North America Cooking Oil Market Outlook to 2030

Region:North America

Author(s):Paribhasha Tiwari

Product Code:KROD4155

Region:North America

Author(s):Paribhasha Tiwari

Product Code:KROD4155

December 2024

85

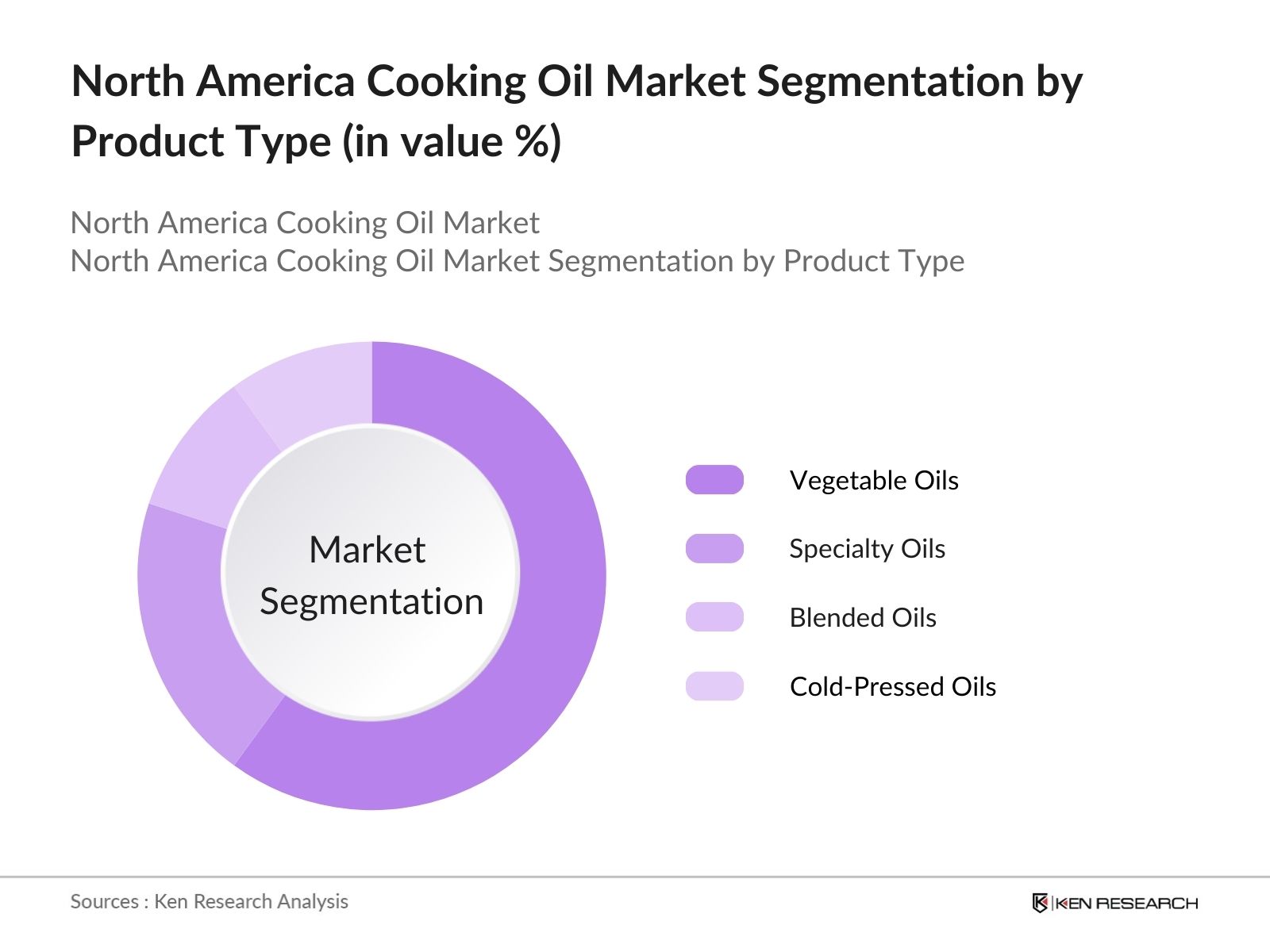

By Product Type: The North America cooking oil market is segmented by product type into vegetable oils, specialty oils, blended oils, and cold-pressed oils. Vegetable oils, including soybean, canola, and corn oil, continue to dominate the market share due to their widespread availability and cost-effectiveness. Soybean oil, in particular, holds a significant market share as it is widely used in both household and commercial food preparation. Its versatility, high smoke point, and affordability make it a staple in the American diet.

