North America Cinema Camera Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD6154

December 2024

100

About the Report

North America Cinema Camera Market Overview

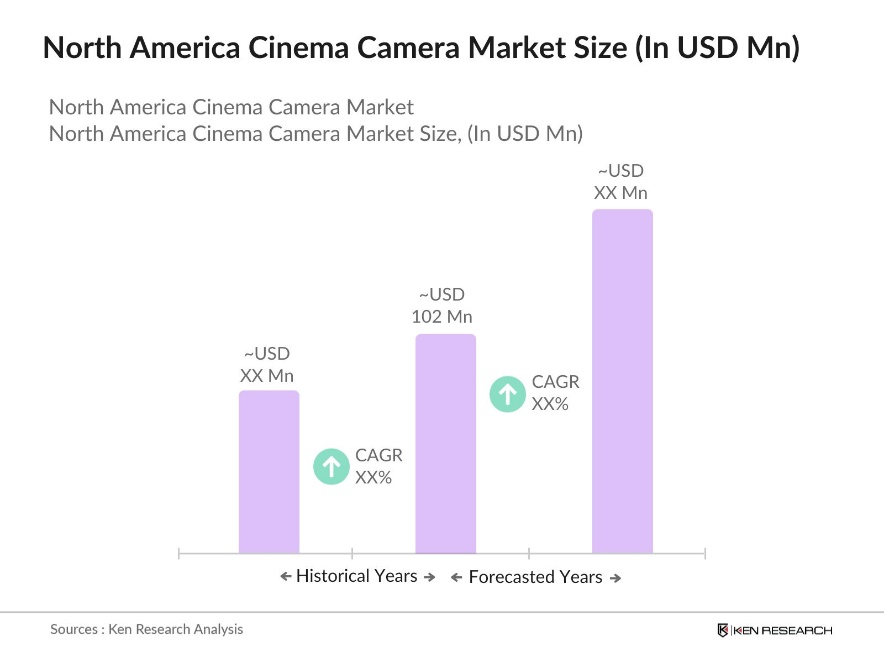

- The North America Cinema Camera Market is valued at USD 102 million, based on a five-year historical analysis. This market is driven by the rising demand for high-quality video content, particularly from the entertainment and media sectors. Advancements in technology, such as 4K and 8K video resolution, have fueled demand for cinema cameras across feature films, television series, and digital streaming platforms. The increased focus on original content by streaming services has led to a surge in demand for professional-grade equipment, driving market growth.

- In terms of dominance, the United States leads the market due to its well-established entertainment industry, home to major film studios like Universal, Warner Bros, and Paramount. Los Angeles and New York serve as major production hubs, attracting a large portion of the cinema camera market due to their infrastructure, talent, and high volume of media production. Canada, particularly Vancouver and Toronto, also plays a significant role, boosted by favorable tax incentives and growing film production activities.

- The U.S. International Trade Commission (USITC) has recommended a four-year safeguard period to protect the domestic industry from increased imports of fine denier polyester staple fiber. This involves a tariff-rate quota on imports and a quantitative restriction on imports under Temporary Importation under Bond (TIB), increasing annually. The recommendation aims to prevent further injury to U.S. producers, and the final decision will be made by the President later in 2024.

