North America Critical Infrastructure Protection Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD4642

October 2024

93

About the Report

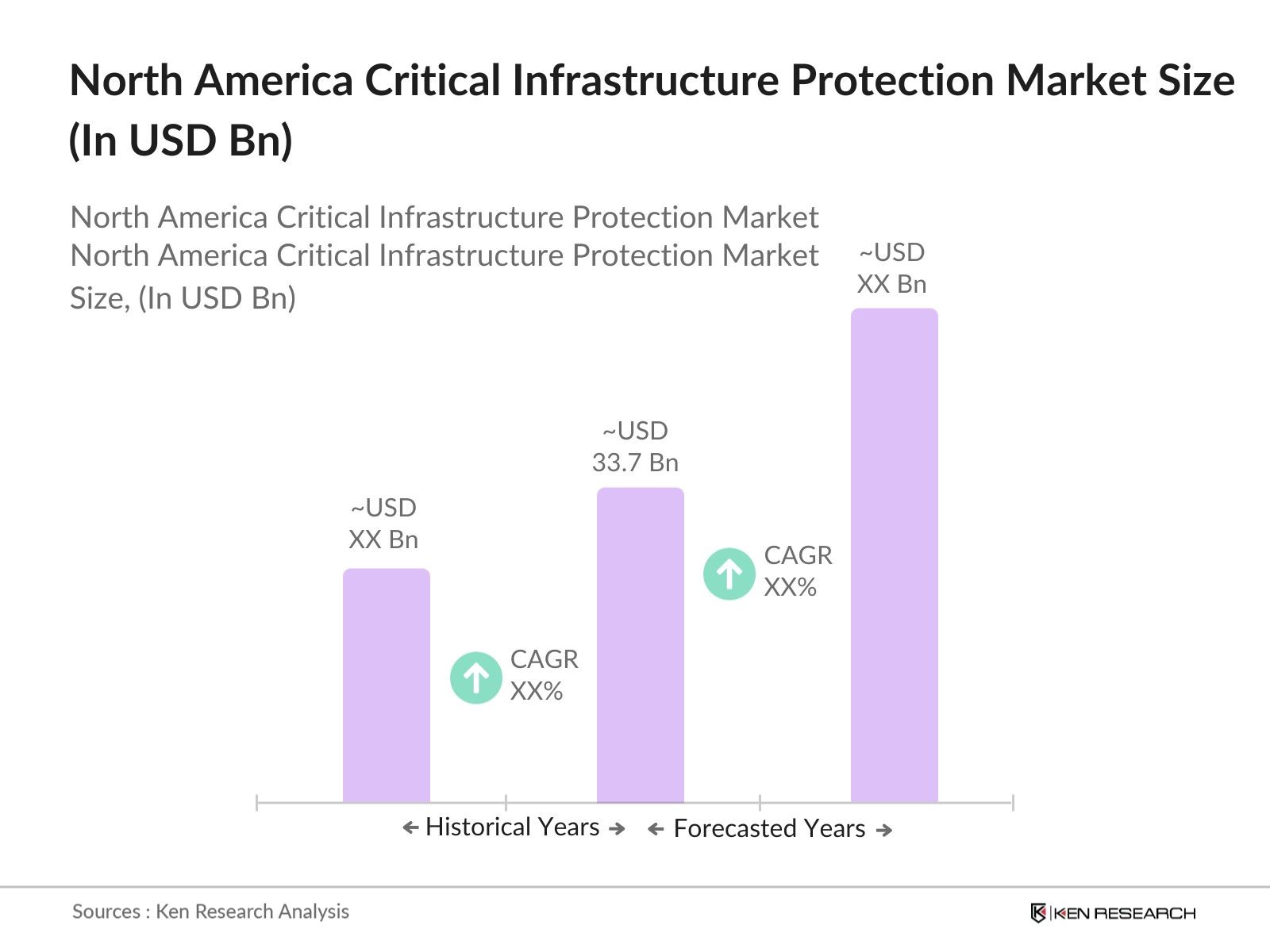

North America Critical Infrastructure Protection Market Overview

- The North America Critical Infrastructure Protection market is valued at USD 33.7 billion, driven by an increasing need to protect essential services such as energy, transportation, financial institutions, and healthcare systems from evolving threats. The rapid rise in cyber-attacks and physical security threats has spurred governments and private organizations to invest heavily in advanced infrastructure protection technologies, boosting market demand. This surge is further fueled by increasing digitalization across industries and stringent government regulations that mandate enhanced security protocols for critical infrastructure.

