North America C-Arm Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD6714

December 2024

96

About the Report

North America C-Arm Market Overview

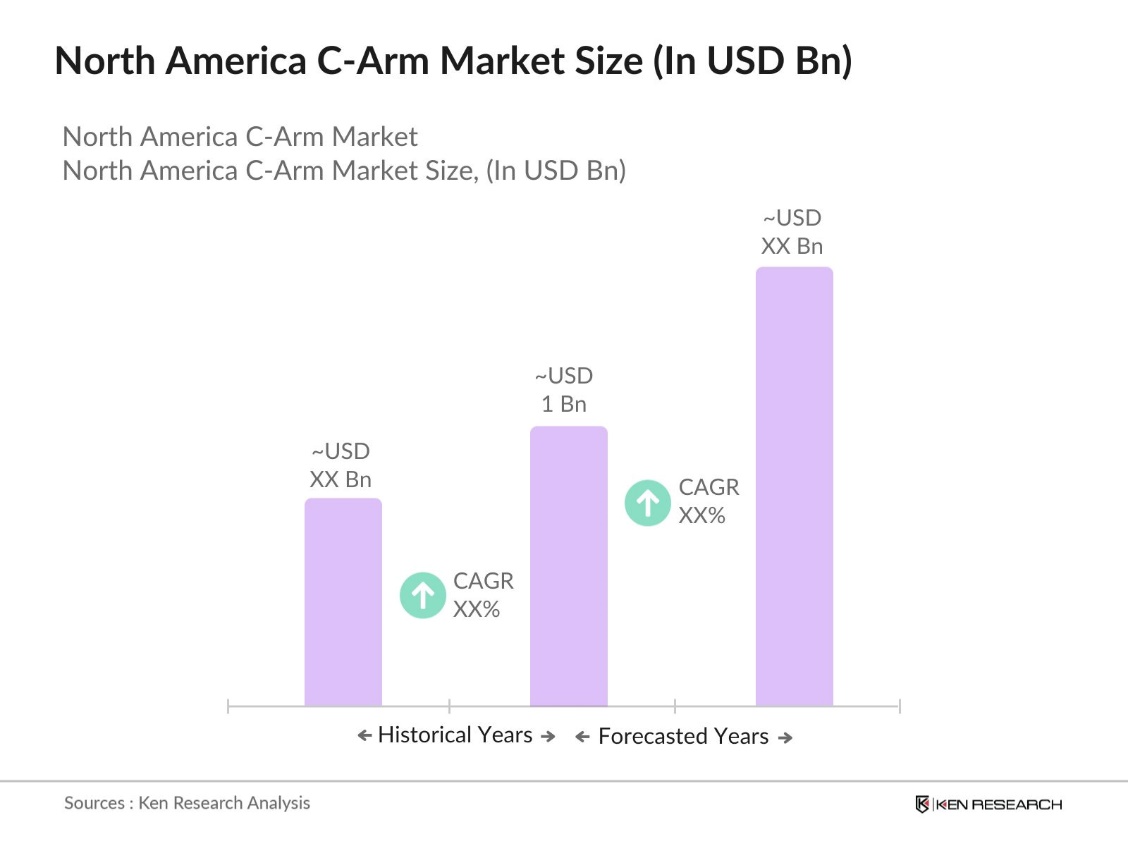

- The North America C-Arm Market is valued at USD 1 billion, driven by the increasing demand for advanced imaging technologies in healthcare facilities. Growth is primarily fueled by the rise in minimally invasive surgeries and the aging population, leading to higher incidences of chronic diseases such as cardiovascular and orthopedic conditions. The demand for C-Arms in surgical applications is continuously rising, supported by increasing investments in healthcare infrastructure and technology advancements in medical imaging devices, particularly in the U.S. and Canada.

- The United States dominates the North American C-Arm market due to its advanced healthcare infrastructure, high adoption of technologically advanced medical devices, and a robust healthcare reimbursement system. Additionally, the presence of leading global manufacturers and significant investment in R&D further solidifies the U.S.'s position as the market leader. Canada, with its universal healthcare system and increasing demand for portable C-Arms, is also a notable player in this market.

- The Medical Device Reporting (MDR) guidelines in North America require manufacturers and healthcare facilities to report adverse events related to medical devices, including C-Arms. In 2022, the FDA received over two million medical device reports related to suspected device-associated deaths, serious injuries, and malfunctions. These guidelines help monitor the safety and performance of C-Arms in clinical settings, ensuring that any malfunctions or issues are promptly addressed to prevent patient harm.

