North America Digital Signature Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD4160

October 2024

97

About the Report

North America Digital Signature Market Overview

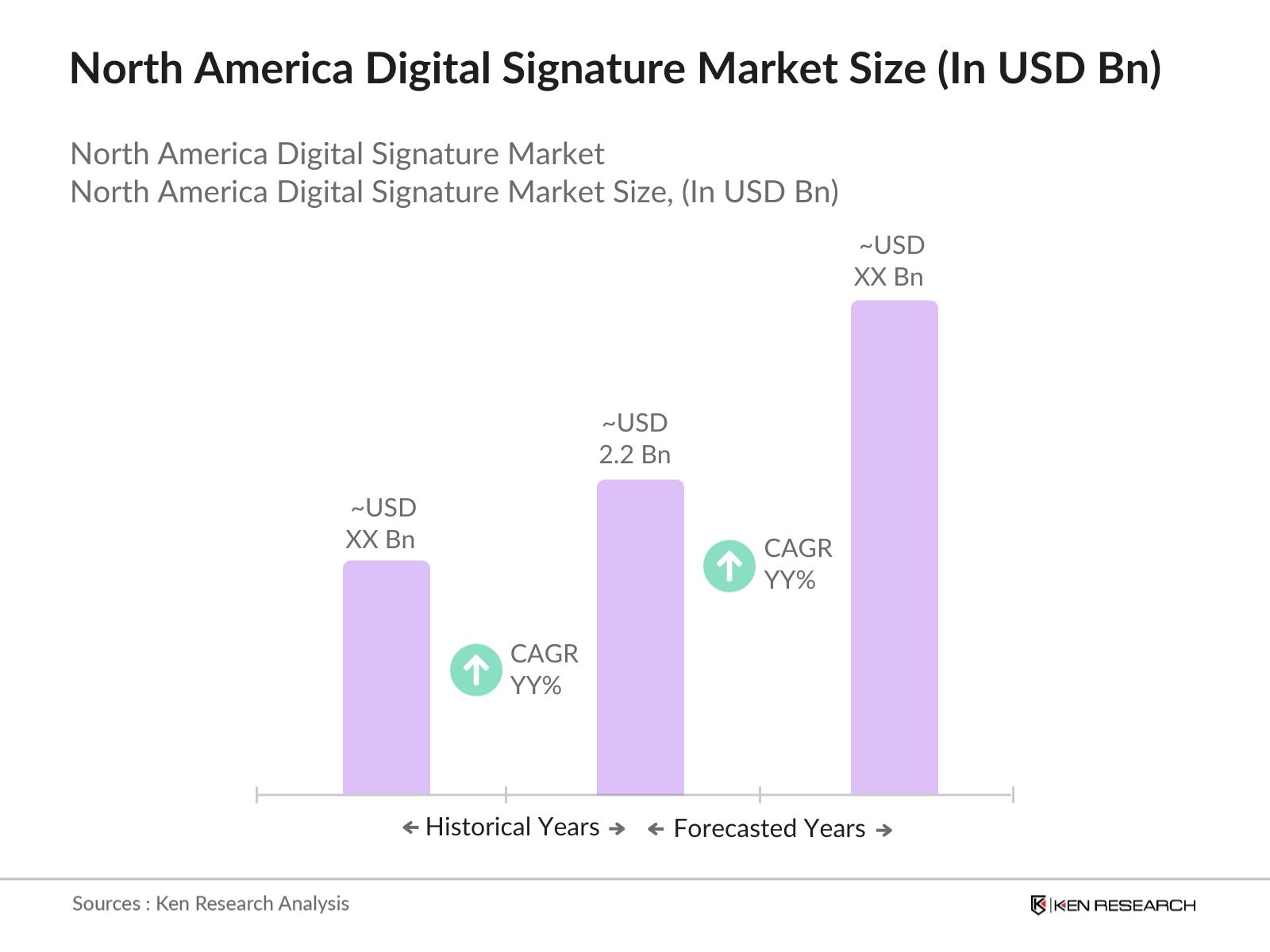

- The North America Digital Signature market is valued at USD 2.2 billion, based on a five-year historical analysis. This growth has been primarily driven by the rising demand for secure digital transactions, coupled with stringent regulations regarding digital documentation and electronic signatures, such as the E-Sign Act. The necessity for remote work solutions, especially in the post-pandemic era, has also fueled the adoption of digital signatures across industries, particularly in BFSI, healthcare, and government sectors.

- The United States dominates the market due to its advanced technological infrastructure, strong regulatory framework, and widespread digital transformation across industries. Major cities like New York, Los Angeles, and Chicago lead in the adoption of digital signatures owing to their concentration of financial institutions, healthcare providers, and large corporations that require secure and efficient document authentication solutions.

