North America Carbon Fiber Market Outlook to 2030

Region:North America

Author(s):Mukul

Product Code:KROD2265

October 2024

95

About the Report

North America Carbon Fiber Market Overview

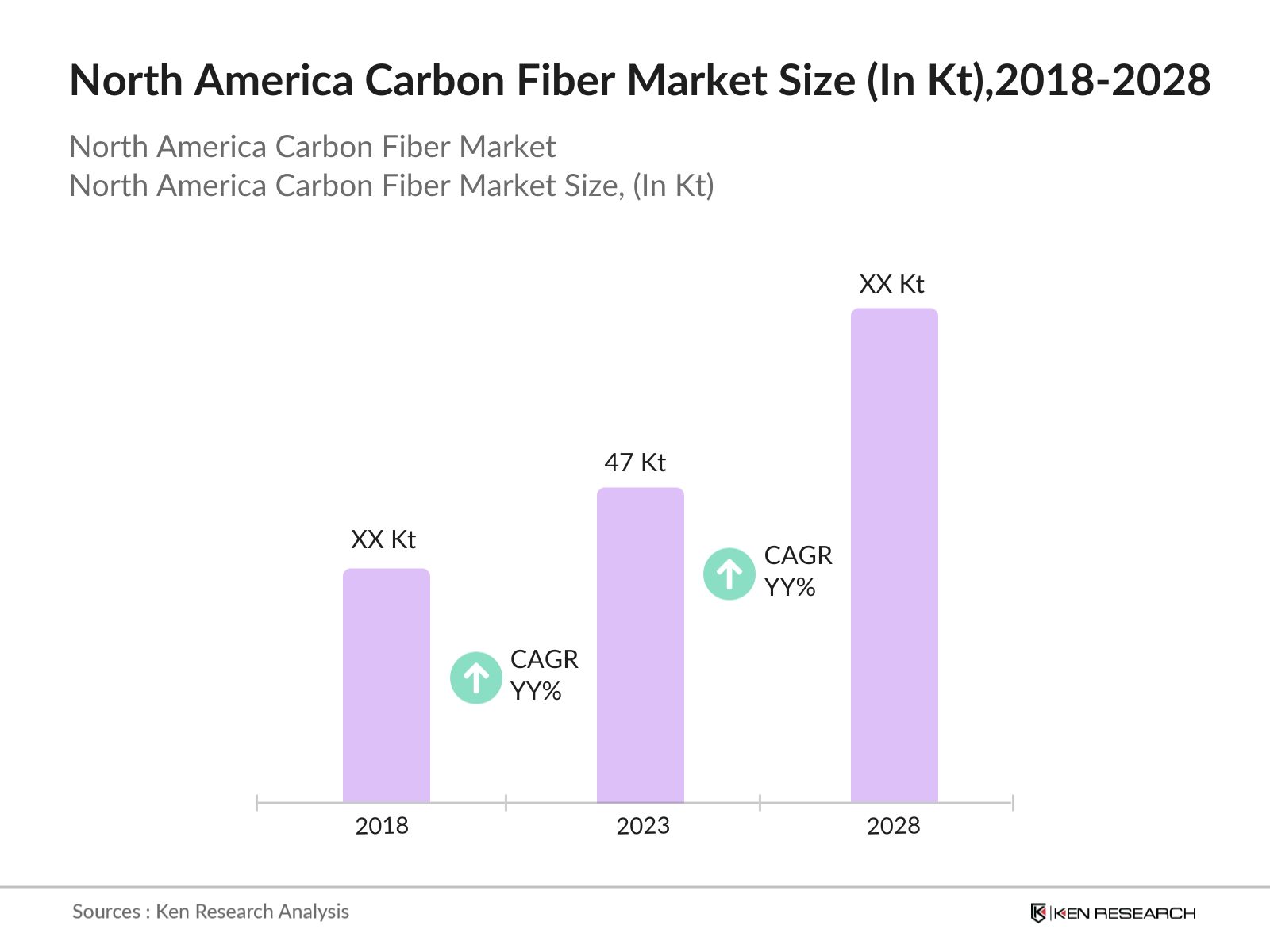

- The North America Carbon Fiber Market was valued at 47 kilotons in 2023, driven by the rising demand across industries like aerospace, automotive, and renewable energy. The increasing need for lightweight, durable materials to enhance fuel efficiency and reduce emissions has contributed significantly to the market's growth.

