Middle East & Africa Smart Highway Market Outlook to 2030

Region:Middle East

Author(s):Yogita Sahu

Product Code:KROD3822

October 2024

85

About the Report

Middle East & Africa Smart Highway Market Overview

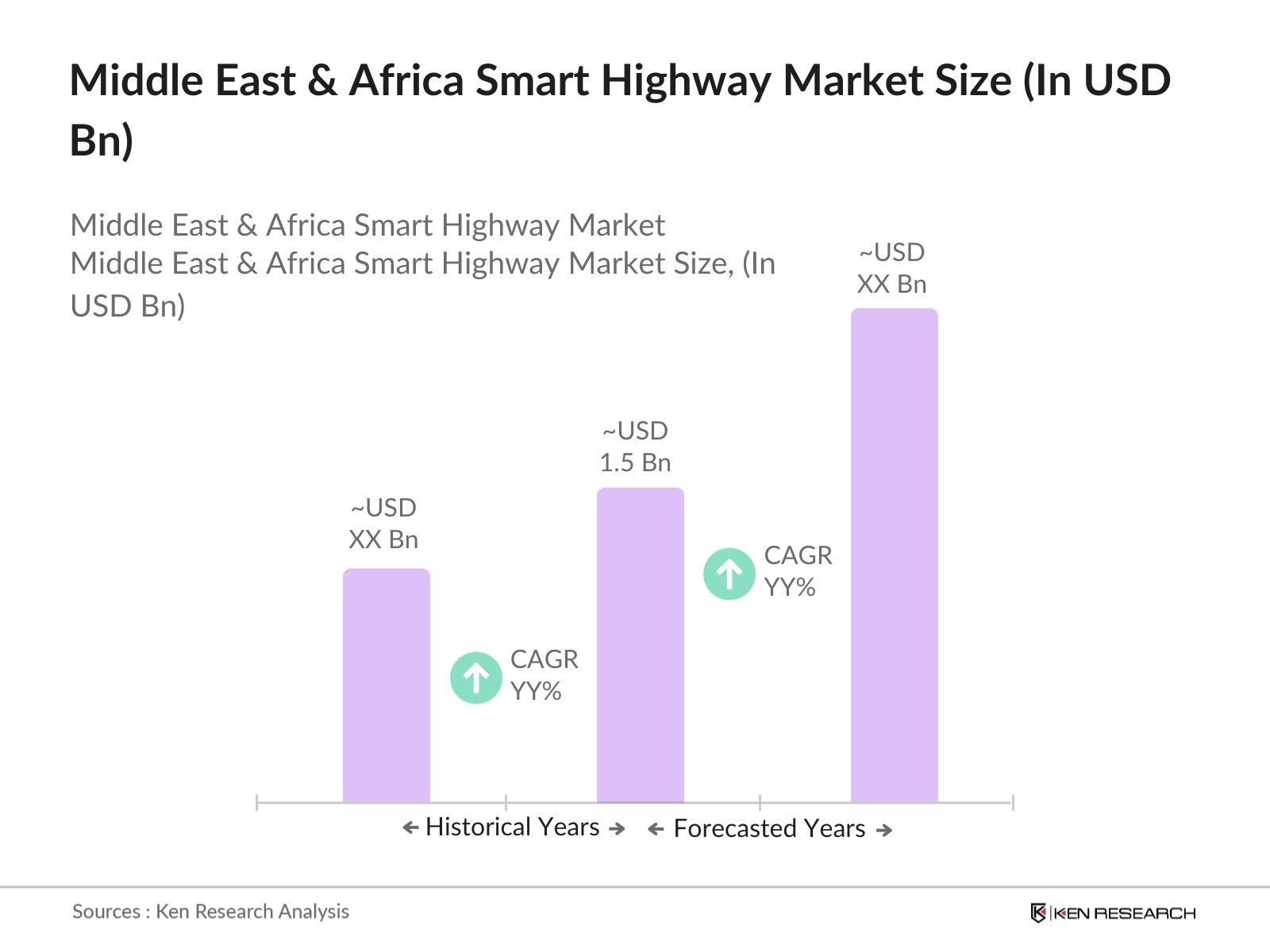

- The Middle East & Africa Smart Highway market is valued at USD 1.5 billion, reflecting a five-year historical analysis. This market is primarily driven by significant government investments in smart infrastructure, particularly within the framework of national smart city projects. The rising adoption of technologies like IoT, artificial intelligence, and connected traffic management systems has boosted the deployment of smart highways across the region.

