North America Aerospace Plastics Market Outlook to 2030

Region:North America

Author(s):Paribhasha Tiwari

Product Code:KROD3661

October 2024

90

About the Report

North America Aerospace Plastics Market Overview

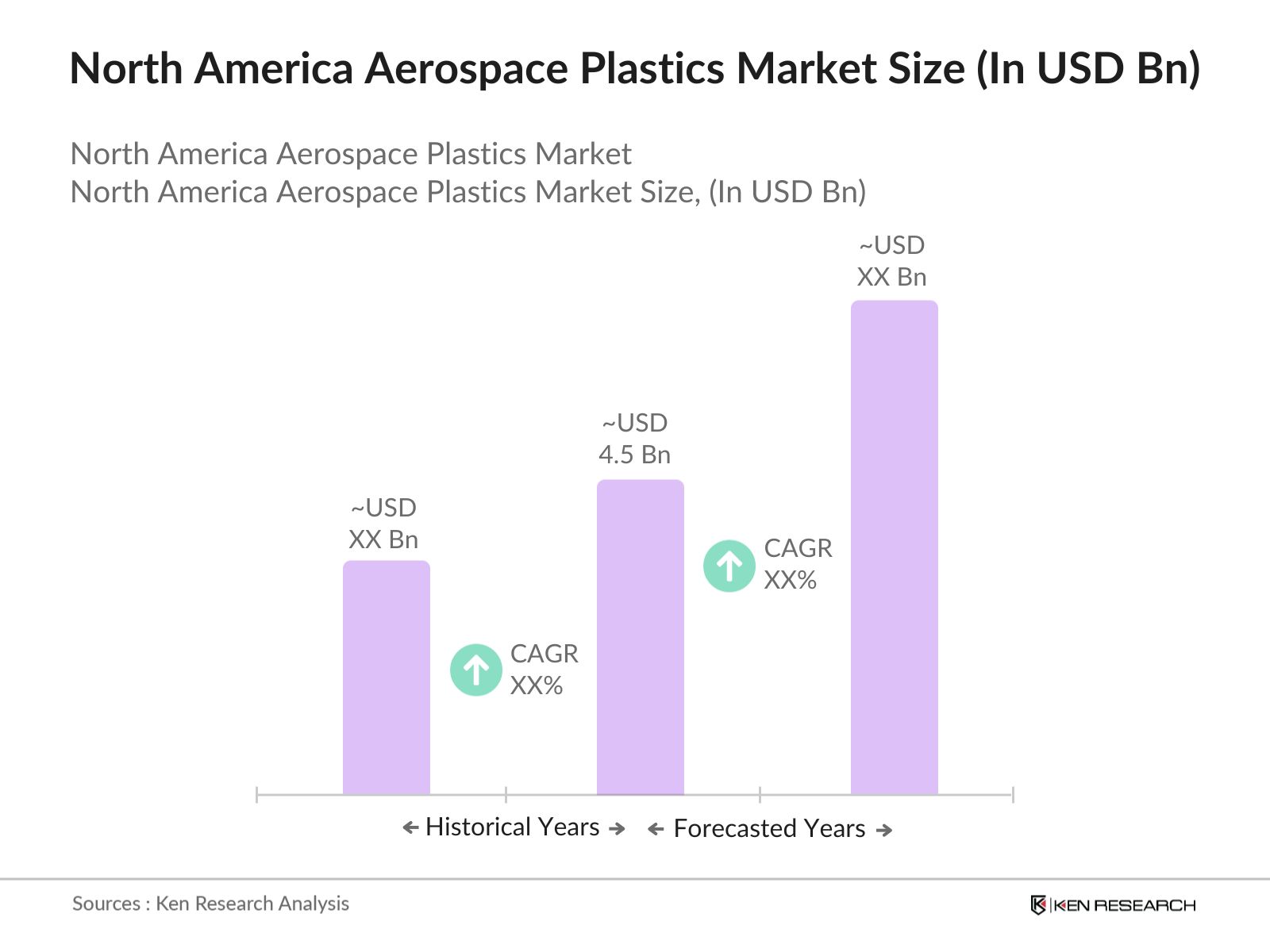

- The North America aerospace plastics market is valued at 5 billion. This market size is primarily driven by the increasing demand for lightweight, durable, and fuel-efficient materials in both commercial and military aircraft manufacturing. Aerospace plastics, including high-performance materials like PEEK and polycarbonate, help reduce the overall weight of aircraft, contributing to fuel efficiency and reducing CO2 emissions. The push for sustainability, alongside stringent government regulations for weight reduction and safety standards, is driving the adoption of these materials across the aerospace industry.

- The United States dominates the North America aerospace plastics market due to its significant aerospace manufacturing base, including major players like Boeing and Lockheed Martin. The country’s robust defense sector and the growing number of commercial airlines further boost demand for aerospace plastics. Canada and Mexico are also key contributors, with Mexico becoming a low-cost aerospace manufacturing hub, thanks to its proximity to the U.S. market and the availability of skilled labor.

- In 2023, the U.S. Federal Aviation Administration (allocated over USD 100 million to support research and initiatives focused on reducing noise and emissions in the aerospace industry. As part of broader environmental goals, this funding encourages the development of lightweight, sustainable materials like aerospace plastics, which play a critical role in improving fuel efficiency and reducing the carbon footprint of aircraft. The initiative aligns with efforts to achieve net-zero emissions in the aerospace sector by 2050.