- Key regions driving the market include the United States and Canada, with the U.S. being a dominant player due to its large-scale investments in infrastructure and extensive technological advancements in cybersecurity and physical security systems. The presence of large critical infrastructure sectors like energy, telecommunications, and financial services has made North America a hotspot for infrastructure protection solutions. The U.S. government's emphasis on bolstering national security and protecting public services further solidifies the region's leadership in this space.

- Compliance with NERC-CIP (Critical Infrastructure Protection) standards is mandatory for all energy operators in North America, driving significant investments in cybersecurity and physical security measures. In 2023, over 1,500 energy companies were audited for compliance, with non-compliant firms facing fines of up to $1 million per day. These regulations are aimed at protecting the bulk power system from both physical and cyber threats, ensuring the security and reliability of the energy grid.

North America Critical Infrastructure Protection Market Segmentation

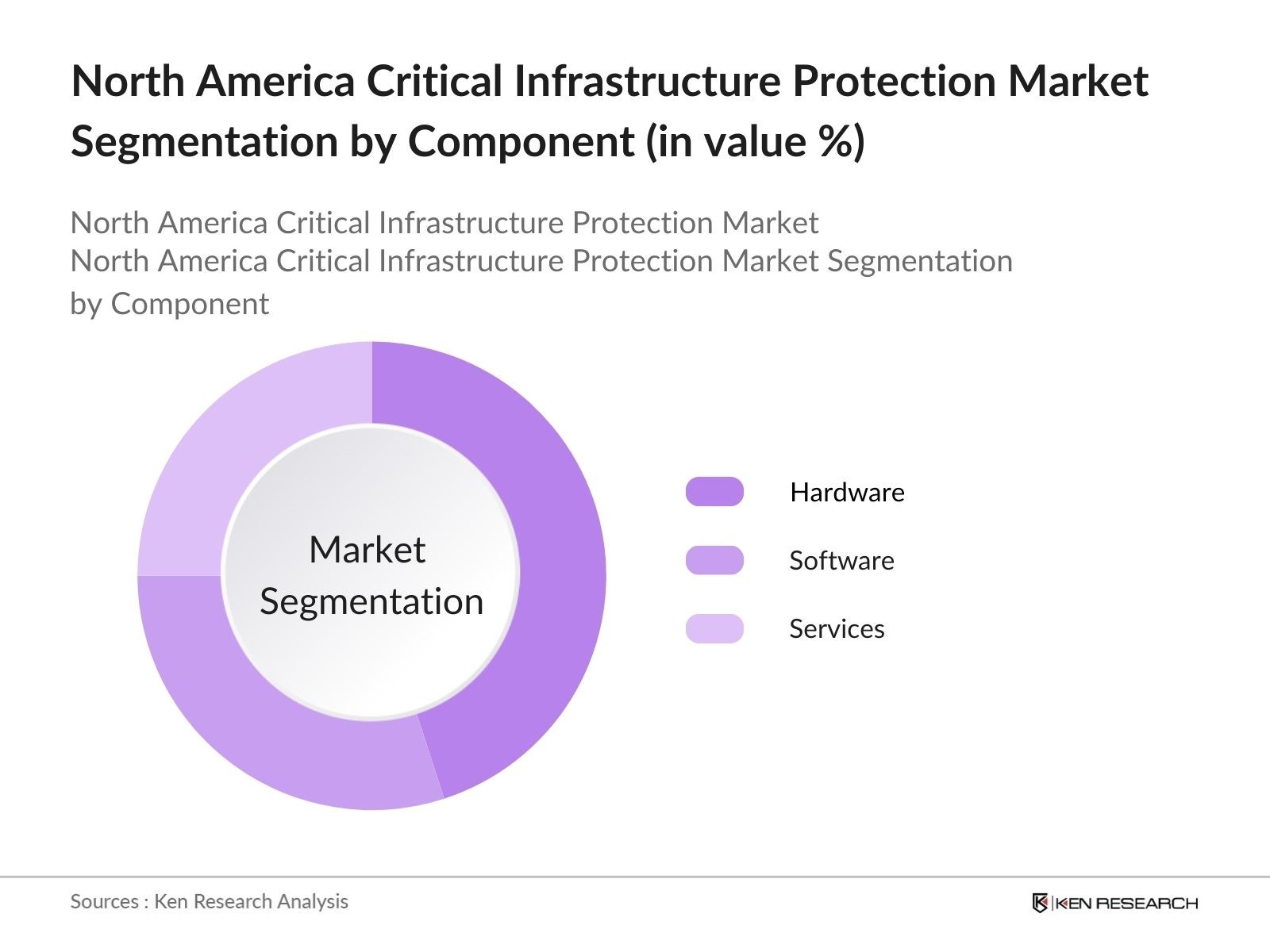

By Component: The market is segmented by component into hardware, software, and services. Hardware components, such as surveillance systems and sensors, dominate the market share, owing to the increasing need for real-time monitoring and advanced physical security mechanisms. The widespread adoption of smart surveillance solutions to monitor sensitive infrastructure like power grids and transportation networks has led to significant demand for high-quality hardware components. Moreover, innovations in video surveillance and IoT-connected sensors have further boosted this segment's dominance.