North America Cinema Camera Market Segmentation

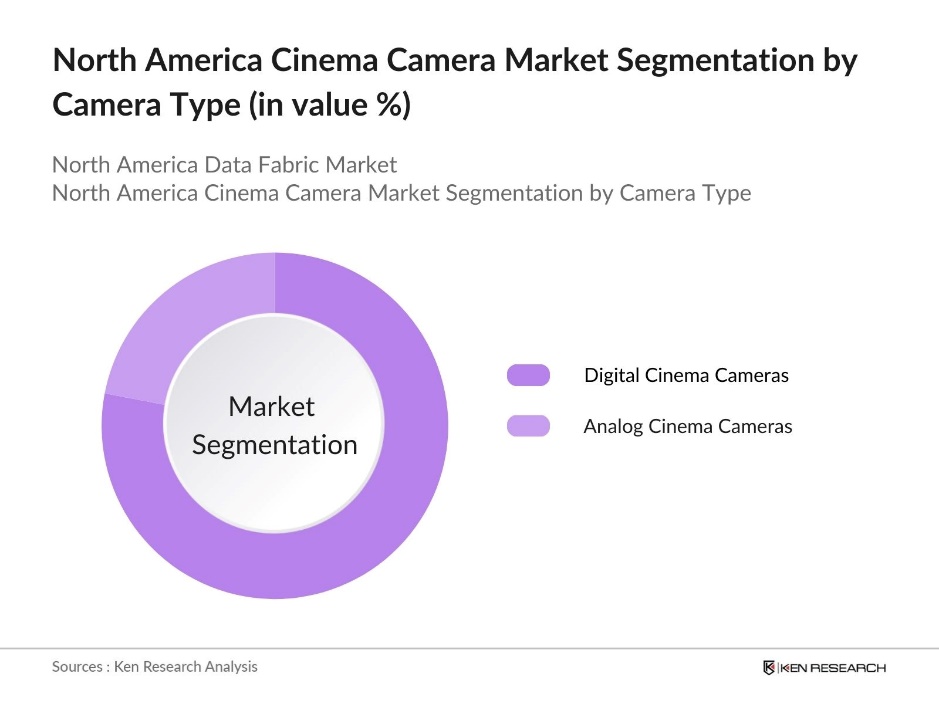

By Camera Type: The North America Cinema Camera market is segmented by camera type into digital cinema cameras and analog cinema cameras. Digital cinema cameras dominate the market share due to their advanced features such as high dynamic range, superior image resolution, and ease of post-production editing. Brands like ARRI and RED Digital Cinema are highly preferred for high-budget productions due to their renowned reliability and performance. Analog cameras are used mainly in niche projects or artistic productions that favor the aesthetic of film over digital, but they represent a much smaller segment of the market.