North America C-Arm Market Segmentation

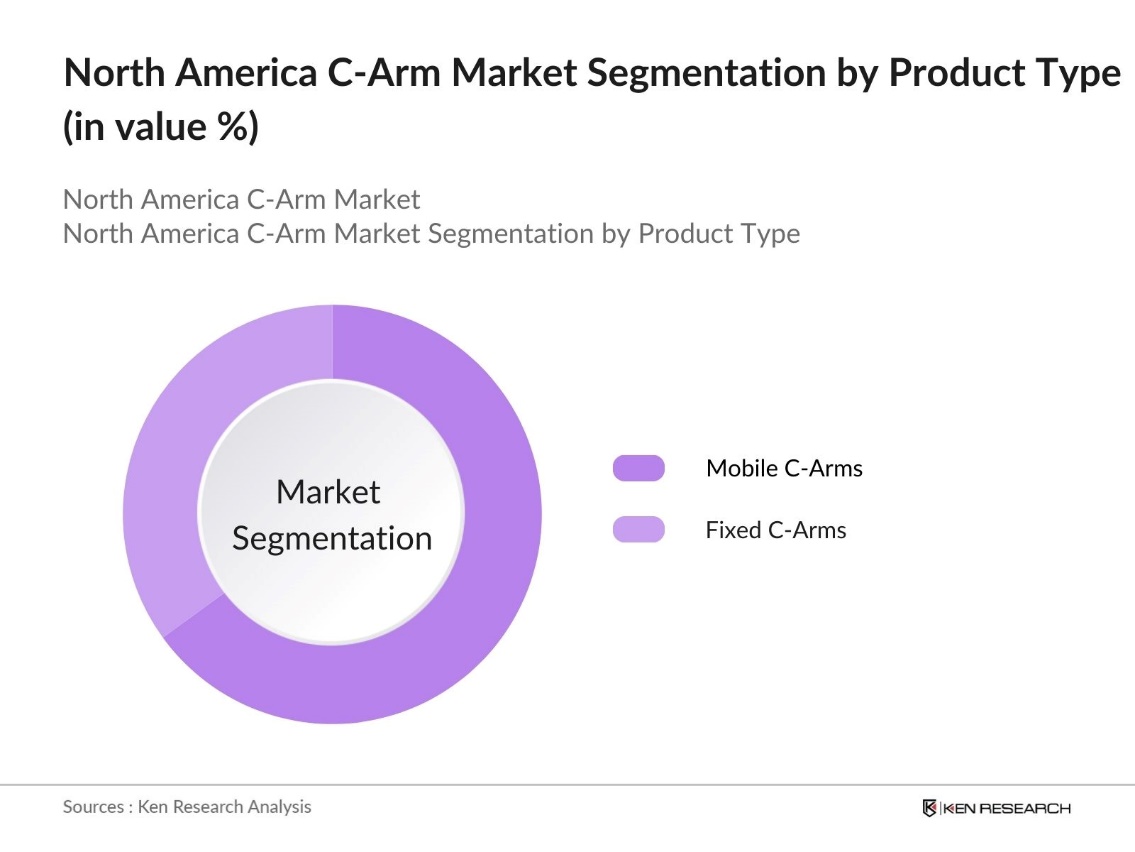

By Product Type: The North America C-Arm market is segmented by product type into mobile C-Arms and fixed C-Arms. Recently, mobile C-Arms have dominated the market due to their flexibility, ease of use, and cost-effectiveness in a variety of medical settings, such as ambulatory surgical centers and smaller hospitals. Mobile C-Arms are preferred for their portability, enabling healthcare providers to utilize them in different surgical environments, thereby increasing their utility across diverse healthcare applications.