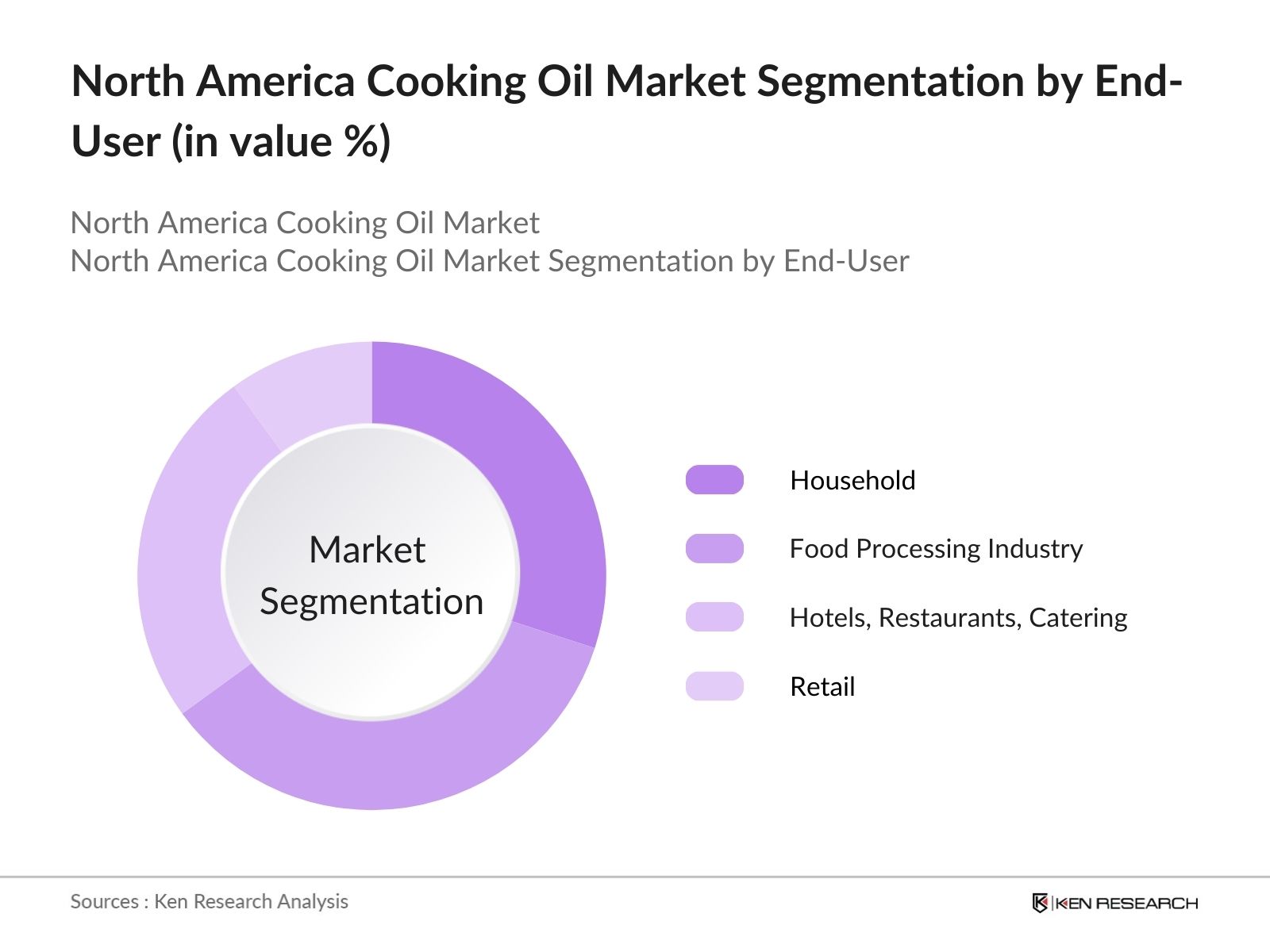

By End-User: The market is also segmented by end-user into household, HoReCa (Hotels, Restaurants, Catering), food processing industry, and retail. The food processing industry holds a dominant position in the market, with significant demand for oils used in the production of baked goods, snacks, and processed foods. The industry's reliance on cost-effective and high-volume oils, such as palm oil and soybean oil, drives this demand. Household consumption of cooking oils is also substantial, particularly due to the rise of home cooking during the pandemic and the growing trend of using healthier oil options like olive oil.