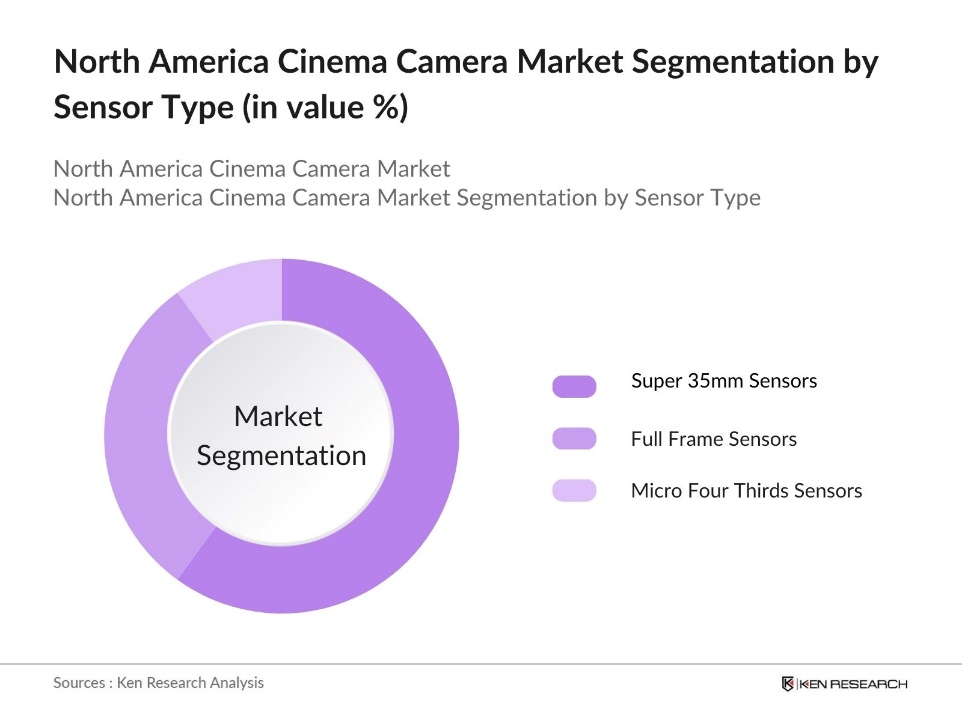

By Sensor Type: The North America Cinema Camera market is segmented by sensor type into full-frame sensors, Super 35mm sensors, and Micro Four Thirds sensors. Super 35mm sensors hold a dominant market share due to their balance between high-quality image capture and the ability to use a wide range of lenses, which is preferred in the professional filmmaking environment. Full-frame sensors are becoming more popular, especially in high-budget productions, offering superior image quality, while Micro Four Thirds sensors are used in more compact, lightweight camera setups for specialized applications.

North America Cinema Camera Market Competitive Landscape

The market is dominated by a few major players, including ARRI, RED Digital Cinema, and Sony Corporation. These companies maintain a significant influence over the market, benefiting from strong R&D capabilities and well-established distribution networks. Global competition from brands like Canon and Panasonic, which offer innovative technologies and diverse product ranges, has also intensified the market landscape. Companies compete on factors like image resolution, camera ergonomics, and adaptability to different filming environments.

|

Company Name |

Year Established |

Headquarters |

No. of Employees |

R&D Investment |

Revenue (USD) |

Product Portfolio |

Market Presence |

Key Innovations |

|

ARRI |

1917 |

Germany |

||||||

|

RED Digital Cinema |

1999 |

USA |

||||||

|

Sony Corporation |

1946 |

Japan |

||||||

|

Canon Inc. |

1937 |

Japan |

||||||

|

Panasonic Corporation |

1918 |

Japan |

North America Cinema Camera Industry Analysis

Growth Drivers

- Rise in Professional Film Production: Professional film production in North America has seen a significant boost, especially in cities like Los Angeles, New York, and Vancouver, where film industry hubs are well-established. The 2024 employment rate in motion picture and sound recording industries increased to 452,200 jobs, reflecting growing investment in large-scale productions. A notable portion of this investment is directed toward acquiring advanced cinema cameras, as filmmakers aim to produce higher-quality content to meet the demands of global streaming platforms and theaters.

- Increasing Popularity of Streaming Platforms: The explosion of content on streaming platforms such as Netflix, Hulu, and Amazon Prime has significantly driven the demand for cinema-grade cameras. As of 2024, there are 354 million streaming subscriptions in the U.S., according to Digital TV Research. This surge in demand has pushed both independent filmmakers and professional studios to invest in high-quality cinema cameras for sharper, cinematic visuals, especially as 4K and 8K content becomes standard.

- Technological Innovations (4K, 8K cameras, etc.): Technological innovations, particularly the adoption of 4K and 8K resolutions, have significantly boosted cinema camera usage in professional film and TV production. These advancements, including faster autofocus, AI-enhanced image stabilization, and higher frame rates, have made cinema cameras more attractive for filmmakers. As high-quality content becomes the norm, both established manufacturers and new market players are leveraging these innovations to cater to evolving industry demands.

Market Challenges

- High Costs of Premium Cinema Cameras: Premium cinema cameras, often used in high-end productions, remain prohibitively expensive for smaller studios and independent filmmakers. These high costs create a significant barrier, particularly for non-professional and semi-professional filmmakers, slowing the widespread adoption of advanced cinema technology. As demand for higher-quality production rises, many smaller companies struggle to justify the expense of top-tier equipment, limiting access to cutting-edge tools in the industry.

- Technical Skill Gaps Among Users: Despite growth in digital media education, there remains a shortage of professionals with the technical skills needed to operate advanced cinema cameras. The complexity of evolving technology, such as 4K and 8K cameras, requires specialized knowledge that many filmmakers lack. This skills gap, along with the cost of technical training, has slowed adoption rates of these sophisticated tools among production houses.