- Some of the leading players in the North America Carbon Fiber Market include Hexcel Corporation, Toray Industries, Mitsubishi Chemical Holdings, SGL Carbon, and Teijin Limited. These companies have established significant market share through continuous investments in research and development, innovative product offerings, and mergers and acquisitions aimed at expanding their production capacities.

- The cities that dominate the North America Carbon Fiber Market include Los Angeles, Seattle, and Detroit. Los Angeles is home to a significant aerospace industry presence, including companies like Boeing and Northrop Grumman, which drive carbon fiber demand. Seattle's dominance is due to the headquarters of Boeing, a key player in aerospace manufacturing. Detroit remains a hub for the automotive sector

- In 2023, Mitsubishi Chemical Holdings announced a USD 300 million expansion of its U.S. production facilities to meet growing demand for carbon fiber in electric vehicles. This move reflects the increased importance of carbon fiber in meeting sustainability goals across industries, particularly as the U.S. transitions to clean energy.

North America Carbon Fiber Market Segmentation

-

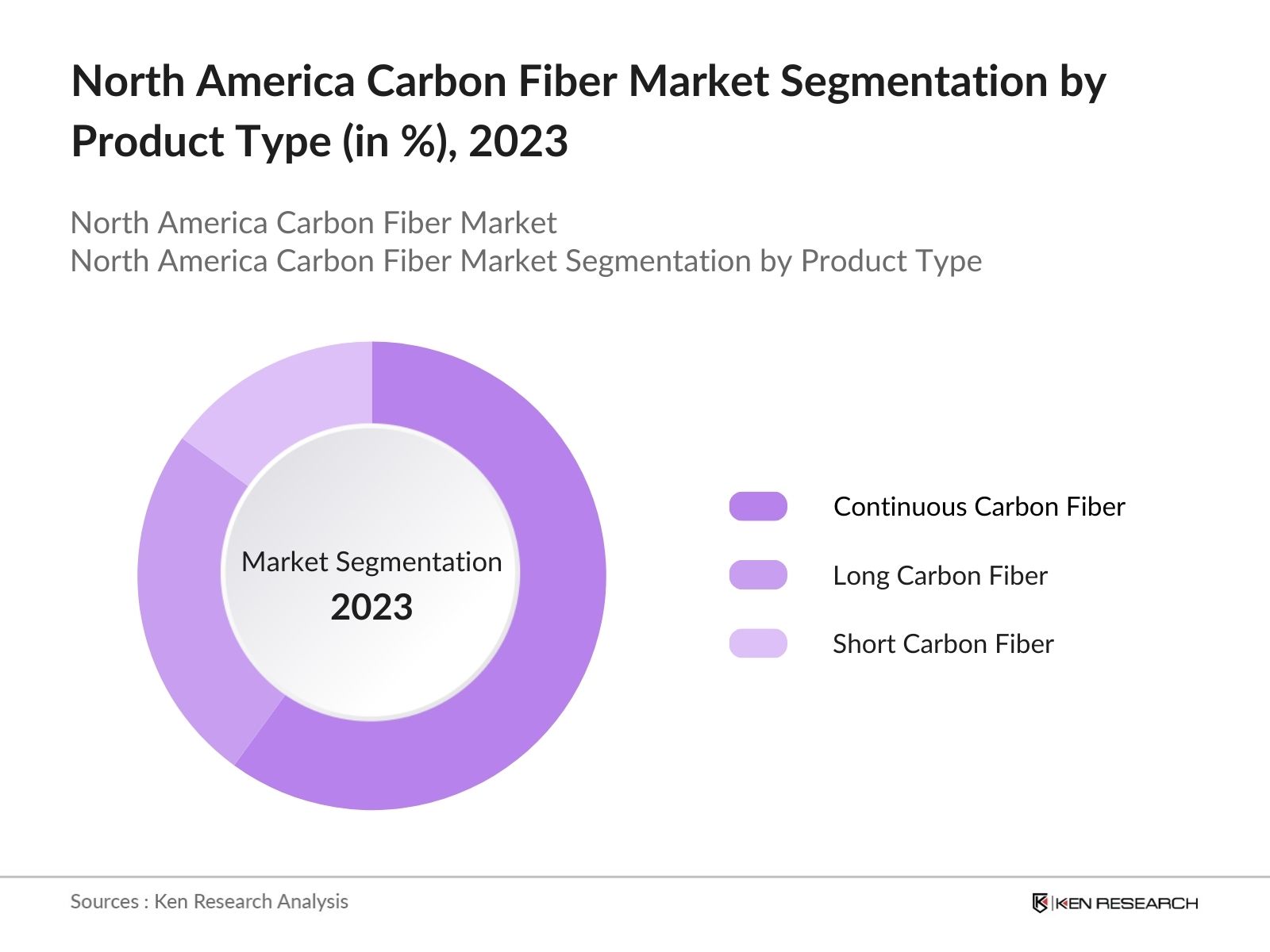

By Product Type: The North America Carbon Fiber Market is segmented by product type into Continuous Carbon Fiber, Long Carbon Fiber, and Short Carbon Fiber. In 2023, Continuous Carbon Fiber dominated the market due to its extensive use in the aerospace and automotive industries. Its high tensile strength and flexibility make it a preferred choice for manufacturers requiring high-performance materials.

