North America Data Acquisition Market Outlook to 2030

Region:Global

Author(s):Sanjna

Product Code:KROD6138

November 2024

99

About the Report

North America Data Acquisition Market Overview

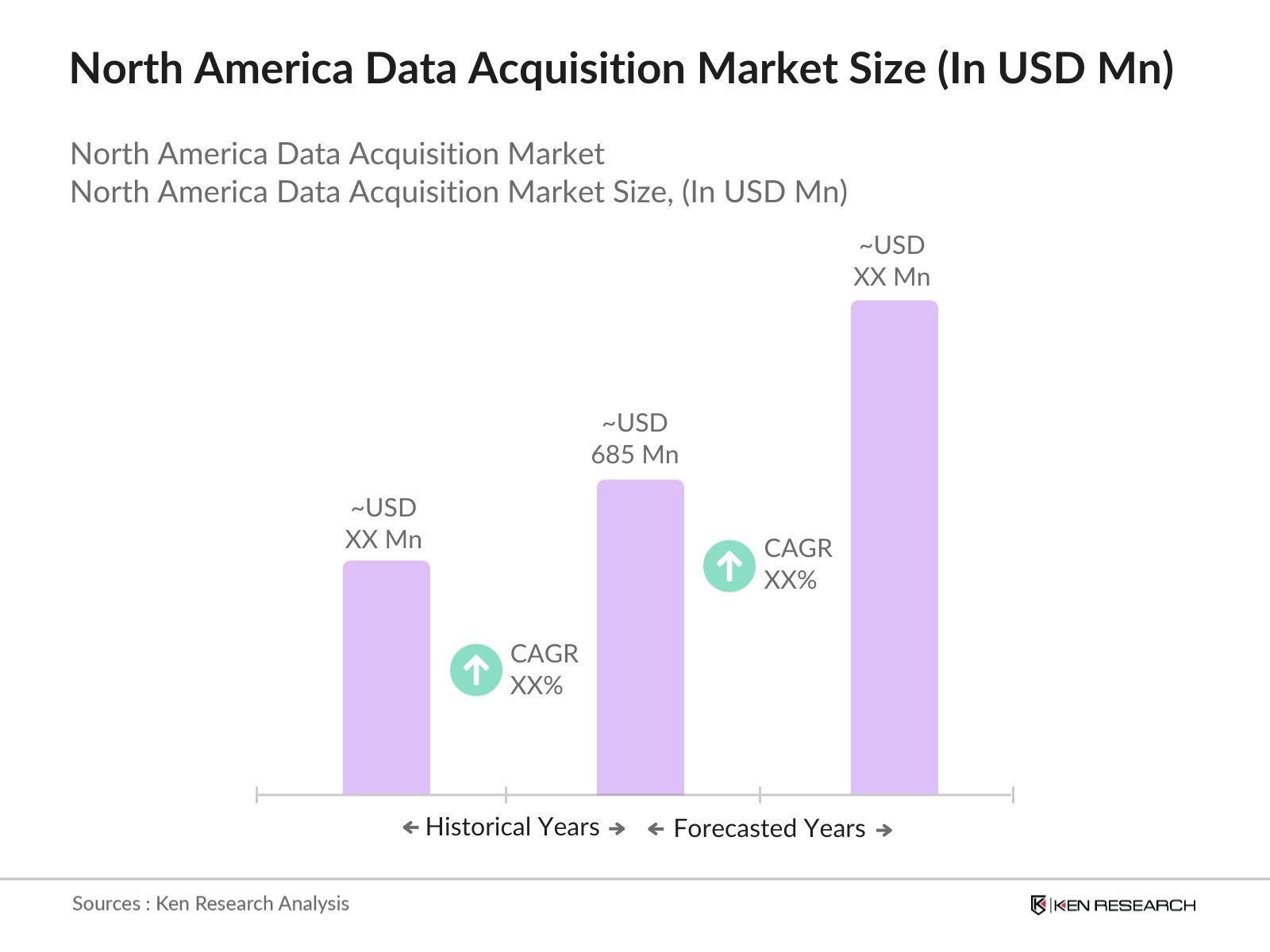

- The North America Data Acquisition (DAQ) Market is valued at USD 685 million based on a five-year historical analysis, driven by the increasing adoption of automation across industrial sectors, including manufacturing, energy, and automotive testing. The need for precise data collection and real-time monitoring systems is propelling the demand for advanced DAQ systems. Additionally, regulatory bodies in the U.S. are enforcing strict standards on data accuracy in sectors like healthcare and power generation, boosting market growth.