North America Aerospace Plastics Market Segmentation

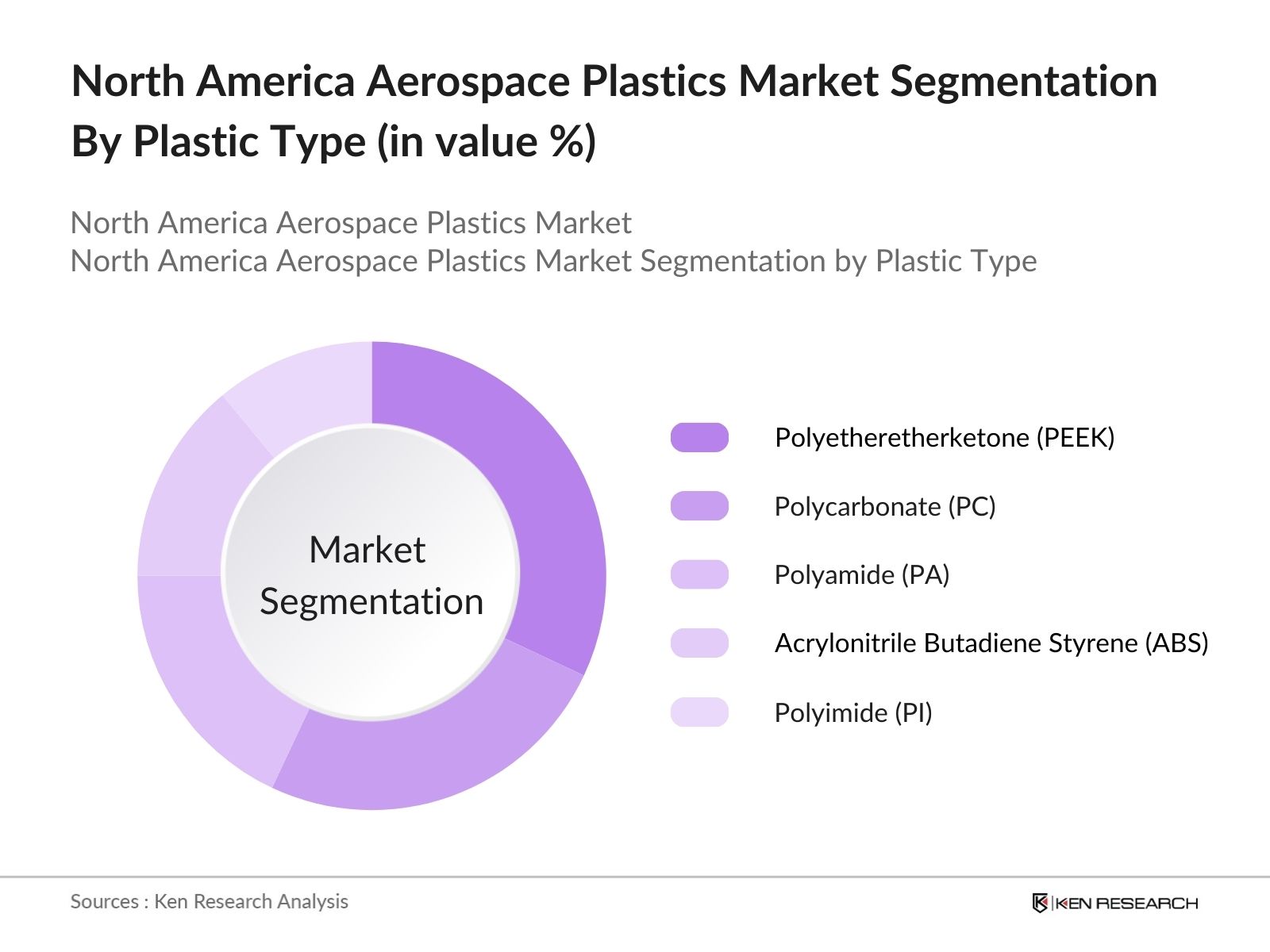

By Plastic Type: The North America aerospace plastics market is segmented by plastic type into polyetheretherketone (PEEK), polycarbonate (PC), polyamide (PA), acrylonitrile butadiene styrene (ABS), and polyimide (PI). Among these, polyetheretherketone (PEEK) has emerged as a dominant player. This is due to its superior strength-to-weight ratio, excellent thermal stability, and chemical resistance. PEEK is particularly favored for use in airframe components and engine parts, where both lightweight and high-performance properties are critical. PEEK's ability to withstand extreme conditions without compromising safety has made it a preferred choice for high-stress applications in both commercial and military aviation sectors.

