North America Carbon Capture and Storage Market Outlook to 2030

Region:North America

Author(s):Mukul

Product Code:KROD3140

October 2024

88

About the Report

North America Carbon Capture and Storage Market Overview

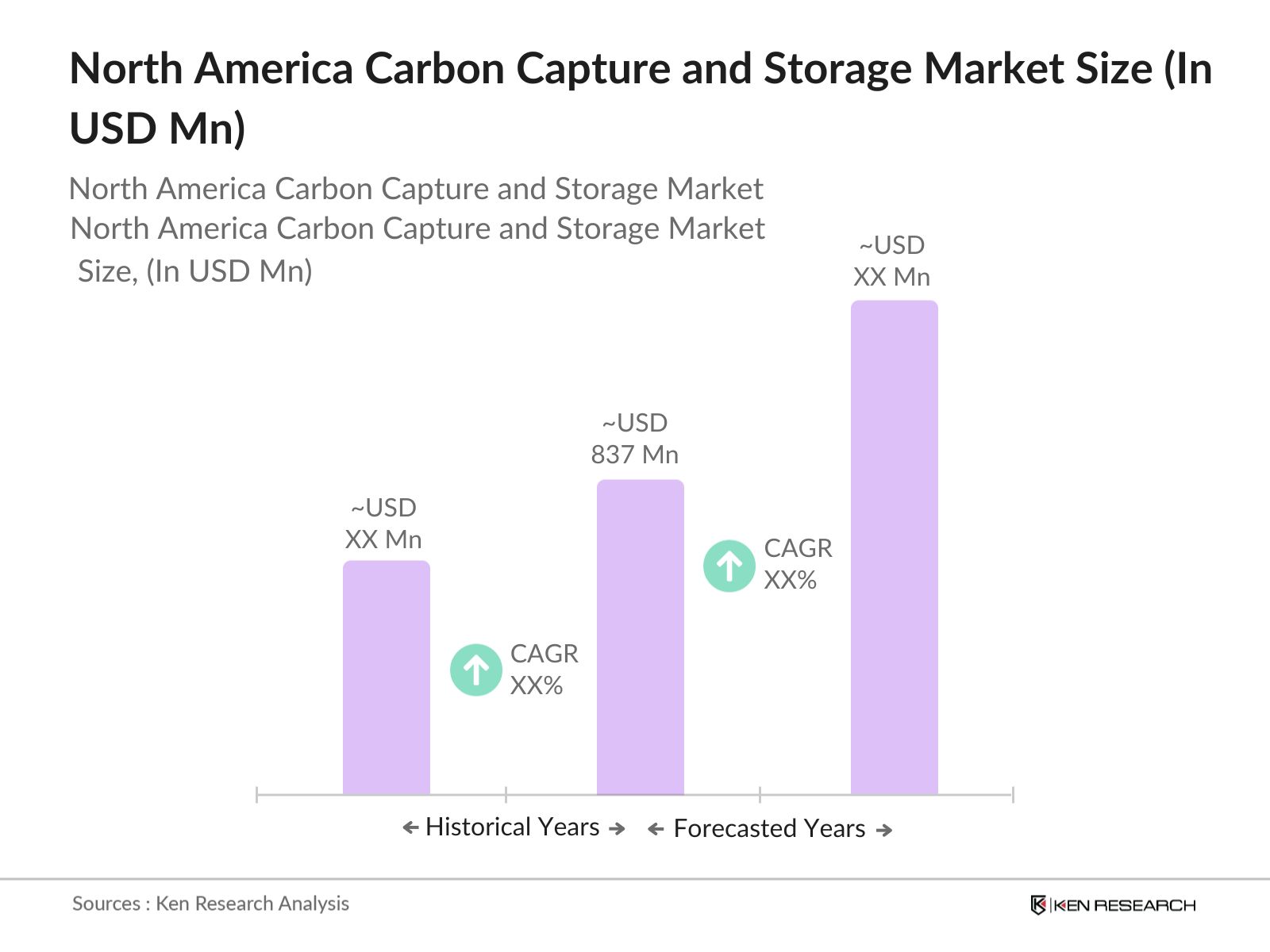

- The North America Carbon Capture and Storage (CCS) market is valued at USD 837 million, driven primarily by the countrys strong regulatory support for reducing carbon emissions, coupled with growing corporate interest in sustainability. Government incentives, such as the 45Q tax credit, have played a crucial role in accelerating CCS project deployment across various sectors, including energy and heavy industries. The deployment of CCS is further bolstered by advancements in carbon capture technology and the increasing demand for CO mitigation solutions in industries like cement and steel production.

- The North America dominates the CCS market, with cities such as Houston, Texas, and Sacramento, California, leading the charge in CCS project deployment. Houston, known as the "Energy Capital of the World," houses numerous CCS projects due to its proximity to oil and gas industries and geological formations suited for CO storage. Similarly, Sacramentos push toward zero-emission energy solutions and support from Californias Low Carbon Fuel Standard makes it a focal point for CCS advancements. These regions industrial activities and government-backed initiatives create a favorable environment for large-scale CCS projects.

- he U.S. federal government and several state governments have implemented policies to promote CCS deployment. The Bipartisan Infrastructure Law of 2021 allocated $3.5 billion towards CCS projects, while the 2022 Inflation Reduction Act extended tax credits for carbon capture under Section 45Q, offering $85 per metric ton of captured CO2. In addition, states like California have established their own regulations, including the Low Carbon Fuel Standard, which incentivizes carbon capture in industries. These policies are pivotal for accelerating CCS projects across the country.

