MENA Healthcare Market Outlook to 2030

Region:Africa

Author(s):Sanjna

Product Code:KROD9817

Region:Africa

Author(s):Sanjna

Product Code:KROD9817

December 2024

96

Listen to the audio summary

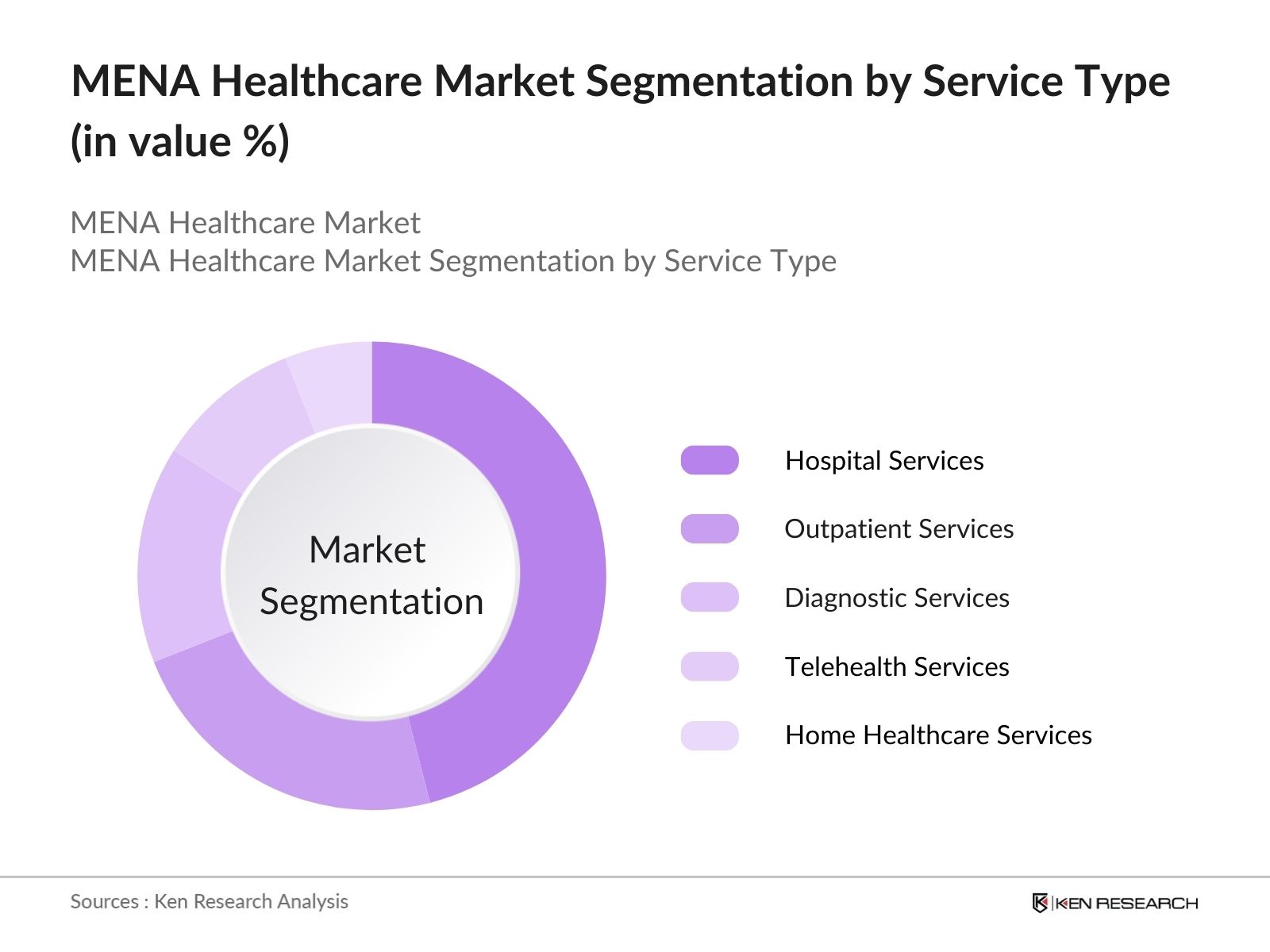

By Service Type: The MENA healthcare market is segmented by service type into hospital services, outpatient services, diagnostic services, telehealth services, and home healthcare services. Hospital services have a dominant market share in the MENA healthcare market, owing to the presence of state-of-the-art medical facilities and the increasing incidence of complex diseases requiring specialized care. The high investments in hospital infrastructure, especially in Saudi Arabia and the UAE, are also contributing to this segment's dominance.

