Middle East & Africa Bottled Water Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD4008

December 2024

86

About the Report

Middle East & Africa Bottled Water Market Overview

- The bottled water market in the Middle East & Africa is valued at USD 13 billion based on a five-year historical analysis. The market's growth is driven by increasing consumer awareness regarding hydration, health benefits, and the scarcity of safe drinking water in many regions. Additionally, rising urbanization and the tourism boom in several Gulf countries have escalated demand, leading to a surge in bottled water consumption. This market is also benefiting from the high temperatures in the region, making bottled water an essential product for daily consumption.

- Several countries, including Saudi Arabia, the UAE, and South Africa, dominate the bottled water market due to their substantial urban populations and robust tourism industries. Saudi Arabia and the UAE, in particular, have witnessed rising demand for premium bottled water, fueled by affluent consumer segments and the region's desert climate. In contrast, South Africa leads due to its large population and the increasing preference for bottled water amid concerns about water safety and infrastructure challenges.

- Plant-based packaging materials are gaining traction in the MEA bottled water market as consumers become more environmentally conscious. In 2024, several UAE-based bottled water companies, such as Agthia, introduced biodegradable plant-based bottles, which now make up 5% of the market. This shift aligns with global efforts to reduce plastic waste and appeals to eco-conscious consumers across the region. Government support for sustainable packaging initiatives is expected to drive further adoption of plant-based bottles.