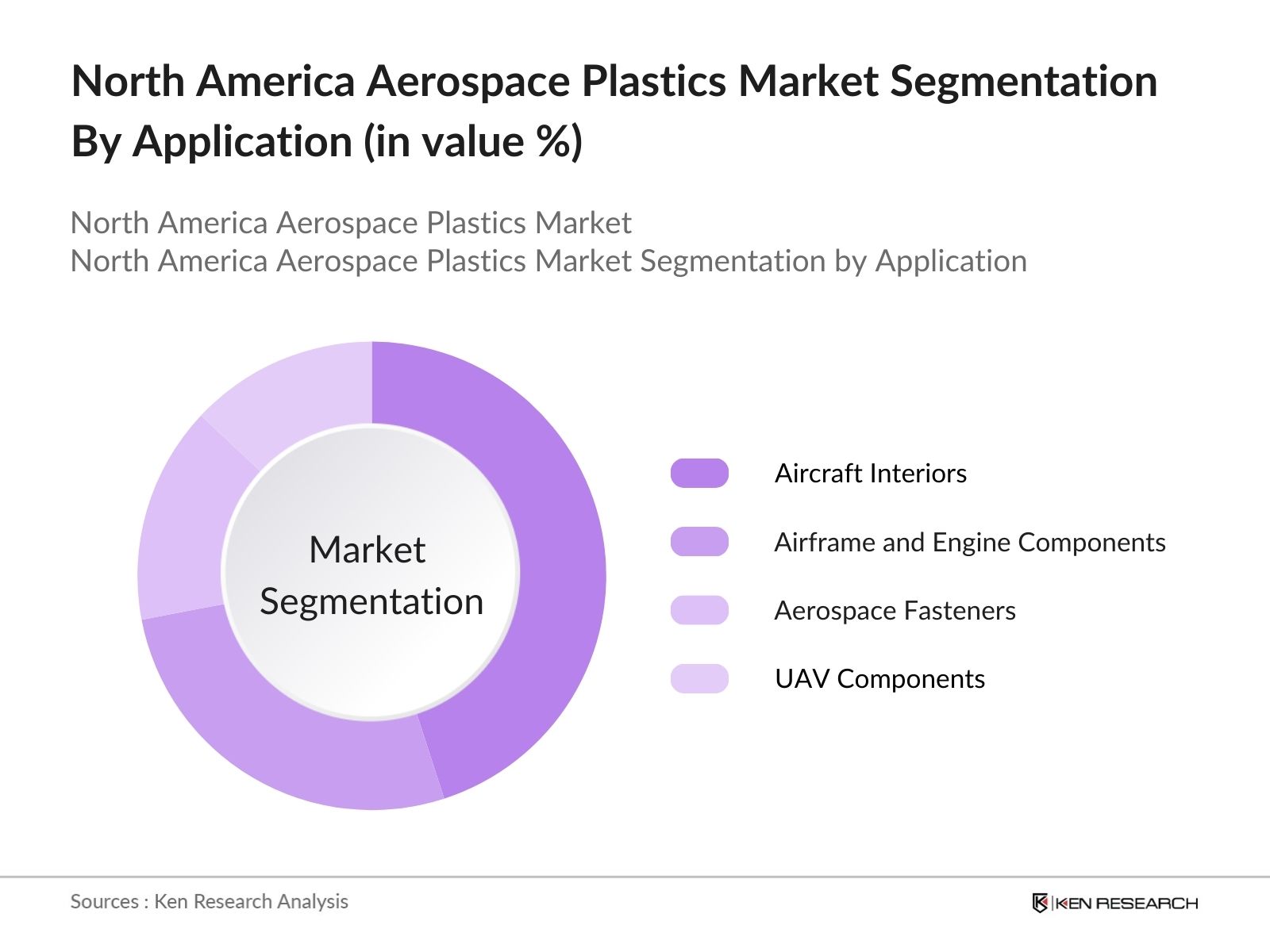

By Application: The aerospace plastics market is segmented by application into aircraft interiors, airframe and engine components, aerospace fasteners, and UAV components. Aircraft interiors dominate this segment due to the increasing focus on passenger comfort and cabin aesthetics. Plastics are widely used for cabin panels, seating, overhead bins, and other interior components because they offer the advantages of being lightweight, durable, and cost-effective compared to traditional materials like metal. In addition, aircraft manufacturers are increasingly opting for plastics to meet strict fire safety and impact resistance regulations, which adds to the dominance of this segment.

North America Aerospace Plastics Market Competitive Landscape

The North America aerospace plastics market is highly competitive, with both global and regional players. The market is characterized by innovation, with companies focusing on developing advanced composite materials and improving their production processes to meet the stringent requirements of the aerospace industry. Key players include both raw material suppliers and manufacturers of aerospace components.

|

Company Name |

Establishment Year |

Headquarters |

Plastic Type Expertise |

R&D Investment |

Sustainability Initiatives |

Global Presence |

Industry Certifications |

Revenue Growth |

|

Solvay S.A. |

1863 |

Brussels, Belgium |

||||||

|

Hexcel Corporation |

1948 |

Stamford, USA |

||||||

|

BASF SE |

1865 |

Ludwigshafen, Germany |

||||||

|

SABIC |

1976 |

Riyadh, Saudi Arabia |

||||||

|

Victrex plc |

1993 |

Lancashire, UK |

North America Aerospace Plastics Market Analysis

Growth Drivers

-

Increasing Aircraft Production (Commercial Aircraft, Military Aircraft, UAVs): The rising demand for new aircraft is a key plastics. According to the International Air Transport Association (IATA), there were approximately 25,000 commercial aircraft in operation in 2023, and global passenger traffic has returned to pre-pandemic levels, driving a need for fleet expansion. The United States is one of the largest producers of military aircraft, with over 1,500 fighter aircraft active in its fleet. The growing UAV market, supported by military applications and commercial sectors, is further fueling the demand for lightweight materials like aerospace plastics.