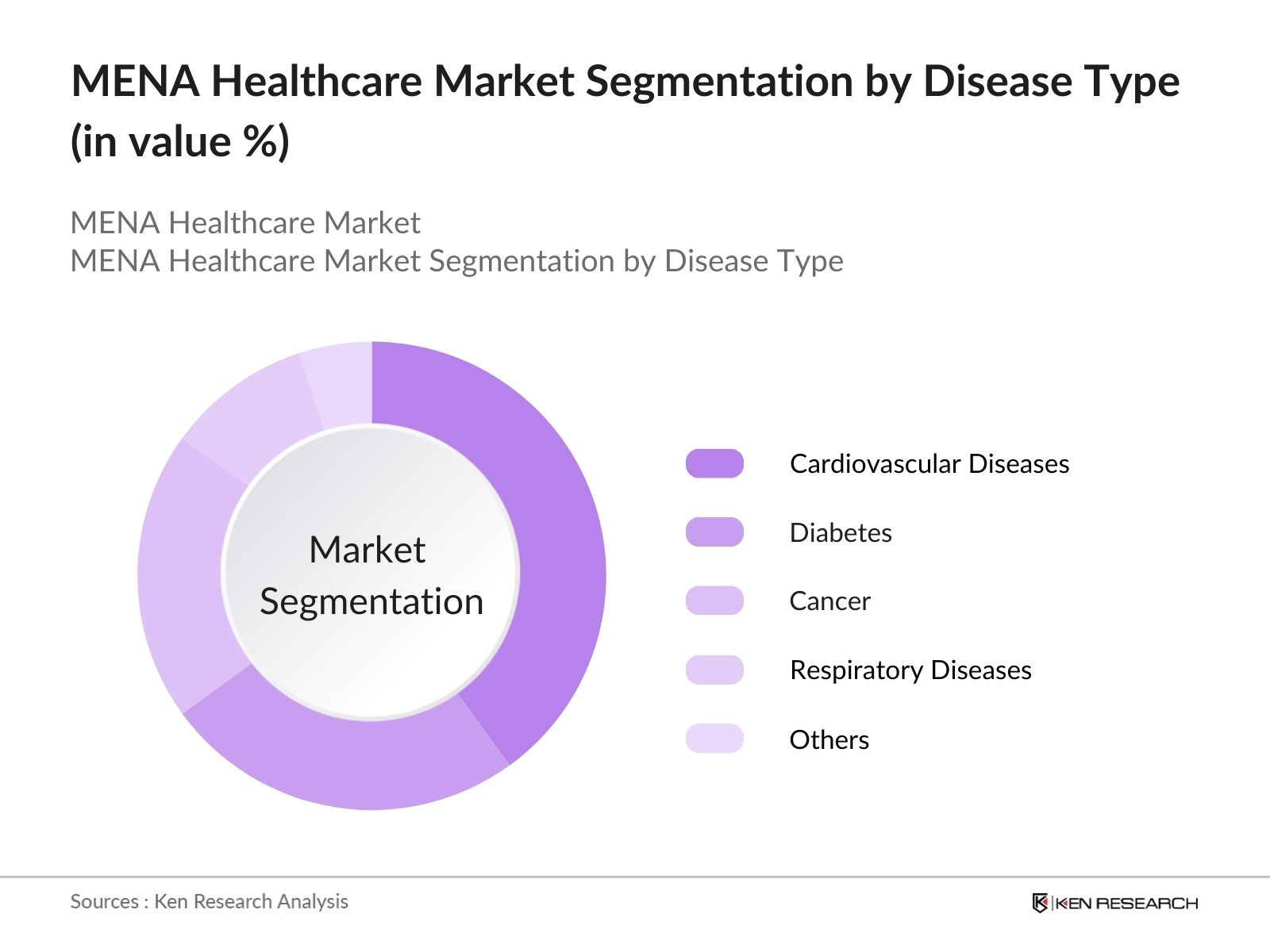

By Disease Type: The MENA healthcare market is also segmented by disease type into cardiovascular diseases, diabetes, cancer, respiratory diseases, and others. Cardiovascular diseases dominate this segment due to the rising prevalence of sedentary lifestyles and unhealthy diets in the region. Government programs aimed at reducing heart disease incidences and the establishment of specialized cardiac care centers contribute to the segment's growth.

The MENA healthcare market is dominated by major players, including multinational corporations and local entities. These companies invest heavily in technology, partnerships, and infrastructure development, shaping the competitive dynamics of the region. The MENA healthcare market is led by both local and international players such as Daman, Bupa Global, and Cigna, showcasing a blend of strong regional presence and global expertise. The competitive landscape reflects a focus on innovation, digital health solutions, and strategic collaborations.