The North America cooking oil market is competitive, with several key players controlling a substantial portion of the market. Major global and regional companies compete on the basis of price, product quality, distribution reach, and brand reputation. The market's competitive landscape is dominated by agricultural giants with strong supply chains and vertically integrated operations.

|

Company |

Year of Establishment |

Headquarters |

Production Capacity |

Product Portfolio |

R&D Investment |

Sustainability Initiatives |

Brand Presence |

Geographical Reach |

|

Archer Daniels Midland (ADM) |

1902 |

Chicago, USA |

- | - | - | - | - | - |

|

Cargill Incorporated |

1865 |

Minnesota, USA |

- | - | - | - | - | - |

|

Bunge Limited |

1818 |

Missouri, USA |

- | - | - | - | - | - |

|

Wilmar International |

1991 |

Singapore |

- | - | - | - | - | - |

|

Conagra Brands |

1919 |

Illinois, USA |

- | - | - | - | - | - |

The North America cooking oil market is poised for steady growth, driven by evolving consumer preferences and advancements in oil production technologies. Increasing awareness regarding the health benefits of oils like olive, avocado, and coconut, coupled with the growing demand for organic and non-GMO products, is expected to propel market expansion. Additionally, innovations in oil packaging, particularly eco-friendly options, are likely to further boost market penetration across retail and foodservice sectors.

|

By Product Type |

Vegetable Oils Specialty Oils Blended Oils Cold-Pressed Oils |

|

By Source |

Organic Conventional Non-GMO |

|

By End-User |

Household HoReCa Food Processing Industry Retail |

|

By Distribution Channel |

Supermarkets and Hypermarkets Online Channels Specialty Stores Direct to Consumer |

|

By Region |

U.S. Canada Mexico |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Volume, Value)

1.4. Market Segmentation Overview (Product Type, Source, End-User, Distribution Channel, Region)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis (Volume, Revenue)

2.3. Key Market Developments and Milestones (Government Initiatives, Key M&A)

3.1. Growth Drivers (Current Demand Trends, Regulatory Support, Health Consciousness)

3.1.1. Rise in Health-Conscious Consumption (Olive Oil, Avocado Oil, and Other Healthy Alternatives)

3.1.2. Growing Demand for Organic and Non-GMO Oils

3.1.3. Regulatory Policies Promoting Healthier Fats and Oils

3.1.4. Demand from Food Services and HoReCa (Hotel, Restaurant, and Caf) Sector

3.2. Market Challenges (Production, Logistics, Price Volatility, Sustainability Concerns)

3.2.1. Supply Chain Disruptions and Fluctuating Raw Material Costs (Palm, Soy, and Canola Oils)

3.2.2. Environmental Impact and Sustainability in Oil Production (Palm Oil, Soybean Oil)

3.2.3. High Competition in Pricing Leading to Profit Margin Reduction

3.2.4. Regulatory Compliance for New Product Development

3.3. Opportunities (Emerging Trends, Market Gaps, Investment Scope)

3.3.1. Rise of Cold-Pressed Oils as a Health-Conscious Alternative

3.3.2. Increasing Adoption of Smart Packaging Solutions for Extended Shelf Life

3.3.3. Potential Growth in Plant-Based Cooking Oil Innovations

3.3.4. Expansion of Private Label Brands in Retail Stores

3.4. Trends (Consumer Behavior, Technology, New Product Development)

3.4.1. Growing Popularity of Infused Oils (Herb, Garlic, Truffle)

3.4.2. Technological Advances in Oil Refining for Healthier Product Lines

3.4.3. Shift Toward Sustainable and Eco-Friendly Packaging Solutions

3.4.4. Adoption of Health-Centric Labelling and Certifications (Organic, Keto, Vegan)

3.5. Government Regulations (FDA Regulations, Labeling, Import Restrictions, Trade Agreements)

3.5.1. U.S. FDA Nutrition Labeling Requirements for Oils

3.5.2. Import Regulations on Key Cooking Oil Products (Olive Oil, Palm Oil)

3.5.3. Regulations on Trans-Fat Content and Oil Composition

3.5.4. Trade Agreements Impacting Cooking Oil Imports and Exports

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Suppliers, Distributors, End Users, Regulatory Bodies)

