North America Connected Car Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD1776

October 2024

86

About the Report

North America Connected Car Market Overview

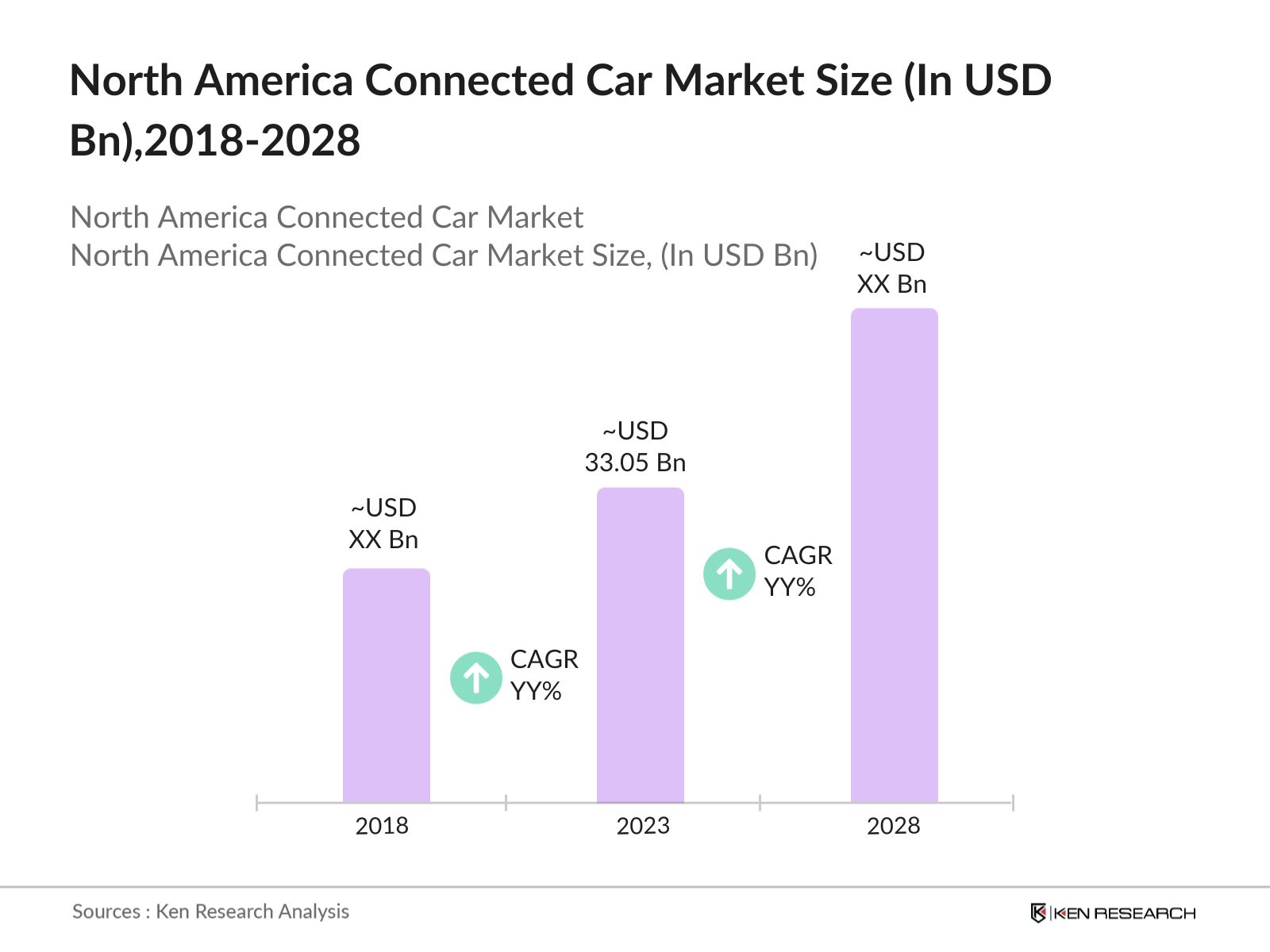

- The North America Connected Car Market was valued at USD 33.05 billion in 2023. The growth has been fueled by several factors, including the proliferation of 4G and 5G networks, the increasing integration of Internet of Things (IoT) technologies, and growing concerns around road safety which have led to increased adoption of advanced driver assistance systems (ADAS) and telematics.

- The major players in the market are General Motors, Ford Motor Company, Tesla, Continental AG, and Harman International. These companies have leveraged their technological expertise and strong market presence to maintain a competitive edge, continually introducing new features and services that enhance vehicle connectivity, safety, and user experience.

