North America Autonomous Underwater Vehicle Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD9603

Region:North America

Author(s):Sanjeev

Product Code:KROD9603

October 2024

81

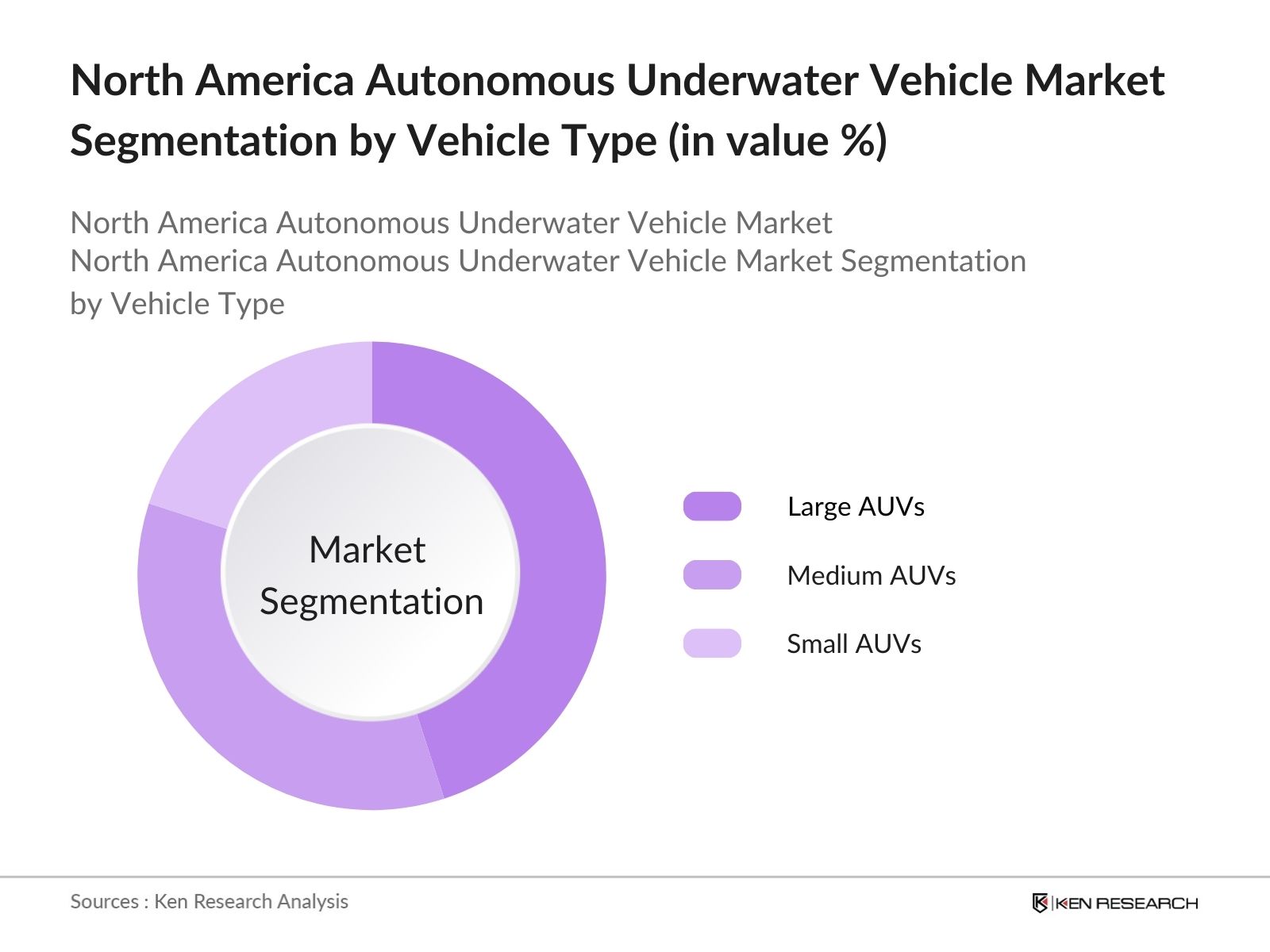

By Vehicle Type: The market is segmented by vehicle type into large AUVs, medium AUVs, and small AUVs. Large AUVs hold the dominant market share due to their capability to perform long-duration, deep-sea missions that are crucial for military and offshore oil exploration operations. Their advanced sensor integration, longer battery life, and extensive communication systems make them ideal for high-stakes missions. Large AUVs are used extensively by defense and energy sectors, where operational reliability and deep-sea capabilities are essential.

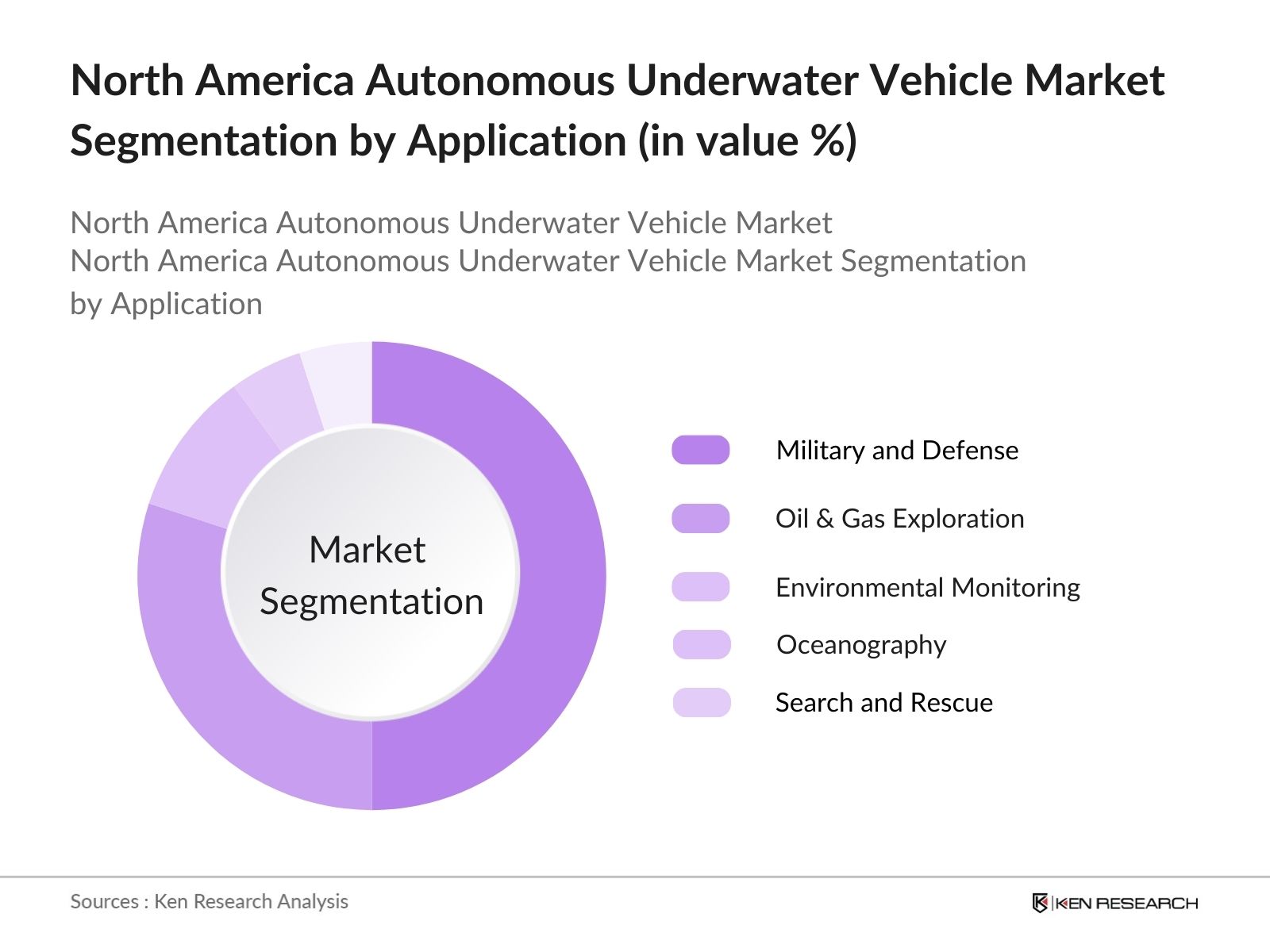

By Application: The market in North America is segmented by application into military and defense, oil & gas exploration, environmental monitoring, oceanography, and search and rescue. The military and defense segment dominates the market due to the increasing use of AUVs for surveillance, mine detection, and underwater combat operations. The demand for unmanned underwater systems in naval operations continues to grow, driven by the need for reducing human risk in hazardous missions and enhancing real-time data collection capabilities.

The North America Autonomous Underwater Vehicle market is dominated by key players, with a few large corporations controlling portions of the market. These companies lead in terms of R&D investment, technological innovation, and strategic partnerships with defense and energy sectors. The defense sector is heavily consolidated with companies like General Dynamics and Boeing, leveraging their historical ties to the U.S. Navy.

| Company Name | Establishment Year | Headquarters | Revenue (USD bn) | R&D Investment (%) | Key Contracts | No. of Employees | Primary Application | Strategic Partnerships |

|---|---|---|---|---|---|---|---|---|

| General Dynamics | 1952 | Reston, Virginia, USA | - | - | - | - | - | - |

| Boeing | 1916 | Chicago, Illinois, USA | - | - | - | - | - | - |

| L3Harris Technologies | 2019 | Melbourne, Florida, USA | - | - | - | - | - | - |

| Teledyne Marine | 1960 | Thousand Oaks, CA, USA | - | - | - | - | - | - |

| Saab AB | 1937 | Stockholm, Sweden | - | - | - | - | - | - |

The North America Autonomous Underwater Vehicle market is poised for substantial growth over the next five years, driven by increasing investments in underwater robotics, military modernization programs, and the growing demand for oil and gas exploration in deeper waters. Technological advancements in sensor integration, artificial intelligence (AI), and machine learning are expected to enhance the capabilities of AUVs, leading to wider adoption across both defense and commercial sectors. Moreover, initiatives for environmental conservation and the exploration of uncharted deep-sea areas will further boost market demand.

|

By Vehicle Type |

Large AUVs Medium AUVs Small AUVs

|

|

By Technology |

Collision Avoidance Sonar Technology Underwater Positioning System |

|

By Application |

Military and Defense Oil & Gas Exploration Environmental Monitoring Oceanography Search and Rescue |

|

By Propulsion Type |

Electric Mechanical Hybrid |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increased Defense Spending (Military Applications)

3.1.2. Advancements in Underwater Communication Technology

3.1.3. Rise in Offshore Oil & Gas Exploration (Commercial Applications)

3.1.4. Growing Environmental Monitoring and Surveying Initiatives (Environmental Protection and Surveying Applications)

3.2. Market Challenges

3.2.1. High Capital Costs (Initial Investment Costs)

3.2.2. Limited Operational Range and Battery Life

3.2.3. Regulatory Barriers in Underwater Exploration

3.3. Opportunities

3.3.1. Growing Demand for Seabed Mapping and Data Collection (Marine Science)

3.3.2. Expanding Application in Underwater Mining

3.3.3. Collaboration with Academic and Research Institutions for R&D

3.4. Trends

3.4.1. Integration of AI and Machine Learning in AUVs

3.4.2. Miniaturization and Modularity of AUVs

3.4.3. Adoption of Hybrid AUV-ROV Systems

3.5. Government Regulation

3.5.1. Environmental Regulations for Marine Operations

3.5.2. Naval Standards for AUV Deployment

3.5.3. International Maritime Organization (IMO) Guidelines for Underwater Operations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Vehicle Type (In Value %)

4.1.1. Large AUVs

4.1.2. Medium AUVs

4.1.3. Small AUVs

4.2. By Technology (In Value %)

4.2.1. Collision Avoidance

4.2.2. Sonar Technology

4.2.3. Underwater Positioning Systems

4.3. By Application (In Value %)

4.3.1. Military and Defense

4.3.2. Oil & Gas Exploration

4.3.3. Environmental Monitoring

4.3.4. Oceanography

4.3.5. Search and Rescue

4.4. By Propulsion Type (In Value %)

4.4.1. Electric

4.4.2. Mechanical

4.4.3. Hybrid

4.5. By Region (In Value %)

4.5.1. North

4.5.2. West

4.5.3. East

4.5.4. South

5.1. Detailed Profiles of Major Companies

5.1.1. General Dynamics

5.1.2. Boeing

5.1.3. Lockheed Martin

5.1.4. L3Harris Technologies

5.1.5. Teledyne Marine

5.1.6. Saab AB

5.1.7. Kongsberg Gruppen

5.1.8. Fugro

5.1.9. Bluefin Robotics

5.1.10. Ocean Infinity

5.1.11. International Submarine Engineering Ltd.

5.1.12. Atlas Elektronik GmbH

5.1.13. iXblue

5.1.14. ECA Group

5.1.15. Hydroid Inc.

5.2. Cross Comparison Parameters (Revenue, Headquarters, Employees, Product Portfolio, R&D Investment, Market Share, Contracts Secured, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental and Maritime Regulations

6.2. Compliance Requirements for Defense Contracts

6.3. Certification Processes for Autonomous Systems

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Vehicle Type (In Value %)

8.2. By Technology (In Value %)

8.3. By Application (In Value %)

8.4. By Propulsion Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. White Space Opportunity Analysis

9.4. Market Entry and Expansion Strategies

The first phase involves identifying key variables influencing the North America AUV market, focusing on defense contracts, oil exploration, and environmental monitoring. Extensive secondary research using proprietary databases is conducted to define market drivers, challenges, and opportunities.

This step compiles historical data related to AUV deployments, analyzing defense spending patterns, offshore exploration activities, and research missions in North American waters. An assessment of operational success rates and technological adoption is also conducted.

Market hypotheses on AUV adoption trends are validated through expert interviews with industry leaders from defense, oil, and environmental sectors. These insights offer a deeper understanding of operational challenges and R&D investment trends.

Finally, primary data collected from AUV manufacturers is combined with secondary research to synthesize a final report. This process ensures that the market analysis is comprehensive, providing an accurate reflection of the North America AUV market dynamics.

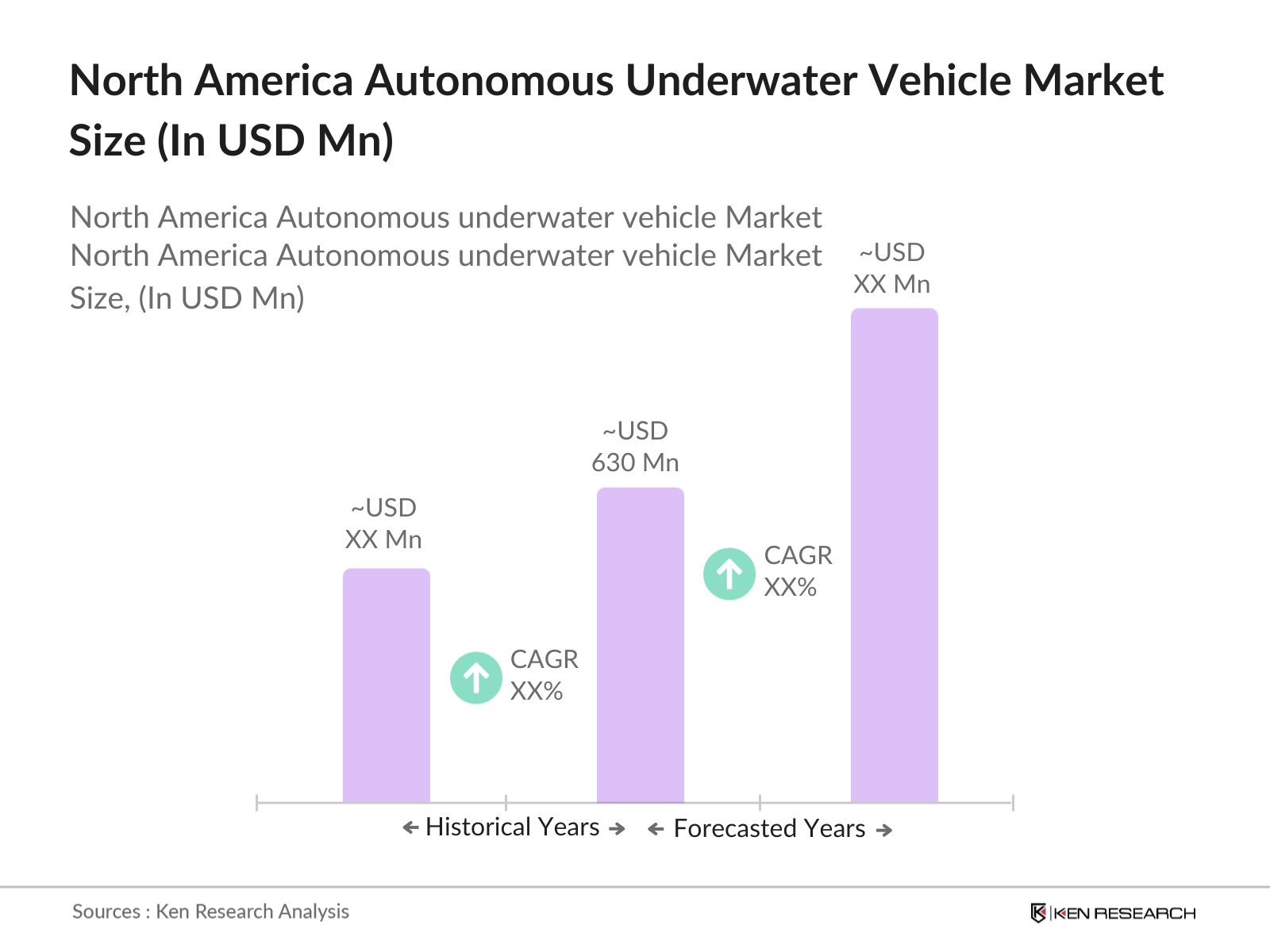

The North America Autonomous Underwater Vehicle market is valued at USD 630 million, driven by increased defense spending and the growing need for environmental monitoring in offshore regions.

Challenges in North America Autonomous Underwater Vehicle market include high operational costs, limited battery life, and regulatory barriers in underwater operations. These challenges hinder the wider adoption of AUVs, particularly in commercial sectors.

Key players in the North America Autonomous Underwater Vehicle market include General Dynamics, Boeing, Lockheed Martin, L3Harris Technologies, and Teledyne Marine. These companies dominate due to their extensive R&D capabilities and strong defense sector ties.

Growth drivers in North America Autonomous Underwater Vehicle market include rising defense budgets, advancements in underwater communication technologies, and the increasing need for oil and gas exploration in deeper waters.

Government regulations play a crucial role in North America Autonomous Underwater Vehicle market, particularly in defense contracts and environmental monitoring mandates. Compliance with international maritime laws also shapes market strategies for AUV manufacturers.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.