Middle East & Africa Bottled Water Market Segmentation

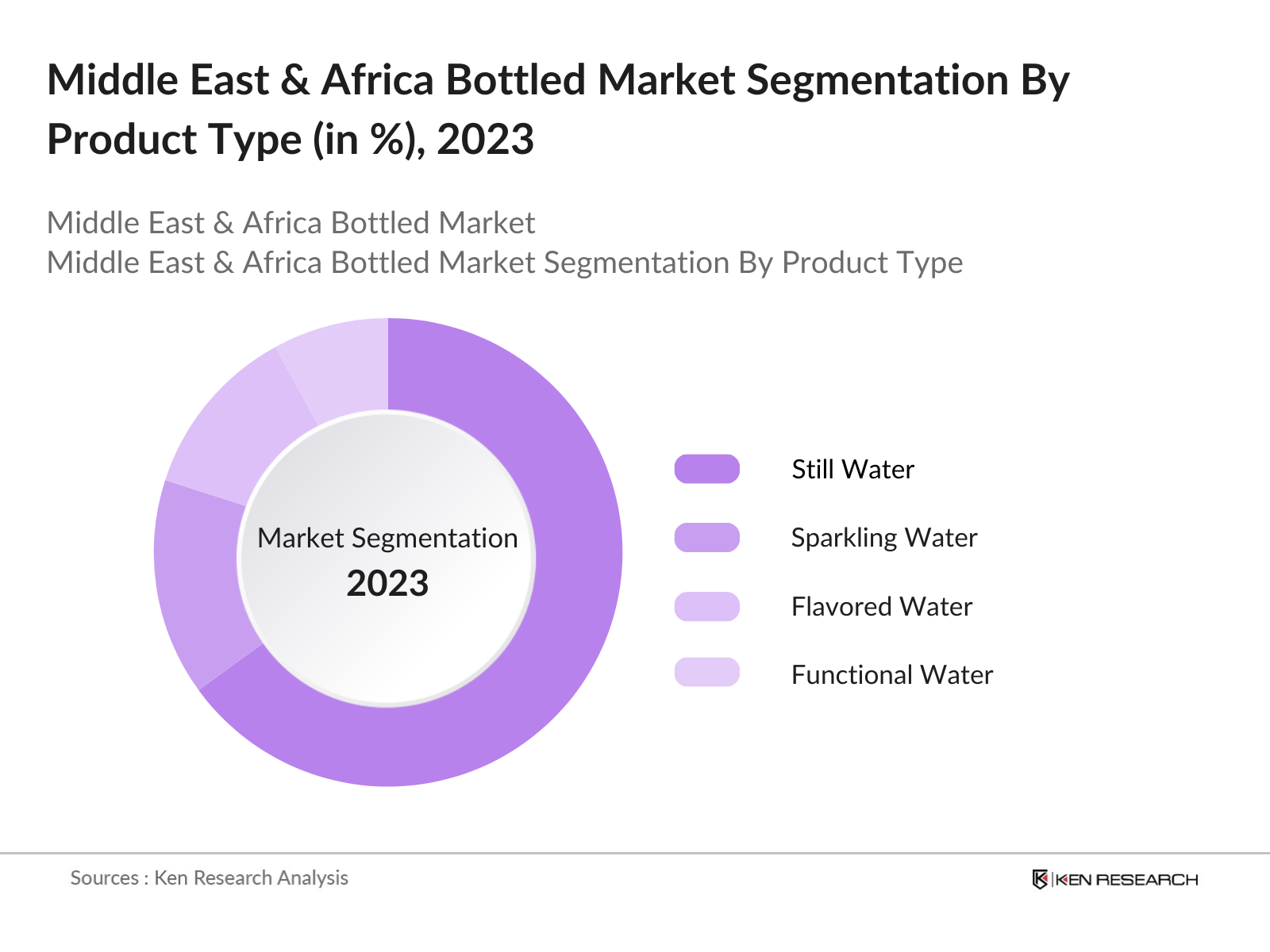

By Product Type: The Middle East & Africa bottled water market is segmented by product type into still water, sparkling water, flavored water, and functional water. Still water holds the dominant share in the market, driven by its affordability and widespread availability. Consumers in this region prefer still water for daily hydration due to its lower cost and the general perception of it being the safest and most natural option. Brands such as Masafi and Nestl Waters have capitalized on this preference by offering various still water products across the region.