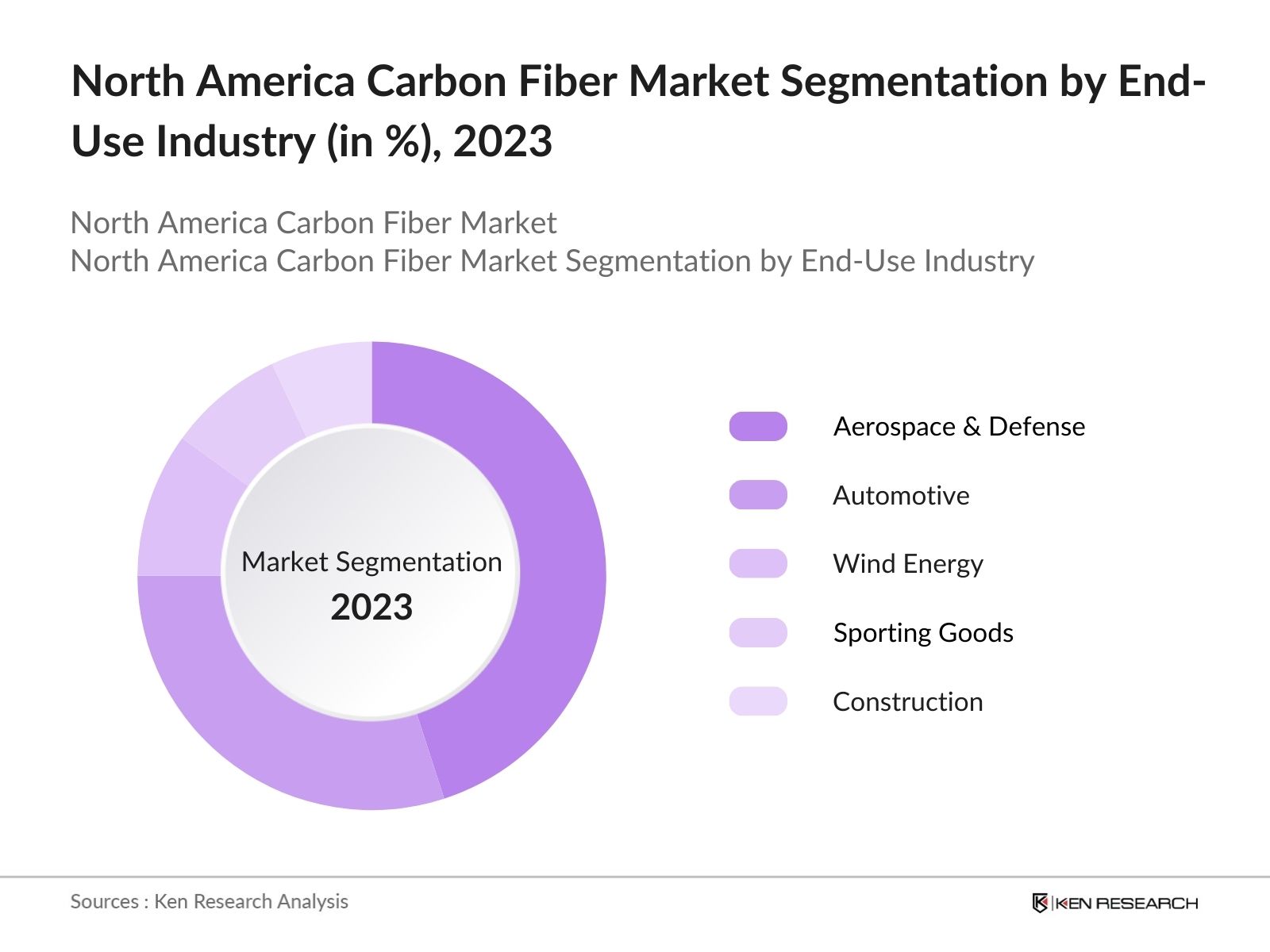

- By End-Use Industry: The North America Carbon Fiber Market is segmented by end-use industry into Aerospace & Defense, Automotive, Wind Energy, Sporting Goods, and Construction. Aerospace & Defense dominated the market in 2023, driven by the increasing demand for lightweight materials to enhance fuel efficiency and reduce emissions in aircraft and defense vehicles.

- By Region: The North America Carbon Fiber Market is segmented by region into the United States and Canada. The United States dominated the market in 2023 due to its advanced automotive and aerospace industries, where carbon fiber is increasingly used to meet fuel efficiency and performance requirements.

North America Carbon Fiber Market Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|

Hexcel Corporation |

1948 |

Stamford, CT, USA |

|

Toray Industries |

1926 |

Tokyo, Japan |

|

Mitsubishi Chemical Holdings |

1933 |

Tokyo, Japan |

|

SGL Carbon |

1878 |

Wiesbaden, Germany |

|

Teijin Limited |

1918 |

Tokyo, Japan |

- SGL Carbon: SGL Automotive Carbon Fibers, a joint venture between SGL Group and BMW Group, is set to investUSD 100 millionto expand its Moses Lake facility in Washington in 2023. This expansion willdoublethe current production capacity to meet the increasing demand for carbon fiber, particularly for BMW's electric vehicles.

- Hexcel Corporation: In 2023, Hexcel Corporation expanded its engineered core operations plant in Casablanca, Morocco, with aUSD 100 millioninvestment to double its production capacity, primarily to meet the increasing demand from the aerospace sector.

North America Carbon Fiber Industry Analysis

North America Carbon Fiber Market Growth Drivers:

