Middle East & Africa Marine Vessel Market Outlook to 2030

Region:Global

Author(s):Abhinav Kumar

Product Code:KROD5075

Region:Global

Author(s):Abhinav Kumar

Product Code:KROD5075

December 2024

93

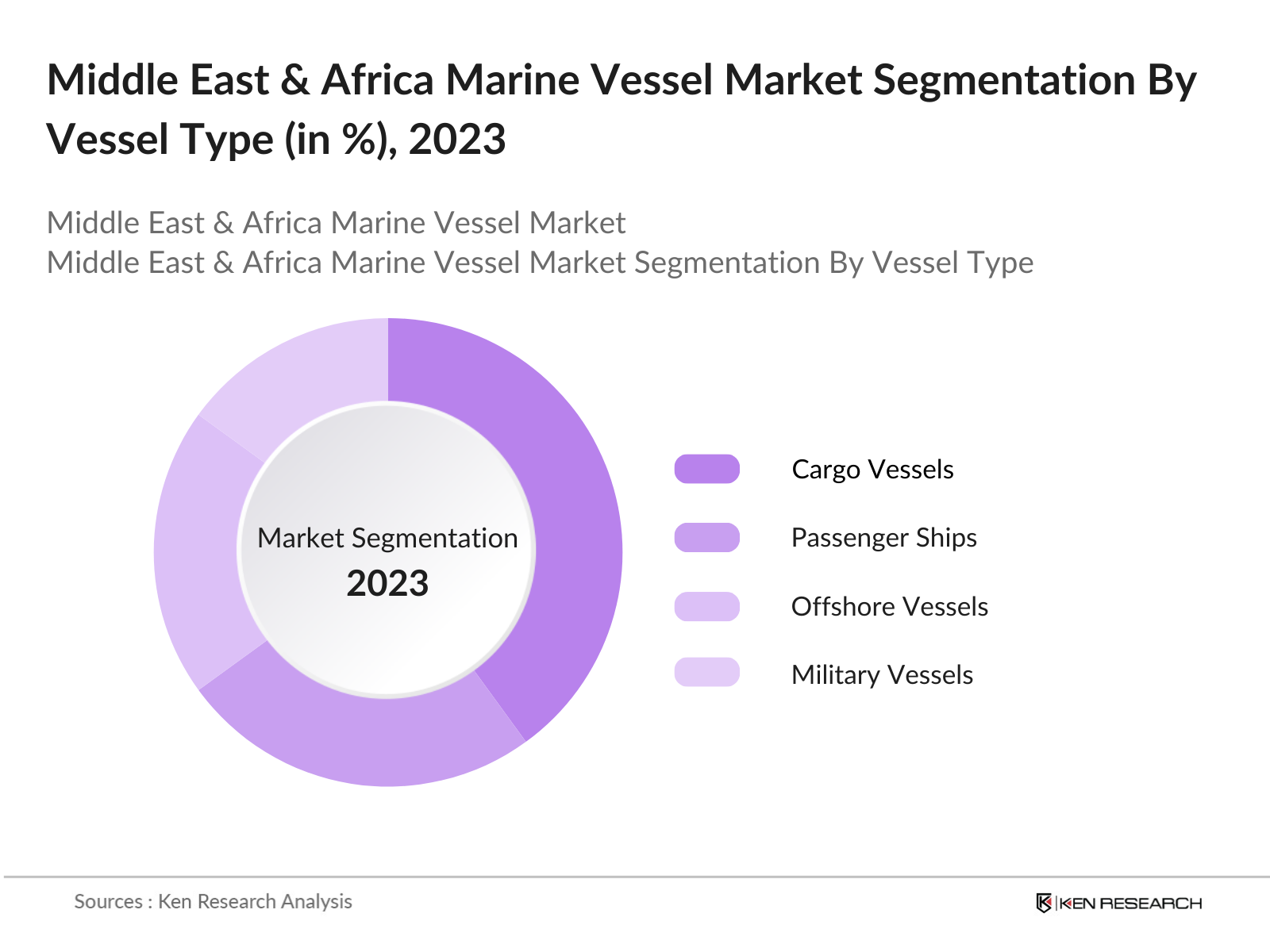

By Vessel Type: The Middle East & Africa Marine Vessel market is segmented by vessel type into cargo vessels, passenger ships, offshore vessels, and military vessels. Recently, cargo vessels have gained a dominant market share due to the increasing international seaborne trade and the heavy reliance of Middle Eastern and African economies on exports of oil, gas, and other natural resources. The expansion of major shipping routes like the Suez Canal and extensive investment in cargo infrastructure across key ports have also contributed to this growth.