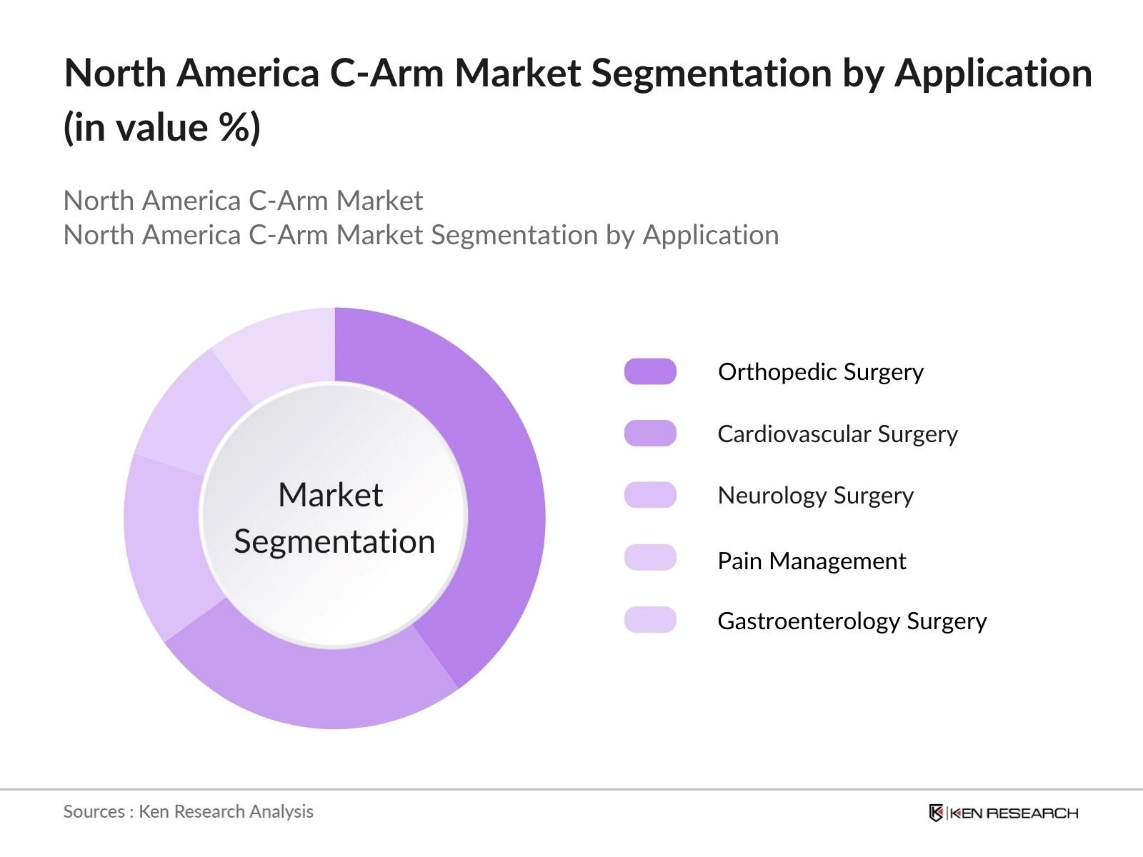

By Application: The North America C-Arm market is segmented by application into orthopedic surgery, cardiovascular surgery, neurology surgery, pain management, and gastroenterology surgery. Orthopedic surgery holds a significant share of the market, driven by the increasing number of trauma cases, sports injuries, and the aging population, which leads to more joint replacement and spinal surgeries. The precise imaging offered by C-Arms is crucial in ensuring successful outcomes in these surgeries, hence the dominance of this segment.

North America C-Arm Market Competitive Landscape

The market is dominated by a few major players, including global brands like GE Healthcare, Siemens Healthineers, and Philips Healthcare, which have established a significant presence through continuous innovation and strategic partnerships. Local manufacturers such as OrthoScan also play a crucial role, catering to the specialized needs of ambulatory surgical centers and clinics. This consolidation reflects the high entry barriers due to the significant capital investments and stringent regulatory approvals required in the medical device industry.

|

Company |

Year Established |

Headquarters |

R&D Investment |

Number of Employees |

Annual Revenue |

Market Presence |

Key Innovation |

|

GE Healthcare |

1892 |

Chicago, USA |

|||||

|

Siemens Healthineers |

1847 |

Erlangen, Germany |

|||||

|

Philips Healthcare |

1891 |

Amsterdam, Netherlands |

|||||

|

OrthoScan |

2002 |

Scottsdale, USA |

|||||

|

Canon Medical Systems |

1930 |

tawara, Japan |

North America C-Arm Industry Analysis

Growth Drivers

- Aging Population & Increasing Incidence of Chronic Diseases: North America has a growing elderly population, which increases demand for advanced healthcare equipment like C-Arm systems. According to the U.S. Census Bureau, 57.8 million adults aged 65 and older living in the U.S. in 2022. Chronic conditions like cardiovascular diseases and cancers are prevalent in older populations. The rise in these health conditions necessitates more imaging systems to support diagnosis and minimally invasive treatments.

