

4.6. Segmentation of Establishment by Type of Club and Average Spending Across Regions by Club Type in KSA, 2023

4.7. Cross Comparison for Budget, Mid-Market, and Premium Gyms in KSA

4.8. Cross Comparison Between Key Gym Operators in KSA, 2023

5. Qatar Fitness Equipment Market

5.1. Executive Summary Qatar Fitness Equipment Market, 2018-2029

5.2. Ecosystem Supply Side of Fitness Equipment Market in Qatar

5.3. Ecosystem Demand Side of Fitness Equipment Market in Qatar

5.4. Fitness Equipment Market Size in Qatar, 2018-2029

5.5. Number of Gym Establishments in Qatar by Type of Institution, 2023

5.6. Segmentation of Establishment by Type of Club and Average Spending Across Regions by Club Type in Qatar, 2023

5.7. Cross Comparison for Budget, Mid-Market, and Premium Gyms in Qatar

5.8. Cross Comparison Between Key Gym Operators in Qatar, 2023

6. Kuwait Fitness Equipment Market

6.1. Executive Summary Kuwait Fitness Equipment Market, 2018-2029

6.2. Ecosystem Supply Side of Fitness Equipment Market in Kuwait

6.3. Ecosystem Demand Side of Fitness Equipment Market in Kuwait

6.4. Fitness Equipment Market Size in Kuwait, 2018-2029

6.5. Number of Gym Establishments in Kuwait by Type of Institution, 2023

6.6. Segmentation of Establishment by Type of Club and Average Spending Across Regions by Club Type in Kuwait, 2023

6.7. Cross Comparison for Budget, Mid-Market, and Premium Gyms in Kuwait

6.8. Cross Comparison Between Key Gym Operators in Kuwait, 2023

7. Egypt Fitness Equipment Market

7.1. Executive Summary Egypt Fitness Equipment Market, 2018-2029

7.2. Ecosystem Supply Side of Fitness Equipment Market in Egypt

7.3. Ecosystem Demand Side of Fitness Equipment Market in Egypt

7.4. Fitness Equipment Market Size in Egypt, 2018-2029

7.5. Number of Gym Establishments in Egypt by Type of Institution, 2023

7.6. Segmentation of Establishment by Type of Club and Average Spending Across Regions by Club Type in Egypt, 2023

7.7. Cross Comparison for Budget, Mid-Market, and Premium Gyms in Egypt

7.8. Cross Comparison Between Key Gym Operators in Egypt, 2023

8. Research Methodology

8.1. Market Definitions

8.2. Abbreviations

8.3. Market Sizing Approach

8.4. Consolidated Research Approach

8.5. Sample Size Inclusion

8.6. Limitation and Future Conclusions

8.7. Diversification Strategies: Next Phase

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping stakeholders across the MENA fitness equipment market. Desk research is conducted using industry reports and proprietary databases to identify and define key variables affecting market growth, such as consumer demand trends and technological innovations.

Step 2: Market Analysis and Construction

In this phase, historical data on the fitness equipment market is analyzed. Factors like equipment sales trends, gym memberships, and revenue contributions from various regions are evaluated to build accurate market estimates.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses are developed and validated through interviews with industry experts and manufacturers. These consultations provide real-time insights into challenges and opportunities in the market, ensuring a well-rounded analysis.

Step 4: Research Synthesis and Final Output

A synthesis of findings is conducted, integrating insights from primary and secondary research. This ensures the final report provides a detailed and validated perspective on the MENA fitness equipment market.

Frequently Asked Questions

01. How big is the MENA Fitness Equipment Market?

The MENA fitness equipment market is valued at USD 460 million, driven by the rising popularity of fitness activities and growing health consciousness across the region.

02. What are the challenges in the MENA Fitness Equipment Market?

Challenges include high costs of fitness equipment, limited accessibility in rural areas, and cultural barriers to fitness adoption in certain parts of the region.

03. Who are the major players in the MENA Fitness Equipment Market?

Key players include Life Fitness, Technogym, Johnson Health Tech, Precor Incorporated, and ICON Health & Fitness.

04. What are the growth drivers of the MENA Fitness Equipment Market?

The market is driven by health awareness, government initiatives promoting fitness, and the integration of smart technologies in equipment.

05. What trends are shaping the MENA Fitness Equipment Market?

Trends include the adoption of IoT-enabled fitness equipment, the popularity of at-home workouts, and the rise of boutique fitness studios.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.