North America Cinema Camera Market Future Outlook

Over the next few years, the North America Cinema Camera market is expected to witness steady growth driven by technological advancements and the rise of digital content creation. The proliferation of 8K resolution cameras, alongside the integration of AI-powered tools in cinematography, is anticipated to push the demand for professional-grade cinema cameras. The continued rise of online streaming platforms such as Netflix, Amazon Prime, and Disney+ will further enhance the need for original content production, propelling market expansion.

Market Opportunities

- Increasing Demand in Indie Film and YouTube Content: The growth of independent filmmaking and content creation on platforms like YouTube has opened new opportunities for cinema camera adoption. Many creators are transitioning from simpler DSLR or mirrorless cameras to cinema-grade equipment to produce polished, cinematic videos. Independent filmmakers are investing in these tools to meet the expectations of a growing online audience that demands higher-quality content, especially in digital-first environments where professional video standards are increasingly prioritized.

- Adoption by Corporate and Commercial Filmmakers: Corporate filmmaking and commercial video production have expanded as companies prioritize digital content for branding and marketing. High-quality video content is essential in todays competitive landscape, leading businesses to invest in premium cinema cameras for their advertising campaigns. The demand for professional visuals in corporate media has driven an increased reliance on cinema-grade equipment, enhancing the production quality of commercial videos across various industries.

Scope of the Report

|

Camera Type |

Digital Cinema Cameras Analog Cinema Cameras |

|

Sensor Type |

Full Frame Sensors Super 35mm Sensors Micro Four Thirds Sensors |

|

Resolution |

4K 6K 8K and Above |

|

Application |

Feature Films Documentary Filmmaking Advertising and Corporate Videos Streaming and YouTube Content Creation |

|

Region |

United States Canada Mexico |

Products

Key Target Audience

Streaming Platforms (Netflix, Amazon Prime)

Television Production Companies

Advertising Agencies

Digital Media Companies

Government and Regulatory Bodies (U.S. Federal Communications Commission, Canadian Radio-television and Telecommunications Commission)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

ARRI

RED Digital Cinema

Sony Corporation

Canon Inc.

Panasonic Corporation

Blackmagic Design

Z CAM

Kinefinity

AJA Video Systems

Phantom (Vision Research)