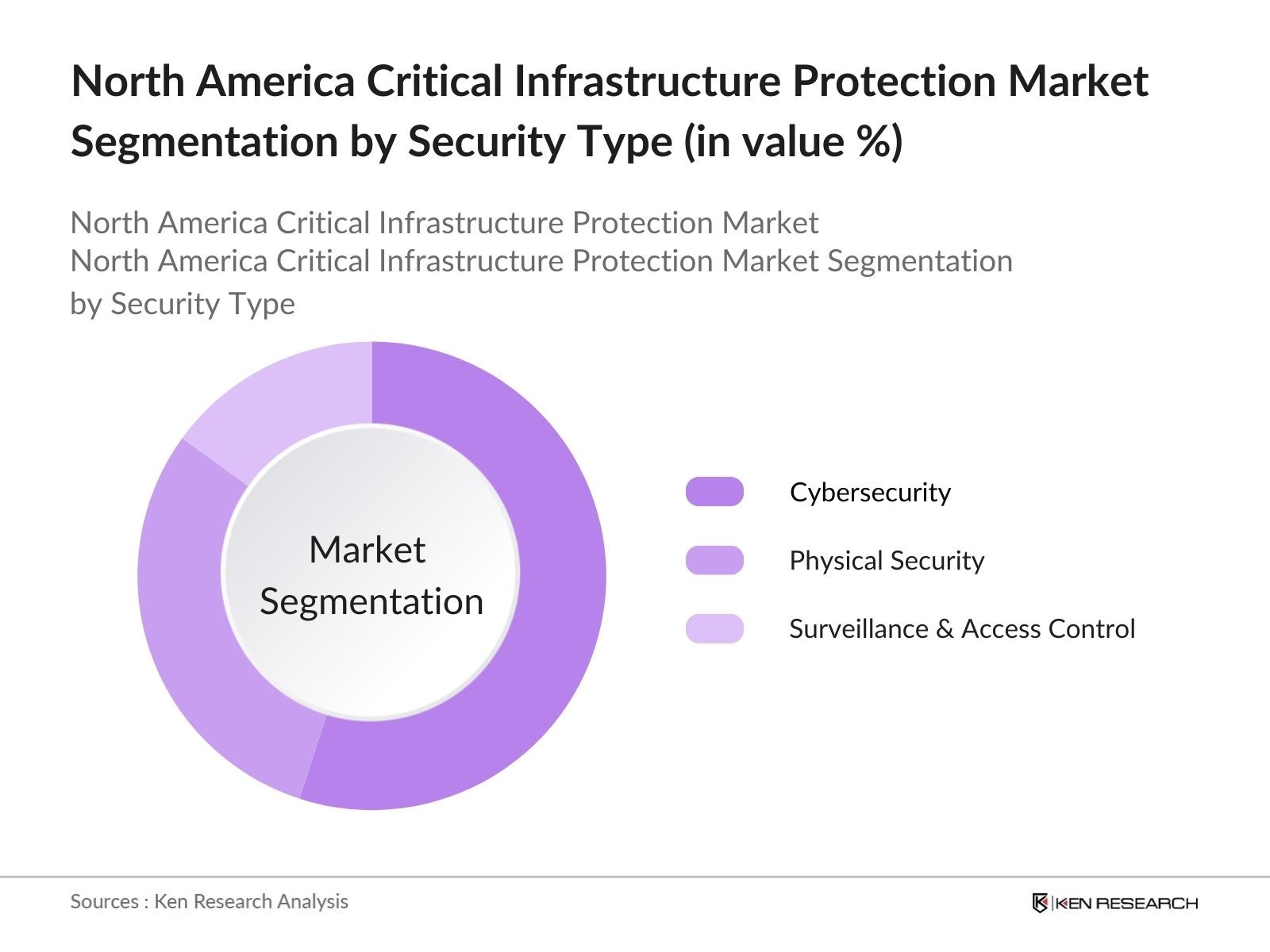

By Security Type: The market is segmented by security type into physical security, cybersecurity, and surveillance & access control. Cybersecurity holds the dominant market share due to the increasing number of cyber threats targeting essential services such as power grids, water systems, and financial institutions. Rising cyber-attacks, such as ransomware and phishing, which compromise sensitive data and disrupt critical operations, have made cybersecurity solutions indispensable. Key factors contributing to this dominance are advancements in encryption technologies, threat detection systems, and growing awareness of cybersecurity risks among public and private stakeholders.

North America Critical Infrastructure Protection Competitive Landscape

The North America Critical Infrastructure Protection market is dominated by several key players who offer advanced security solutions to safeguard essential services. The competitive landscape is characterized by the presence of global technology giants and specialized defense contractors. Companies are increasingly investing in new technologies such as artificial intelligence (AI), machine learning, and IoT to maintain their competitive edge. Mergers, acquisitions, and collaborations between leading security firms and governments are also shaping the market.

|

Company |

Established |

Headquarters |

Product Range |

Revenue (2023) |

No. of Employees |

Global Reach |

Local Market Share |

Distribution Network |

|

Raytheon Technologies Corp. |

1922 |

South Korea |

- |

- |

- |

- |

- |

- |

|

Northrop Grumman Corp. |

1939 |

USA |

- |

- |

- |

- |

- |

- |

|

Lockheed Martin Corp. |

1995 |

South Korea |

- |

- |

- |

- |

- |

- |

|

Honeywell International Inc. |

1906 |

Vietnam |

- |

- |

- |

- |

- |

- |

|

Cisco Systems Inc. |

1984 |

China |

- |

- |

- |

- |

- |

- |

North America Critical Infrastructure Protection Industry Analysis

Growth Drivers

-

Increased Cybersecurity Threats to Critical Infrastructure: Cyberattacks on critical infrastructure in North America have significantly increased, leading to concerns about the region’s resilience. In 2023, the U.S. Cybersecurity & Infrastructure Security Agency (CISA) reported over 3,000 significant cyber incidents targeting critical sectors like energy, healthcare, and finance. The growing use of digital technologies in critical systems makes them vulnerable, with cyberattacks costing over $2 trillion annually, disrupting essential services. This surge highlights the urgent need for advanced cybersecurity measures, particularly in safeguarding critical infrastructure such as energy grids and water supply systems.