- Technological Advancements in Imaging Systems: Technological advancements in C-Arm systems, such as the integration of digital imaging and 3D visualization, have enhanced their diagnostic accuracy. In 2023, the U.S. FDA approved several new C-Arm systems equipped with these capabilities, which have been instrumental in improving outcomes in complex surgeries. These advancements allow for better image clarity and lower radiation exposure for patients. The increased capabilities have prompted hospitals and surgical centers across North America to upgrade their existing imaging infrastructure, driving market growth.

- Rising Adoption of Minimally Invasive Procedures: Minimally invasive surgeries are gaining popularity due to their advantages, such as shorter recovery times and reduced complications. C-Arms are crucial in these procedures, offering real-time imaging that enhances the accuracy of surgical interventions. As healthcare providers look to improve patient outcomes and reduce recovery periods, the adoption of C-Arm systems in North America is increasing. These imaging systems enable precise guidance during surgeries, making them an integral part of the shift towards minimally invasive techniques in hospitals and surgical centers across the region.

Market Challenges

- High Costs Associated with C-Arm Devices: The high cost of advanced C-Arm systems poses a challenge for smaller hospitals and clinics in North America. These devices require a substantial financial investment, which limits their accessibility in certain healthcare facilities. In addition to the upfront cost, expenses related to maintenance, software updates, and staff training further increase the overall financial burden. As a result, smaller healthcare providers may find it difficult to adopt these advanced imaging systems, even though they offer significant benefits for improving patient care and surgical outcomes.

- Regulatory Compliance and Approval Delays: C-Arm devices in North America face rigorous regulatory approval processes, which can delay their availability in the market. These approvals, often governed by strict safety and quality standards, can take considerable time depending on the complexity of the technology. Such delays slow down the introduction of new and innovative C-Arm systems, hindering the adoption of the latest advancements in imaging technology within healthcare settings. This process creates challenges for manufacturers looking to introduce cutting-edge devices to hospitals and clinics swiftly.

North America C-Arm Market Future Outlook

The North America C-Arm market is expected to witness steady growth over the next few years, driven by continuous technological advancements and the rising demand for minimally invasive surgeries. Healthcare facilities are increasingly adopting mobile C-Arms due to their flexibility and ease of integration into various surgical environments. Moreover, the introduction of artificial intelligence (AI) in imaging systems and the development of hybrid operating rooms are likely to further propel the demand for C-Arms in both hospitals and ambulatory surgical centers.

Market Opportunities

- High Costs Associated with C-Arm Devices: The high cost of advanced C-Arm systems poses a challenge for smaller hospitals and clinics in North America. These devices require a substantial financial investment, which limits their accessibility in certain healthcare facilities. In addition to the upfront cost, expenses related to maintenance, software updates, and staff training further increase the overall financial burden. As a result, smaller healthcare providers may find it difficult to adopt these advanced imaging systems, even though they offer significant benefits for improving patient care and surgical outcomes.

- Regulatory Compliance and Approval Delays: C-Arm devices in North America face rigorous regulatory approval processes, which can delay their availability in the market. These approvals, often governed by strict safety and quality standards, can take considerable time depending on the complexity of the technology. Such delays slow down the introduction of new and innovative C-Arm systems, hindering the adoption of the latest advancements in imaging technology within healthcare settings. This process creates challenges for manufacturers looking to introduce cutting-edge devices to hospitals and clinics swiftly.

Scope of the Report

|

By Product Type |

Mobile C-Arms Fixed C-Arms |

|

By Technology |

2D C-Arms 3D C-Arms |

|

By Application |

Orthopedic Surgery Cardiovascular Surgery Neurology Surgery Pain Management Gastroenterology Surgery |

|

By End-User |

Hospitals Ambulatory Surgical Centers Specialty Clinics |

|

By Region |

United States Canada Mexico |

Products

Key Target Audience

Healthcare Providers

Medical Device Manufacturers

Telemedicine and Remote Diagnostic Companies

Ambulatory Surgical Centers

Medical Device Importers and Exporters

Regulatory and Government Bodies (FDA, Health Canada)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

GE Healthcare

Siemens Healthineers

Philips Healthcare

Canon Medical Systems

OrthoScan

Ziehm Imaging

Shimadzu Corporation

Hologic, Inc.