- The dominant players in the market include countries such as the United Arab Emirates, Saudi Arabia, and South Africa. These regions have established themselves as market leaders due to substantial government support, strategic investments, and ongoing infrastructure projects such as Dubais Smart Dubai 2021 initiative and Saudi Arabia's Vision 2030.

- In line with its Vision 2030, the Saudi government has allocated over $10 billion for infrastructure projects in 2024, with a significant portion aimed at upgrading highways with smart solutions like intelligent traffic lights, automated tolling, and connected vehicle technologies. The government aims to cut travel times and reduce accidents across the nations road network, ensuring more efficient and safer roads by 2030.

Middle East & Africa Smart Highway Market Segmentation

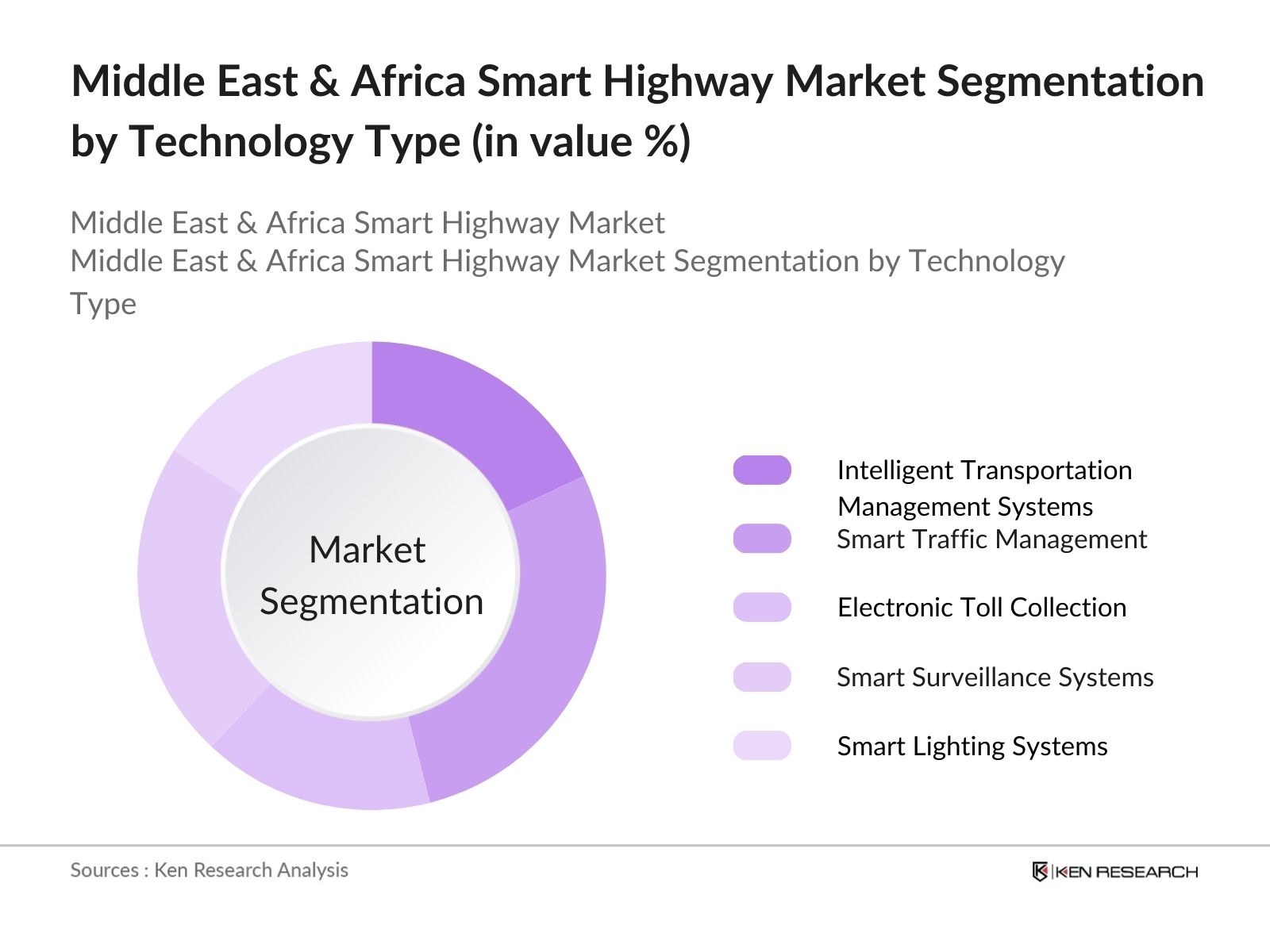

By Technology Type: The market is segmented by technology type into Intelligent Transportation Management Systems, Smart Traffic Management, Electronic Toll Collection, Smart Surveillance Systems, and Smart Lighting Systems. Smart Traffic Management has a dominant market share, as it is widely used for real-time traffic monitoring and congestion management. This technology integrates with advanced sensor systems and AI to improve the efficiency of vehicle flow on highways, particularly in high-density urban areas where traffic congestion is a major challenge.