- In 2023, General Motors announced its partnership with Qualcomm to integrate the Snapdragon Digital Chassis across its fleet. This collaboration is expected to enhance vehicle connectivity, enabling more sophisticated ADAS features, over-the-air updates, and immersive in-car experiences. The Snapdragon platform is anticipated to be integrated into GM's new electric vehicle lineup, starting in late 2024, positioning GM at the forefront of the connected car revolution.

- The United States is currently the dominant region in the market, with the high adoption rate of advanced technologies, the presence of major automakers, and strong government support for connected and autonomous vehicle development. Cities like Detroit and Silicon Valley, a hub for tech innovation, have been at the forefront of this growth, driving investments in R&D and infrastructure to support the connected car ecosystem.

North America Connected Car Market Segmentation

The market is segmented into various factors like technology, application, and region.

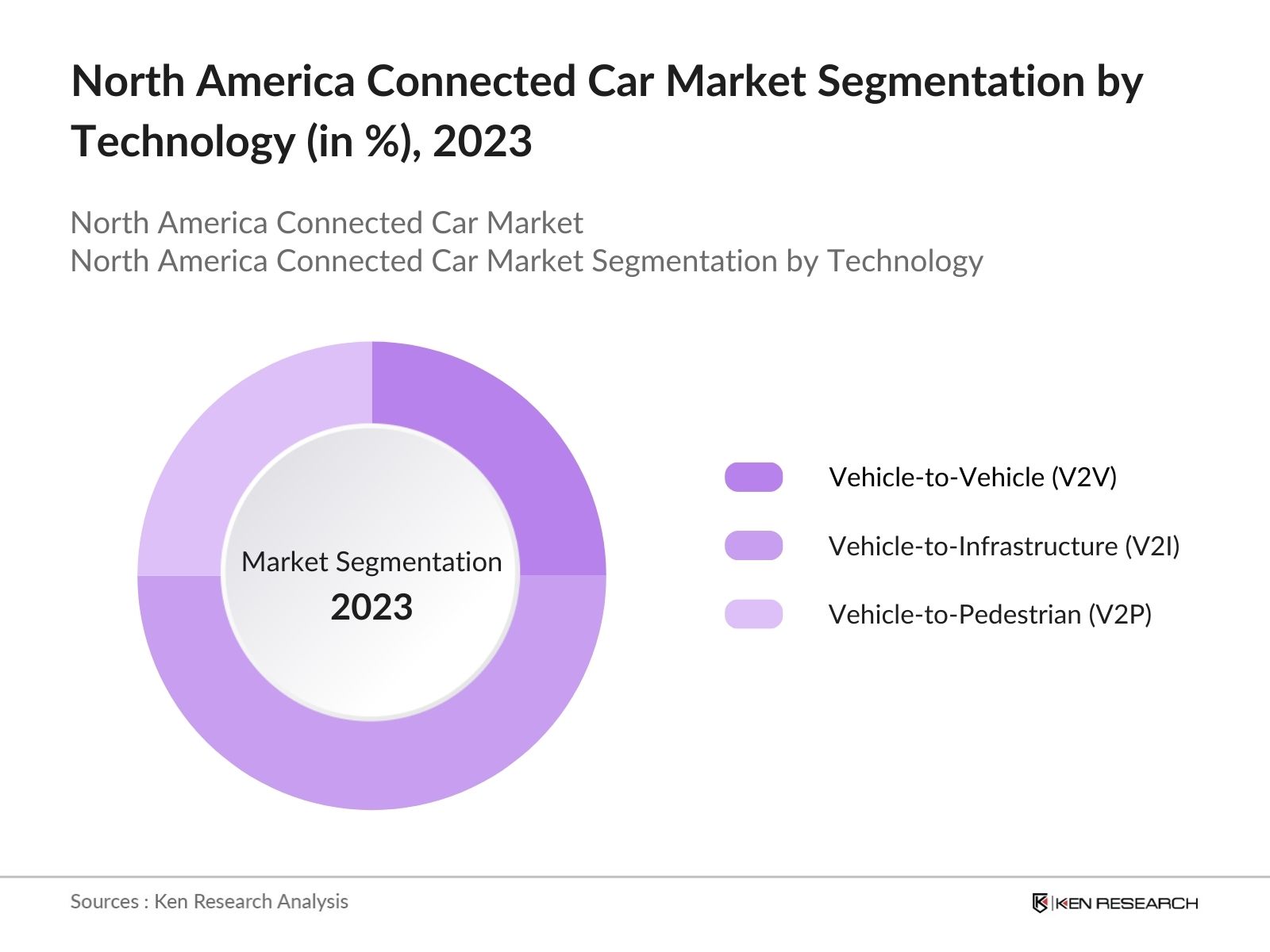

By Technology: The market is segmented by technology into Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), and Vehicle-to-Pedestrian (V2P) communications. In 2023, Vehicle-to-Infrastructure (V2I) technology held the dominant market share due to its critical role in enabling smart city initiatives and improving traffic management systems. The increasing deployment of smart traffic signals and roadside units (RSUs) across major North American cities.