- In 2024, the U.S. government launched its updated National Cybersecurity Strategy, which emphasizes the adoption of secure digital signature technologies across federal agencies. This initiative requires all government bodies to implement secure electronic signature solutions for internal and external document handling, with the aim of improving data security and reducing the risk of cyberattacks.

North America Digital Signature Market Segmentation

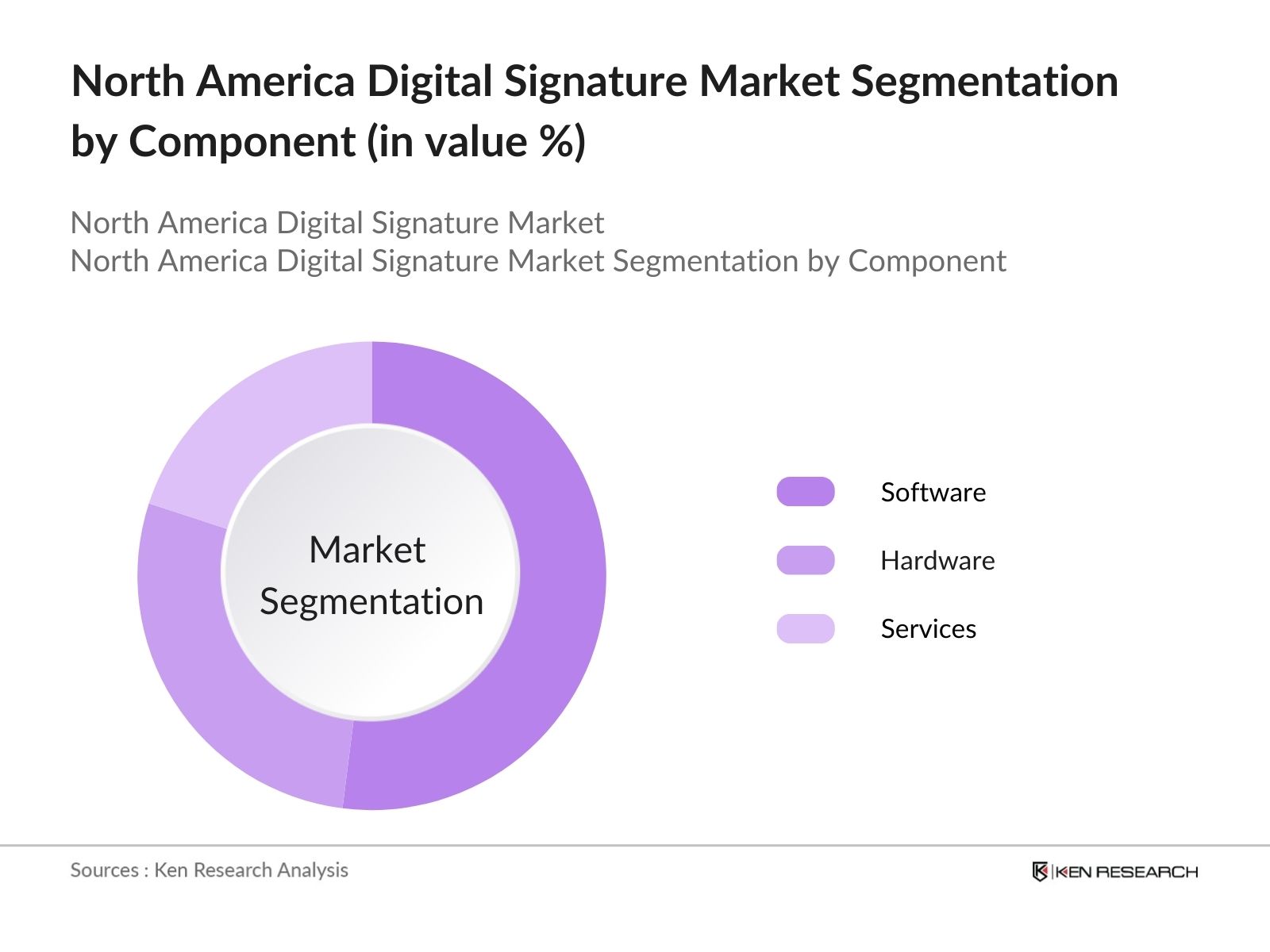

By Component: The market is segmented by component into software, hardware, and services. Software solutions have held a dominant market share under the component segmentation due to the increasing demand for cloud-based solutions and the shift towards Software-as-a-Service (SaaS) platforms. Companies are moving away from physical hardware solutions towards more scalable and cost-effective software platforms that integrate with their existing digital ecosystems, driving the dominance of the software sub-segment.

