North America Antifungal Drugs Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD5527

November 2024

89

About the Report

North America Antifungal Drugs Market Overview

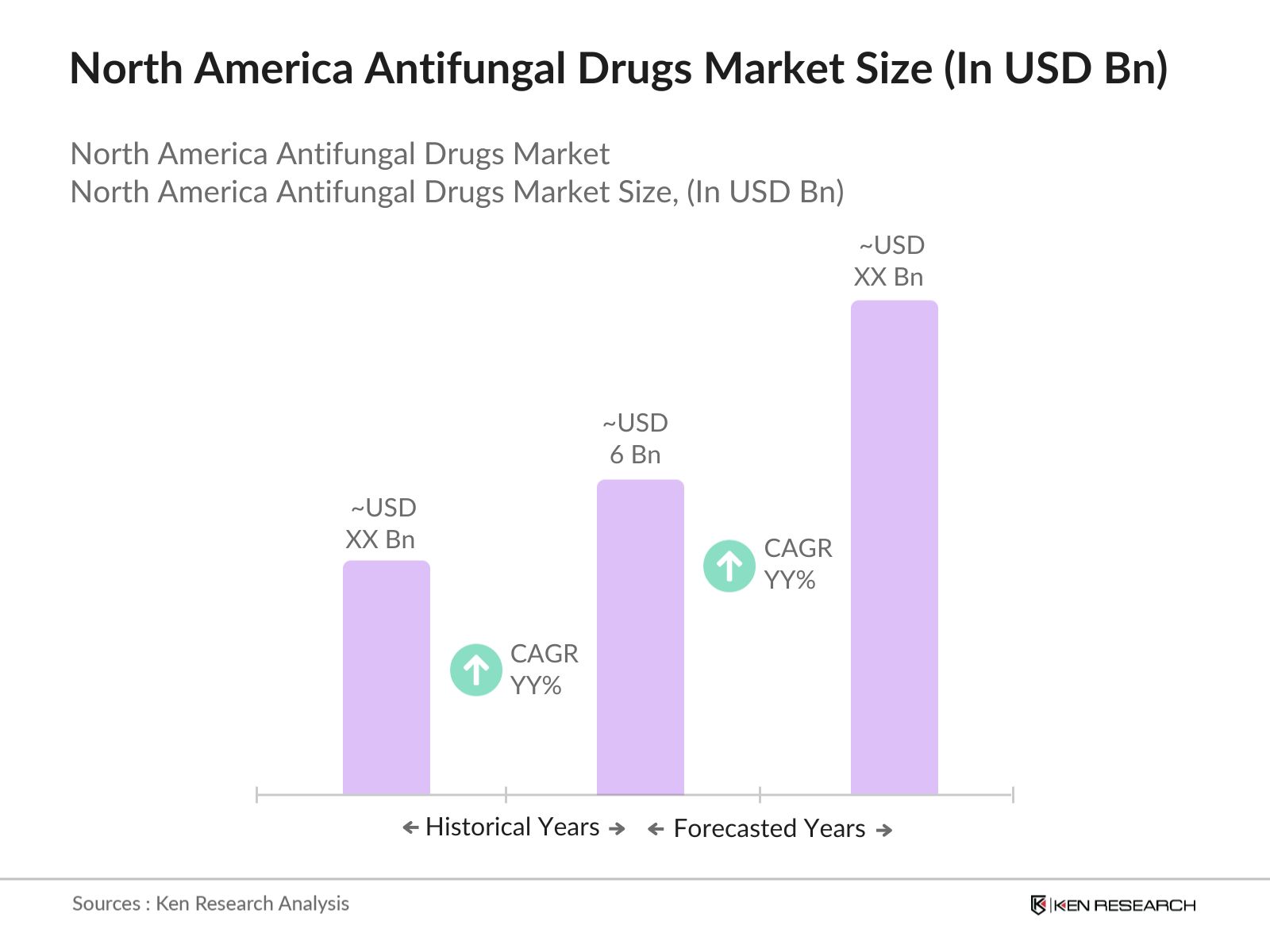

- The North America Antifungal Drugs Market is valued at USD 6 billion, based on a five-year historical analysis. This market is driven by the increasing incidence of fungal infections, particularly among immunocompromised patients, such as those undergoing chemotherapy, organ transplants, or HIV treatment.