-

Increasing Demand from Aerospace Industry: The aerospace sector is a major driver for carbon fiber demand, with the market projected to grow significantly. Carbon fiber's lightweight and high-strength properties are essential for improving fuel efficiency in aircraft. The aerospace industry accounted for20% of global carbon fiber consumptionas of 2020, highlighting its critical role in market growth.

- Expansion of Wind Energy Projects: The wind energy sector is increasingly utilizing carbon fiber to manufacture lightweight and durable wind turbine blades. As of 2020, the wind energy industry accounted for around 23% of global carbon fiber consumption, making it the largest consumer of carbon fiber. The growing investment in renewable energy projects further supports this trend.

- Technological Advancements: Innovations in carbon fiber manufacturing processes and materials are making carbon fiber more accessible and cost-effective, encouraging its adoption across various industries, including automotive, aerospace, and consumer goods.

North America Carbon Fiber Market Challenges:

- Supply Chain Disruptions: In 2023, disruptions in the global supply chain, particularly in the availability of raw materials from Asia, caused delays in carbon fiber production. Mitsubishi Chemical Holdings reported a 10% reduction in production output due to supply chain bottlenecks.

- Environmental Concerns: Carbon fiber production has raised environmental concerns due to its energy-intensive manufacturing process. In 2024, the U.S. Environmental Protection Agency (EPA) reported that carbon fiber production generates 2.5 metric tons of CO2 emissions for every ton of carbon fiber produced.