North America Carbon Capture and Storage Market Segmentation

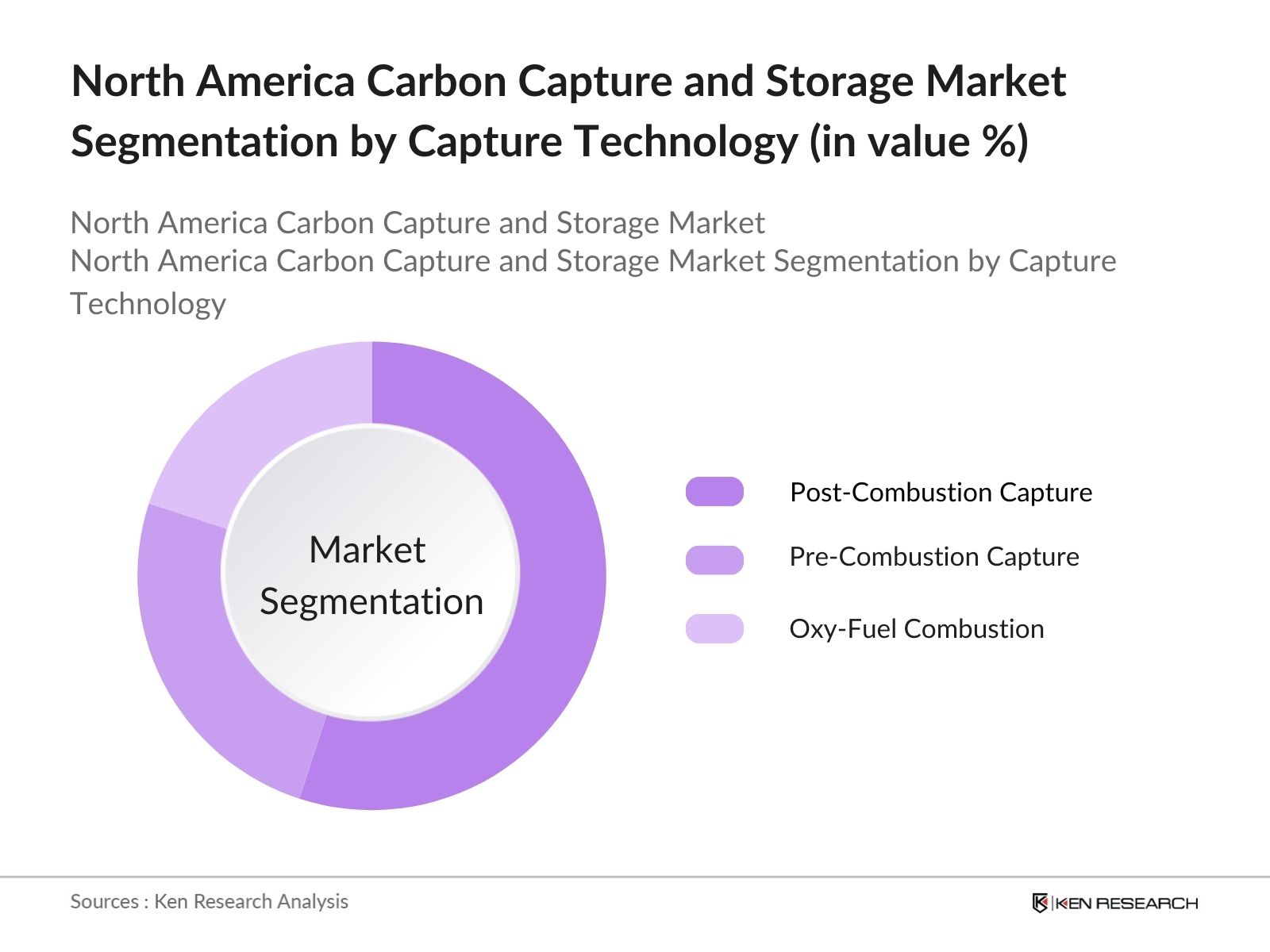

- By Capture Technology: The North America CCS market is segmented by capture technology into post-combustion capture, pre-combustion capture, and oxy-fuel combustion. Post-combustion capture holds the largest share due to its versatility and ability to retrofit existing power plants and industrial facilities without requiring major modifications. This technology is also well-suited for power plants using fossil fuels, where emissions are captured after the combustion process, contributing to its dominance in the market.