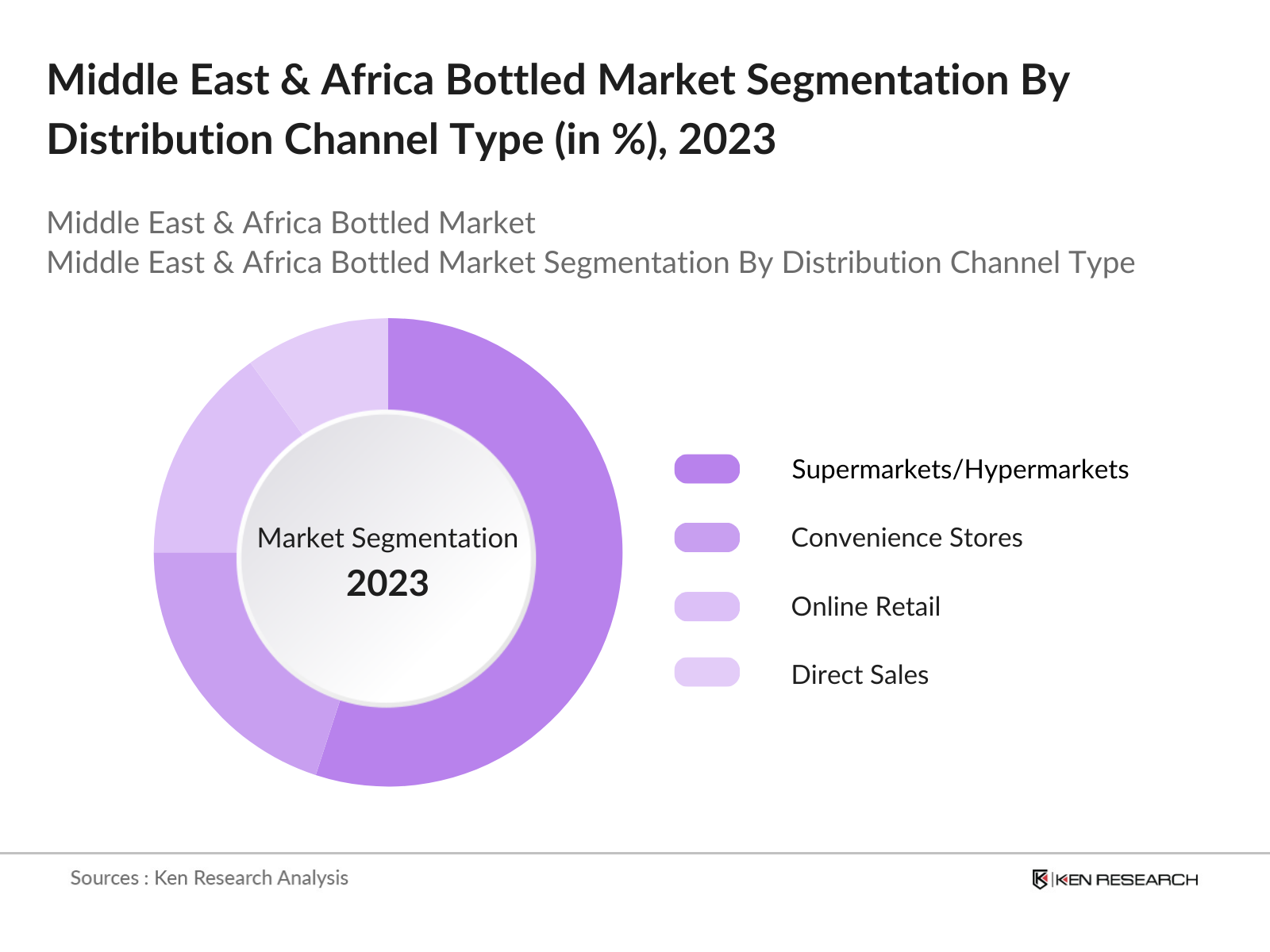

By Distribution Channel: In terms of distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail, and direct sales. Supermarkets and hypermarkets dominate the market, accounting for the largest share of bottled water sales in 2023. The dominance of this channel is attributed to the increasing presence of large retail chains in urban centers and the growing consumer preference for bulk purchases, which are often facilitated by promotions and discounts offered in these outlets.

Middle East & Africa Bottled Water Market Competitive Landscape

The bottled water market in the Middle East & Africa is dominated by both global giants and regional players. Multinational companies such as Nestl Waters and Coca-Cola maintain significant market shares due to their vast distribution networks, strong brand equity, and ability to offer a diverse range of water products. Regional brands like Masafi and Mai Dubai have also established a strong foothold by catering to local tastes and preferences. The competition is characterized by increasing focus on sustainability, with companies adopting environmentally friendly packaging and investing in recycling initiatives to appeal to eco-conscious consumers.

|

Company Name |

Established Year |

Headquarters |

Distribution Network |

Sustainability Initiatives |

Brand Portfolio |

Revenue (USD Bn) |

Product Innovations |

Water Source |

|

Nestl Waters |

1992 |

Vevey, Switzerland |

_ |

_ |

_ |

_ |

_ |

_ |

|

Coca-Cola (Aquafina) |

1886 |

Atlanta, USA |

_ |

_ |

_ |

_ |

_ |

_ |

|

Masafi |

1977 |

Dubai, UAE |

_ |

_ |

_ |

_ |

_ |

_ |

|

Mai Dubai |

2014 |

Dubai, UAE |

_ |

_ |

_ |

_ |

_ |

_ |

|

Danone Waters |

1965 |

Paris, France |

_ |

_ |

_ |

_ |

_ |

_ |

Middle East & Africa Bottled Water Industry Analysis

Growth Drivers

- Increasing Urbanization and Population Growth: The Middle East & Africa (MEA) region is witnessing rapid urbanization, with urban populations growing by over 2 million annually as of 2024, according to the World Bank. This urban shift is directly linked to increased bottled water consumption as urban residents rely more on packaged drinking water. The United Nations reports that by 2025, 60% of the region's population will live in cities, demanding improved access to clean drinking water. Governments have struggled to meet growing water needs, which further drives bottled water demand as an alternative.

- Growing Awareness of Health and Hydration Benefits: Rising awareness of the health benefits of proper hydration has significantly increased the consumption of bottled water in the MEA region. Countries like Saudi Arabia and the UAE have invested in public health campaigns, with reports indicating that nearly 45% of the population in urban areas now prioritizes bottled water over sugary drinks. The World Health Organization estimates that 50% of the population in the Gulf states drinks bottled water daily as part of a healthier lifestyle.

- Expansion of Tourism and Hospitality Sector: Tourism is a significant economic driver in countries such as the UAE, Saudi Arabia, and Egypt, which collectively welcomed over 50 million international visitors in 2023. Bottled water is a staple in hotels, resorts, and restaurants across these countries, contributing to a higher demand for premium bottled water products. The World Tourism Organization highlights that the hospitality sector accounts for over 25% of the bottled water consumption in the region, particularly in tourist-heavy cities like Dubai and Cairo.

Market Challenges

- Environmental Concerns Over Plastic Waste: Plastic waste from bottled water packaging has become a critical environmental issue in the MEA region. As of 2024, nearly 8 million metric tons of plastic waste are generated annually in the region, with a significant portion linked to single-use plastics, including bottled water containers. Government agencies such as the Saudi National Center for Waste Management are pushing for more stringent regulations to curb plastic waste, which has affected the bottled water industry. Environmental groups estimate that only 10% of plastic bottles are recycled in the region.