-

Fuel Efficiency and Weight Reduction Requirements (Composite Material Integration): Fuel efficiency is a top priority for the aviation industry, with aviation fuel costs constituting a significant expenses. Modern aircraft, such as the Boeing 787 and Airbus A350, incorporate up to 50% composite materials, reducing their weight by 20%. This weight reduction contributes to saving millions of gallons of fuel annually. With jet fuel prices exceeding $3 per gallon in 2024, airlines are increasingly adopting lightweight plastics and composites to enhance fuel efficiency, which directly reduces operational costs. Aerospace plastics play a critical role in achieving these efficiency goals.

-

Expansion of Aerospace Manufacturing Hubs (Regional Manufacturing Focus): North America is a major hub for ufacturing, with Boeing and Lockheed Martin spearheading commercial and defense aircraft production. In 2022, the U.S. aerospace sector employed over 500,000 workers, with aerospace exports exceeding $130 billion. Aerospace clusters in Washington, Texas, and Alabama are expanding, driven by government investments and favorable manufacturing policies. This regional manufacturing focus is creating substantial opportunities for aerospace plastics manufacturers, as new production lines for both civil and military aircraft require high-performance materials that meet stringent safety and durability standards.

Market Challenges

- High Cost of Advanced Plastics: Advanced aerospace-grade plastics, such as PEEK and polyimides, come at a higher cost compared to conventional materials like aluminum or steel. These materials offer superior performance in terms of weight reduction, thermal stability, and chemical resistance, but the cost can be a barrier for widespread adoption. For instance, polyether ether ketone (PEEK) can cost up to $1,000 per kilogram, compared to aluminum at approximately $2 per kilogram. The price disparity is a significant challenge, especially for cost-sensitive commercial airlines looking to optimize their fleets without incurring excessive material costs.

- Stringent Regulatory Standards (FAA, EASA): Aerospace plastics must comply with stringent safety and performance regulations set by bodies like the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA). These regulations cover everything from flame retardancy to mechanical strength and material behavior in extreme temperatures. The cost of compliance and rigorous testing processes can delay the introduction of new materials. For example, the FAA requires that aircraft interior materials must meet specific flammability requirements, which adds complexity and costs to the production process of aerospace-grade plastics.

North America Aerospace Plastics Market Future Outlook

The North America aerospace plastics market is expected to experience robust growth over the next five years. This growth is driven by increasing demand for lightweight and fuel-efficient aircraft, coupled with technological advancements in composite materials. Governments are also pushing for stricter environmental regulations, which is accelerating the adoption of recyclable and bio-based plastics. Furthermore, the growth of the commercial aviation sector, coupled with advancements in UAV technology, will continue to drive demand for aerospace plastics in the region.

Market Opportunities

- Increasing Demand for Lightweight UAVs: The demand for lightweight unmanned aerial vehicles (UAVs) is expanding rapidly in both commercial and military applications. In 2022, the U.S. Department of Defense allocated over $7 billion for UAV procurement. Lightweight aerospace plastics are critical for developing more efficient, longer-endurance drones, particularly for surveillance and reconnaissance missions. Additionally, the Federal Aviation Administration (FAA) registered over 800,000 commercial UAVs in the U.S. by 2023, further driving demand for lightweight and durable materials that can reduce UAV fuel consumption and improve operational range.