-

Rising Concerns about Terrorism and Physical Security: Terrorist threats remain a key concern for North American infrastructure, especially in urban centers. The U.S. Department of Homeland Security allocated $615 million for terrorism-related infrastructure protection in 2023, focusing on transportation, power plants, and communications systems. The rise of domestic terrorism, in particular, has driven the need for enhanced physical security in critical sectors, with over 10,000 incidents recorded between 2022 and 2023. This funding and heightened awareness are driving investments in physical and digital protection systems for vital infrastructure.

-

Need for Resilience in Response to Natural Disasters: Natural disasters such as hurricanes, wildfires, and floods are intensifying in North America, with over 1,300 major disaster declarations made by FEMA between 2020 and 2023. This has prompted governments and private sectors to allocate significant resources towards building resilient critical infrastructure, particularly in vulnerable areas. In 2023, the U.S. government committed over $50 billion to resilience-building projects for energy grids, transportation systems, and emergency response facilities, ensuring the continuity of operations during catastrophic events.

Market Challenges

-

High Costs of Infrastructure Protection Solutions: The cost of securing critical infrastructure remains a major challenge, with an estimated $130 billion spent on infrastructure protection in North America in 2023 alone. These costs include investments in cybersecurity, physical security, and disaster resilience. While governments and large enterprises are able to invest, smaller entities often face budget constraints, leading to gaps in their protective measures. This disparity in resources poses a significant challenge to overall infrastructure security in the region.

-

Complexity in Meeting Regulatory Compliance: Meeting regulatory compliance is a complex and costly process for critical infrastructure operators in North America. The energy sector alone must comply with over 500 regulations across federal, state, and local levels, including NERC-CIP standards. Non-compliance can lead to penalties, with fines reaching up to $1 million per day for violations in some sectors. The regulatory environment is expected to tighten further with the introduction of new cybersecurity frameworks, adding additional compliance burdens.