- Countries like the United States and Canada dominate the market due to their well-established healthcare infrastructure, high investment in research and development, and strong presence of key pharmaceutical players. In these regions, the increasing prevalence of fungal infections among aging populations and immunocompromised individuals has led to higher demand for antifungal medications.

- In 2023, the CDC continued its funding under the Antimicrobial Resistance (AMR) Solutions Initiative, dedicating over $170 million annually to fight drug-resistant pathogens, including antifungal resistance. This program supports the surveillance and development of diagnostic tools that enable healthcare providers to identify resistant fungal strains more effectively, thereby driving demand for new and innovative antifungal drugs.

North America Antifungal Drugs Market Segmentation

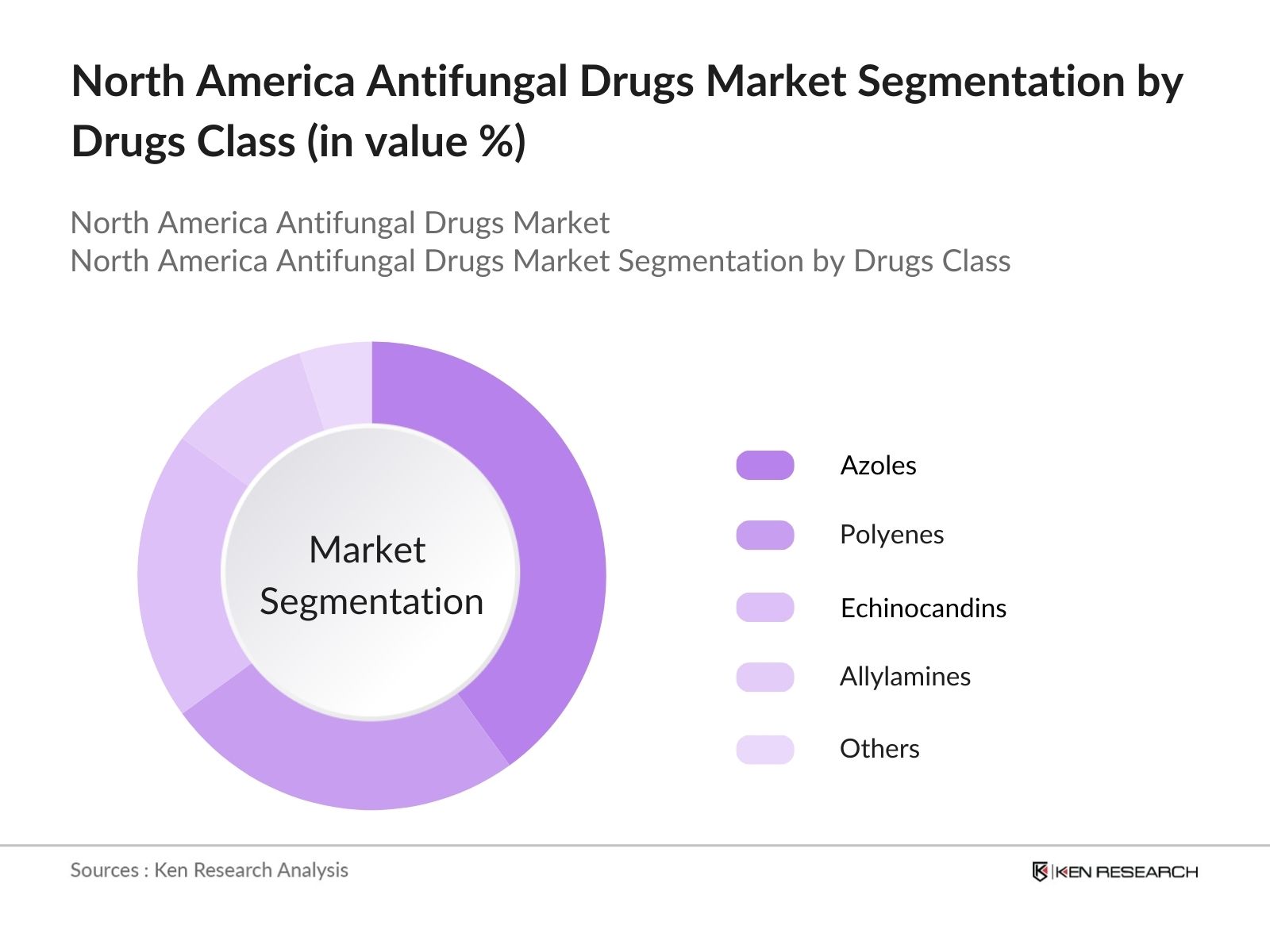

By Drug Class: The market is segmented by drug class into azoles, polyenes, echinocandins, allylamines, and others. Azoles hold a dominant market share due to their widespread usage and efficacy in treating a broad spectrum of fungal infections. Azoles, such as fluconazole and itraconazole, are known for their lower toxicity compared to other antifungal classes and their ability to treat both superficial and systemic fungal infections effectively. The availability of these drugs in both oral and intravenous forms makes them a preferred choice in hospitals and clinics across North America.