- Dominant countries in the market include the United States and Canada. The dominance of the U.S. stems from its well-established industrial base, technological innovation in automation, and significant investments in research and development (R&D) across sectors like aerospace, defense, and automotive. Canada, on the other hand, plays a pivotal role in the renewable energy sector, where data acquisition systems are essential for monitoring and controlling grid performance, enhancing the countrys market presence.

- Government regulations from agencies like OSHA and the EPA are enforcing stringent safety and efficiency standards across industries, driving the adoption of data acquisition systems. In 2024, over 90% of U.S. manufacturing companies are required to comply with federal safety standards, with real-time data acquisition systems used to monitor workplace safety and ensure compliance. Failure to adhere to these regulations can result in penalties exceeding $500,000 per violation, prompting industries to invest in advanced data monitoring systems.

North America Data Acquisition Market Segmentation

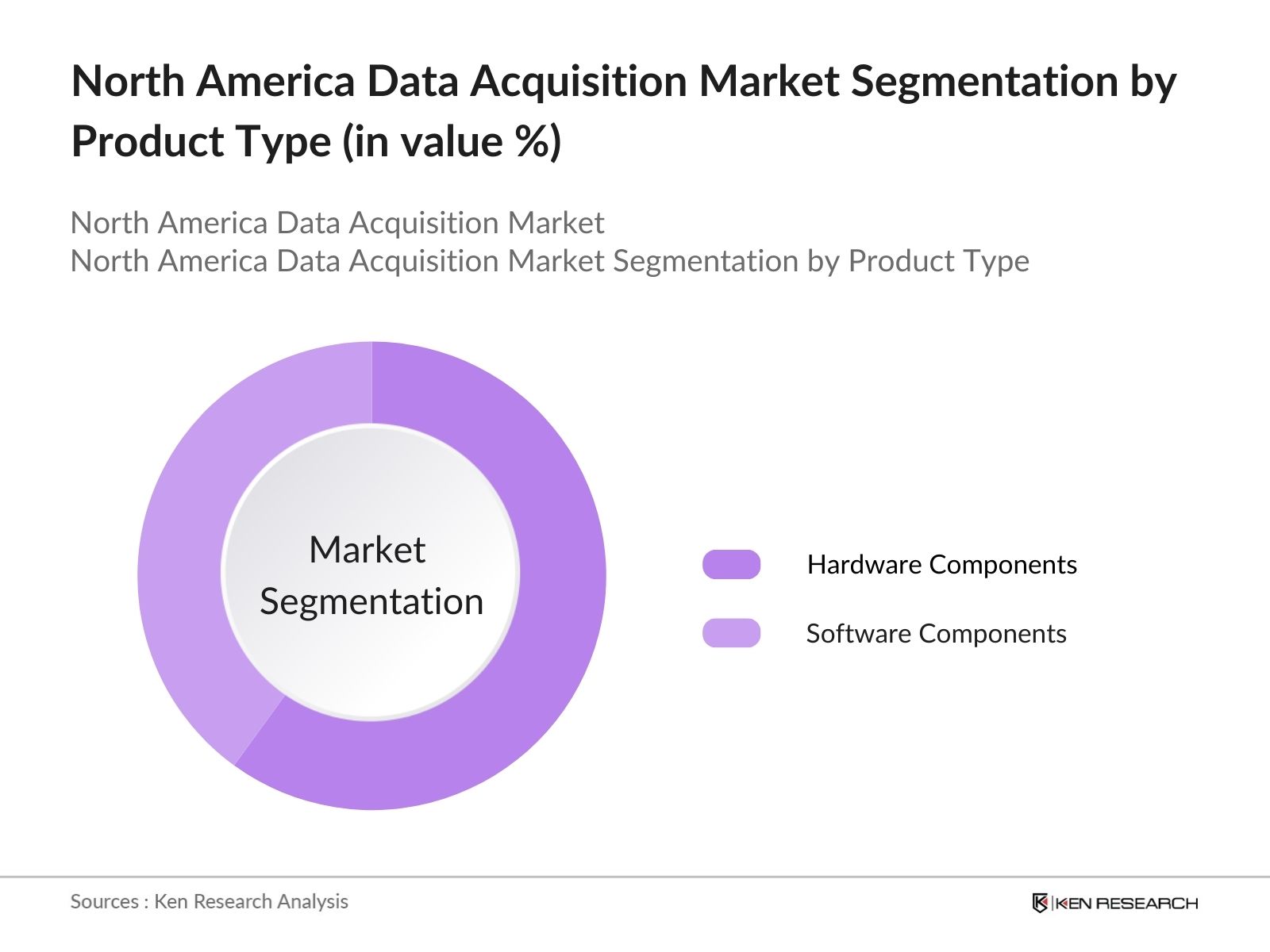

By Product Type: The North America Data Acquisition market is segmented by product type into hardware components (data loggers, signal conditioners, DAQ cards, and controllers) and software components (data analysis software, data visualization tools, and remote monitoring solutions). Recently, hardware components have a dominant market share in the region. This is primarily due to the increasing demand for data loggers and controllers in industrial automation, where accuracy and robustness are critical.