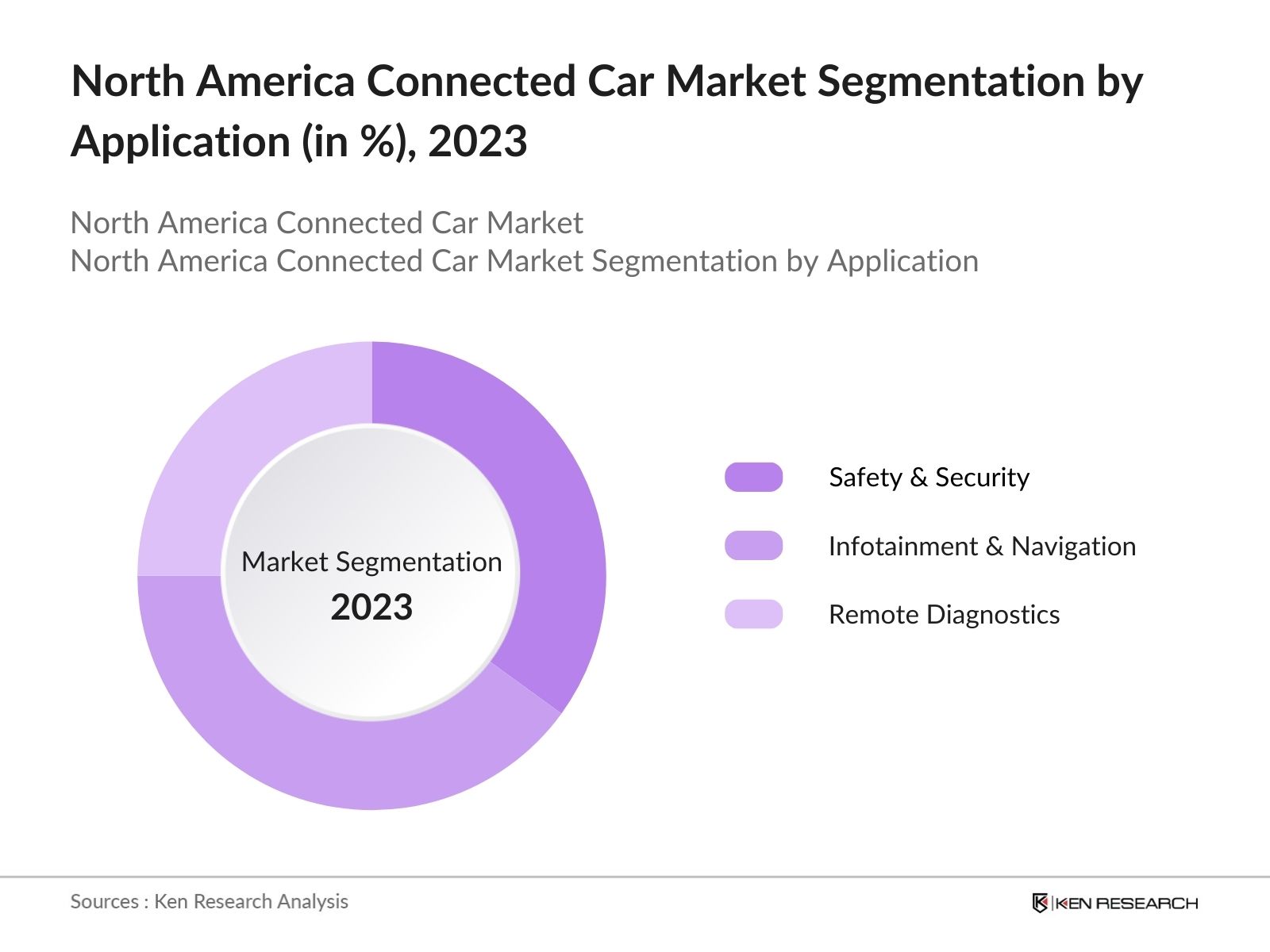

By Application: The market is segmented by application into safety & security, infotainment & navigation, and remote diagnostics. In 2023, the Infotainment & Navigation segment emerged as the dominant market with the demand for advanced infotainment systems, which include features like real-time traffic updates, voice-activated controls, and integrated streaming services, has been a major driver.