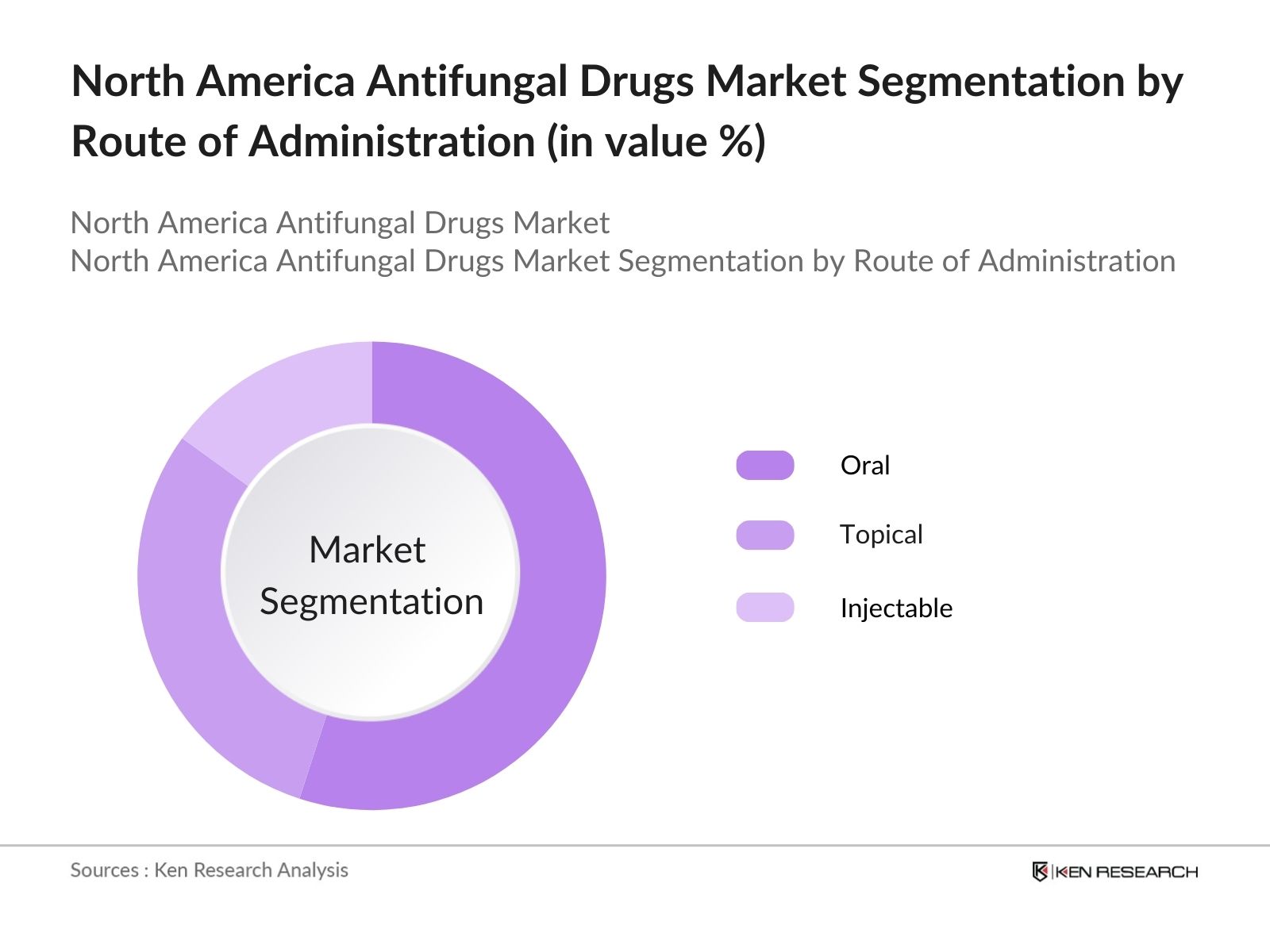

By Route of Administration: The market is also segmented by route of administration into oral, topical, and injectable. Oral antifungals dominate the market because of their ease of administration and patient compliance. Drugs like fluconazole and terbinafine are commonly prescribed in oral form for treating fungal infections, ranging from superficial infections like dermatophytosis to more severe systemic infections. Oral antifungals are favored for their convenience, especially in outpatient settings, and offer effective results for both acute and chronic fungal conditions.

North America Antifungal Drugs Market Competitive Landscape

The market is highly consolidated, with a few major pharmaceutical players leading the sector. Companies like Pfizer, Merck & Co., and Gilead Sciences hold market positions due to their extensive drug portfolios, substantial R&D investments, and strong distribution networks.

|

Company |

Establishment Year |

Headquarters |

Drug Portfolio |

R&D Investment |

Patents |

Pipeline Drugs |

Market Share |

Global Presence |

|

Pfizer Inc. |

1849 |

New York, U.S. |

||||||

|

Merck & Co., Inc. |

1891 |

Kenilworth, U.S. |

||||||

|

Gilead Sciences, Inc. |

1987 |

Foster City, U.S. |

||||||

|

Novartis AG |

1996 |

Basel, Switzerland |

||||||

|

Johnson & Johnson |

1886 |

New Brunswick, U.S. |

North America Antifungal Drugs Market Analysis

Market Growth Drivers

- Increasing Incidence of Fungal Infections in Immunocompromised Patients: Immunocompromised individuals, particularly those undergoing cancer treatments, organ transplants, or HIV/AIDS patients, have a higher risk of fungal infections. According to the Centers for Disease Control and Prevention (CDC), in 2023, the number of organ transplants in the U.S. was around 46,000 annually, which has been steadily increasing, leading to a greater demand for antifungal treatments, thereby driving the demand for antifungal drugs in North America.

- Growing Hospitalization Rates: Hospital-acquired infections, including fungal infections such as invasive candidiasis, are a critical concern. In 2023, the U.S. saw over 36 million hospital admissions, out of which around 90,000 cases of hospital-acquired fungal infections were documented (CDC). The high volume of hospitalizations, particularly in intensive care units (ICUs), creates a sustained demand for antifungal therapies in hospitals, making it a key driver for the market.