- Innovation in Thermoplastics and Thermoset Resins (Material Innovations): Advances in material science are opening new avenues for thermoplastics and thermoset resins in aerospace applications. High-performance thermoplastics, such as polyimides and polyamides, offer better heat resistance and mechanical properties, making them suitable for high-stress environments like engine components. In 2023, material innovations led to the development of recyclable thermoset composites, which retain the durability of traditional thermosets but allow for easier disposal and recycling, addressing environmental concerns. This innovation is particularly relevant as the aviation industry seeks to reduce waste and improve the sustainability of its operations.

Scope of the Report

|

Segment |

Sub-Segment |

|

By Plastic Type |

Polyetheretherketone (PEEK) Polycarbonate (PC) Polyamide (PA) Acrylonitrile Butadiene Styrene (ABS) Polyimide (PI) |

|

By Application |

Aircraft Interiors Airframe and Engine Components Aerospace Fasteners UAV Components |

|

By End-User |

Commercial Aviation Military Aviation General Aviation Unmanned Aerial Vehicles (UAVs) |

|

By Manufacturing Process |

Injection Molding Thermoforming Compression Molding Additive Manufacturing |

|

By Region |

U.S. Canada |

Products

Key Target Audience

Aerospace Manufacturers (Boeing, Airbus, Lockheed Martin)

Aerospace Plastics Suppliers (Victrex, Solvay, BASF)

Aircraft Interior Designers and Suppliers

Defense Contractors (Northrop Grumman, Raytheon)

Aerospace Component Manufacturers

Environmental and Sustainability Agencies

Government and Regulatory Bodies (FAA, EASA)

Investors and Venture Capitalist Firms

Companies

Solvay S.A.

Hexcel Corporation

BASF SE

SABIC

Victrex plc

Evonik Industries AG

Arkema S.A.

DuPont de Nemours, Inc.

Mitsubishi Chemical Holdings Corporation

Teijin Limited

Ensinger GmbH

Quadrant Group

Röchling Group

Saint-Gobain Performance Plastics

PlastiComp, Inc.

Table of Contents

1. North America Aerospace Plastics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Aerospace Plastics Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Aerospace Plastics Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Aircraft Production (Commercial Aircraft, Military Aircraft, UAVs)

3.1.2. Fuel Efficiency and Weight Reduction Requirements (Composite Material Integration)

3.1.3. Expansion of Aerospace Manufacturing Hubs (Regional Manufacturing Focus)

3.1.4. Shift Towards Sustainable and Recyclable Plastics (Bio-based Materials)

3.2. Market Challenges

3.2.1. High Cost of Advanced Plastics

3.2.2. Stringent Regulatory Standards (FAA, EASA)

3.2.3. Technological Complexities in Composite Processing

3.3. Opportunities

3.3.1. Increasing Demand for Lightweight UAVs

3.3.2. Innovation in Thermoplastics and Thermoset Resins (Material Innovations)

3.3.3. Expansion of Aftermarket Services (Aerospace Plastics Repair and Maintenance)

3.4. Trends

3.4.1. Integration of 3D Printing in Aerospace Plastics Manufacturing (Additive Manufacturing)

3.4.2. Advancements in Carbon Fiber-Reinforced Plastics (CFRP Adoption)

3.4.3. Use of Nanomaterials for Enhanced Strength (Nanocomposite Innovations)

3.5. Government Regulation

3.5.1. FAA Regulations for Plastic Materials in Aircraft Interiors

3.5.2. Environmental Compliance for Aerospace Plastics Recycling

3.5.3. Restrictions on Harmful Chemicals (REACH, RoHS Compliance)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces

3.9. Competition Ecosystem

4. North America Aerospace Plastics Market Segmentation

4.1. By Plastic Type (In Value %)

4.1.1. Polyetheretherketone (PEEK)

4.1.2. Polycarbonate (PC)

4.1.3. Polyamide (PA)

4.1.4. Acrylonitrile Butadiene Styrene (ABS)

4.1.5. Polyimide (PI)

4.2. By Application (In Value %)

4.2.1. Aircraft Interiors (Cabin Components, Overhead Bins, Seating)

4.2.2. Airframe and Engine Components

4.2.3. Aerospace Fasteners

4.2.4. UAV Components

4.3. By End-User (In Value %)

4.3.1. Commercial Aviation

4.3.2. Military Aviation

4.3.3. General Aviation

4.3.4. Unmanned Aerial Vehicles (UAVs)

4.4. By Manufacturing Process (In Value %)

4.4.1. Injection Molding

4.4.2. Thermoforming

4.4.3. Compression Molding

4.4.4. Additive Manufacturing

4.5. By Region (In Value %)

4.5.1. U.S.

4.5.2. Canada

5. North America Aerospace Plastics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Solvay S.A.

5.1.2. Hexcel Corporation

5.1.3. BASF SE

5.1.4. SABIC

5.1.5. Victrex plc

5.1.6. Evonik Industries AG

5.1.7. Arkema S.A.

5.1.8. DuPont de Nemours, Inc.

5.1.9. Mitsubishi Chemical Holdings Corporation

5.1.10. Teijin Limited

5.1.11. Ensinger GmbH

5.1.12. Quadrant Group

5.1.13. Röchling Group

5.1.14. Saint-Gobain Performance Plastics

5.1.15. PlastiComp, Inc.

5.2. Cross Comparison Parameters (Plastic Type Expertise, R&D Investment, Sustainability Initiatives, Global Presence, Industry Certification, Revenue Growth, Product Portfolio, Customer Base)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Aerospace Plastics Market Regulatory Framework

6.1. FAA Material Compliance Standards

6.2. EASA Certification for Aerospace Plastics

6.3. Environmental Standards (REACH, RoHS)

6.4. Fire Safety Standards for Aircraft Interiors

7. North America Aerospace Plastics Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Aerospace Plastics Future Market Segmentation

8.1. By Plastic Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User (In Value %)

8.4. By Manufacturing Process (In Value %)

8.5. By Region (In Value %)

9. North America Aerospace Plastics Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research begins by constructing an ecosystem map of the North America aerospace plastics market, identifying key stakeholders, including manufacturers, suppliers, and regulatory bodies. This phase involves extensive desk research using both secondary sources and proprietary databases to map out the core variables affecting the market, such as material innovation, regulatory frameworks, and sustainability initiatives.

Step 2: Market Analysis and Construction

In this step, historical data related to aerospace plastic consumption, demand trends, and supply chain dynamics are analyzed. The market analysis also includes a thorough review of advancements in manufacturing processes like 3D printing and additive manufacturing, as well as evaluating the influence of government regulations on market growth.

Step 3: Hypothesis Validation and Expert Consultation

Key industry experts from aerospace manufacturing companies, material suppliers, and regulatory bodies are consulted to validate market hypotheses through structured interviews and surveys. This expert insight helps to refine market estimates and forecast trends based on real-time industry feedback.

Step 4: Research Synthesis and Final Output

The final phase consolidates the data collected from various sources into a cohesive market report, focusing on market size, growth drivers, and competitive analysis. A bottom-up approach is employed to ensure the accuracy of revenue projections and market segmentation.

Frequently Asked Questions

01. How big is the North America Aerospace Plastics Market?

The North America aerospace plastics market is valued at USD 4.5 billion, driven by increased demand for lightweight materials in aircraft production and growing government regulations for fuel efficiency.

02. What are the challenges in the North America Aerospace Plastics Market?

Key challenges include the high cost of advanced materials, stringent regulatory standards for safety and performance, and the technological complexities of integrating composite materials into aircraft structures.

03. Who are the major players in the North America Aerospace Plastics Market?

Major players include Solvay S.A., Hexcel Corporation, BASF SE, SABIC, and Victrex plc, who dominate due to their expertise in high-performance plastics and established relationships with aerospace manufacturers.

04. What are the growth drivers of the North America Aerospace Plastics Market?

The market is propelled by the need for lightweight materials that improve fuel efficiency and reduce carbon emissions, as well as advancements in composite material technologies like PEEK and CFRP.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.