North America Carbon Fiber Market Government Initiatives:

- Carbon Fiber Technology Facility (CFTC): Established by the U.S. Department of Energy's Vehicles Technologies Office (VTO) at Oak Ridge National Laboratory, the CFTC was created to lower the production costs of carbon fiber. This facility enables companies to test low-cost carbon fiber for various industries, including clean energy technologies.

- Funding for Renewable Carbon Fiber: The U.S. Department of Energy's Bioenergy Technologies Office announced funding for developing processes that produce carbon fiber precursors from renewable, non-food-based biomass feedstocks. This initiative aims to make carbon fiber production more sustainable and reduce reliance on fossil fuels, addressing environmental concerns associated with traditional carbon fiber manufacturing

North America Carbon Fiber Market Future Outlook

The North America Carbon Fiber Market is expected to experience robust growth through 2028, driven by increasing adoption in electric vehicles, aerospace, and renewable energy sectors. As industries strive to improve energy efficiency and reduce emissions, carbon fiber will play a key role in achieving these goals.

Future Market Trends

- Increased Use in Electric Vehicles: Over the next five years, the automotive industry will increasingly adopt carbon fiber to meet stricter fuel efficiency and emissions regulations. Electric vehicle manufacturers will prioritize lightweight carbon fiber components to improve battery life and extend vehicle range, contributing to the materials growing use.

- Growth in Renewable Energy Applications: The wind energy sector will continue to see increased demand for carbon fiber in the production of wind turbine blades. As governments push for more renewable energy installations, carbon fibers lightweight and durable properties will make it a key material in improving turbine efficiency and lowering maintenance costs.

Scope of the Report

|

USA Canada |

|

|

By Product |

Continuous Carbon Fiber Long Carbon Fiber Short Carbon Fiber |

|

By End-Use Industry |

Aerospace & Defense Automotive Wind Energy Sporting Goods Construction |

|

By Fiber Type |

PAN-based Carbon Pitch-based Carbon Fiber Other Carbon Fibers |

|

By Application |

Structural Components Body Panels Turbine Blades Sporting Goods Equipment |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Carbon Fiber Manufacturers

Aerospace & Defense Companies

Automotive OEMs

Wind Energy Companies

Government Agencies (U.S. Department of Energy, Environment and Climate Change Canada)

Electric Vehicle Manufacturers

Venture Capitalist Firms

Renewable Energy Developers

Carbon Fiber Recycling Technology Providers

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report

Hexcel Corporation

Toray Industries

Mitsubishi Chemical Holdings

SGL Carbon

Teijin Limited

Solvay

Formosa Plastics Corporation

Cytec Industries

Gurit Holding AG

DowAksa

Zoltek Companies, Inc.

Hyosung Corporation

Table of Contents

1.North America Carbon Fiber Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.North America Carbon Fiber Market Size (in Kilotons), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.North America Carbon Fiber Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand from Aerospace Industry