Hitachi Medical

Agfa Healthcare

Table of Contents

1. North America C-Arm Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America C-Arm Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America C-Arm Market Analysis

3.1. Growth Drivers

3.1.1. Aging Population & Increasing Incidence of Chronic Diseases

3.1.2. Rising Adoption of Minimally Invasive

3.1.3. Technological Advancements in Imaging Systems

3.1.4. Increasing Government Initiatives for Healthcare Infrastructure

3.2. Market Challenges

3.2.1. High Costs Associated with C-Arm Devices

3.2.2. Regulatory Compliance and Approval Delays

3.2.3. Shortage of Skilled Professionals for C-Arm Operations

3.3. Opportunities

3.3.1. Expansion of Mobile C-Arms

3.3.2. Growth in Ambulatory Surgical Centers

3.3.3. Strategic Collaborations Between OEMs and Hospitals

3.4. Trends

3.4.1. Integration with AI-Based Imaging

3.4.2. Use of Hybrid Operating Rooms

3.4.3. Development of Flat Panel Detectors in C-Arms

3.5. Regulatory Framework

3.5.1. FDA Regulations on Medical Imaging Devices

3.5.2. North American Medical Device Reporting Guidelines

3.5.3. Healthcare Compliance Standards for Imaging Systems

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.7.1. OEM Manufacturers

3.7.2. Healthcare Institutions

3.7.3. Insurance Providers

3.8. Porters Five Forces

3.9. Competitive Ecosystem

4. North America C-Arm Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Mobile C-Arms

4.1.2. Fixed C-Arms

4.2. By Technology (In Value %)

4.2.1. 2D C-Arms

4.2.2. 3D C-Arms

4.3. By Application (In Value %)

4.3.1. Orthopedic Surgery

4.3.2. Cardiovascular Surgery

4.3.3. Neurology Surgery

4.3.4. Pain Management

4.3.5. Gastroenterology Surgery

4.4. By End-User (In Value %)

4.4.1. Hospitals

4.4.2. Ambulatory Surgical Centers

4.4.3. Specialty Clinics

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America C-Arm Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. GE Healthcare

5.1.2. Siemens Healthineers

5.1.3. Philips Healthcare

5.1.4. Canon Medical Systems

5.1.5. Ziehm Imaging

5.1.6. Shimadzu Corporation

5.1.7. Hologic, Inc.

5.1.8. OrthoScan Inc.

5.1.9. Eurocolumbus

5.1.10. Genoray Co. Ltd.

5.1.11. Allengers Medical Systems

5.1.12. DMS Group

5.1.13. EcoRay Co. Ltd.

5.1.14. Hitachi Medical

5.1.15. Agfa Healthcare

5.2 Cross Comparison Parameters (Headquarters, Revenue, No. of Employees, Installed Base, Market Share, R&D Investment, Manufacturing Facilities, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America C-Arm Market Regulatory Framework

6.1. Medical Device Regulations in North America

6.2. FDA Medical Device Approval Process

6.3. Compliance and Safety Standards

7. North America C-Arm Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America C-Arm Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Technology (In Value %)

8.3. By Application (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9. North America C-Arm Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first phase involves mapping out the C-Arm market ecosystem in North America. This includes stakeholders such as healthcare providers, manufacturers, and regulatory bodies. Data from secondary sources like government reports and proprietary databases help in defining the core market drivers, challenges, and opportunities.

Step 2: Market Analysis and Construction

Historical data analysis is performed to understand the market dynamics, including the penetration of mobile and fixed C-Arms, revenue generated, and market segmentation. In addition, service quality statistics are assessed to ensure reliability in estimating the market size and growth.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are tested and validated through consultations with industry experts. These consultations offer insights into product innovations, sales trends, and operational efficiency, which help refine market projections.

Step 4: Research Synthesis and Final Output

The final stage involves synthesizing the research with feedback from healthcare providers and manufacturers. This ensures the market insights are accurate, validated, and reflective of the actual market conditions. The final report includes detailed analysis and expert recommendations.

Frequently Asked Questions

01 How big is the North America C-Arm Market?

The North America C-Arm Market is valued at USD 1 billion, driven by the rising demand for minimally invasive surgeries and advancements in medical imaging technology.

02 What are the challenges in the North America C-Arm Market?

Challenges in North America C-Arm Market include the high costs associated with C-Arm devices, regulatory approval delays, and the shortage of skilled professionals to operate the devices efficiently.

03 Who are the major players in the North America C-Arm Market?

Major players in the North America C-Arm Market include GE Healthcare, Siemens Healthineers, Philips Healthcare, and Canon Medical Systems. These companies dominate the market due to their strong brand presence and advanced technology offerings.

04 What are the growth drivers of the North America C-Arm Market?

The North America C-Arm Market is propelled by factors such as the increasing number of surgeries, advancements in imaging technology, and the growing aging population, which leads to a higher incidence of chronic diseases requiring surgical interventions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.