- Growing Geriatric Population: The U.S. Census Bureau estimated that in 2023, there were approximately 56 million people aged 65 or older in the U.S. This number is expected to increase steadily over the next decade, with elderly populations being more vulnerable to fungal infections due to weakened immune systems and the increased likelihood of comorbidities. As the elderly population grows, the demand for antifungal treatments is projected to increase proportionally.

Market Challenges

- Drug Resistance in Fungal Infections: One of the key challenges is the rising resistance to existing antifungal medications. Candida auris, which was first identified in the U.S., has shown growing resistance to commonly used antifungal drugs. By 2023, nearly 30% of C. auris cases exhibited resistance to at least one type of antifungal, which makes treatment more difficult and costly. This issue continues to challenge healthcare systems in the region.

- Side Effects and Toxicity of Antifungal Drugs: Antifungal drugs, especially those used to treat invasive fungal infections, often come with serious side effects such as liver toxicity and kidney damage. According to the U.S. Food and Drug Administration (FDA), in 2023, reports of adverse drug reactions associated with certain antifungals like Amphotericin B led to a growing concern about the long-term safety of these drugs, which can limit their use in vulnerable populations such as the elderly or those with pre-existing conditions.

North America Antifungal Drugs Market Future Outlook

Over the next five years, the North America Antifungal Drugs industry is expected to exhibit growth, driven by rising fungal infection cases, advancements in drug formulations, and the expansion of the healthcare infrastructure. The increasing availability of combination therapies, which offer higher efficacy and lower resistance, is also anticipated to boost the market.

Future Market Opportunities

- Increased Focus on Combination Therapies: Over the next five years, pharmaceutical companies are expected to increasingly focus on combination therapies for fungal infections. By 2029, more than 15% of antifungal treatment regimens are projected to involve combinations of different drug classes, aimed at improving efficacy and addressing drug resistance, particularly for invasive fungal infections like candidemia and aspergillosis.