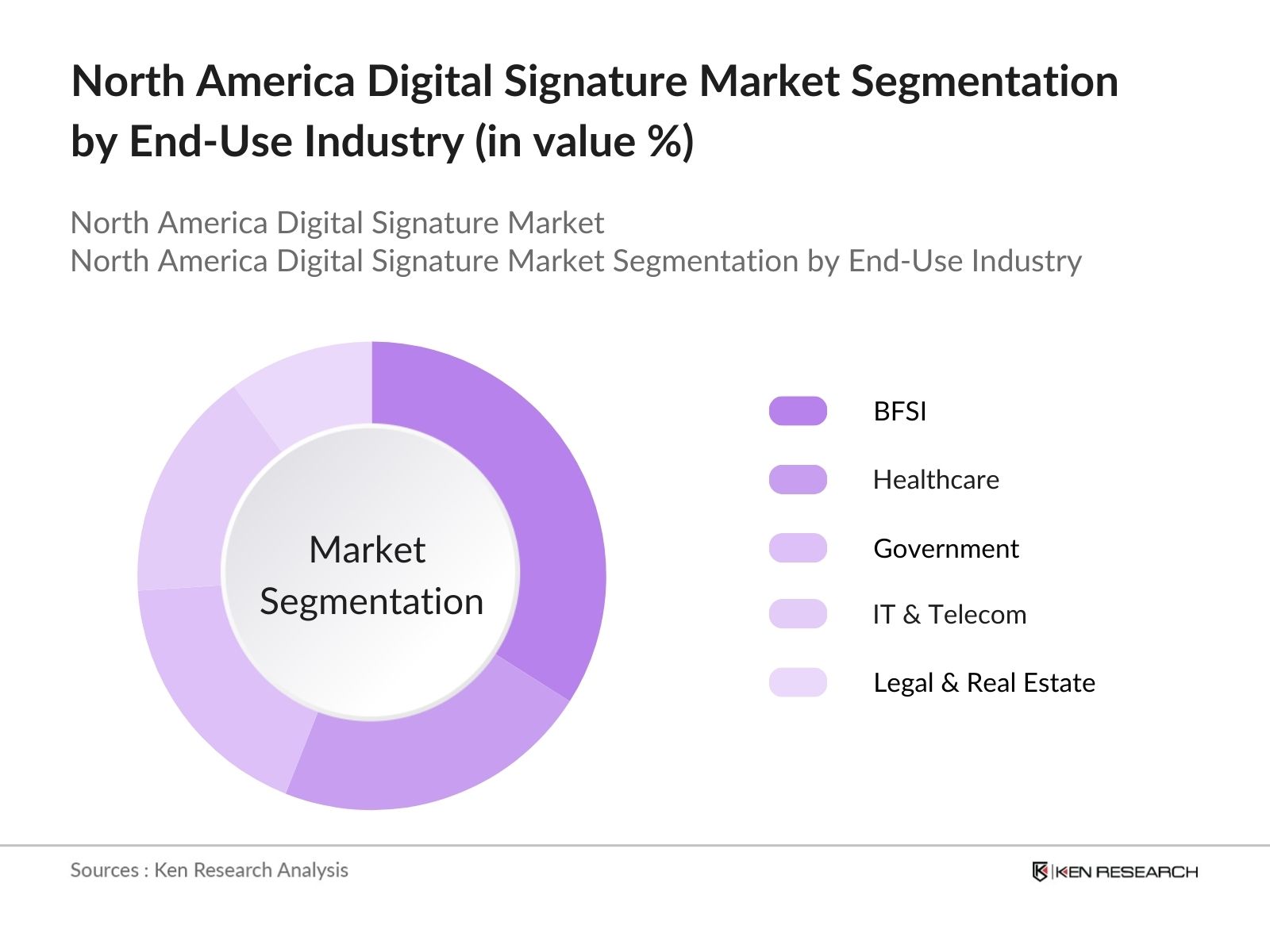

By End-Use Industry: The market is also segmented by end-use industries, which include BFSI, healthcare, government, IT & telecom, and legal & real estate. The BFSI sector dominates this segmentation, driven by the need for secure, legally binding digital documentation in financial transactions. With increasing online banking activities, financial institutions are adopting digital signatures to ensure the authenticity and security of documents, contracts, and agreements, thereby maintaining the integrity of their operations and compliance with regulations.