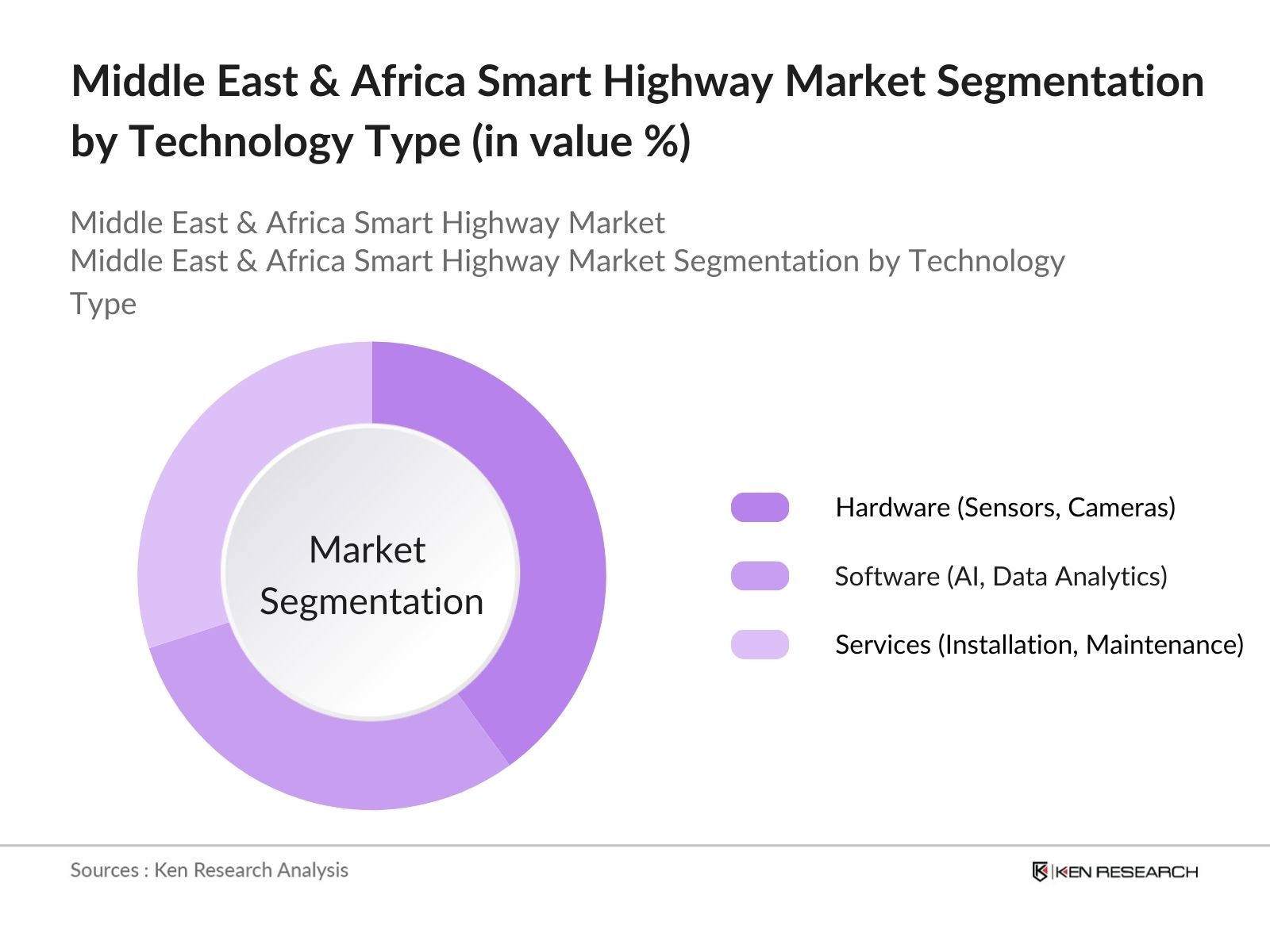

By Component Type: The market is also segmented by component type into Hardware, Software, and Services. Hardware components hold the largest share of the market due to the widespread deployment of physical infrastructure such as sensors, cameras, and traffic signals. Hardware systems are the backbone of smart highways, enabling data collection and real-time analytics. Countries like Saudi Arabia and the UAE have invested heavily in hardware infrastructure, particularly in smart surveillance and traffic management systems, to monitor and manage highway usage efficiently.

Middle East & Africa Smart Highway Market Competitive Landscape

The market is characterized by the presence of several global and regional players. The market is competitive, with companies focusing on strategic collaborations, technological advancements, and infrastructure projects to maintain their positions. The leading players in the market leverage their technological capabilities and market reach to secure contracts, particularly in countries like Saudi Arabia and the UAE.

|

Company Name |

Establishment Year |

Headquarters |

Technology Focus |

Major Project Involvement |

Regional Presence |

Market Revenue |

R&D Investments |

Partnerships |

|

Siemens AG |

1847 |

Germany |

||||||

|

Cisco Systems, Inc. |

1984 |

USA |

||||||

|

Huawei Technologies Co. |

1987 |

China |

||||||

|

Schneider Electric |

1836 |

France |

||||||

|

Kapsch TrafficCom AG |

1892 |

Austria |

Middle East & Africa Smart Highway Market

Market Growth Drivers

- Infrastructure Investment Expansion: Middle Eastern and African nations are investing significantly in smart highway infrastructure to enhance road safety and reduce traffic congestion. In 2024, the African Development Bank allocated $1.3 billion for infrastructure projects across several African countries, including smart highway systems. In the Middle East, the UAE government announced a $2.5 billion investment in smart infrastructure as part of its 2024 Vision, with the majority allocated to enhancing the existing highway systems with smart technology like AI and IoT-based traffic management systems.