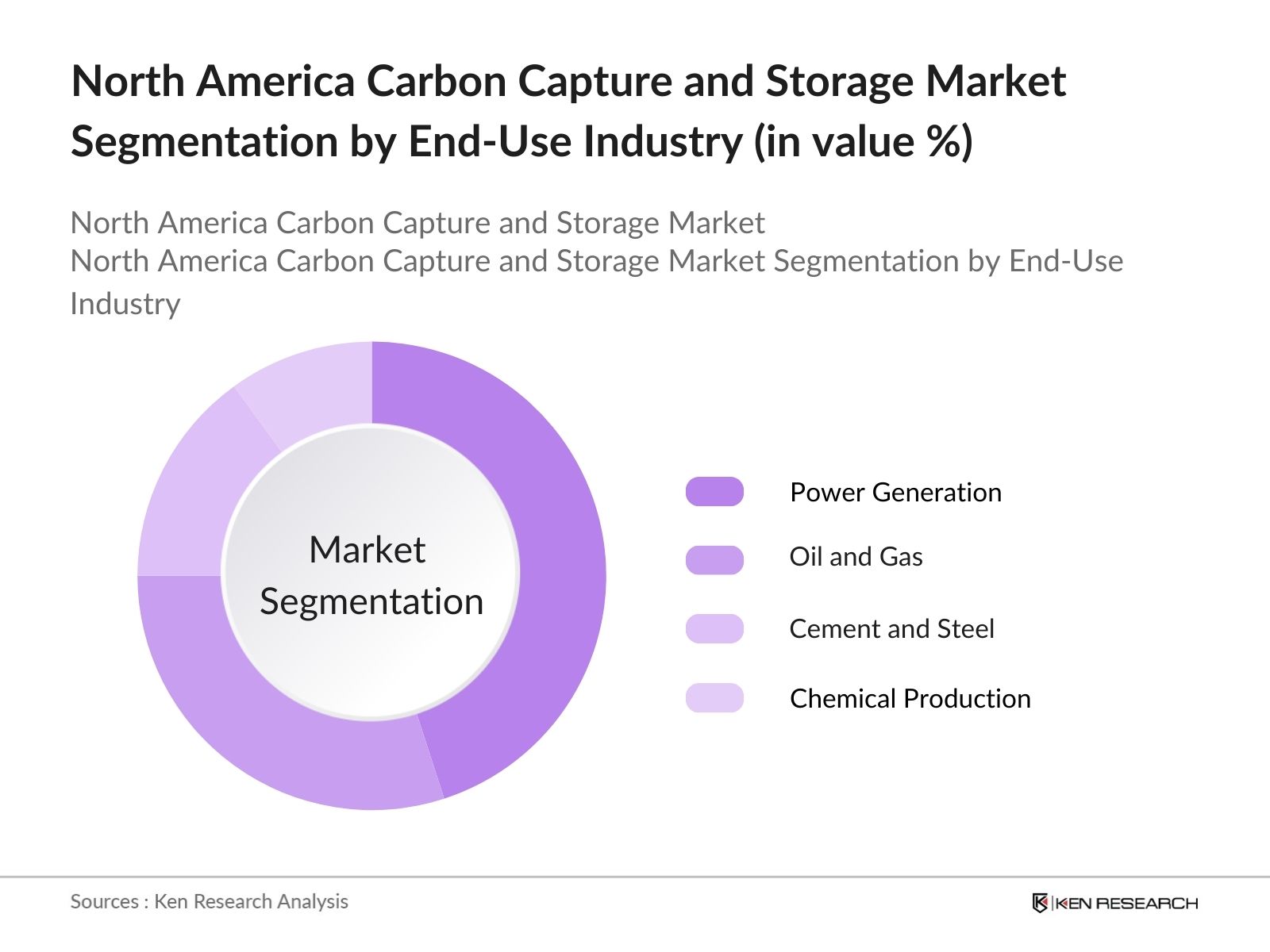

- By End-Use Industry: The North America CCS market is further segmented by end-use industry into power generation, oil and gas, cement and steel, and chemical production. Power generation dominates due to the high carbon emissions from coal and natural gas power plants, which account for a significant portion of the country's greenhouse gas emissions. The NORTH AMERICA's reliance on fossil fuels for electricity generation has driven the demand for CCS to meet emissions reduction goals, positioning power generation as the leading end-use industry.

North America Carbon Capture and Storage Market Competitive Landscape

The North America CCS market is dominated by major players, including a mix of traditional oil and gas companies and technology innovators. These companies have established themselves through extensive investment in CCS projects, partnerships with government bodies, and advancements in capture and storage technologies. The competitive landscape features both large-scale industrial players and smaller technology-focused firms working on innovative solutions for CO capture and utilization.

|

Company |

Establishment Year |

Headquarters |

CO Captured (Mt) |

CCS Projects |

Revenue from CCS |

R&D Investments |

Strategic Partnerships |

Government Collaborations |

|

ExxonMobil |

1870 |

Texas, NORTH AMERICA |

||||||

|

Chevron |

1879 |

California, NORTH AMERICA |

||||||

|

Shell |

1907 |

Texas, NORTH AMERICA |

||||||

|

BP |

1909 |

London, UK |

||||||

|

Climeworks |

2009 |

Zurich, Switzerland |

North America Carbon Capture and Storage Industry Analysis

North America Carbon Capture and Storage Market Growth Drivers

- Climate Change Mitigation Policies: The NORTH AMERICA's commitment to addressing climate change is anchored in its policies focused on achieving carbon neutrality by mid-century. The federal government aims to reduce carbon emissions by over 50% below 2005 levels by 2030, driven by the Biden administration's rejoining of the Paris Agreement. Several states, including California, have also set ambitious targets. As of 2023, the U.S. Environmental Protection Agency (EPA) estimates that CO2 emissions from fossil fuel combustion accounted for approximately 5,000 million metric tons annually, necessitating large-scale CCS projects to meet reduction targets.

