North America Consumer Packaged Goods (CPG) Market Outlook to 2030

Region:North America

Author(s):Shreya

Product Code:KROD1865

October 2024

85

About the Report

North America Consumer Packaged Goods (CPG) Market Overview

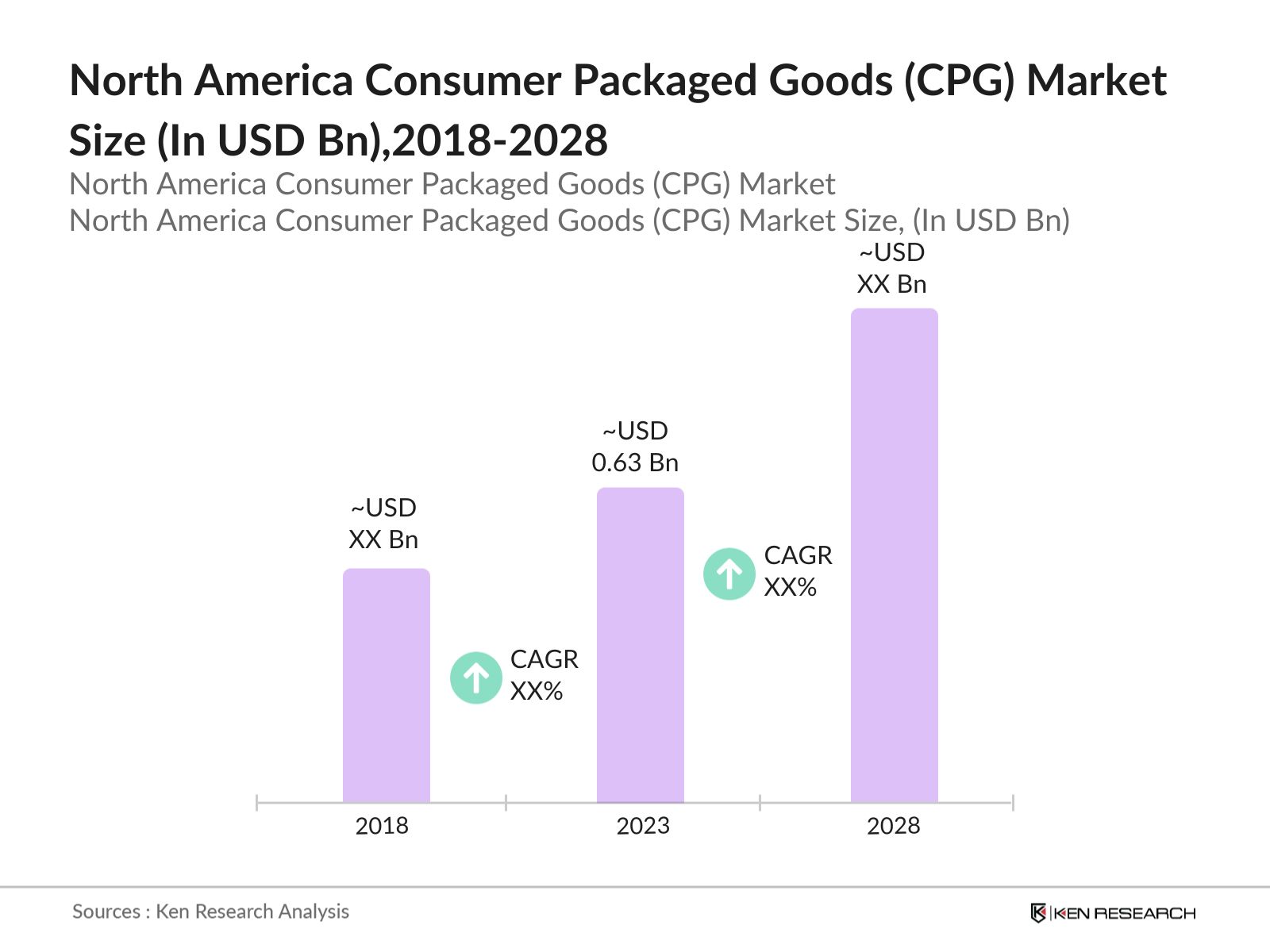

The North America Consumer Packaged Goods (CPG) market was valued at USD 630 billion in 2023. This growth is primarily driven by changing consumer preferences, increasing disposable income, and the rise of e-commerce, which has expanded the reach of CPG products. The CPG market encompasses a wide range of products, including food and beverages, personal care items, and household goods.