3.8. Porters Five Forces (Competition, Supplier Bargaining Power, Buyer Bargaining Power, Threat of Substitution, Threat of New Entrants)

3.9. Competition Ecosystem (Market Concentration, Differentiation, Entry Barriers)

4.1. By Product Type (In Value and Volume %)

4.1.1. Vegetable Oils (Soybean, Canola, Corn)

4.1.2. Specialty Oils (Olive, Coconut, Avocado, Palm)

4.1.3. Blended Oils

4.1.4. Cold-Pressed Oils

4.2. By Source (In Value and Volume %)

4.2.1. Organic

4.2.2. Conventional

4.2.3. Non-GMO

4.3. By End-User (In Value and Volume %)

4.3.1. Household

4.3.2. HoReCa (Hotels, Restaurants, Catering)

4.3.3. Food Processing Industry

4.3.4. Retail

4.4. By Distribution Channel (In Value and Volume %)

4.4.1. Supermarkets and Hypermarkets

4.4.2. Online Channels

4.4.3. Specialty Stores

4.4.4. Direct to Consumer

4.5. By Region (In Value and Volume %)

4.5.1. U.S.

4.5.2. Canada

4.5.3. Mexico

5.1 Detailed Profiles of Major Companies

5.1.1. Archer Daniels Midland (ADM)

5.1.2. Cargill Incorporated

5.1.3. Bunge Limited

5.1.4. Wilmar International Limited

5.1.5. Conagra Brands

5.1.6. The J.M. Smucker Company

5.1.7. Unilever

5.1.8. Associated British Foods plc

5.1.9. Fuji Oil Holdings Inc.

5.1.10. Louis Dreyfus Company

5.1.11. Riceland Foods

5.1.12. Ventura Foods

5.1.13. Mazola

5.1.14. Nutiva

5.1.15. Spectrum Organic Products

5.2 Cross Comparison Parameters (Production Capacity, Sustainability Initiatives, Market Penetration, Brand Value, Product Portfolio, Geographical Footprint, R&D Investment, Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product Launches, Joint Ventures, Acquisitions)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. FDA Nutritional Labeling Standards

6.2. Compliance Requirements for Product Safety

6.3. Certification Processes (USDA Organic, Non-GMO Certification)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value and Volume %)

8.2. By Source (In Value and Volume %)

8.3. By End-User (In Value and Volume %)

8.4. By Distribution Channel (In Value and Volume %)

8.5. By Region (In Value and Volume %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

In the first phase, we develop an ecosystem map of the North America Cooking Oil Market, including all key stakeholders, such as manufacturers, suppliers, and retailers. This involves comprehensive desk research using government databases and proprietary resources to define the variables that affect market dynamics.

Historical data is collected and analyzed to understand the key trends and growth patterns in the North America cooking oil market. This includes evaluating market penetration, consumer preferences, and revenue generation from various product segments.

Interviews with industry experts, including oil manufacturers and retail distributors, are conducted to validate our market hypotheses. These insights help us refine our data and ensure the accuracy of our revenue and market share estimates.

In the final stage, we synthesize data from primary and secondary research to produce a comprehensive analysis of the market. Direct interactions with key market players further enhance the validity of our findings.