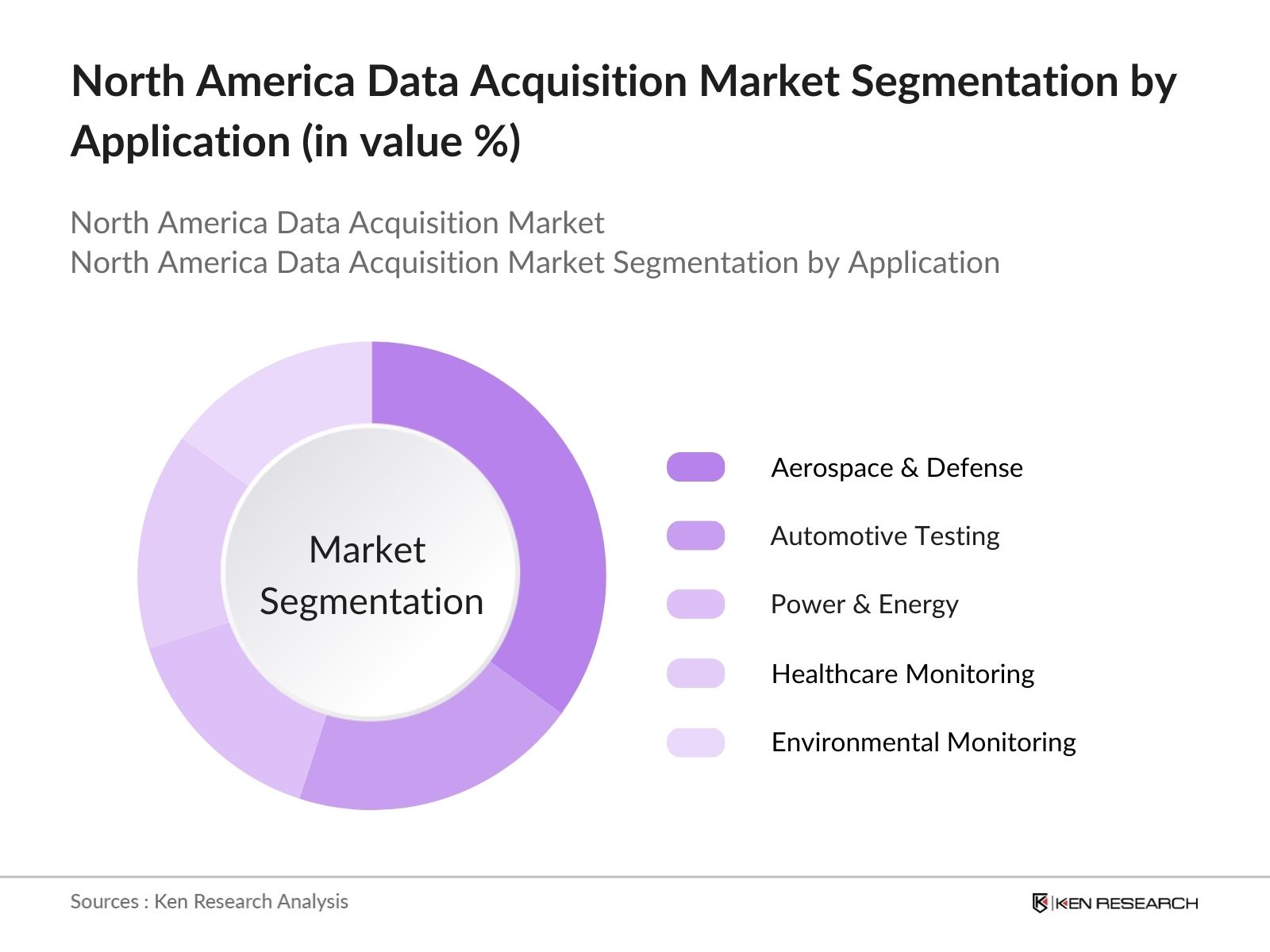

By Application: The North America Data Acquisition market is segmented by application into aerospace & defense, automotive testing, power & energy, healthcare monitoring, and environmental monitoring. Among these, aerospace & defense leads the market share, as the sector relies heavily on high-precision data acquisition systems for tasks such as flight testing, engine diagnostics, and spacecraft monitoring. The U.S. governments significant investments in defense R&D and space exploration have driven demand for advanced DAQ systems in this segment, cementing its position as a dominant sub-segment.

By Application: The North America Data Acquisition market is segmented by application into aerospace & defense, automotive testing, power & energy, healthcare monitoring, and environmental monitoring. Among these, aerospace & defense leads the market share, as the sector relies heavily on high-precision data acquisition systems for tasks such as flight testing, engine diagnostics, and spacecraft monitoring. The U.S. governments significant investments in defense R&D and space exploration have driven demand for advanced DAQ systems in this segment, cementing its position as a dominant sub-segment.

North America Data Acquisition Market Competitive Landscape

North America Data Acquisition Market Competitive Landscape

The North America Data Acquisition market is dominated by major global and regional players that contribute significantly to its development. These companies are pivotal due to their extensive product portfolios and consistent innovation in technology. The market remains concentrated, with a few key players having a large influence. National Instruments, for example, dominates the hardware space with its wide range of DAQ systems, while Honeywell excels in industrial applications and remote monitoring solutions.