Over the next five years, the MENA healthcare market is expected to experience substantial growth driven by technological advancements, increasing adoption of telemedicine, and government initiatives aimed at improving healthcare accessibility. With a focus on digital transformation and the expansion of medical tourism, the market will continue to attract significant investments.

Expansion of Private Healthcare Sector: Countries like Saudi Arabia and the UAE are encouraging private investments in healthcare through public-private partnerships and favorable policies. For instance, Saudi Arabia aims to increase the private sector's contribution to healthcare from 25% to 35% by 2030, reflecting a strategic focus on PPPs. This expansion presents opportunities for private healthcare providers to establish advanced medical facilities, introduce innovative healthcare solutions, and cater to the growing healthcare needs of the population.

|

Segment |

Sub-Segments |

|

Service Type |

Hospital Services |

|

End User |

Public Sector |

|

Country |

Saudi Arabia |

|

Disease Type |

Cardiovascular Diseases |

|

Technology |

Electronic Health Records (EHR) |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Population Growth and Demographics

3.1.2. Prevalence of Non-Communicable Diseases

3.1.3. Government Initiatives and Investments

3.1.4. Technological Advancements

3.2. Market Challenges

3.2.1. Regulatory and Compliance Issues

3.2.2. High Healthcare Costs

3.2.3. Limited Access in Rural Areas

3.3. Opportunities

3.3.1. Expansion of Private Healthcare Sector

3.3.2. Growth in Medical Tourism

3.3.3. Adoption of Digital Health Solutions

3.4. Trends

3.4.1. Telemedicine and Remote Patient Monitoring

3.4.2. Integration of Artificial Intelligence in Diagnostics

3.4.3. Personalized Medicine and Genomics

3.5. Government Regulations

3.5.1. Health Insurance Mandates

3.5.2. Quality Standards and Accreditation

3.5.3. Public-Private Partnerships

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4.1. By Service Type (In Value %)

4.1.1. Hospital Services

4.1.2. Outpatient Services

4.1.3. Diagnostic Services

4.1.4. Telehealth Services

4.1.5. Home Healthcare Services

4.2. By End User (In Value %)

4.2.1. Public Sector

4.2.2. Private Sector

4.2.3. Non-Governmental Organizations (NGOs)

4.3. By Country (In Value %)

4.3.1. Saudi Arabia

4.3.2. United Arab Emirates

4.3.3. Egypt

4.3.4. Kuwait

4.3.5. Qatar

4.3.6. Rest of MENA

4.4. By Disease Type (In Value %)

4.4.1. Cardiovascular Diseases

4.4.2. Diabetes

4.4.3. Cancer

4.4.4. Respiratory Diseases

4.4.5. Others

4.5. By Technology (In Value %)

4.5.1. Electronic Health Records (EHR)

4.5.2. Telemedicine Platforms

4.5.3. Health Information Systems

4.5.4. Wearable Devices

4.5.5. Artificial Intelligence Applications

5.1. Detailed Profiles of Major Companies

5.1.1. National Health Insurance Company (Daman)

5.1.2. Bupa Global

5.1.3. Cigna

5.1.4. Allianz

5.1.5. ADNIC

5.1.6. MetLife Services and Solutions, LLC

5.1.7. AXA Group

5.1.8. Delta Life Insurance Company Limited

5.1.9. Dhofar Insurance Company S.A.O.G.

5.1.10. Misr Life Insurance

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Market Share, Service Portfolio, Regional Presence, Strategic Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Healthcare Policies and Reforms

6.2. Licensing and Accreditation Processes

6.3. Compliance Requirements

6.4. International Standards and Certifications

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Service Type (In Value %)

8.2. By End User (In Value %)

8.3. By Country (In Value %)

8.4. By Disease Type (In Value %)

8.5. By Technology (In Value %)

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The first step involved mapping the healthcare ecosystem across the MENA region, identifying key variables such as service type, disease prevalence, and regional trends. Extensive desk research using government publications and proprietary databases provided a comprehensive data foundation.

This step focused on analyzing historical data for the healthcare market in MENA, including penetration rates, service demand, and revenue generation. The data was validated through cross-verification with industry reports and official statistics.

Insights were refined through consultations with industry experts, including hospital administrators, policymakers, and healthcare technology providers. These consultations ensured a robust and reliable data interpretation process.

The final stage included synthesizing all collected data to prepare actionable insights, segmentation analyses, and competitive benchmarking for the MENA healthcare market.