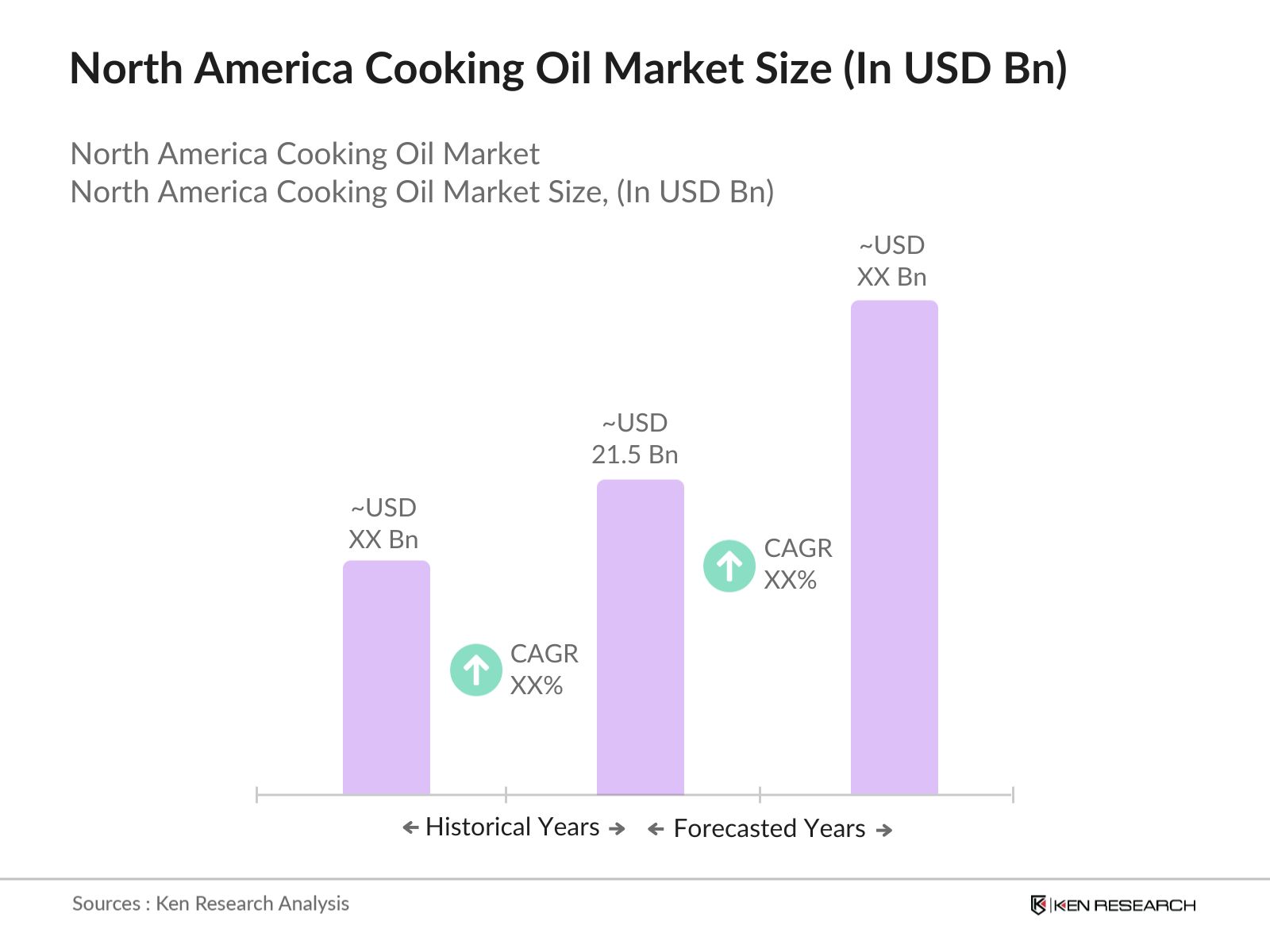

The North America cooking oil market was valued at USD 21.5 billion, driven by demand for both traditional oils like soybean and canola, as well as alternative oils such as olive and avocado.

Challenges in the North America cooking oil market include supply chain disruptions, fluctuating raw material costs, and the environmental concerns associated with large-scale oil production, particularly for palm oil.

Key players in the North America cooking oil market include Archer Daniels Midland (ADM), Cargill Incorporated, Bunge Limited, Wilmar International, and Conagra Brands, all of which dominate due to their extensive production capacities and strong distribution networks.

The North America cooking oil market is driven by increasing health consciousness among consumers, a shift toward healthier oil alternatives, and growing demand from the foodservice and food processing industries.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.