North America Aircraft Turn Coordinator Market Outlook to 2030

Region:Mexico

Author(s):Meenakshi Bisht

Product Code:KROD5944

Region:Mexico

Author(s):Meenakshi Bisht

Product Code:KROD5944

December 2024

89

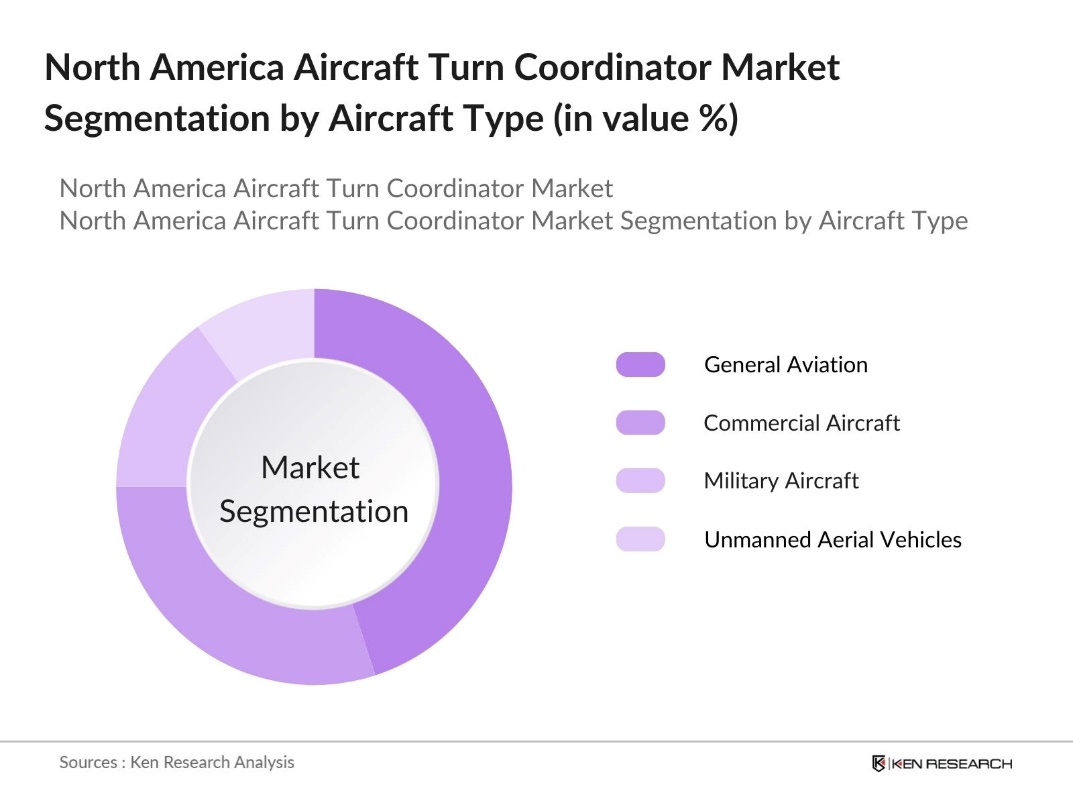

By Aircraft Type: The North America Aircraft Turn Coordinator Market is segmented by aircraft type into General Aviation, Commercial Aircraft, Military Aircraft, and Unmanned Aerial Vehicles (UAVs). General aviation aircraft have a dominant market share under this segmentation due to the large fleet size in North America, particularly in the United States. General aviation, which encompasses private planes, charter services, and recreational aircraft, accounts for a significant demand for turn coordinators because of the mandatory installation of avionics safety systems in smaller aircraft.