- Increasing Carbon Emission Reduction Targets: The U.S. has been increasing its carbon reduction goals, aligning with the Paris Agreement's aim to limit global temperature rise. Under the 2022 US federal climate policies, carbon emissions reduction has been prioritized with federal incentives to cut emissions by 50-52% by 2030. In 2023, the U.S. emitted around 4.9 billion metric tons of CO2, necessitating stronger policies across industries, especially in energy-intensive sectors. The targets demand the implementation of carbon capture and storage, with projections to capture millions of metric tons annually across the cement and steel sectors.

- Industry Adoption: The adoption of CCS technology by industries like cement, steel, and power generation is critical for meeting the U.S. climate goals. In 2022, the cement industry alone accounted for 7% of global CO2 emissions, with the U.S. contributing significantly. Major industries like fossil fuels are initiating CCS projects to align with regulatory frameworks, capturing an estimated 45 million metric tons of CO2 by 2024. The power generation sector is also advancing towards large-scale adoption, aiming to sequester 60 million metric tons of CO2 annually by 2025.

North America Carbon Capture and Storage Market Restraints

- High Initial Infrastructure Cost: The high capital expenditure required for CCS infrastructure development remains a significant challenge. According to the U.S. Department of Energy, the average cost of constructing a large-scale CCS facility ranges from $500 million to $1 billion, depending on location and technology. Despite government incentives, the funding gap for full-scale implementation is a bottleneck, with only 12 CCS projects operational in 2023. The lack of sufficient financial resources and high operating costs, especially for industries like steel and cement, remains a critical barrier to broader adoption.

- Regulatory Barriers: The regulatory landscape surrounding CCS implementation in the U.S. is complex and fragmented, with long permit approval processes and potential legal liabilities slowing down project development. The Environmental Protection Agency (EPA) and other bodies require extensive environmental impact assessments, which can delay projects by up to 5 years. Legal issues surrounding liability for long-term CO2 storage also create uncertainty for companies, contributing to only 25% of proposed projects moving beyond the approval stage. This challenge is compounded by varying state regulations, particularly in oil-producing states like Texas.

North America Carbon Capture and Storage Market Future Outlook

Over the next five years, the NORTH AMERICA CCS market is expected to witness significant growth driven by regulatory pressures to reduce carbon emissions and advancements in CCS technology. The expansion of federal and state-level tax credits and grants, such as the 45Q tax credit and Californias Low Carbon Fuel Standard, is expected to increase investment in CCS projects across various industrial sectors. Additionally, increasing corporate sustainability commitments and public-private partnerships are poised to accelerate the commercialization of CCS technology, fostering further market expansion.

Market Opportunities

- International Collaborations: International collaborations provide a pathway for expanding CCS technologies. In 2023, the U.S. joined the Carbon Capture Utilization and Storage (CCUS) alliance, which aims to facilitate knowledge exchange and funding opportunities between countries. This collaboration enables the U.S. to access global funding initiatives, contributing to an additional $500 million in investments for CCS infrastructure. Countries like Norway and the U.K. have already committed significant funds for joint CCS research and projects, positioning the U.S. to benefit from these partnerships, especially in high-emission sectors like petrochemicals.

- Technological Innovation: The U.S. has seen a surge in innovation surrounding low-cost carbon capture technologies. For instance, research funded by the U.S. Department of Energy in 2023 has led to the development of membranes capable of capturing 90% of emissions from industrial plants. Furthermore, hydrogen integration with CCS is a promising avenue, as the Hydrogen Energy Earthshot program aims to reduce the cost of clean hydrogen production to $1 per kilogram by 2030. These technological innovations are poised to make carbon capture more cost-effective and scalable for high-emission industries.