North America Critical Infrastructure Protection Market Future Outlook

Over the next few years, the North America Critical Infrastructure Protection market is expected to experience robust growth driven by the continuous advancements in technology, particularly in cybersecurity and artificial intelligence. Government regulations mandating stricter security measures across energy, transportation, and communication sectors will play a crucial role in market expansion.

Future Market Opportunities

- Adoption of AI and Automation for Infrastructure Security: AI and automation technologies are becoming increasingly important in securing critical infrastructure in North America. In 2023, the U.S. government allocated $2 billion towards AI-based threat detection and response systems for critical sectors, including energy and transportation. AI is being used to monitor network traffic, identify anomalies, and predict potential cyber threats, reducing response times to incidents and improving overall security. The widespread adoption of these technologies offers opportunities for enhancing infrastructure protection.

- Expanding Public-Private Collaborations for Infrastructure Safety: Public-private partnerships (PPPs) are a key opportunity for improving critical infrastructure protection in North America. In 2023, the U.S. and Canadian governments launched joint initiatives with private firms, allocating $8 billion for infrastructure security upgrades. These collaborations aim to leverage the expertise and resources of the private sector in cybersecurity, physical security, and disaster resilience. As PPPs expand, the private sector’s role in critical infrastructure protection is expected to grow, enhancing the overall security landscape.

Scope of the Report

|

By Component |

Services Hardware Software |

|

By Security Type |

Physical Security Cybersecurity Surveillance and Access Control |

|

By Application |

Energy and Power Transportation Government and Defense Banking and Finance Healthcare |

|

By Vertical |

BFSI Oil and Gas Utilities Communication Manufacturing |

|

By Region |

North East West South |

Products

Key Target Audience

- Government and Regulatory Bodies (Department of Homeland Security, CISA, NERC)

- Critical Infrastructure Providers (Energy, Transportation, Communication)

- Private Sector Security Companies

- Technology Providers and System Integrators

- Venture Capital Firms

- Banks and Financial Institutes

- Defense Contractors

- Public-Private Partnership Firms

- Cybersecurity and Physical Security Equipment Manufacturers

Companies

North America Critical Infrastructure Protection Market Major Players

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Honeywell International Inc.

- Cisco Systems Inc.

- IBM Corporation

- BAE Systems

- General Dynamics Corporation

- Siemens AG

- Unisys Corporation

- Schneider Electric SE

- Thales Group

- Hewlett Packard Enterprise (HPE)

- Leidos Holdings Inc.

- Booz Allen Hamilton Inc.

Table of Contents

1. North America Critical Infrastructure Protection Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. North America Critical Infrastructure Protection Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. North America Critical Infrastructure Protection Market Analysis