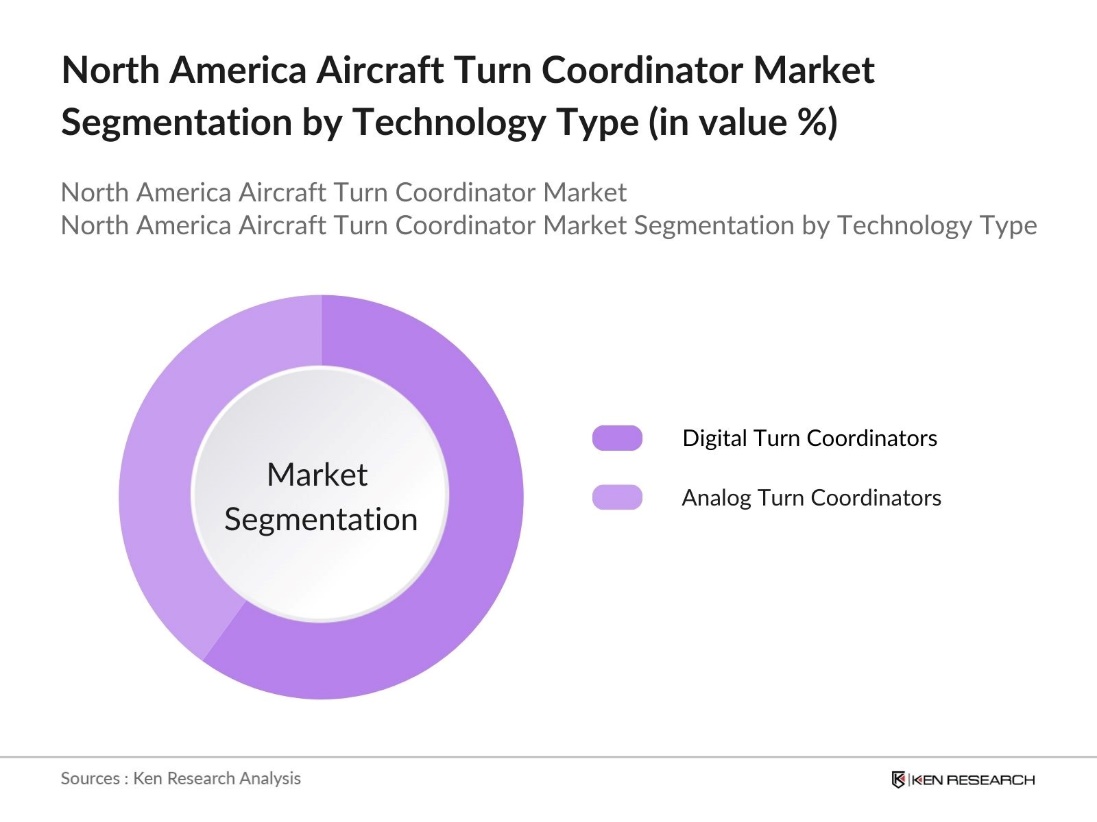

By Technology: The North America Aircraft Turn Coordinator Market is also segmented by technology into Analog Turn Coordinators and Digital Turn Coordinators. Digital turn coordinators dominate the market share due to the increasing trend of cockpit digitalization and enhanced reliability compared to analog systems. Aircraft operators, especially in the commercial and military segments, are investing heavily in digital avionics suites to improve operational efficiency and comply with regulatory requirements.

The North America Aircraft Turn Coordinator Market is characterized by a competitive landscape where several key players hold significant positions. The market is largely dominated by major avionics manufacturers such as Honeywell and Garmin. These companies have a strong foothold due to their robust product portfolios, long-standing client relationships, and continuous innovation in avionics technologies.

|

Company Name |

Establishment Year |

Headquarters |

Key Product Line |

R&D Investment (USD Mn) |

Employees |

Market Revenue (USD Mn) |

Technology Patents |

Geographic Reach |

|

Honeywell International Inc. |

1906 |

Charlotte, USA |

||||||

|

Garmin Ltd. |

1989 |

Olathe, USA |

||||||

|

Collins Aerospace |

2018 (merged) |

Charlotte, USA |

||||||

|

L3Harris Technologies |

1890 |

Melbourne, USA |

||||||

|

Dynon Avionics |

2000 |

Woodinville, USA |

Over the next few years, the North America Aircraft Turn Coordinator Market is expected to see continued growth due to rising investments in advanced avionics, increasing demand for unmanned aerial systems, and the push for the modernization of existing aircraft fleets. The market will benefit from new aircraft production as well as retrofit programs for aging aircraft, particularly in the general aviation sector.

|

By Aircraft Type |

General Aviation Commercial Aircraft Military Aircraft UAVs and Drones |

|

By Technology |

Analog Turn Coordinators Digital Turn Coordinators |

|

By Sales Channel |

OEM Aftermarket |

|

By End-User |

Civil Aviation Military Aviation UAV Operators |

|

By Region |

United States Canada Mexico |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Incorporating Aircraft Fleet Expansion, Navigation System Advancements)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Technological Integrations, Fleet Upgrades)