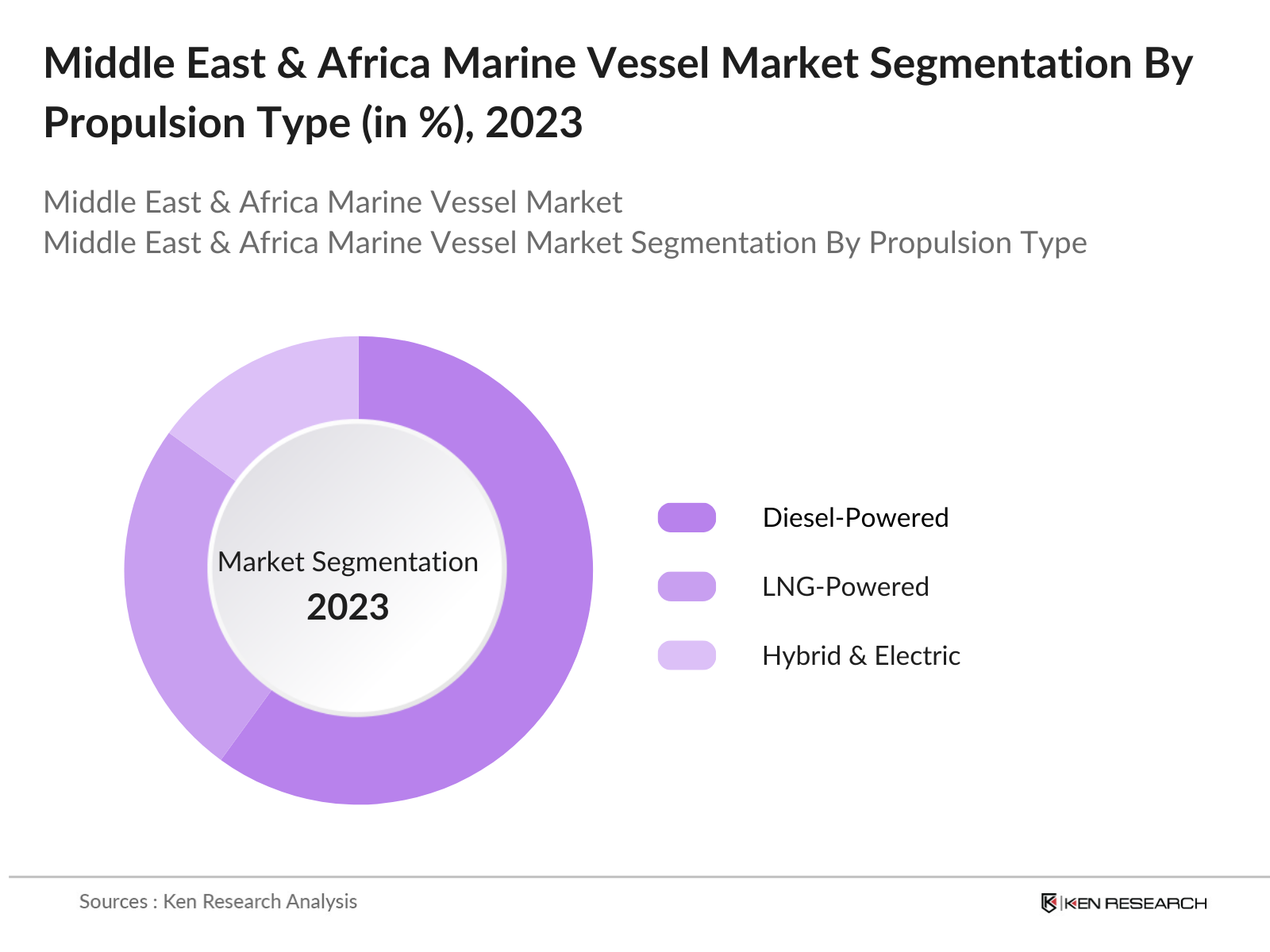

By Propulsion Type: The market is also segmented by propulsion type into diesel-powered vessels, LNG-powered vessels, and hybrid & electric vessels. Diesel-powered vessels dominate the market, holding the largest share, as they remain the preferred choice due to their established technology and widespread availability. However, with growing environmental concerns and stringent emissions regulations, LNG-powered and hybrid vessels are gaining traction, especially in the GCC countries where investments in cleaner marine fuels are increasing.

The Middle East & Africa Marine Vessel market is characterized by the presence of both local and international players. Companies like Hyundai Heavy Industries and Damen Shipyards Group dominate the market, along with local players like Abu Dhabi Ship Building. These firms have a substantial influence due to their innovative vessel designs, shipbuilding capacity, and strong connections with governments and military sectors. The competitive landscape is highly consolidated, with the top five players contributing significantly to the markets total revenue. The market's competitiveness is further heightened by companies investing in green technologies and expanding into autonomous shipping, a growing trend in the region.

|

Company Name |

Establishment Year |

Headquarters |

Shipbuilding Capacity |

Order Backlog |

R&D Spending |

No. of Employees |

Global Presence |

|

Hyundai Heavy Industries |

1972 |

Ulsan, South Korea |

_ |

_ |

_ |

_ |

_ |

|

Damen Shipyards Group |

1927 |

Gorinchem, Netherlands |

_ |

_ |

_ |

_ |

_ |

|

Abu Dhabi Ship Building |

1996 |

Abu Dhabi, UAE |

_ |

_ |

_ |

_ |

_ |

|

Mitsubishi Heavy Industries |

1884 |

Tokyo, Japan |

_ |

_ |

_ |

_ |

_ |

|

Fincantieri S.p.A. |

1959 |

Trieste, Italy |

_ |

_ |

_ |

_ |

_ |

Over the next five years, the Middle East & Africa Marine Vessel market is expected to witness significant growth. This growth will be fueled by increased investments in port infrastructure, advancements in vessel technology, and the shift towards greener, more energy-efficient vessels. The region's strategic importance in global trade routes, coupled with government initiatives promoting maritime development, will further enhance market prospects. Additionally, as environmental regulations tighten, demand for LNG and hybrid-powered vessels is likely to see exponential growth.