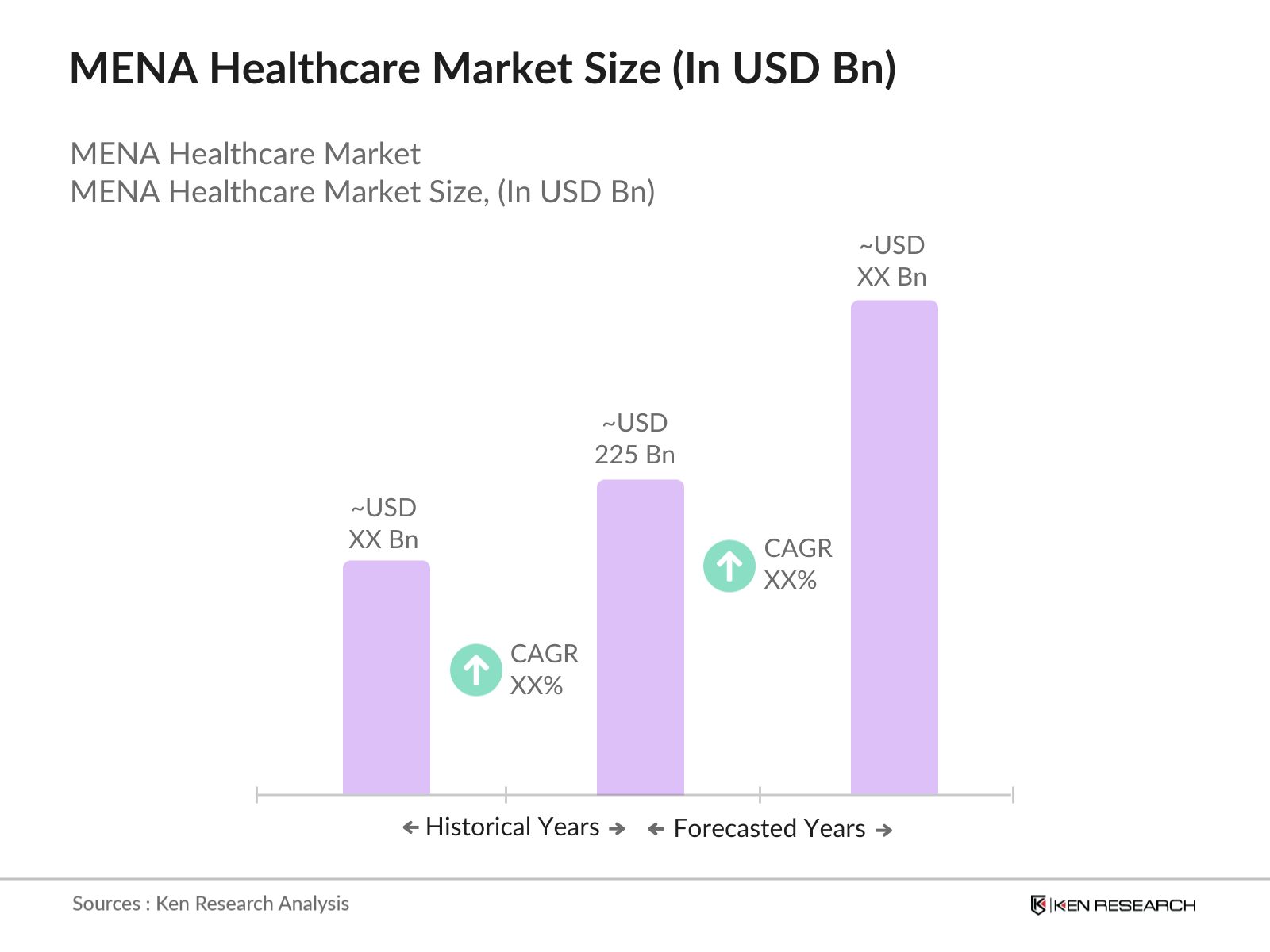

The MENA healthcare market is valued at USD 225 billion, driven by robust investments in infrastructure, the adoption of advanced medical technologies, and a focus on universal healthcare coverage.

Challenges in MENA healthcare market include regulatory barriers, high operational costs, and limited access to healthcare in rural and underserved areas. These issues impact the overall efficiency of healthcare delivery.

Key players in MENA healthcare market include Daman, Bupa Global, Cigna, Allianz, and ADNIC. Their dominance is due to their comprehensive service portfolios, strong regional presence, and strategic partnerships.

Growth in MENA healthcare market is propelled by rising disease prevalence, increased healthcare spending, and government initiatives to improve medical infrastructure and services.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.