By Region: The market is segmented by region into the United States and Canada. In 2023, the United States dominated the regional market due to the countrys leadership in automotive innovation, coupled with strong government support and consumer demand, has propelled the U.S. to the forefront of the market.

North America Connected Car Market Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|

General Motors |

1908 |

Detroit, Michigan |

|

Ford Motor Company |

1903 |

Dearborn, Michigan |

|

Tesla |

2003 |

Palo Alto, California |

|

Continental AG |

1871 |

Hanover, Germany |

|

Harman International |

1980 |

Stamford, Connecticut |

- Ford Motor Company: In 2023, Ford Motor Company announced an investment of USD 3 billion in expanding its connected vehicle services, including a new cloud-based platform that enables over-the-air software updates and enhanced telematics. This investment is part of Fords broader strategy to transition towards a software-driven business model, leveraging its connected car ecosystem to offer new revenue-generating services, such as subscription-based features and remote diagnostics.

- Continental AG: At Agritechnica 2023, Continental introduced a scalable telematics platform for agricultural machinery, emphasizing cybersecurity. This platform allows flexibility with 4G and 5G standards and is designed to combat increasing cyber threats in agriculture, anticipating the EU's Cyber Resilience Act expected in spring 2024.

North America Connected Car Market Analysis

Market Growth Drivers

- Adoption of 5G Technology for Connected Vehicles: The growing implementation of 5G technology across North America is a growth driver for the market. By 2024, Cisco and TELUS will integrate 5G capabilities into over 1.5 million connected cars. This advanced connectivity enhances real-time data exchange, enabling seamless vehicle-to-infrastructure communication and faster software updates for features such as infotainment and safety applications.

- Increased Demand for Advanced Driver Assistance Systems (ADAS): The demand for ADAS continues to rise as consumers prioritize road safety and convenience features. By the end of 2024, North America are expected to have some form of ADAS, such as adaptive cruise control and automated lane-keeping systems. These technologies depend on vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication, which is central to the connected car ecosystem.

- Telematics and Insurance Integration: The integration of telematics for usage-based insurance has become another key growth driver. In 2024, North America will have telematics systems that help insurers track driving behavior. This technology not only allows insurers to offer more competitive premiums based on individual driving data but also encourages the adoption of connected car features like real-time diagnostics and monitoring.

Market Challenges

- Lack of Standardized Communication Protocols: A key technical challenge in the industry is the lack of standardized protocols for V2V and V2I communication. Various automakers use proprietary systems, which can hinder the integration of connected cars into broader smart city infrastructures. Industry-wide standardization is necessary to ensure interoperability, but achieving this is complex given the different systems currently in place.

- High Costs of Advanced Connectivity Features: The cost of equipping vehicles with full connectivity systems remains a significant barrier to widespread adoption. The average price of a connected car with 5G, ADAS, and telematics capabilities, limiting these features primarily to luxury vehicle segments. This cost issue could slow the mass adoption of connected technologies, particularly among budget-conscious consumers.

Government Initiatives

- U.S. Department of Transportations V2X Program: The U.S. government has allocated USD 6.4 billion over five years to enhance Vehicle-to-Everything (V2X) communication solutions. This funding will support projects aimed at reducing greenhouse gas emissions and improving safety through connected vehicle technology, including Roadside Units (RSUs) for efficient traffic management and prioritization of emergency vehicles.

- Canadian Governments Investment in Smart Cities: In Canada, the government has allocated USD 300 million to smart city projects, focusing on integrating connected vehicle technologies into urban transportation networks. These projects are expected to support the development of infrastructure that allows for seamless V2I communication, driving the market forward.

North America Connected Car Market Future Outlook

The future trends in the North America connected car industry include increased integration of artificial intelligence (AI) in vehicles, growth in autonomous vehicle adoption, expansion of vehicle-to-everything (V2X) communication networks, and the rise of subscription-based connected vehicle services.

Future Market Trends

- Expansion of Vehicle-to-Everything (V2X) Communication Networks: V2X communication networks are expected to become more widespread by 2028, with over 200,000 smart intersections and roadside units operational across North America. These networks will enable real-time communication between vehicles, infrastructure, and pedestrians, significantly enhancing traffic management and road safety.

- Increased Integration of Artificial Intelligence (AI) in Connected Vehicles: By 2028, over 120 million vehicles in North America are expected to be equipped with AI-based systems. These systems will manage various aspects of vehicle operation, including predictive maintenance, traffic management, and personalized in-car experiences. AI will be pivotal in enhancing vehicle safety, efficiency, and user experience, driving significant growth in the connected car market.