3.1 Growth Drivers (Cybersecurity Threats, Terrorism, Natural Disasters, Critical Infrastructure Digitalization)

3.1.1 Increased Cybersecurity Threats to Critical Infrastructure

3.1.2 Rising Concerns about Terrorism and Physical Security

3.1.3 Need for Resilience in Response to Natural Disasters

3.1.4 Digital Transformation of Critical Infrastructure

3.2 Market Challenges (Budget Constraints, Regulatory Compliance, Integration with Legacy Systems)

3.2.1 High Costs of Infrastructure Protection Solutions

3.2.2 Complexity in Meeting Regulatory Compliance

3.2.3 Challenges in Integrating with Existing Legacy Systems

3.3 Opportunities (Emerging Technologies, Public-Private Partnerships, Cross-border Collaboration)

3.3.1 Adoption of AI and Automation for Infrastructure Security

3.3.2 Expanding Public-Private Collaborations for Infrastructure Safety

3.3.3 Increasing Cross-border Cooperation in Cybersecurity

3.4 Trends (IoT Integration, Cloud Security, AI in Threat Detection)

3.4.1 Increased Use of IoT Devices in Critical Infrastructure

3.4.2 Growing Cloud-based Security Solutions

3.4.3 AI-based Predictive Threat Detection and Response

3.5 Government Regulations (NERC-CIP Standards, Executive Orders on Cybersecurity, Data Privacy Regulations)

3.5.1 Compliance with NERC-CIP Standards for Energy Sector

3.5.2 Executive Orders Focusing on Cybersecurity Improvements

3.5.3 Data Privacy Regulations Impacting Infrastructure Protection

4. North America Critical Infrastructure Protection Market Segmentation

4.1 By Component (In Value %)

4.1.1 Hardware

4.1.2 Software

4.1.3 Services

4.2 By Security Type (In Value %)

4.2.1 Physical Security

4.2.2 Cybersecurity

4.2.3 Surveillance and Access Control

4.3 By Application (In Value %)

4.3.1 Energy and Power

4.3.2 Transportation

4.3.3 Government and Defense

4.3.4 Banking and Finance

4.3.5 Healthcare

4.4 By Vertical (In Value %)

4.4.1 BFSI

4.4.2 Oil and Gas

4.4.3 Utilities

4.4.4 Communication

4.4.5 Manufacturing

4.5 By Region (In Value %)

4.5.1 U.S.

4.5.2 Canada

4.5.3 Mexico

5. North America Critical Infrastructure Protection Market Competitive Analysis

5.1 Detailed Profiles of Major Competitors

5.1.1 Raytheon Technologies Corporation

5.1.2 Northrop Grumman Corporation

5.1.3 Lockheed Martin Corporation

5.1.4 Honeywell International Inc.

5.1.5 Cisco Systems Inc.

5.1.6 General Dynamics Corporation

5.1.7 IBM Corporation

5.1.8 BAE Systems

5.1.9 Leidos Holdings Inc.

5.1.10 Unisys Corporation

5.1.11 Schneider Electric SE

5.1.12 Booz Allen Hamilton Inc.

5.1.13 Thales Group

5.1.14 Hewlett Packard Enterprise (HPE)

5.1.15 Siemens AG

5.2 Cross Comparison Parameters (Market Share, Technology Expertise, Number of Patents, Key Partnerships, Financial Strength, Customer Base, Service Portfolio, R&D Capabilities)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. North America Critical Infrastructure Protection Market Regulatory Framework

6.1 Industry Standards (NIST, ISO, IEC)

6.2 Compliance Requirements (CISA, Federal Directives)

6.3 Certification Processes (Security Clearances, Risk Assessments)

7. North America Critical Infrastructure Protection Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. North America Critical Infrastructure Protection Future Market Segmentation

8.1 By Component (In Value %)

8.2 By Security Type (In Value %)

8.3 By Application (In Value %)

8.4 By Vertical (In Value %)

8.5 By Region (In Value %)

9. North America Critical Infrastructure Protection Market Analysts’ Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves developing a comprehensive map of key stakeholders within the North America Critical Infrastructure Protection market. Extensive desk research using a combination of public and proprietary databases helps in identifying critical factors influencing market dynamics, including government policies, technological advancements, and security threats.

Step 2: Market Analysis and Construction

This phase focuses on analyzing historical data, market penetration, and the relationship between critical infrastructure sectors and security providers. Evaluations of revenue streams, service quality statistics, and the impact of new security technologies are used to construct accurate market models.

Step 3: Hypothesis Validation and Expert Consultation

Interviews with industry experts via computer-assisted telephone interviews (CATIs) validate the hypotheses derived from initial research. These discussions provide valuable operational insights from security firms and critical infrastructure providers, allowing for the refinement of market estimates.

Step 4: Research Synthesis and Final Output

The final phase synthesizes all gathered data and expert opinions to produce a validated market report. Direct engagement with companies specializing in physical and cyber defense solutions helps verify the bottom-up analysis and ensures the comprehensiveness of the market study.

Frequently Asked Questions

01. How big is the North America Critical Infrastructure Protection Market?

The North America Critical Infrastructure Protection market is valued at USD 33.7 billion, driven by significant investments in cybersecurity and physical security solutions for sectors like energy, transportation, and healthcare.

02. What are the major challenges in the North America Critical Infrastructure Protection Market?

The major challenges include high costs associated with implementing advanced security solutions, meeting stringent regulatory compliance requirements, and integrating new technologies with legacy systems.

03. Who are the leading players in the North America Critical Infrastructure Protection Market?

Leading players include Raytheon Technologies Corporation, Northrop Grumman Corporation, Lockheed Martin Corporation, Honeywell International Inc., and Cisco Systems Inc., with expertise in both physical and cybersecurity solutions.

04. What drives the North America Critical Infrastructure Protection Market?

The market is driven by rising cyber threats, increased vulnerability of critical infrastructure sectors, and the growing need for integrated security solutions that protect both physical and digital assets.

05. What is the future outlook for the North America Critical Infrastructure Protection Market?

The market is expected to grow substantially due to advancements in AI, IoT, and cloud security solutions, alongside stricter government regulations aimed at protecting essential public and private infrastructure.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.