- Development of Personalized Antifungal Therapies: The rise of precision medicine will impact the antifungal drugs market. By 2028, personalized treatment plans based on genetic and molecular profiling of fungal pathogens are expected to become more common, as indicated by recent advancements in genomics and molecular diagnostics. This shift will allow for more targeted and effective antifungal therapies, reducing treatment durations and side effects.

Scope of the Report

|

By Drug Class |

Azoles Polyenes Echinocandins Allylamines Others |

|

By Route of Administration |

Oral Topical Injectable |

|

By Indication |

Candidiasis Aspergillosis Cryptococcosis Dermatophytosis Others |

|

By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

|

By Region |

U.S. Canada Mexico |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Pharmaceutical Manufacturers

Healthcare Providers

Government and Regulatory Bodies (U.S. FDA, Health Canada)

Banks and Financial Institution

Venture Capital and Investment Firms

Biotech Startups

Companies

Players Mentioned in the Report:

Pfizer Inc.

Merck & Co., Inc.

Gilead Sciences, Inc.

Novartis AG

Johnson & Johnson

Astellas Pharma Inc.

Bristol-Myers Squibb

GlaxoSmithKline Plc

Cipla Inc.

Mylan N.V.

Bayer AG

Sanofi S.A.

Basilea Pharmaceutica Ltd.

Scynexis Inc.

Sun Pharmaceutical Industries Ltd.

Table of Contents

1. North America Antifungal Drugs Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate (CAGR, Revenue, Prescription Volume)

1.4 Market Segmentation Overview

2. North America Antifungal Drugs Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis (Growth Rate, Prescription Trends)

2.3 Key Market Developments and Milestones (Approvals, Launches, Mergers)

3. North America Antifungal Drugs Market Analysis

3.1 Growth Drivers

3.1.1 Rising Incidence of Fungal Infections (Candida, Aspergillus, Cryptococcus)

3.1.2 Increased Demand for Immunocompromised Patient Treatment (HIV/AIDS, Cancer, Organ Transplant)

3.1.3 Advancements in Diagnostic Techniques (Fungal Susceptibility Testing)

3.2 Market Challenges

3.2.1 Drug Resistance (Azole and Echinocandin Resistance)

3.2.2 High Cost of Development and Clinical Trials (R&D Expenditure)

3.2.3 Regulatory Barriers (FDA Regulations, EMA Guidelines)

3.3 Opportunities

3.3.1 Growth of Combination Therapies (Polyenes + Echinocandins)

3.3.2 Expansion into Untapped Geographies (Rural and Low-Income Markets)

3.3.3 Introduction of Novel Antifungal Classes (Olorofim, Rezafungin)

3.4 Trends

3.4.1 Increasing Focus on Fungal Infection Prevention (Prophylactic Treatments)

3.4.2 Partnerships Between Biotech and Pharma Companies (Collaborations, Licensing)

3.4.3 Growth in Telemedicine Prescriptions (Digital Health, Remote Prescriptions)

3.5 Government Regulations

3.5.1 U.S. FDA Antifungal Drug Approvals

3.5.2 Canadian Health Regulatory Standards

3.5.3 U.S. CDC Guidelines on Fungal Infections

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Pharma Companies, Diagnostic Labs, Hospitals, Clinics)

3.8 Porters Five Forces (Buyer Power, Supplier Power, Competitive Rivalry, Substitution Risk, New Entrants)

3.9 Competition Ecosystem

4. North America Antifungal Drugs Market Segmentation

4.1 By Drug Class (In Value %)

4.1.1 Azoles (Fluconazole, Itraconazole)

4.1.2 Polyenes (Amphotericin B, Nystatin)

4.1.3 Echinocandins (Caspofungin, Micafungin)

4.1.4 Allylamines (Terbinafine)

4.1.5 Others (Flucytosine)

4.2 By Route of Administration (In Value %)

4.2.1 Oral

4.2.2 Topical

4.2.3 Injectable

4.3 By Indication (In Value %)

4.3.1 Candidiasis (Oropharyngeal, Invasive, Vaginal)

4.3.2 Aspergillosis

4.3.3 Cryptococcosis

4.3.4 Dermatophytosis (Onychomycosis, Tinea)

4.3.5 Others (Zygomycosis)

4.4 By Distribution Channel (In Value %)

4.4.1 Hospital Pharmacies

4.4.2 Retail Pharmacies

4.4.3 Online Pharmacies

4.5 By Region (In Value %)

4.5.1 U.S.

4.5.2 Canada

4.5.3 Mexico

5. North America Antifungal Drugs Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Pfizer Inc.

5.1.2 Merck & Co., Inc.

5.1.3 Gilead Sciences, Inc.

5.1.4 Novartis AG

5.1.5 Astellas Pharma Inc.

5.1.6 Johnson & Johnson

5.1.7 Bristol-Myers Squibb

5.1.8 GlaxoSmithKline Plc

5.1.9 Cipla Inc.

5.1.10 Mylan N.V.

5.1.11 Bayer AG

5.1.12 Sanofi S.A.

5.1.13 Basilea Pharmaceutica Ltd.

5.1.14 Scynexis Inc.

5.1.15 Sun Pharmaceutical Industries Ltd.

5.2 Cross Comparison Parameters (Market Share, Drug Portfolio, Revenue, R&D Investment, Patent Strength, Pipeline Drugs, Market Presence, Manufacturing Facilities)

5.3 Market Share Analysis (In %, By Drug Class, Indication)

5.4 Strategic Initiatives (New Launches, Partnerships, Joint Ventures, Collaborations)

5.5 Mergers and Acquisitions

5.6 Investment Analysis (Venture Capital, Private Equity)

6. North America Antifungal Drugs Market Regulatory Framework

6.1 U.S. FDA Compliance and Guidelines

6.2 Health Canada Regulations

6.3 Intellectual Property Laws for Pharmaceuticals

6.4 Drug Approval Pathways

7. North America Antifungal Drugs Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. North America Antifungal Drugs Future Market Segmentation

8.1 By Drug Class (In Value %)

8.2 By Route of Administration (In Value %)

8.3 By Indication (In Value %)

8.4 By Distribution Channel (In Value %)

8.5 By Region (In Value %)

9. North America Antifungal Drugs Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The research process begins with the identification of key variables influencing the North America Antifungal Drugs Market. This includes an ecosystem analysis of stakeholders such as pharmaceutical companies, healthcare providers, and regulatory bodies. Comprehensive desk research and industry databases were utilized to define the primary variables.

Step 2: Market Analysis and Construction

Historical data on drug class penetration, revenue, and prescription trends were collected and analyzed. The market's revenue generation is scrutinized, ensuring the reliability of the data. Additionally, healthcare infrastructure statistics are reviewed to forecast future demand.

Step 3: Hypothesis Validation and Expert Consultation

Consultations with industry experts, including drug manufacturers and healthcare providers, were conducted. These consultations validate the data and offer firsthand insights into market trends and operational performance, refining our hypotheses.

Step 4: Research Synthesis and Final Output

The final step involved the synthesis of research findings, providing a comprehensive outlook on market size, segmentation, and competitive landscape. These insights were cross-verified with multiple antifungal drug manufacturers and healthcare experts.

Frequently Asked Questions

01. How big is the North America Antifungal Drugs Market?

The North America Antifungal Drugs Market is valued at USD 6 billion, driven by the increasing prevalence of fungal infections and growing demand for advanced antifungal therapies.

02. What are the challenges in the North America Antifungal Drugs Market?

The major challenges in the North America Antifungal Drugs Market include rising drug resistance, stringent regulatory hurdles, and high R&D costs, which can slow down new drug development and market entry.

03. Who are the major players in the North America Antifungal Drugs Market?

Key players in the North America Antifungal Drugs Market include Pfizer Inc., Merck & Co., Gilead Sciences, Novartis AG, and Johnson & Johnson. These companies dominate due to their extensive drug portfolios and strong R&D investments.

04. What are the growth drivers of the North America Antifungal Drugs Market?

Growth drivers in the North America Antifungal Drugs Market include the increasing incidence of fungal infections, rising immunocompromised populations, and advancements in diagnostic technologies, which enable early detection and treatment.

05. What are the future prospects for the North America Antifungal Drugs Market?

The North America Antifungal Drugs Market is expected to grow in the coming years, driven by the development of new antifungal drug classes, combination therapies, and advancements in healthcare infrastructure across North America.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.