Major players in the North American CPG market include Procter & Gamble, Unilever, Nestl, PepsiCo, and The Coca-Cola Company. These companies dominate the market through extensive distribution networks, strong brand recognition, and continuous innovation in product offerings. Their ability to adapt to changing consumer preferences and invest in digital transformation has positioned them as leaders in the industry.

In 2023, Unilever announced a investment of USD 200 million in its North American operations to enhance its digital capabilities and sustainability efforts. This investment is aimed at reducing the companys carbon footprint and increasing the use of recycled materials in packaging. This move aligns with the growing consumer demand for environmentally friendly products and reflects Unilevers commitment to sustainability.

United States dominates the market in 2023, as reported by Euromonitor International. This dominance is attributed to the large consumer base, high disposable income, and a well-established retail infrastructure. Within the U.S., California and Texas are the leading states due to their large populations and significant retail markets.

North America Consumer Packaged Goods (CPG) Market Segmentation

North America CPG market is segmented into various segments such as product type, distribution channel and region.

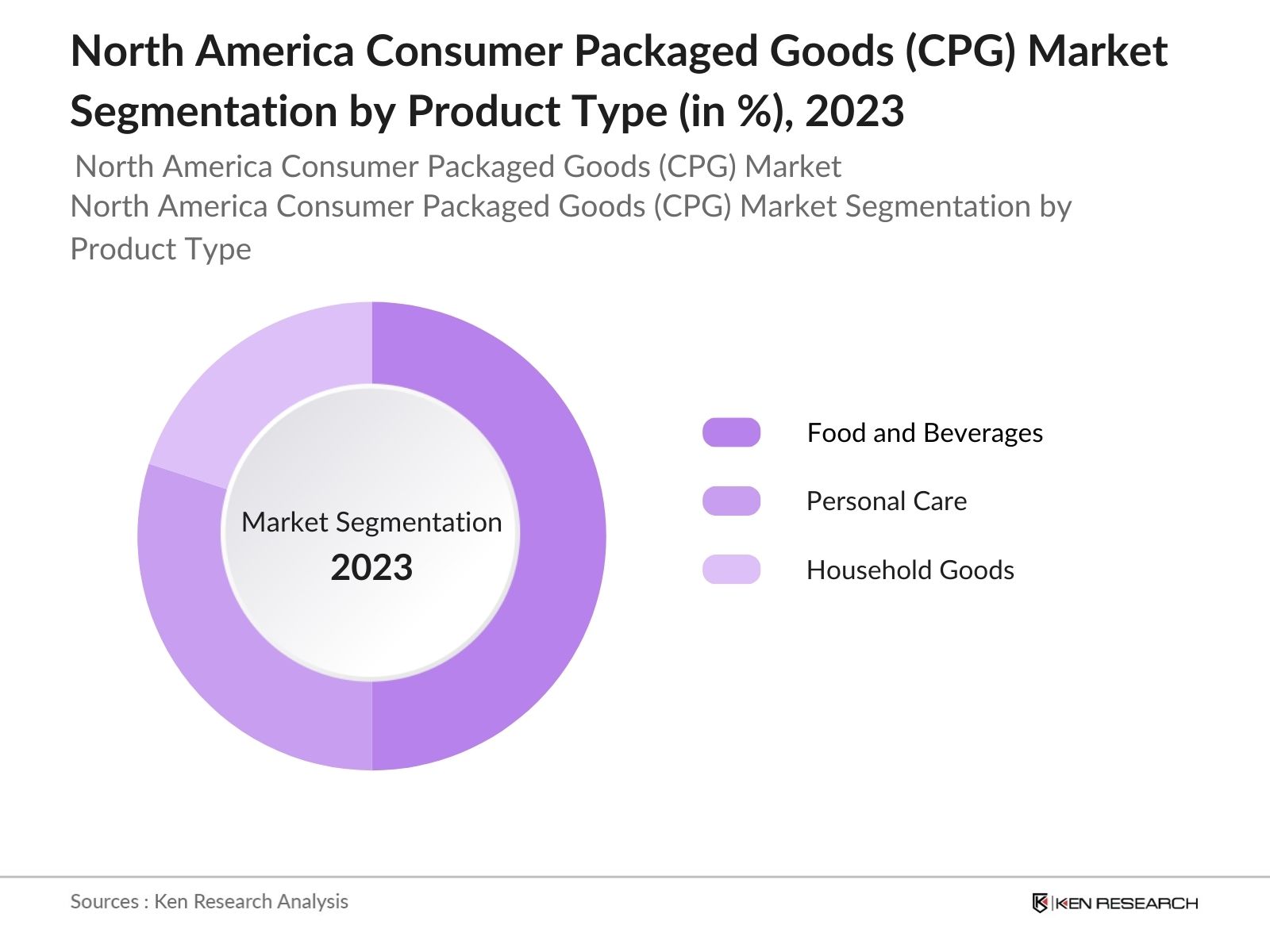

1.By Product Type: The market is segmented by product type into food and beverages, personal care products, and household goods. In 2023, the food and beverages segment held the dominant market share. This dominance is due to the high demand for packaged food and beverages, driven by the growing trend of convenience and on-the-go consumption. The increasing preference for healthy and organic food products also contributes to the segments growth.

2.By Distribution Channel: The market is also segmented by distribution channel into supermarkets and hypermarkets, convenience stores, online retail, and others. Online retail is expected to dominate the market share in 2023, driven by the increasing adoption of e-commerce and the convenience it offers. The COVID-19 pandemic accelerated the shift towards online shopping, and this trend is expected to continue, with more consumers preferring the convenience and safety of online purchases.