Table of Contents

1. North America Cinema Camera Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics Overview

1.4. Market Segmentation Overview

2. North America Cinema Camera Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Milestones and Developments

3. North America Cinema Camera Market Analysis

3.1. Growth Drivers (Cinema Camera Adoption Rate, Demand in Content Creation, Advancements in Technology)

3.1.1. Rise in Professional Film Production

3.1.2. Increasing Popularity of Streaming Platforms

3.1.3. Technological Innovations (4K, 8K cameras, etc.)

3.2. Market Challenges (Price Sensitivity, High Maintenance Costs, Technological Complexity)

3.2.1. High Costs of Premium Cinema Cameras

3.2.2. Technical Skill Gaps Among Users

3.2.3. Limited Consumer Awareness in Non-Professional Segments

3.3. Opportunities (New Market Entrants, Emerging Independent Filmmakers, Digital Media Growth)

3.3.1. Increasing Demand in Indie Film and YouTube Content

3.3.2. Adoption by Corporate and Commercial Filmmakers

3.3.3. Growth in Regional and Local Content Creation

3.4. Trends (Customization, Compact Cinema Cameras, Remote Filmmaking Tools)

3.4.1. Rise of Compact and Lightweight Cinema Cameras

3.4.2. Customizable Accessories for Versatile Filming

3.4.3. Remote and Virtual Filmmaking Post-COVID

3.5. Government Regulations (Import Tariffs, Industry Standards, Local Content Production Incentives)

3.5.1. Regulations Impacting Digital Media Production

3.5.2. Incentives for Local Cinema Productions

3.5.3. Tariffs on Imported Camera Equipment

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape Overview

4. North America Cinema Camera Market Segmentation

4.1. By Camera Type (In Value %)

4.1.1. Digital Cinema Cameras

4.1.2. Analog Cinema Cameras

4.2. By Sensor Type (In Value %)

4.2.1. Full Frame Sensors

4.2.2. Super 35mm Sensors

4.2.3. Micro Four Thirds Sensors

4.3. By Resolution (In Value %)

4.3.1. 4K

4.3.2. 6K

4.3.3. 8K and Above

4.4. By Application (In Value %)

4.4.1. Feature Films

4.4.2. Documentary Filmmaking

4.4.3. Advertising and Corporate Videos

4.4.4. Streaming and YouTube Content Creation

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Cinema Camera Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. ARRI

5.1.2. RED Digital Cinema

5.1.3. Sony Corporation

5.1.4. Canon Inc.

5.1.5. Blackmagic Design

5.1.6. Panasonic Corporation

5.1.7. Kinefinity

5.1.8. Z Cam

5.1.9. AJA Video Systems

5.1.10. Phantom (Vision Research)

5.1.11. GoPro Inc.

5.1.12. Ikegami Electronics

5.1.13. Nikon Corporation

5.1.14. Sigma Corporation

5.1.15. Leica Camera AG

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Product Portfolio, R&D Investments, Revenue)

5.3. Market Share Analysis

5.4. Strategic Initiatives and Developments

5.5. Mergers and Acquisitions

5.6. Investment and Expansion Plans

5.7. Partnership and Collaboration Trends

5.8. Venture Capital Funding

6. North America Cinema Camera Market Regulatory Framework

6.1. Industry Certification Standards

6.2. Compliance Requirements for Camera Imports

6.3. Environmental and Sustainability Regulations

6.4. Government Incentives for Local Film Production

7. North America Cinema Camera Market Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Influencing Future Growth

8. North America Cinema Camera Future Market Segmentation

8.1. By Camera Type (In Value %)

8.2. By Sensor Type (In Value %)

8.3. By Resolution (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. North America Cinema Camera Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Market Penetration Strategy

9.3. Niche Market Targeting

9.4. Strategic Growth Opportunities

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research process begins with an ecosystem mapping of the North America Cinema Camera market, identifying major stakeholders such as manufacturers, distributors, and end-users. Secondary research from government databases, market reports, and proprietary data sources is used to define the variables influencing the market.

Step 2: Market Analysis and Construction

This step involves gathering historical data on market penetration, sales performance, and usage statistics for various cinema camera segments. These datasets are used to construct a comprehensive market analysis, ensuring a clear understanding of the revenue generated and consumption patterns.

Step 3: Hypothesis Validation and Expert Consultation

Key hypotheses regarding market trends, demand drivers, and consumer preferences are validated through interviews with industry experts and major market participants. This step refines the market model, providing insights into operational and financial aspects of the industry.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing data from both primary and secondary sources. Cinema camera manufacturers and distributors provide detailed feedback on product performance and sales figures, ensuring the reliability of the market analysis. The final output is a validated report providing an accurate depiction of the North America Cinema Camera market.

Frequently Asked Questions

01 How big is the North America Cinema Camera Market?

The North America Cinema Camera Market was valued at USD 102 million, driven by increasing demand for high-quality video content and technological advancements in imaging solutions.

02 What are the challenges in the North America Cinema Camera Market?

Key challenges in North America Cinema Camera Market include high costs associated with premium cinema cameras, limited consumer knowledge in non-professional sectors, and competition from smartphone cameras that offer relatively high-quality video capabilities.

03 Who are the major players in the North America Cinema Camera Market?

Major players in North America Cinema Camera Market include ARRI, RED Digital Cinema, Sony Corporation, Canon Inc., and Panasonic Corporation. These companies dominate the market due to their strong brand reputation, innovative product offerings, and global distribution networks.

04 What drives growth in the North America Cinema Camera Market?

The North America Cinema Camera Market growth is driven by rising demand for professional video production for films, TV, and digital content platforms, alongside technological innovations like 4K and 8K video resolution cameras.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.