- Rising Vehicle Ownership and Transport Demand: The number of registered vehicles in Saudi Arabia reached 10 million by the start of 2024, increasing the demand for advanced road management systems. Similarly, in South Africa, vehicle registration is expected to surpass 13 million by the end of 2024, intensifying the pressure on governments to implement smart highway solutions that can accommodate the growing traffic volumes and improve road safety standards.

- Government Focus on Reducing Traffic Fatalities: Traffic accidents in African countries have been a growing concern, with more than 180,000 road fatalities recorded in 2023. Governments are focusing on reducing this number by deploying intelligent traffic systems (ITS) on highways. In 2024, South Africa allocated over $800 million for upgrading highways with ITS to ensure better traffic flow and reduce accidents by 25,000 cases annually, while Saudi Arabias Vision 2030 targets a reduction in road fatalities by 50,000 annually by implementing smart road technology.

Market Challenges

- Lack of Skilled Workforce: The Middle East and Africa region faces a shortage of skilled labor to design, implement, and maintain smart highway systems. In 2024, less than 20,000 engineers across the region have the necessary qualifications to work on ITS projects, with demand for skilled professionals exceeding 50,000. This talent gap has slowed down the pace of smart highway adoption in countries like Egypt and South Africa, where training programs remain underfunded.

- Political and Economic Instability: Political instability in countries like Nigeria, Sudan, and Ethiopia has made it difficult to maintain consistent infrastructure projects. In 2024, $3 billion in funding for smart highway projects in North Africa was delayed due to ongoing conflicts and political unrest. The fluctuating economies in parts of the region, with inflation rates reaching double digits in 2024, further complicate long-term planning and investment in infrastructure projects.

Middle East & Africa Smart Highway Market Future Outlook

Over the next five years, the Middle East & Africa Smart Highway industry is expected to witness robust growth, driven by increasing government support for smart infrastructure and technological advancements in AI, IoT, and data analytics. Governments in the region are prioritizing the development of smart cities, with smart highways being a key element of this vision.