|

Company Name |

Establishment Year |

Headquarters |

Employees |

Revenue |

DAQ Specialization |

Innovation Index |

Patent Holdings |

R&D Investment |

Global Presence |

|

National Instruments |

1976 |

Austin, TX, USA |

- |

- |

- |

- |

- |

- |

- |

|

Honeywell International |

1906 |

Charlotte, NC, USA |

- |

- |

- |

- |

- |

- |

- |

|

Yokogawa Electric Corp. |

1915 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

- |

|

General Electric |

1892 |

Boston, MA, USA |

- |

- |

- |

- |

- |

- |

- |

|

Keysight Technologies |

2014 |

Santa Rosa, CA, USA |

- |

- |

- |

- |

- |

- |

- |

North America Data Acquisition Market Analysis

Growth Drivers

- Expansion of Industrial IoT (IIoT): The adoption of Industrial IoT (IIoT) has rapidly accelerated across industries, driving demand for real-time data acquisition systems. In 2024, IIoT applications in manufacturing, utilities, and logistics are generating a vast volume of operational data, requiring high-precision data acquisition systems to improve productivity and operational efficiency. For instance, the manufacturing sectors IoT-connected devices are expected to surpass 8 billion units by the end of 2024. Government initiatives are further encouraging IIoT adoption across sectors.

- Rising Demand for Remote Monitoring and Control: Remote monitoring and control systems are increasingly crucial across industries like oil and gas, manufacturing, and power generation, contributing significantly to the demand for data acquisition systems. In 2024, approximately 75% of global companies in the utilities sector rely on data acquisition systems for remote monitoring of operations, reducing downtime and improving process control.