- High Cost of Water Purification Technologies: The cost of adopting advanced water purification technologies remains high, particularly for local bottled water producers. Desalination is one of the primary sources of bottled water in countries like the UAE and Saudi Arabia, with reports showing that over 60% of bottled water in these countries comes from desalination plants. However, the cost of desalination has increased by 15% in the last two years due to energy price fluctuations and new regulatory requirements. This has led to higher operational costs for bottled water companies.

Middle East & Africa Bottled Water Market Future Outlook

Over the next five years, the Middle East & Africa bottled water market is expected to grow steadily, driven by increasing concerns about water safety, rising health consciousness, and the development of more sustainable packaging options. The shift towards premium and functional water categories, along with the growing demand for bottled water in tourism-driven economies like the UAE and Saudi Arabia, will further bolster the market. Additionally, the regions extreme weather conditions and the limited availability of potable tap water will continue to fuel the demand for bottled water across all segments.

Opportunities

- Shift Towards Sustainable Packaging Solutions: With growing environmental awareness, there is a significant opportunity for bottled water companies in the MEA region to invest in sustainable packaging. As of 2024, over 10% of bottled water brands in the UAE have transitioned to using recycled plastic or biodegradable materials. The Saudi government has introduced incentives for companies that reduce plastic usage, which is expected to increase the adoption of eco-friendly packaging across the region. National reports indicate that investment in sustainable packaging solutions grew by over $500 million in 2023.

- Expansion in Rural Areas and Untapped Markets: Rural areas across the MEA region represent an untapped market for bottled water companies. According to the World Bank, over 40% of the region's population resides in rural areas, many of whom lack access to clean drinking water. Governments in countries like Morocco and Kenya are investing heavily in rural water infrastructure, creating opportunities for bottled water companies to expand their distribution networks. In 2024, over $1 billion was allocated to improve water access in rural communities across the MEA region, opening new market prospects.

Scope of the Report

|

Product Type |

Still Water, Sparkling Water Flavored Water Functional Water |

|

Distribution Channel |

Supermarkets/Hypermarkets Convenience Stores Online Retail Direct Sales |

|

Packaging Type |

Plastic Bottles Glass Bottles Cans Cartons |

|

Source |

Natural Spring Water Mineral Water Purified Water Distilled Water |

|

Region |

GCC Countries North Africa Sub-Saharan Africa East Africa |

Products

Key Target Audience

Bottled Wate Companies

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (GCC Water Regulatory Authority, African Water Development Council)

Food & Beverage Companies

Hospitality and Tourism Industry

Environmental Agencies (Middle East Waste Management Regulatory Body, African Environmental Management Agency)

Distribution Channel Companies

Companies

Major Players in the Middle East & Africa Bottled Water Market

Nestl Waters

Coca-Cola Company

PepsiCo Inc.

Danone Waters

Masafi

Mai Dubai

Agthia Group (Al Ain)

Bisleri International

Awafi Mineral Water Co.

Hayat Water

Aquafina (PepsiCo)

Jannah Water

Highland Spring Group

Suntory Beverage & Food

Al Bayan Water Company

Table of Contents

1. Middle East & Africa Bottled Water Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Middle East & Africa Bottled Water Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Middle East & Africa Bottled Water Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Urbanization and Population Growth

3.1.2. Growing Awareness of Health and Hydration Benefits

3.1.3. Expansion of Tourism and Hospitality Sector

3.1.4. Rising Demand for Premium and Flavored Water

3.2. Market Challenges

3.2.1. Environmental Concerns Over Plastic Waste

3.2.2. High Cost of Water Purification Technologies

3.2.3. Fluctuating Regulatory Framework Across Countries

3.2.4. Market Competition from Local Water Brands

3.3. Opportunities

3.3.1. Shift Towards Sustainable Packaging Solutions

3.3.2. Expansion in Rural Areas and Untapped Markets

3.3.3. Growing Investment in Recycling and Water Purification

3.3.4. Rising Demand for Alkaline and Mineral-Enriched Water

3.4. Trends

3.4.1. Emergence of Plant-Based Bottled Water Packaging

3.4.2. Increased Demand for On-the-Go Bottled Water Formats

3.4.3. Integration of Smart Technologies in Bottled Water Distribution

3.4.4. Rising Preference for Sparkling and Functional Water

3.5. Government Regulation

3.5.1. Bottled Water Standards and Safety Regulations

3.5.2. Plastic Waste Reduction Policies and Bans on Single-Use Plastics

3.5.3. Import/Export Tariffs on Bottled Water

3.5.4. Environmental Compliance for Water Extraction and Bottling

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. Middle East & Africa Bottled Water Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Still Water