Future Market Opportunities

- AI-Driven Predictive Traffic Management Systems: Over the next five years, predictive traffic management systems powered by AI will become standard on smart highways in the Middle East and Africa. By 2028, it is expected that more than 1,500 kilometers of highways in the GCC will be equipped with AI traffic analytics tools, which will enable real-time traffic management, accident prediction, and congestion control, reducing road fatalities and traffic jams across the region.

- Expansion of Autonomous Vehicle Lanes: By 2028, countries like Saudi Arabia and the UAE will implement dedicated lanes for autonomous vehicles on smart highways. As of 2024, Saudi Arabia has already allocated toward autonomous vehicle infrastructure, with plans to expand this network by 50% over the next five years. This will enable faster and safer transportation, with an estimated 300 kilometers of such lanes expected to be operational in the UAE by 2028.

Scope of the Report

|

By Technology Type |

Intelligent Transportation Management Systems |

|

Smart Traffic Management |

|

|

Electronic Toll Collection |

|

|

Smart Surveillance Systems |

|

|

Smart Lighting Systems |

|

|

By Service Type |

Managed Services |

|

Maintenance and Operation |

|

|

Consulting Services |

|

|

By Deployment Type |

On-Premises |

|

Cloud-Based Solutions |

|

|

By Component Type |

Hardware (Sensors, Cameras, Traffic Signals) |

|

Software (AI, Data Analytics, Cloud Management) |

|

|

Services (Installation, Integration, Maintenance) |

|

|

By Region |

North |

|

South |

|

|

East |

|

|

West |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Government and Regulatory Bodies (e.g., Dubai Roads and Transport Authority, Saudi Ministry of Transport)

Highway Construction Companies

Telecommunications Providers

IoT and AI Solution Providers

Investments and Venture Capitalist Firms

Electric Vehicle Charging Infrastructure Providers

Transportation and Logistics Firms

Companies

Players Mentioned in the Report:

Siemens AG

Huawei Technologies Co. Ltd.

Cisco Systems, Inc.

IBM Corporation

Schneider Electric

Kapsch TrafficCom AG

Indra Sistemas S.A.

Toshiba Corporation

Alstom SA

ABB Ltd.

Johnson Controls International plc

Honeywell International Inc.

Thales Group

Hitachi Ltd.

EFKON AG

Table of Contents

1. Middle East & Africa Smart Highway Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Middle East & Africa Smart Highway Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Middle East & Africa Smart Highway Market Analysis

3.1. Growth Drivers

3.1.1. Infrastructure Modernization (Deployment of IoT-enabled traffic management systems)

3.1.2. Government Smart City Initiatives (Highway technology integration with national smart city projects)

3.1.3. Public Safety Concerns (Implementation of accident prevention systems)

3.1.4. Energy Efficiency Demands (Adoption of smart lighting and renewable-powered highways)

3.2. Market Challenges

3.2.1. High Capital Expenditure (Cost of technology deployment and integration)

3.2.2. Technological Disparities (Variability in regional technological capabilities)

3.2.3. Data Privacy and Cybersecurity Risks (Increasing vulnerability with IoT and AI systems)

3.3. Opportunities

3.3.1. Integration with 5G Networks (Enhanced vehicle-to-infrastructure communication)

3.3.2. AI-driven Traffic Management (Real-time decision-making through AI)

3.3.3. Partnerships with Automotive Sector (Connected vehicles for smart highways)

3.4. Trends

3.4.1. Increased Adoption of Electric Vehicle (EV) Charging Infrastructure

3.4.2. Deployment of Smart Surveillance Systems (Monitoring and enforcement of road safety)

3.4.3. Use of Advanced Sensor Technologies (Dynamic road maintenance and monitoring)

3.5. Government Regulation

3.5.1. Smart Transportation Policy Frameworks

3.5.2. Public-Private Partnerships (PPP) (Financing smart highway projects)

3.5.3. National Data Protection Regulations (Impact on real-time data collection)

3.5.4. Carbon Emission Standards (Influence on sustainable highway development)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Involvement of technology providers, regulators, and construction firms)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Middle East & Africa Smart Highway Market Segmentation