|

Vessel Type |

Cargo Vessels Passenger Ships Offshore Vessels Military Vessels |

|

Propulsion Type |

Diesel-Powered LNG-Powered Hybrid & Electric |

|

Application |

Commercial Defense Offshore |

|

Region |

GCC Countries South Africa Nigeria Egypt |

|

End-User |

Shipping Companies Government Authorities |

1.1. Definition and Scope

1.2. Market Taxonomy (Commercial, Defense, Offshore, Cargo)

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increase in Seaborne Trade

3.1.2. Offshore Oil & Gas Exploration

3.1.3. Naval Modernization Programs

3.1.4. Technological Advancements in Vessel Design

3.2. Market Challenges

3.2.1. High Operating and Fuel Costs

3.2.2. Stringent Environmental Regulations

3.2.3. Volatility in Global Trade

3.3. Opportunities

3.3.1. Growth in Maritime Tourism

3.3.2. Technological Innovation in Green Vessels

3.3.3. Investments in Port Infrastructure

3.4. Trends

3.4.1. Shift Toward LNG-Powered Vessels

3.4.2. Adoption of Digitalization & AI in Marine Operations

3.4.3. Rising Demand for Autonomous Vessels

3.5. Government Regulation

3.5.1. IMO 2020 Emission Standards

3.5.2. National Maritime Safety Regulations

3.5.3. Environmental Incentives for Green Ships

3.5.4. Subsidies for Shipbuilding

3.6. SWOT Analysis

3.6.1. Strengths

3.6.2. Weaknesses

3.6.3. Opportunities

3.6.4. Threats

3.7. Stakeholder Ecosystem (Shipbuilders, Owners, Operators)

3.8. Porters Five Forces Analysis

3.8.1. Threat of New Entrants

3.8.2. Bargaining Power of Buyers

3.8.3. Bargaining Power of Suppliers

3.8.4. Threat of Substitutes

3.8.5. Competitive Rivalry

3.9. Competition Ecosystem (Marine Transport, Offshore Shipping)

4.1. By Vessel Type (In Value %)

4.1.1. Cargo Vessels

4.1.2. Passenger Ships

4.1.3. Offshore Vessels

4.1.4. Military Vessels

4.2. By Propulsion Type (In Value %)

4.2.1. Diesel-Powered

4.2.2. LNG-Powered

4.2.3. Hybrid & Electric

4.3. By Application (In Value %)

4.3.1. Commercial

4.3.2. Defense

4.3.3. Offshore

4.4. By Region (In Value %)

4.4.1. GCC Countries

4.4.2. South Africa

4.4.3. Nigeria

4.4.4. Egypt

4.5. By End-User (In Value %)

4.5.1. Shipping Companies

4.5.2. Government Authorities

4.5.3. Offshore Operators

4.5.4. Private Owners

5.1. Detailed Profiles of Major Competitors

5.1.1. Hyundai Heavy Industries

5.1.2. Daewoo Shipbuilding & Marine Engineering

5.1.3. Samsung Heavy Industries

5.1.4. China State Shipbuilding Corporation

5.1.5. Fincantieri S.p.A.

5.1.6. Damen Shipyards Group

5.1.7. Mitsubishi Heavy Industries

5.1.8. Abu Dhabi Ship Building

5.1.9. Oman Drydock Company

5.1.10. Naval Group

5.1.11. Huntington Ingalls Industries

5.1.12. Austal Limited

5.1.13. China Shipbuilding Industry Corporation

5.1.14. Keppel Offshore & Marine

5.1.15. STX Offshore & Shipbuilding

5.2. Cross Comparison Parameters

5.2.1. No. of Employees

5.2.2. Headquarters Location

5.2.3. Inception Year

5.2.4. Revenue

5.2.5. Order Backlog

5.2.6. Shipbuilding Capacity

5.2.7. R&D Spending

5.2.8. Geographic Presence

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Joint Ventures & Partnerships

5.8. Government Grants

6.1. Environmental Standards (IMO, MARPOL)

6.2. Compliance Requirements

6.3. Certification Processes (Classification Societies)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Vessel Type (In Value %)

8.2. By Propulsion Type (In Value %)

8.3. By Application (In Value %)

8.4. By Region (In Value %)

8.5. By End-User (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The research process begins by mapping out the entire ecosystem of the Middle East & Africa Marine Vessel Market. Through extensive desk research and proprietary databases, we identified critical variables influencing market growth, such as trade volume, energy exports, and defense budgets.

We then compiled historical data to assess market penetration and shipbuilding activity. This involved evaluating trends in commercial and defense vessels, port infrastructure investments, and demand for fuel-efficient vessels.

Our market hypotheses were validated through direct consultation with industry experts, including shipbuilding companies, port authorities, and energy sector stakeholders, using computer-assisted telephone interviews (CATIs).

The final research phase involved integrating insights from various manufacturers to verify key statistics on market segments, vessel design, and propulsion trends, ensuring an accurate, validated analysis.

The Middle East & Africa Marine Vessel Market is valued at USD 9 billion. It is driven by increased maritime trade, energy exploration projects, and strategic government investments in shipbuilding.

Key challenges include high operational costs, stringent environmental regulations, and geopolitical uncertainties that can affect trade routes and demand for maritime logistics services.

The market is dominated by Hyundai Heavy Industries, Damen Shipyards Group, Abu Dhabi Ship Building, and Fincantieri, known for their shipbuilding capacities and technological advancements.

Growth is propelled by increasing global trade, demand for oil and gas exports, and investments in green vessel technologies such as LNG-powered ships.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.