3.By Region: Geographically, the North America market is segmented into United States and Canada. The United States, including states like New York and Massachusetts, dominated the 2023 market share. This dominance is attributed to the high population density, higher disposable income, and a strong retail presence. The regions diverse consumer base and preference for premium and organic products also contribute to its leading position.

|

Region |

Market Share (2023) |

|---|---|

|

North |

20% |

|

South |

30% |

|

East |

40% |

|

West |

10% |

North America Consumer Packaged Goods (CPG) Market Competitive Landscape

|

Company Name |

Establishment Year |

Headquarters |

|---|---|---|

|

Procter & Gamble |

1837 |

Cincinnati, USA |

|

Unilever |

1929 |

London, UK |

|

Nestl |

1866 |

Vevey, Switzerland |

|

PepsiCo |

1965 |

Purchase, USA |

|

The Coca-Cola Company |

1892 |

Atlanta, USA |

- Unilever: Unilever has been managing its portfolio in North America through acquisitions and disposals.In recent years, the company has acquired several brands like SmartyPants Vitamins in 2020. It is also strengthening its investment in the fast-growing health and wellbeing sector, with the Unilever Health & Wellbeing Collective now a 1 billion+ portfolio of lifestyle brands.

- Pepsico: The company has diversified its packaging strategies by introducing new offerings include Frito-Lay Minis, which are bite-sized versions of popular snacks, and the introduction of paper-based solutions to replace plastic rings in multipack beverages.This shift not only caters to consumer preferences but also supports sustainability initiatives aimed at reducing plastic waste.

North America Consumer Packaged Goods (CPG) Industry Analysis

Growth Drivers

- E-Commerce Expansion: The market's robust digital infrastructure supports this growth, with over 300 million internet users in the United States and Canada combined. The expansion of e-commerce platforms like Amazon and Walmarts online marketplace further facilitates this trend, providing consumers with easy access to a wide range of CPG products. This boom in online shopping is fueled by consumer demand for convenience and increased disposable income.