3.1.2. Expansion of Wind Energy Projects

3.1.3. Technological Advancements

3.2. Challenges

3.2.1. Supply Chain Disruptions

3.2.2. High Production Costs

3.2.3. Environmental Concerns

3.3. Opportunities

3.3.1. Growing Electric Vehicle Market

3.3.2. Adoption in New Applications (Sporting Goods, Construction)

3.3.3. Expansion into Emerging Markets

3.4. Trends

3.4.1. Increased Use in Electric Vehicles

3.4.2. Growth in Renewable Energy Applications

3.4.3. Advancements in Carbon Fiber Recycling Technologies

3.5. Government Regulation

3.5.1. U.S. Department of Energys Carbon Fiber Technology Facility (CFTC)

3.5.2. Funding for Renewable Carbon Fiber Development

3.5.3. Clean Energy Initiatives Supporting Carbon Fiber Usage

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competition Ecosystem

4.North America Carbon Fiber Market Segmentation, 2023

4.1. By Product Type (in Value %)

4.1.1. Continuous Carbon Fiber

4.1.2. Long Carbon Fiber

4.1.3. Short Carbon Fiber

4.2. By End-Use Industry (in Value %)

4.2.1. Aerospace & Defense

4.2.2. Automotive

4.2.3. Wind Energy

4.2.4. Sporting Goods

4.2.5. Construction

4.3. By Region (in Value %)

4.3.1. United States

4.3.2. Canada

4.4. By Fiber Type (in Value %)

4.4.1. PAN-based Carbon Fiber

4.4.2. Pitch-based Carbon Fiber

4.4.3. Other Carbon Fibers

4.5. By Application (in Value %)

4.5.1. Structural Components

4.5.2. Body Panels

4.5.3. Turbine Blades

4.5.4. Sporting Goods Equipment

4.5.5. Construction Reinforcement

5.North America Carbon Fiber Market Cross Comparison

5.1 Detailed Profiles of Major Companies

5.1.1. Hexcel Corporation

5.1.2. Toray Industries

5.1.3. Mitsubishi Chemical Holdings

5.1.4. SGL Carbon

5.1.5. Teijin Limited

5.1.6. Solvay

5.1.7. Formosa Plastics Corporation

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.North America Carbon Fiber Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.North America Carbon Fiber Market Regulatory Framework

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

8.North America Carbon Fiber Future Market Size (in Kilotons), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.North America Carbon Fiber Future Market Segmentation, 2028

9.1. By Product Type (in Value %)

9.2. By End-Use Industry (in Value %)

9.3. By Region (in Value %)

9.4. By Fiber Type (in Value %)

9.5. By Application (in Value %)

10.North America Carbon Fiber Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

11.Disclaimer

12.Contact Us

Research Methodology

Step 1: Identifying Key Variables

Ecosystem creation for all major entities involved in the North America carbon fiber market, including manufacturers, suppliers, and key end-use industries like aerospace, automotive, and renewable energy. We referred to multiple secondary and proprietary databases to perform desk research and gather industry-level information, such as production capacities, technological advancements, and consumption trends.

Step 2: Market Building

Collating statistics on the North America carbon fiber market over the years, including demand from key sectors such as aerospace, defense, and electric vehicles. This step also involved analyzing the adoption rates of carbon fiber in different applications to compute revenue generation for the market. Additionally, we reviewed supply chain dynamics, raw material availability, and pricing trends to understand factors impacting market growth.

Step 3: Validating and Finalizing

Building market hypotheses based on initial research and conducting Computer-Assisted Telephonic Interviews (CATIs) with industry experts, such as executives from carbon fiber manufacturers and end-use industries. These interviews helped validate statistics and seek detailed insights on operational and financial information from key players. This step ensured accuracy in data points, projections, and market forecasts.

Step 4: Research Output

Our team engaged with carbon fiber manufacturers, industry associations, and experts to understand the nature of product segments, sales, pricing trends, and technological developments. This feedback allowed us to refine the research findings and validate statistics derived through a bottom-up approach. Consumer preferences, manufacturing innovations, and governmental policies were also taken into consideration to provide a comprehensive market outlook.

Frequently Asked Questions

1.How big is the North America Carbon Fiber Market?

The North America Carbon Fiber Market reached a valuation of 47 kilotons in 2023, fueled by growing demand from sectors such as aerospace, automotive, and renewable energy. The rising need for lightweight, high-strength materials to improve fuel efficiency and cut emissions has been a major factor in the market's expansion.

2.What are the challenges in the North America Carbon Fiber Market?

Challenges include high production costs, supply chain disruptions affecting material availability, and environmental concerns related to carbon fiber manufacturing processes. These factors hinder the widespread adoption of carbon fiber across some industries.

3.Who are the major players in the North America Carbon Fiber Market?

Key players in the market include Hexcel Corporation, Toray Industries, Mitsubishi Chemical Holdings, SGL Carbon, and Teijin Limited. These companies lead the market due to their extensive R&D investments and robust production capacities.

4.What are the growth drivers of the North America Carbon Fiber Market?

The market is driven by the increasing adoption of electric vehicles, the expansion of the aerospace and defense industries, and the growing use of carbon fiber in wind energy projects. Government initiatives supporting sustainable materials further fuel this growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.