- Government Regulations Promoting Industrial Automation: In 2024, governments worldwide are implementing regulations to promote industrial automation, directly increasing demand for advanced data acquisition systems. For example, the U.S. governments "Smart Manufacturing Leadership Act" incentivizes factories to adopt automated data-driven processes, aiming to improve manufacturing efficiency by 10-20% by the years end. Similarly, European regulations push for integrating Industry 4.0 technologies, including mandatory real-time data reporting and monitoring systems, especially in high-risk industries like pharmaceuticals and energy.

Challenges

- High Initial Setup Costs: Data acquisition systems often come with significant upfront costs, making it challenging for small to medium-sized enterprises (SMEs) to adopt these technologies. In 2024, the average cost of implementing a basic data acquisition system across industries is estimated at around $50,000 per site, with advanced systems surpassing $100,000. This cost includes sensors, installation, and integration with existing infrastructure. The cost barrier is especially pronounced in developing economies, where capital investment in automation technologies remains limited.

- Complex Integration with Legacy Systems: Integrating modern data acquisition systems with legacy infrastructure poses significant challenges for industries with outdated equipment. In 2024, nearly 40% of industrial facilities worldwide report difficulties in seamlessly integrating new data acquisition technologies with existing systems, causing delays in deployment and increased operational costs. In sectors like manufacturing and energy, the transition to smart data-driven operations requires significant re-engineering of existing processes.

North America Data Acquisition Market Future Outlook

North America Data Acquisition market is expected to witness significant growth, driven by the increasing adoption of automation technologies in industries such as manufacturing, aerospace, and energy. The shift toward real-time monitoring and control, along with advancements in wireless data acquisition systems, will further propel market expansion. Government initiatives promoting industrial automation and stringent regulatory standards in healthcare and energy sectors will continue to be key drivers.

Market Opportunities

- Rising Demand for Cloud-Based Data Acquisition Solutions: Cloud-based data acquisition systems are gaining traction as they offer scalability, flexibility, and real-time data access. In 2024, the global market for cloud-based industrial data acquisition systems is expected to surpass 400 million connected devices. The power generation sector is leading this trend, with cloud-based systems used to monitor energy output and equipment performance remotely, reducing downtime and improving operational efficiency.

- Growth in Renewable Energy Projects: The renewable energy sector is driving the demand for data acquisition systems, particularly in wind and solar energy projects. In 2024, global investments in renewable energy are expected to exceed $500 billion, with data acquisition systems playing a critical role in monitoring and optimizing energy output. The wind energy sector, in particular, relies on real-time data monitoring systems to improve turbine performance and reduce maintenance costs. This demand presents significant opportunities for data acquisition system providers.

Scope of the Report

|

Segment |

Sub-Segment |

|

By Product Type |

Hardware Components |

|

Software Components |

|

|

By Connectivity Type |

Wired Data Acquisition Systems |

|

Wireless Data Acquisition Systems |

|

|

By Application |

Aerospace & Defense |

|

Automotive Testing |

|

|

Power & Energy |

|

|

Healthcare Monitoring |

|

|

Environmental Monitoring |

|

|

By Industry Vertical |

Industrial Automation |

|

Manufacturing |

|

|

Telecommunications |

|

|

Oil & Gas |

|

|

By Region |

United States |

|

Canada |

|

|

Mexico |

Products

Key Target Audience

Aerospace & Defense Contractors

Automotive Testing Facilities

Power Generation and Utility Companies

Industrial Automation Manufacturers

Healthcare Monitoring Providers

Renewable Energy Project Developers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (U.S. Environmental Protection Agency, Occupational Safety and Health Administration)

Companies

Players Mentioned in the Report

National Instruments

Honeywell International Inc.

Yokogawa Electric Corporation

General Electric

Keysight Technologies

Siemens AG

ABB Ltd.