Scope of the Report

|

Capture Technology |

Post-Combustion Capture Pre-Combustion Capture Oxy-Fuel Combustion |

|

End-Use Industry |

Power Generation Oil and Gas Industry Cement and Steel Chemical Production |

|

Storage Method |

Geological Storage Enhanced Oil Recovery (EOR) Mineralization |

|

Project Type |

Large-Scale CCS Projects Pilot and Demonstration Projects Commercialized CCS Projects |

|

Region |

North America Europe Asia-Pacific Middle East and Africa South America |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Power Generation Companies

Oil and Gas Companies

Cement and Steel Manufacturers

Chemical Production Companies

CCS Technology Providers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (U.S. Department of Energy, U.S. Environmental Protection Agency)

Environmental and Energy Policy Advocacy Groups

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

ExxonMobil

Chevron

Shell

BP

Climeworks

TotalEnergies

Aker Solutions

Linde

Fluor Corporation

Mitsubishi Heavy Industries

Air Products and Chemicals

Schlumberger

Baker Hughes

Hitachi Zosen

Siemens Energy

Table of Contents

North America Carbon Capture and Storage Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (CCS deployment, CO storage capacity, CCS project deployment, and emission targets)

1.4. Market Segmentation Overview

North America Carbon Capture and Storage Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (CCS project expansions, technological innovations, major policy announcements)

North America Carbon Capture and Storage Market Analysis

3.1. Growth Drivers

3.1.1. Climate Change Mitigation Policies

3.1.2. Increasing Carbon Emission Reduction Targets (Paris Agreement, US Federal Climate Policies)

3.1.3. Industry Adoption (Fossil Fuel Industry, Cement and Steel, Power Generation)

3.1.4. Technological Advancements (Direct Air Capture, Enhanced Oil Recovery)

3.2. Market Challenges

3.2.1. High Initial Infrastructure Cost

3.2.2. Regulatory Barriers (Permit Approval Process, Legal Liabilities)

3.2.3. Public and Political Opposition (Environmental Concerns, Stakeholder Pushback)

3.3. Opportunities

3.3.1. International Collaborations (CCS Alliances, Global Funding Initiatives)

3.3.2. Technological Innovation (Lower-Cost Capture Technologies, Hydrogen Integration)

3.3.3. Expansion into High-Emission Sectors (Petrochemical, Heavy Industries)

3.4. Trends

3.4.1. Private-Sector Investment (Venture Capital in CCS, Corporate Carbon Commitments)

3.4.2. Carbon Trading and Pricing Mechanisms

3.4.3. Integration with Clean Energy Solutions (Renewable Hydrogen, Energy Storage)

3.5. Government Regulation

3.5.1. US Federal and State-Level CCS Policies

3.5.2. Tax Incentives and Carbon Pricing (45Q Tax Credit, Regional Greenhouse Gas Initiative)

3.5.3. Environmental Impact Assessments and Safety Standards

3.5.4. Funding Support for CCS Infrastructure Development

3.6. SWOT Analysis (Market-specific strengths, weaknesses, opportunities, threats related to CCS)

3.7. Stakeholder Ecosystem (Public, private, and third-party CCS project stakeholders)

3.8. Porters Five Forces Analysis (Bargaining power of suppliers and buyers, threat of substitutes, industry competition)

3.9. Competition Ecosystem

North America Carbon Capture and Storage Market Segmentation

4.1. By Capture Technology (In Value %)

4.1.1. Post-Combustion Capture

4.1.2. Pre-Combustion Capture

4.1.3. Oxy-Fuel Combustion

4.2. By End-Use Industry (In Value %)

4.2.1. Power Generation

4.2.2. Oil and Gas Industry

4.2.3. Cement and Steel

4.2.4. Chemical Production

4.3. By Storage Method (In Value %)

4.3.1. Geological Storage

4.3.2. Enhanced Oil Recovery (EOR)

4.3.3. Mineralization

4.4. By Project Type (In Value %)

4.4.1. Large-Scale CCS Projects

4.4.2. Pilot and Demonstration Projects

4.4.3. Commercialized CCS Projects

4.5. By Region (In Value %)

4.5.1. North America (NORTH AMERICA focus)

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East and Africa

4.5.5. South America

North America Carbon Capture and Storage Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. ExxonMobil