3.1. Growth Drivers

3.1.1. Increasing Adoption of General Aviation Aircraft

3.1.2. Advancements in Avionics Systems (Emphasis on Safety and Compliance Standards)

3.1.3. Growing Commercial Aviation Sector

3.1.4. Regulatory Requirements for Aircraft Safety

3.2. Market Challenges

3.2.1. High Cost of Aircraft Avionics Components

3.2.2. Stringent Certification Processes (FAA and EASA Standards)

3.2.3. Limited Availability of Skilled Technicians

3.3. Opportunities

3.3.1. Emerging Demand from UAV and Drone Manufacturers

3.3.2. Technological Collaborations in Avionics Development

3.3.3. Expansion into Electric and Hybrid Aircraft Segments

3.4. Trends

3.4.1. Shift Towards Digital Cockpit Systems

3.4.2. Integration with Autonomous Navigation Systems

3.4.3. Increased Focus on Lightweight Components for Fuel Efficiency

3.5. Government Regulation

3.5.1. FAA Mandates on Avionics Safety Standards

3.5.2. EASA Compliance for Turn Coordinator Systems

3.5.3. Trade and Import Regulations Impacting Component Availability

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis (Focusing on Supplier Power and New Entrants in Avionics Manufacturing)

3.9. Competition Ecosystem (Including OEMs and Aftermarket Providers)

4.1. By Aircraft Type (In Value %)

4.1.1. General Aviation

4.1.2. Commercial Aircraft

4.1.3. Military Aircraft

4.1.4. UAVs and Drones

4.2. By Technology (In Value %)

4.2.1. Analog Turn Coordinators

4.2.2. Digital Turn Coordinators

4.3. By Sales Channel (In Value %)

4.3.1. OEM

4.3.2. Aftermarket

4.4. By End-User (In Value %)

4.4.1. Civil Aviation

4.4.2. Military Aviation

4.4.3. UAV Operators

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5.1 Detailed Profiles of Major Companies (Competitors Analysis)

5.1.1. Honeywell International Inc.

5.1.2. Garmin Ltd.

5.1.3. Collins Aerospace (Raytheon Technologies)

5.1.4. L3Harris Technologies, Inc.

5.1.5. Dynon Avionics

5.1.6. BendixKing

5.1.7. Mid-Continent Instruments and Avionics

5.1.8. Aerosonic Corporation

5.1.9. SigmaTek

5.1.10. Genesys Aerosystems

5.1.11. Aspen Avionics

5.1.12. Sandia Aerospace

5.1.13. TruTrak Flight Systems

5.1.14. Avidyne Corporation

5.1.15. Precise Flight Inc.

5.2 Cross Comparison Parameters (Product Portfolio, Turn Coordinator Types, Production Capacity, Avionics Integration)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers, Partnerships, and Acquisitions)

5.5. Investment Analysis (R&D Investment in Avionics Systems)

5.6. Venture Capital Funding (For Start-ups in Avionics Innovation)

5.7. Government Grants and Support for Aircraft Component Manufacturers

6.1. FAA Certification Requirements for Turn Coordinators

6.2. EASA Compliance Guidelines

6.3. Environmental and Sustainability Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Aircraft Type (In Value %)

8.2. By Technology (In Value %)

8.3. By Sales Channel (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives (Focusing on Aftermarket Expansion)

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe first step involved mapping the ecosystem of stakeholders in the North America Aircraft Turn Coordinator Market, utilizing both primary and secondary sources. Extensive desk research was conducted through governmental aviation agencies and proprietary databases to identify the most critical variables, such as avionics demand trends, regulatory requirements, and technological advancements.

Historical data from the past five years was analyzed, including the penetration of turn coordinators across different aircraft categories. The revenue generation of key market players was also assessed, and sales patterns of turn coordinator systems were analyzed to understand their adoption rates across general aviation, commercial airlines, and UAV manufacturers.

Market hypotheses were developed and validated through direct interviews with industry experts from major avionics manufacturing companies and airlines. These consultations provided insights into the operational and financial dynamics of the turn coordinator market, including key drivers of growth and potential challenges.

The final stage involved engaging with multiple aircraft manufacturers to gain direct feedback on product preferences, regulatory influences, and emerging trends in turn coordinator systems. The collected data was synthesized and cross-verified to deliver a comprehensive report on the North America Aircraft Turn Coordinator Market.