Schneider Electric SE

Teledyne Technologies Incorporated

HBM (Hottinger Baldwin Messtechnik)

Table of Contents

1. North America Data Acquisition Market Overview 1

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Data Acquisition Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Data Acquisition Market Analysis

3.1. Growth Drivers

3.1.1. Expansion of Industrial IoT (IIoT)

3.1.2. Rising Demand for Remote Monitoring and Control

3.1.3. Government Regulations Promoting Industrial Automation

3.1.4. Increased Adoption in Automotive Testing

3.2. Market Challenges

3.2.1. High Initial Setup Costs

3.2.2. Complex Integration with Legacy Systems

3.2.3. Data Security Concerns

3.2.4. Limited Availability of Skilled Workforce

3.3. Opportunities

3.3.1. Rising Demand for Cloud-Based Data Acquisition Solutions

3.3.2. Development of Wireless Data Acquisition Technologies

3.3.3. Growth in Renewable Energy Projects

3.3.4. Expanding Applications in Aerospace & Defense

3.4. Trends

3.4.1. Adoption of Edge Data Acquisition Solutions

3.4.2. Integration with Artificial Intelligence for Predictive Maintenance

3.4.3. Growing Use of Portable Data Acquisition Systems

3.4.4. Data Acquisition as a Service (DaaS) Business Models

3.5. Government Regulation

3.5.1. Federal Safety and Efficiency Standards (OSHA, EPA Compliance)

3.5.2. Mandates for Data Reporting in Power Generation

3.5.3. Standards for Cybersecurity in Industrial Applications

3.5.4. Regulations Promoting Smart Grid Deployments

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. North America Data Acquisition Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Hardware Components

4.1.2. Software Components

4.2. By Connectivity Type (In Value %)

4.2.1. Wired Data Acquisition Systems

4.2.2. Wireless Data Acquisition Systems

4.3. By Application (In Value %)

4.3.1. Aerospace & Defense

4.3.2. Automotive Testing

4.3.3. Power & Energy

4.3.4. Healthcare Monitoring

4.3.5. Environmental Monitoring

4.4. By Industry Vertical (In Value %)

4.4.1. Industrial Automation

4.4.2. Manufacturing

4.4.3. Telecommunications

4.4.4. Oil & Gas

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Data Acquisition Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. National Instruments

5.1.2. Honeywell International Inc.

5.1.3. Yokogawa Electric Corporation

5.1.4. General Electric

5.1.5. Keysight Technologies

5.1.6. Siemens AG

5.1.7. ABB Ltd.

5.1.8. Schneider Electric SE

5.1.9. HBM (Hottinger Baldwin Messtechnik)

5.1.10. Teledyne Technologies Incorporated

5.2 Cross Comparison Parameters (Market Share, Product Portfolio, Innovation Index, Customer Base, Revenue, Geographic Reach, Acquisition Strategies, Patent Holdings)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Data Acquisition Market Regulatory Framework

6.1. Data Acquisition Standards (IEEE 488, IEC 61131-3)

6.2. Compliance Requirements for Industrial Control Systems (ICS)

6.3. Certifications for Safety and Environmental Standards (ISO 9001, ISO 14001)

7. North America Data Acquisition Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Data Acquisition Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Connectivity Type (In Value %)

8.3. By Application (In Value %)

8.4. By Industry Vertical (In Value %)

8.5. By Region (In Value %)

9. North America Data Acquisition Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the North America Data Acquisition Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the North America Data Acquisition Market. This includes assessing market penetration, the ratio of product types to industry verticals, and the resultant revenue generation. Furthermore, an evaluation of sales performance statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple data acquisition system manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the North America Data Acquisition Market.

Frequently Asked Questions

01. How big is the North America Data Acquisition Market?

The North America Data Acquisition market is valued at USD 685 million, driven by the increasing adoption of automation across various industrial sectors, particularly in manufacturing and aerospace.

02. What are the challenges in the North America Data Acquisition Market?

Challenges in North America Data Acquisition market include high initial setup costs, complex integration with legacy systems, and concerns around data security, which affect the broader adoption of data acquisition solutions in smaller enterprises.

03. Who are the major players in the North America Data Acquisition Market?

Key players in North America Data Acquisition market include National Instruments, Honeywell International, Yokogawa Electric Corporation, General Electric, and Keysight Technologies. These companies dominate the market due to their extensive product portfolios and continuous innovation in DAQ technologies.

04. What are the growth drivers of the North America Data Acquisition Market?

North America Data Acquisition market is driven by the expansion of industrial automation, rising demand for real-time monitoring systems, and government regulations promoting efficiency and safety in industrial operations.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.