5.1.2. Shell

5.1.3. Chevron

5.1.4. TotalEnergies

5.1.5. BP

5.1.6. Equinor

5.1.7. Schlumberger

5.1.8. Linde

5.1.9. Air Products and Chemicals

5.1.10. Mitsubishi Heavy Industries

5.1.11. Fluor Corporation

5.1.12. Aker Solutions

5.1.13. Baker Hughes

5.1.14. Hitachi Zosen

5.1.15. Climeworks

5.2. Cross Comparison Parameters (CCS project pipeline, CO captured in Mt, technological capabilities, geographical focus, revenue from CCS operations, research initiatives, alliances/partnerships, government collaborations)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, CCS deployments, Mergers & Acquisitions)

5.5. Investment Analysis (CCS investments from oil and gas majors, venture capital, and private equity)

5.6. Government Grants and Incentives (Federal CCS funding programs, regional support initiatives)

North America Carbon Capture and Storage Market Regulatory Framework

6.1. Compliance and Certification Processes (CCS operational permits, environmental compliance)

6.2. Regulatory Policies and Standards (CO storage standards, CCS liability regulations)

6.3. Environmental Impact and Risk Management (Safety protocols, carbon storage risks, leakage prevention measures)

North America Carbon Capture and Storage Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

North America Carbon Capture and Storage Future Market Segmentation

8.1. By Capture Technology (In Value %)

8.2. By End-Use Industry (In Value %)

8.3. By Storage Method (In Value %)

8.4. By Project Type (In Value %)

8.5. By Region (In Value %)

North America Carbon Capture and Storage Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis (Total Available Market, Serviceable Available Market, Serviceable Obtainable Market)

9.2. Customer Cohort Analysis (CCS stakeholders, private investors, and public sector collaboration)

9.3. White Space Opportunity Analysis (Untapped CCS applications and regional expansions)

Research Methodology

Step 1: Identification of Key Variables

The first step in the research process involves mapping the CCS market ecosystem, focusing on key variables such as technological advancements, regulatory policies, and CO storage capacity. This stage relies on extensive desk research from government reports, CCS industry publications, and proprietary databases to identify the factors that drive the market.

Step 2: Market Analysis and Construction

In this phase, historical data from CCS projects in the NORTH AMERICA is compiled and analyzed, including the number of operational CCS facilities and their total CO capture capacity. The data is then cross-referenced with market revenue to estimate market penetration and project growth trajectories.

Step 3: Hypothesis Validation and Expert Consultation

The research hypotheses are validated through expert consultations with key players in the CCS sector. Interviews are conducted with industry professionals to assess market dynamics, confirm operational data, and provide qualitative insights into future market trends.

Step 4: Research Synthesis and Final Output

The final stage involves synthesizing all gathered data, including primary interviews, secondary research, and market analysis, to produce a comprehensive market report. The report is validated using a bottom-up approach to ensure accuracy in market size estimation and future outlook projections.

Frequently Asked Questions

1.How big is the North America Carbon Capture and Storage Market?

The North America CCS market is valued at USD 837 million, driven by a growing need to reduce carbon emissions and stringent government regulations aimed at meeting climate goals.

2.What are the growth drivers of the North America Carbon Capture and Storage Market?

Growth drivers include regulatory incentives like the 45Q tax credit, advancements in CCS technology, and increasing demand from industries looking to reduce their carbon footprint.

3.Who are the major players in the North America Carbon Capture and Storage Market?

Key players in the North America CCS market include ExxonMobil, Chevron, Shell, BP, and Climeworks, each of which has made significant investments in CCS technology and project deployment.

4.What are the challenges in the North America Carbon Capture and Storage Market?

Challenges include high upfront infrastructure costs, regulatory barriers, and public opposition to large-scale CCS projects due to environmental concerns and safety risks.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.