4.1.2. Sparkling Water

4.1.3. Flavored Water

4.1.4. Functional Water

4.2. By Distribution Channel (In Value %)

4.2.1. Supermarkets/Hypermarkets

4.2.2. Convenience Stores

4.2.3. Online Retail

4.2.4. Direct Sales

4.3. By Packaging Type (In Value %)

4.3.1. Plastic Bottles

4.3.2. Glass Bottles

4.3.3. Cans

4.3.4. Cartons

4.4. By Source (In Value %)

4.4.1. Natural Spring Water

4.4.2. Mineral Water

4.4.3. Purified Water

4.4.4. Distilled Water

4.5. By Region (In Value %)

4.5.1. GCC Countries

4.5.2. North Africa

4.5.3. Sub-Saharan Africa

4.5.4. East Africa

5. Middle East & Africa Bottled Water Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Nestl Waters

5.1.2. Coca-Cola Company

5.1.3. PepsiCo Inc.

5.1.4. Danone Waters

5.1.5. Al Ain Water

5.1.6. Masafi

5.1.7. Mai Dubai

5.1.8. Agthia Group (Al Ain)

5.1.9. Bisleri International

5.1.10. Awafi Mineral Water Co.

5.1.11. Hayat Water

5.1.12. Aquafina (PepsiCo)

5.1.13. Jannah Water

5.1.14. Highland Spring Group

5.1.15. Suntory Beverage & Food

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Revenue, Market Share, Product Portfolio, Sustainability Initiatives, Distribution Network, Innovation Capabilities)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers & Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6. Middle East & Africa Bottled Water Market Regulatory Framework

6.1. Water Quality Standards

6.2. Environmental Regulations for Bottling and Extraction

6.3. Labeling and Packaging Regulations

6.4. Import/Export Regulations and Trade Agreements

7. Middle East & Africa Bottled Water Future Market Size (In USD Bn)

7.1. Key Drivers of Future Growth

7.2. Projected Trends in Bottled Water Consumption

8. Middle East & Africa Bottled Water Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Packaging Type (In Value %)

8.4. By Source (In Value %)

8.5. By Region (In Value %)

9. Middle East & Africa Bottled Water Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing and Branding Initiatives

9.4. White Space Opportunities Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

In the first phase, we developed a comprehensive ecosystem map of the Middle East & Africa Bottled Water Market, identifying key stakeholders such as manufacturers, retailers, regulatory bodies, and consumers. The objective was to pinpoint the key variables influencing market dynamics, such as water safety standards, distribution infrastructure, and consumer preferences, through secondary research leveraging trusted industry sources.

Step 2: Market Analysis and Construction

We gathered historical data on bottled water consumption, distribution channels, and market penetration across various sub-regions. This phase also involved analyzing market metrics such as consumption trends, revenue streams from different product categories, and the growth trajectory of premium water brands.

Step 3: Hypothesis Validation and Expert Consultation

Key market hypotheses, particularly those concerning product innovation and sustainable practices, were validated through in-depth interviews with industry experts, bottling companies, and distributors. These consultations offered valuable insight into market expansion strategies and regional consumer behaviors.

Step 4: Research Synthesis and Final Output

The final phase synthesized primary and secondary data, allowing us to cross-validate figures and market trends. We engaged with major bottled water producers to refine estimates for sales, demand shifts, and product developments, ensuring an accurate, well-rounded market analysis.

Frequently Asked Questions

1. How big is the Middle East & Africa Bottled Water Market?

The Middle East & Africa bottled water market is valued at USD 13 billion, driven by increasing consumer awareness of hydration benefits and the region's hot climate.

2. What are the major challenges in the Middle East & Africa Bottled Water Market?

Challenges include high plastic waste concerns, fluctuating water sourcing regulations, and intense competition among both global and regional brands.

3. Who are the key players in the Middle East & Africa Bottled Water Market?

Major players include Nestl Waters, Coca-Cola Company, Masafi, Mai Dubai, and Danone Waters, each holding significant market presence due to strong distribution networks and brand recognition.

4. What is driving growth in the Middle East & Africa Bottled Water Market?

Growth drivers include increasing urbanization, rising health awareness, expanding tourism, and the growing demand for premium and flavored bottled water products.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.