- Increased Health and Wellness Awareness: There is a growing consumer focus on health and wellness. This shift is driven by increased awareness of the benefits of healthy eating and sustainable living. As a result, CPG companies are investing in product innovation to cater to this demand, introducing new product lines such as plant-based foods and beverages. Additionally, U.S. Food and Drug Administrations guidelines on nutrition labeling, encourages manufacturers to enhance product transparency, which further boosts consumer confidence.

- Innovation in Product Offerings: Companies are increasingly focusing on developing new products that cater to changing consumer preferences and trends. In 2024, it is estimated that CPG companies will launch over 5,000 new products across various categories, including food, beverages, and personal care. The ability to adapt quickly to market trends through product innovation is a key factor contributing to the growth of the CPG market in North America.

Challenges

- Rising Raw Material Costs: The cost of essential ingredients such as wheat, corn, and sugar has increased putting pressure on manufacturers margins. This inflation in costs is attributed to several factors, including adverse weather conditions affecting crop yields, geopolitical tensions disrupting global trade, and increased demand for agricultural commodities. Consequently, CPG companies are grappling with higher input costs, which may lead to price hikes for consumers.

- Intense Market Competition: The market is highly competitive, with numerous well-established brands and new entrants vying for market share. This crowded market environment forces companies to continuously innovate and differentiate their products to capture consumer attention and loyalty. Competitors can erode profit margins and lead to market saturation, posing a challenge for companies aiming to maintain or expand their market presence.

Government Initiatives

- Food Safety Modernization Act (FSMA) Compliance: In 2024, the FDA allocated an additional USD 50 million to bolster compliance monitoring and inspection activities. This funding is intended to ensure that Consumer Packaged Goods (CPG) companies adhere to food safety standards, thereby reducing the risk of foodborne illnesses and protecting public health. The emphasis on compliance means that companies are required to implement robust quality control systems and invest in employee training.

- Support for Local Manufacturing: Established through an Executive Order in January 2021, the Made in America Office (MIAO) within the Office of Management and Budget (OMB) oversees the implementation of these policies. This initiative provides financial assistance, such as grants and low-interest loans, to companies that invest in local production facilities and create jobs in the United States.

North America Consumer Packaged Goods (CPG) Future Outlook

The North America CPG market is expected to continue its growth. The markets future growth will be fueled by technological advancements, increased focus on sustainability, and the expansion of e-commerce. Additionally, companies will likely focus on personalization and direct-to-consumer strategies to better meet the evolving needs of their customers.

Future Trends

- Growth in Personalization and Customization: Over the next five years, the market will see an increase in personalization and customization of products. Companies will leverage advanced data analytics and AI to understand consumer preferences and deliver tailored products that meet individual needs. North America will engage with personalized CPG products, reflecting a growing trend towards customization in the market.

- Expansion of Sustainable and Eco-Friendly Products: The demand for sustainable and eco-friendly products is expected to rise significantly in the coming years. North American consumers will actively seek out CPG products with minimal environmental impact. This trend is driven by increasing environmental awareness and regulatory pressures, prompting companies to invest in sustainable sourcing, packaging, and production practices to meet consumer expectations and comply with evolving regulations.

Scope of the Report

|

By Application |

Food And Beverages Personal Care Products Household Goods |

|

By End User |

Supermarkets And Hypermarkets Convenience Stores Online Retail Others |

|

By Region |

United States Canada Mexico |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Government agency (e.g., U.S. Environmental Protection Agency)

CPG manufacturers

E-commerce platforms

Packaging companies

Logistic service providers

Marketing and advertising firms

Food and beverage companies

Banking and Financial Institutions

Investors and VC Firms

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Procter & Gamble

Unilever

Nestl

PepsiCo

The Coca-Cola Company

Colgate-Palmolive

Johnson & Johnson

Kimberly-Clark

L'Oral

Kraft Heinz

Kellogg's

General Mills

Mondelez International

Danone

Reckitt Benckiser

Table of Contents

1.North America Consumer Packaged Goods (CPG) Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.North America Consumer Packaged Goods (CPG) Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.North America Consumer Packaged Goods (CPG) Market Analysis