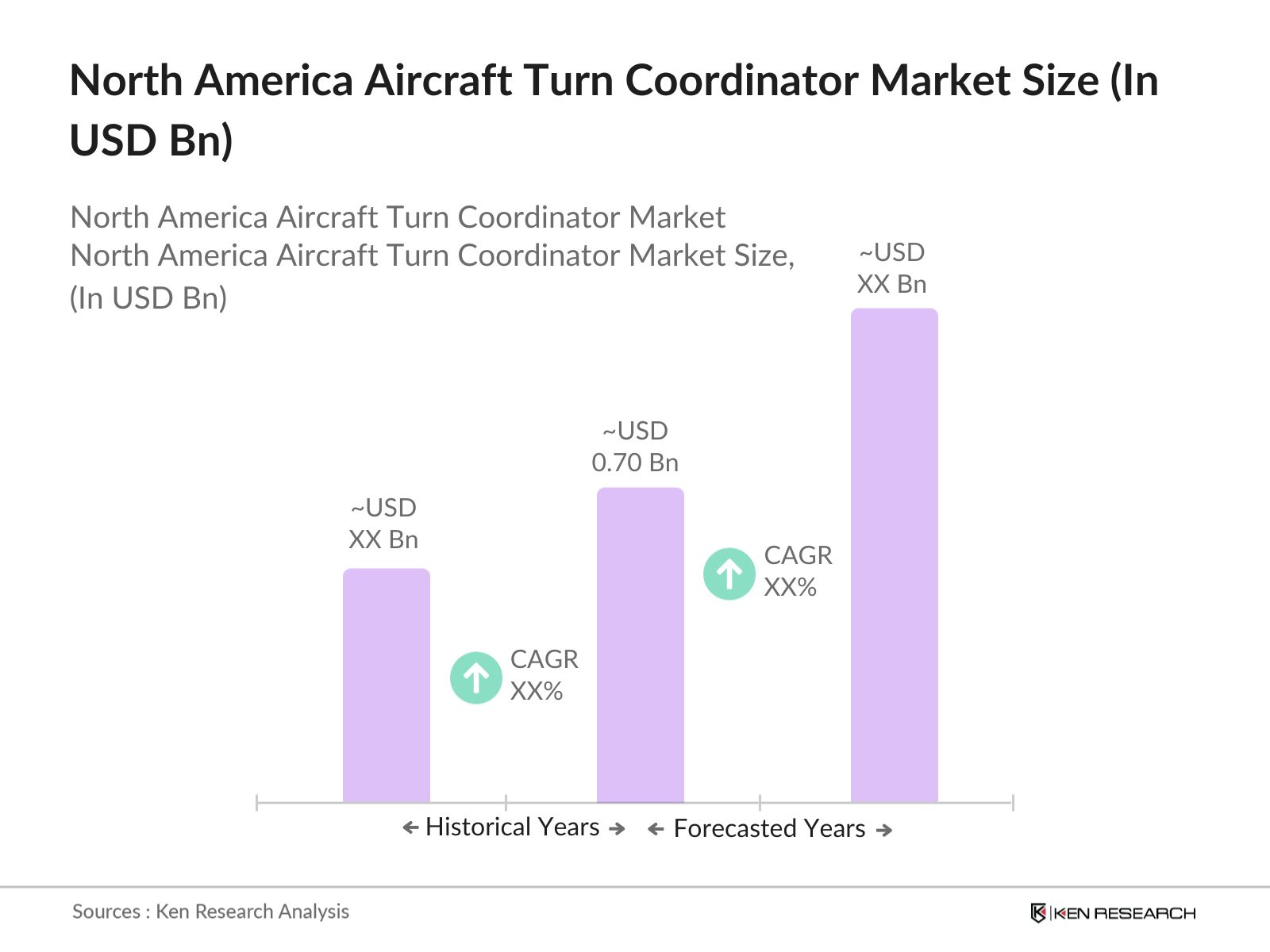

The North America Aircraft Turn Coordinator Market was valued at USD 0.70 billion. The market is driven by advancements in avionics technology and increasing demand from general and commercial aviation sectors, as well as the UAV market.

The key challenges in the North America Aircraft Turn Coordinator Market include high costs of avionics components, stringent certification requirements from aviation authorities like the FAA, and the shortage of skilled technicians required for system installations and maintenance.

Key players in the North America Aircraft Turn Coordinator Market include Honeywell International, Garmin Ltd., Collins Aerospace, Dynon Avionics, and BendixKing, which dominate the market due to their extensive product offerings and strong relationships with aircraft manufacturers and airlines.

Growth drivers in North America Aircraft Turn Coordinator Market include the increasing production of general and commercial aviation aircraft, rising demand for UAV systems, and advancements in digital avionics that improve aircraft safety and operational efficiency.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.