Scope of the Report

|

By Technology |

Vehicle-to-Vehicle (V2V) Vehicle-to-Infrastructure (V2I) Vehicle-to-Pedestrian (V2P) |

|

By Application |

Safety & Security Infotainment & Navigation Remote Diagnostics |

|

By Region |

USA Canada |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Telecommunications Companies

Insurance Companies

Government Regulatory Bodies (e.g., U.S. Department of Transportation)

Automotive Dealerships

Vehicle Leasing Companies

Fleet Management Companies

Logistics and Transportation Companies

Consumer Electronics Companies

Venture Capitalist

Companies

Players Mentioned in the Report:

General Motors

Ford Motor Company

Tesla

Continental AG

Harman International

Qualcomm

BMW Group

Mercedes-Benz

Nissan Motor Corporation

Toyota Motor Corporation

Bosch

AT&T

Verizon

Intel Corporation

Apple Inc.

Table of Contents

1. North America Connected Car Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Connected Car Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Connected Car Market Analysis

3.1. Growth Drivers

3.1.1. 5G Network Adoption

3.1.2. Government Investments in Smart Infrastructure

3.1.3. Rising Demand for ADAS

3.1.4. Increase in Telematics-Based Insurance

3.2. Restraints

3.2.1. Cybersecurity Threats

3.2.2. High Costs of Technology

3.2.3. Lack of Standardization

3.2.4. Consumer Privacy Concerns

3.3. Opportunities

3.3.1. Expansion of V2X Communication Networks

3.3.2. Growth of Autonomous Vehicles

3.3.3. Increased Integration of AI

3.3.4. Subscription-Based Services

3.4. Trends

3.4.1. AI in Connected Vehicles

3.4.2. Autonomous Vehicle Adoption

3.4.3. V2X Communication Expansion

3.4.4. Rise of Subscription Models

3.5. Government Regulation

3.5.1. USDOT's V2X Communication Program

3.5.2. Canadas Smart Cities Challenge

3.5.3. Californias Autonomous Vehicle Testing

3.5.4. Infrastructure Bill for Connected Vehicle Technology

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competition Ecosystem

4. North America Connected Car Market Segmentation, 2023

4.1. By Technology Type (in Value %)

4.1.1. Vehicle-to-Vehicle (V2V)

4.1.2. Vehicle-to-Infrastructure (V2I)

4.1.3. Vehicle-to-Pedestrian (V2P)

4.2. By Application (in Value %)

4.2.1. Safety & Security

4.2.2. Infotainment & Navigation

4.2.3. Remote Diagnostics

4.3. By Region (in Value %)

4.3.1. United States

4.3.2. Canada

5. North America Connected Car Market Cross Comparison

5.1 Detailed Profiles of Major Companies

5.1.1. General Motors

5.1.2. Ford Motor Co.

5.1.3. Tesla Inc.

5.1.4. Continental AG

5.1.5. Harman International

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6. North America Connected Car Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7. North America Connected Car Market Regulatory Framework

7.1. Safety and Compliance Standards

7.2. Certification Processes

8. North America Connected Car Future Market Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9. North America Connected Car Future Market Segmentation, 2028

9.1. By Technology Type (in Value %)

9.2. By Application (in Value %)

9.3. By Connectivity Type (in Value %)

9.4. By Vehicle Type (in Value %)

9.5. By Region (in Value %)

10. North America Connected Car Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step:1 Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step:2 Market Building:

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for North America Connected Car industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step:3 Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step:4 Research output:

Our team will approach multiple automotive companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such automotive companies.

Frequently Asked Questions

01 How big is the North America Connected Car market?

The North America Connected Car Market was valued at USD 33.05 billion in 2023. The growth has been fueled by several factors, including the proliferation of 4G and 5G networks, the increasing integration of Internet of Things (IoT) technologies

02 What are the challenges in the North America Connected Car market?

The challenges in the North America Connected Car market include cybersecurity threats to connected vehicles, high costs associated with advanced connected car technologies, lack of standardization in vehicle communication protocols, and growing consumer privacy concerns.

03 Who are the major players in the North America Connected Car market?

Key players in the North America Connected Car market include General Motors, Ford Motor Company, Tesla, Continental AG, and Harman International. These companies are at the forefront of market innovation and development.

04 What are the main growth drivers of the North America Connected Car market?

The growth of the North America Connected Car market is driven by the widespread adoption of 5G technology, increasing demand for Advanced Driver Assistance Systems (ADAS), rising use of telematics-based insurance, and substantial government investments in smart transportation infrastructure.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.