4.1. By Technology Type (In Value %)

4.1.1. Intelligent Transportation Management Systems

4.1.2. Smart Traffic Management

4.1.3. Electronic Toll Collection

4.1.4. Smart Surveillance Systems

4.1.5. Smart Lighting Systems

4.2. By Service Type (In Value %)

4.2.1. Managed Services

4.2.2. Maintenance and Operation

4.2.3. Consulting Services

4.3. By Deployment Type (In Value %)

4.3.1. On-Premises

4.3.2. Cloud-Based Solutions

4.4. By Component Type (In Value %)

4.4.1. Hardware (Sensors, Cameras, Traffic Signals)

4.4.2. Software (AI, Data Analytics, Cloud Management)

4.4.3. Services (Installation, Integration, Maintenance)

4.5. By Region (In Value %)

4.5.1. Israel

4.5.2. United Arab Emirates

4.5.3. Jordan

4.5.4. Morocco

4.5.5. South Africa

4.5.6. Rest of MEA

5. Middle East & Africa Smart Highway Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Siemens AG

5.1.2. Huawei Technologies Co. Ltd.

5.1.3. Cisco Systems, Inc.

5.1.4. IBM Corporation

5.1.5. Schneider Electric

5.1.6. Kapsch TrafficCom AG

5.1.7. Indra Sistemas S.A.

5.1.8. Toshiba Corporation

5.1.9. Alstom SA

5.1.10. ABB Ltd.

5.1.11. Johnson Controls International plc

5.1.12. Honeywell International Inc.

5.1.13. Thales Group

5.1.14. Hitachi Ltd.

5.1.15. EFKON AG

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Technology Partnerships, Revenue, Smart Highway Projects, Regional Presence, Investments in Smart Highway R&D, Smart Infrastructure Patents)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Middle East & Africa Smart Highway Market Regulatory Framework

6.1. Regional Transportation Policies

6.2. Infrastructure Compliance Requirements

6.3. Certification Processes

6.4. Funding Schemes for Smart Highway Projects

7. Middle East & Africa Smart Highway Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Middle East & Africa Smart Highway Future Market Segmentation

8.1. By Technology Type (In Value %)

8.2. By Service Type (In Value %)

8.3. By Deployment Type (In Value %)

8.4. By Component Type (In Value %)

8.5. By Region (In Value %)

9. Middle East & Africa Smart Highway Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step involved mapping the ecosystem of the Middle East & Africa Smart Highway Market. This step was supported by desk research utilizing a combination of secondary data sources such as government reports, industry journals, and proprietary databases to identify the major variables impacting market growth.

Step 2: Market Analysis and Construction

Historical data on smart highway deployments and technological penetration were analyzed, considering government investments and infrastructure projects across the region. This phase also involved assessing data from IoT and AI solution providers.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, including those from infrastructure development companies and government regulatory bodies, were consulted through interviews. Their insights were vital in validating the data and refining the market growth hypotheses.

Step 4: Research Synthesis and Final Output

After collecting and analyzing the data, the final step included engaging with smart highway technology providers to acquire more detailed insights into the deployment of smart traffic and lighting systems. This input further refined the bottom-up estimates, ensuring accuracy in the final market analysis.

Frequently Asked Questions

01. How big is the Middle East & Africa Smart Highway Market?

The Middle East & Africa Smart Highway market is valued at USD 1.5 billion, driven by increasing government investments in smart infrastructure and a growing need for real-time traffic management systems.

02. What are the challenges in the Middle East & Africa Smart Highway Market?

Challenges in the Middle East & Africa Smart Highway market include high capital expenditure, technological disparities across different countries, and data privacy concerns, especially with the increasing use of AI and IoT-based traffic management systems.

03. Who are the major players in the Middle East & Africa Smart Highway Market?

Key players in the Middle East & Africa Smart Highway market include Siemens AG, Huawei Technologies Co. Ltd., Cisco Systems, Schneider Electric, and Kapsch TrafficCom AG. These companies dominate due to their advanced technological capabilities and involvement in key smart city projects.

04. What are the growth drivers of the Middle East & Africa Smart Highway Market?

The growth drivers in the Middle East & Africa Smart Highway market include government initiatives to develop smart cities, increased traffic congestion necessitating real-time traffic solutions, and the adoption of AI-driven traffic management systems.

05. What are the future trends in the Middle East & Africa Smart Highway Market?

Future trends in the Middle East & Africa Smart Highway market include the integration of renewable energy sources into highway systems, the expansion of electric vehicle charging infrastructure, and the development of autonomous vehicle-friendly highways.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.