North America Digital Signature Market Competitive Landscape

The market is dominated by a few major players, including global companies like Adobe and DocuSign, which have established strong positions in the market through their innovative solutions and extensive customer bases. These companies, along with emerging players such as Thales and OneSpan, continue to shape the competitive landscape by offering solutions that meet regulatory standards and cater to various industry-specific needs.

|

Company |

Established |

Headquarters |

Revenue (USD Bn) |

Market Reach |

R&D Investments |

Employee Count |

Major Products |

|

Adobe Inc. |

1982 |

San Jose, USA |

|||||

|

DocuSign, Inc. |

2003 |

San Francisco, USA |

|||||

|

OneSpan Inc. |

1991 |

Chicago, USA |

|||||

|

Thales Group |

2000 |

Paris, France |

|||||

|

SIGNiX |

2002 |

Chattanooga, USA |

North America Digital Signature Market Analysis

Market Growth Drivers

- Government Regulations Promoting Digital Adoption: The market is primarily driven by stringent government regulations aimed at promoting digital transactions. In 2024, the U.S. government has mandated that over 1,200 federal agencies adopt digital signatures to enhance security and efficiency. The implementation of the ESIGN Act and Uniform Electronic Transactions Act (UETA) ensures that digital signatures are recognized legally across sectors, making the adoption mandatory for many industries such as healthcare, financial services, and insurance, where secure documentation is essential.

- Remote Working Culture: The surge in remote working across North America is a major growth driver for the market. As of 2024, more than 60 million workers in the U.S. alone are working remotely, which increases the demand for secure and efficient methods of signing contracts, agreements, and business documents. Digital signatures have become indispensable for organizations looking to maintain workflow continuity and document security while allowing employees to work from distributed locations across the country.

- Cybersecurity Concerns: The rise in cyber threats has led to an increasing focus on digital security, further driving the adoption of digital signatures. In 2024, North American businesses are estimated to face cybercrime costs. Digital signatures, which provide encryption and authentication, are being widely adopted as part of cybersecurity strategies in sectors such as banking, healthcare, and government. These sectors are particularly vulnerable to data breaches and rely on secure digital signature solutions to protect sensitive information.

Market Challenges

- Regulatory Complexity Across Different Jurisdictions: One of the major challenges facing the market is the complexity of complying with varying state and federal regulations. In 2024, there are over 50 distinct digital signature regulations across North American states, leading to inconsistencies in adoption. Businesses that operate across multiple states must navigate different laws, leading to slower adoption rates and increased compliance costs.

- Lack of Digital Literacy Among End-Users: A portion of the North American population, particularly in rural areas, lacks the digital literacy needed to adopt and use digital signature technology effectively. In 2024, around 30 million people in the U.S. are considered digitally illiterate, making it difficult for organizations to implement digital solutions that require a certain level of technical understanding. This digital divide hinders the widespread use of digital signatures in sectors like healthcare, government services, and local businesses that rely on paper-based systems.

North America Digital Signature Market Future Outlook

Over the next five years, the North America Digital Signature industry is expected to show growth, driven by increasing digital transformation initiatives, advancements in authentication technologies, and the growing demand for secure, paperless workflows. The ongoing expansion of e-commerce and digital banking in North America will also contribute to market growth.

Future Market Opportunities

- Increased Adoption of AI and Blockchain for Secure Signatures: In the next five years, AI and blockchain technologies will play a pivotal role in enhancing the security of digital signatures in North America. By 2029, most digital signature solutions are expected to integrate AI-based authentication, providing real-time fraud detection and improving identity verification processes. Blockchain will ensure tamper-proof document authentication, particularly in sectors like government, healthcare, and finance.

- Expansion into Healthcare Sector: Over the next five years, digital signatures will see increased adoption in the North American healthcare sector, driven by the need for secure electronic health records (EHR). By 2029, digital signatures will be widely used to authenticate medical prescriptions, patient consent forms, and insurance claims, streamlining healthcare processes. This expansion is expected to be supported by federal healthcare regulations, making digital signatures mandatory for certain medical transactions.

Scope of the Report

|

Component |

Software Hardware Services |

|

Deployment Type |

On-Premise Cloud-Based |

|

End-Use Industry |

BFSI Healthcare Government IT & Telecom Legal & Real Estate |

|

Solution Type |

Public Key Infrastructure (PKI) Multi-Factor Authentication Signature Verification Identity Management |

|

Region |

U.S. Canada |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

BFSI Institutions

Healthcare Providers

Government Agencies (U.S. Department of Commerce, National Institute of Standards and Technology)

IT & Telecom Companies

Legal & Real Estate Firms

Cloud Service Providers

Investments and Venture Capitalist Firms

Companies

Players Mentioned in the Report:

Adobe Inc.

DocuSign, Inc.

OneSpan Inc.

Thales Group

SIGNiX

Zoho Corporation Pvt. Ltd.

Entrust Corporation

Ascertia

Gemalto N.V.

Secured Signing

HelloSign (Dropbox)

GlobalSign

eSignLive (Vasco Data Security)

DigiCert

IdenTrust, Inc.

Table of Contents

1. North America Digital Signature Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Digital Signature Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Digital Signature Market Analysis

3.1. