North America Bakery Products Market Outlook to 2030

Region:Mexico

Author(s):Shreya Garg

Product Code:KROD5897

Region:Mexico

Author(s):Shreya Garg

Product Code:KROD5897

December 2024

90

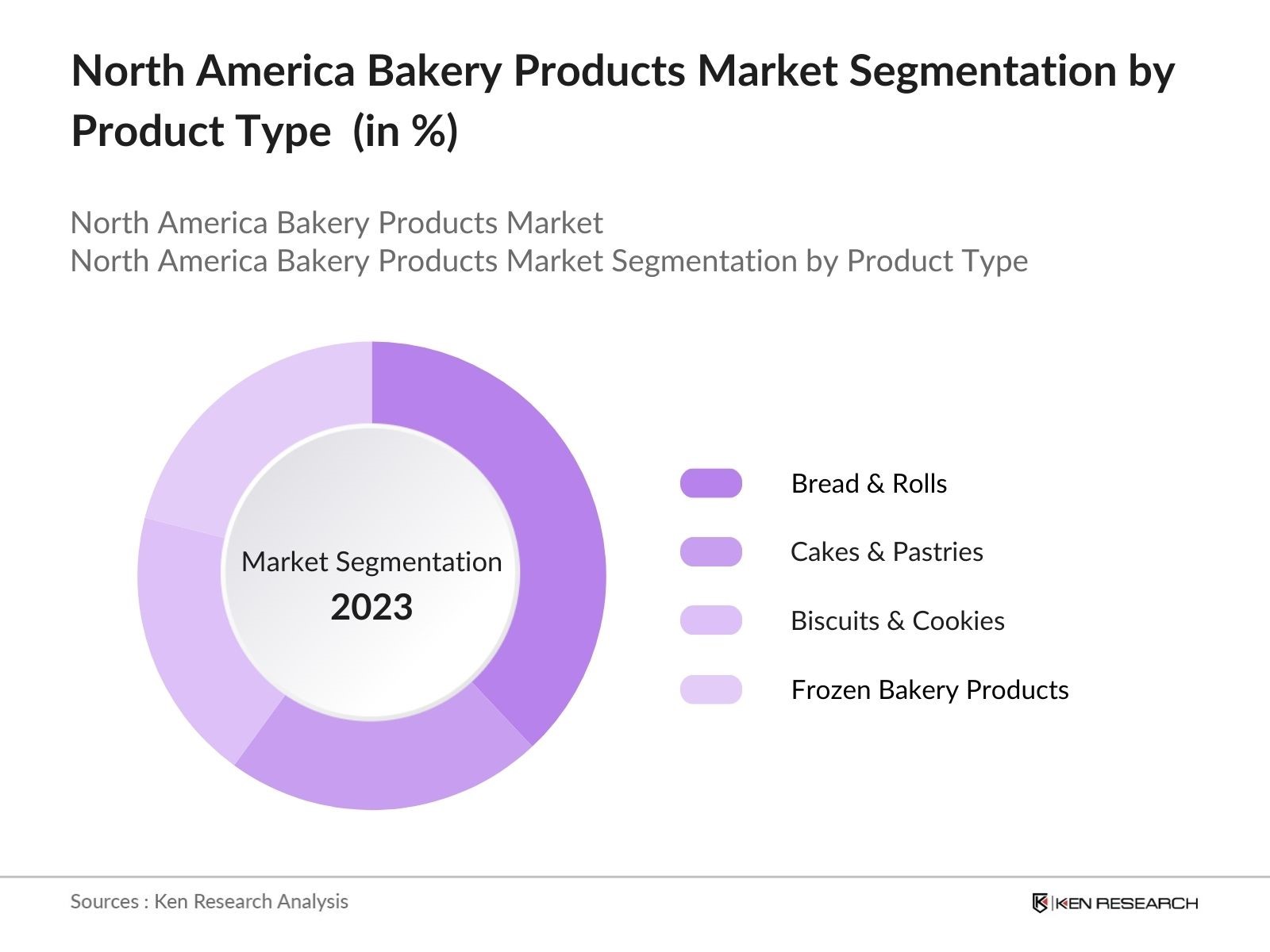

By Product Type: The market is segmented by product type into bread & rolls, cakes & pastries, biscuits & cookies, and frozen bakery products. Bread & rolls hold a dominant market share due to their staple nature in the North American diet. Their widespread consumption, particularly in the form of sandwiches, and the constant introduction of new varieties like whole grain and multigrain products, drive this segment. Additionally, their relatively longer shelf life compared to other baked goods makes them a preferred choice among consumers.

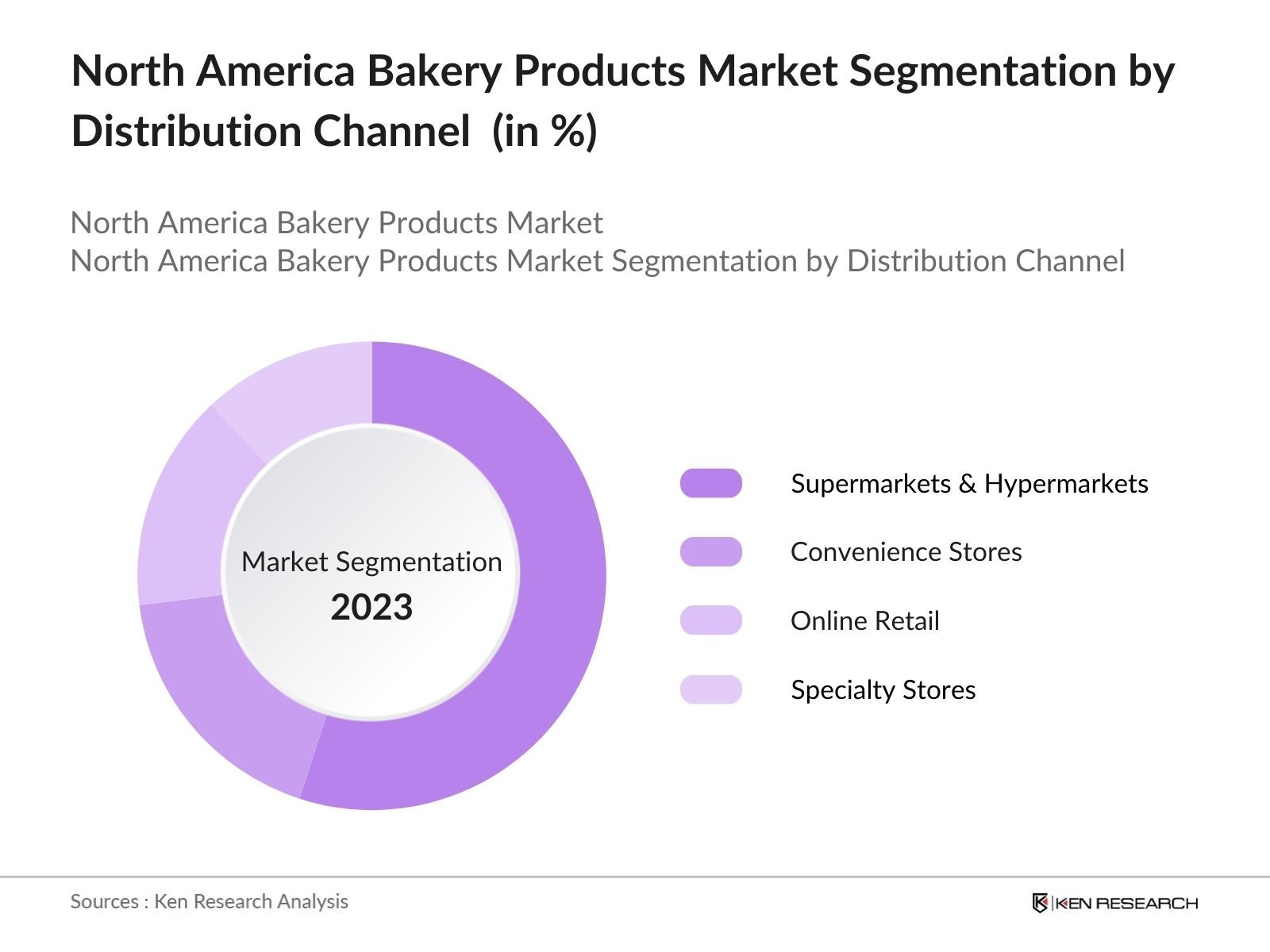

By Distribution Channel: The market is segmented by distribution channels into supermarkets & hypermarkets, convenience stores, online retail, and specialty stores. Supermarkets & hypermarkets lead the market due to their large product variety, ease of access, and promotional offers. These retail outlets provide consumers with a broad selection of bakery products, ranging from freshly baked goods to packaged items, all under one roof. Their significant foot traffic and extensive reach into urban and suburban markets further solidify their position as the dominant distribution channel.

The North American bakery products market is highly competitive, with a mix of global giants and local players. The major companies in this market continually innovate by introducing healthier alternatives and expanding their product portfolios to cater to evolving consumer preferences. Additionally, many key players are focused on sustainability initiatives, such as eco-friendly packaging and reducing carbon footprints across their supply chains.

|

Company |

Establishment Year |

Headquarters |

Product Portfolio |

Revenue (2023) |

Geographic Reach |

R&D Investments |

Sustainability Initiatives |

Partnerships |

|

Grupo Bimbo |

1945 |

Mexico City, Mexico |

||||||

|

Mondelez International |

1923 |

Chicago, USA |

||||||

|

General Mills |

1866 |

Minneapolis, USA |

||||||

|

Flowers Foods |

1919 |

Thomasville, USA |

||||||

|

Aryzta AG |

2008 |

Zurich, Switzerland |

Over the next five years, the North America bakery products market is expected to experience steady growth. This growth will be driven by evolving consumer preferences for healthier options, including gluten-free, organic, and vegan bakery products. The increased focus on premium and artisanal offerings, coupled with technological advancements in packaging and manufacturing, will further propel market expansion. Additionally, the growth of e-commerce platforms for the sale of bakery products is anticipated to offer new opportunities for market players.

|

Product Type |

Bread & Rolls Cakes & Pastries Biscuits & Cookies Frozen Bakery Products Other Bakery Products |

|

Distribution Channel |

Supermarkets & Hypermarkets Convenience Stores Online Retail Specialty Stores Other Channels |

|

Ingredient Type |

Wheat-Based Gluten-Free Dairy-Free Organic Ingredients |

|

End-User |

Retail Consumers Food Service Industry |

|

Region |

USA Canada Mexico |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Consumer Demand for Convenience Foods

3.1.2. Growing Popularity of Health-conscious Bakery Products

3.1.3. Rise in Urbanization and Changing Lifestyles

3.1.4. Expansion of E-commerce in the Food & Beverage Sector

3.2. Market Challenges

3.2.1. Fluctuations in Raw Material Prices (Wheat, Sugar)

3.2.2. Health Regulations on Sugar and Gluten

3.2.3. Rising Competition from Private Labels

3.3. Opportunities

3.3.1. Introduction of Gluten-Free and Organic Products

3.3.2. Increasing Demand for Frozen and Ready-to-Eat Products

3.3.3. Potential for Innovation in Packaging and Shelf-Life Improvement

3.4. Trends

3.4.1. Growing Demand for Vegan and Plant-Based Bakery Products

3.4.2. Rise in Artisanal and Specialty Bakery Products

3.4.3. Expansion of Bakery Cafes and Boutique Stores

3.5. Government Regulations

3.5.1. Food Safety Standards and Labeling Regulations

3.5.2. Regulations on Nutritional Content (Sugar, Fat)

3.5.3. Import Tariffs on Ingredients (Wheat, Dairy)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape

4.1. By Product Type (In Value %)

4.1.1. Bread & Rolls

4.1.2. Cakes & Pastries

4.1.3. Biscuits & Cookies

4.1.4. Frozen Bakery Products

4.1.5. Other Bakery Products

4.2. By Distribution Channel (In Value %)

4.2.1. Supermarkets & Hypermarkets

4.2.2. Convenience Stores

4.2.3. Online Retail

4.2.4. Specialty Stores

4.2.5. Other Channels

4.3. By Ingredient Type (In Value %)

4.3.1. Wheat-Based

4.3.2. Gluten-Free

4.3.3. Dairy-Free

4.3.4. Organic Ingredients

4.4. By End-User (In Value %)

4.4.1. Retail Consumers

4.4.2. Food Service Industry

4.5. By Region (In Value %)

4.5.1. USA

4.5.2. Canada

4.5.3. Mexico

5.1. Detailed Profiles of Major Companies

5.1.1. Grupo Bimbo

5.1.2. Mondelez International

5.1.3. General Mills

5.1.4. Campbell Soup Company

5.1.5. The Kellogg Company

5.1.6. Flowers Foods

5.1.7. Aryzta AG

5.1.8. Hostess Brands, LLC

5.1.9. George Weston Limited

5.1.10. Rich Products Corporation

5.1.11. McKee Foods Corporation

5.1.12. JAB Holding Company

5.1.13. Finsbury Food Group

5.1.14. Weston Foods

5.1.15. Dawn Foods

5.2. Cross Comparison Parameters (Product Portfolio, Geographical Presence, Revenue, Production Capacity, Market Share, Innovation Strategies, Sustainability Initiatives, R&D Investments)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers & Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Food Safety Regulations

6.2. Nutritional Labeling Requirements

6.3. Compliance with Packaging and Sustainability Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Ingredient Type (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior Analysis

9.3. White Space Opportunity Analysis

9.4. Product Innovation Strategies

This phase involves the construction of a detailed ecosystem map of the North America Bakery Products Market. Comprehensive desk research is conducted using proprietary databases and secondary research sources to identify all relevant variables influencing market dynamics.

Historical data is analyzed to evaluate the bakery product markets penetration and revenue generation across key segments. This includes an in-depth assessment of consumer preferences, purchasing patterns, and product innovations.

Market hypotheses are developed and validated through consultations with industry experts, conducted via structured interviews. These interviews provide firsthand insights into market operations, key challenges, and growth opportunities.

The final phase includes direct engagements with manufacturers and industry stakeholders to corroborate findings and ensure the accuracy of the market data. The synthesis of research provides a comprehensive, validated analysis of the North America bakery products market.

The North America bakery products market is valued at USD 94 billion, driven by increasing consumer demand for convenience foods and the rising popularity of gluten-free and organic products.

Challenges in the North America bakery products market include fluctuating raw material prices such as wheat and sugar, strict health regulations concerning sugar and gluten, and increasing competition from private label brands.

Key players in the North America bakery products market include Grupo Bimbo, Mondelez International, General Mills, Flowers Foods, and Aryzta AG. These companies dominate due to their extensive product portfolios, global reach, and sustainability initiatives.

Growth drivers in the North America bakery products market include the increasing consumer demand for healthier products, such as gluten-free and organic options, as well as innovations in packaging that enhance product shelf life.

Supermarkets and hypermarkets dominate the distribution landscape, providing consumers with a wide variety of bakery products and benefiting from extensive foot traffic in urban and suburban areas in the North America bakery products market.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.