3.1. Growth Drivers

3.1.1. Expansion of E-commerce Platforms

3.1.2. Increased Health and Wellness Awareness

3.1.3. Rising Consumer Spending

3.1.4. Innovation in Product Offerings

3.2. Restraints

3.2.1. Supply Chain Disruptions

3.2.2. Rising Raw Material Costs

3.2.3. Regulatory Compliance Challenges

3.3. Opportunities

3.3.1. Growth in Direct-to-Consumer Channels

3.3.2. Expansion into Emerging Product Segments

3.3.3. Investment in Sustainable Practices

3.4. Trends

3.4.1. Personalization and Customization of Products

3.4.2. Adoption of Digital and Omnichannel Strategies

3.4.3. Focus on Health and Wellness Products

3.5. Government Regulation

3.5.1. Sustainable Packaging Legislation

3.5.2. Food Safety Modernization Act (FSMA) Compliance

3.5.3. Tax Incentives for R&D

3.5.4. Support for Local Manufacturing

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competitive Ecosystem

4.North America Consumer Packaged Goods (CPG) Market Segmentation, 2023

4.1. By Product Type (in Value %)

4.1.1. Food and Beverages

4.1.2. Personal Care Products

4.1.3. Household Goods

4.2. By Distribution Channel (in Value %)

4.2.1. Online Retail

4.2.2. Supermarkets and Hypermarkets

4.2.3. Convenience Stores

4.3. By Region (in Value %)

4.3.1. North

4.3.2. South

4.3.3. East

4.3.4. West

5.North America Consumer Packaged Goods (CPG) Market Cross Comparison

5.1. Detailed Profiles of Major Companies

5.1.1. Procter & Gamble

5.1.2. Unilever

5.1.3. Nestl

5.1.4. PepsiCo

5.1.5. The Coca-Cola Company

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.North America Consumer Packaged Goods (CPG) Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.North America Consumer Packaged Goods (CPG) Market Regulatory Framework

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

8.North America Consumer Packaged Goods (CPG) Future Market Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.North America Consumer Packaged Goods (CPG) Future Market Segmentation, 2028

9.1. By Product Type (in Value %)

9.2. By Distribution Channel (in Value %)

9.3. By Region (in Value %)

10.North America Consumer Packaged Goods (CPG) Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

11.Disclaimer

12.Contact Us

Research Methodology

Step:1 Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step:2 Market Building:

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for North America Consumer Packaged goods industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step:3 Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry experts belonging to different consumer packaged goods companies to validate statistics and seek operational and financial information from company representatives.

Step:4 Research output:

Our team will approach multiple construction companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such consumer-packaged goods companies.

Frequently Asked Questions

1.How big is the North America Consumer Packaged Goods (CPG) Market?

The North America Consumer Packaged Goods (CPG) market, valued at USD 630 billion in 2023, is driven by rising consumer spending, increased e-commerce adoption, and growing awareness of health and wellness products.

2.What are the challenges in the North America Consumer Packaged Goods (CPG) Market?

Challenges in the North America CPG market include supply chain disruptions, rising raw material costs, stringent regulatory compliance, and intense market competition, which put pressure on profit margins and operational efficiency.

3.Who are the major players in the North America Consumer Packaged Goods (CPG) Market?

Major players in the North America CPG market include Procter & Gamble, Unilever, Nestl, PepsiCo, and The Coca-Cola Company. These companies lead the market with their strong distribution networks, continuous innovation, and extensive product offerings.

4.What are the growth drivers of the North America Consumer Packaged Goods (CPG) Market?

Growth drivers of the North America CPG market include the expansion of e-commerce platforms, increased health and wellness awareness among consumers, rising consumer spending, and continuous innovation in product offerings, which cater to changing consumer preferences.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.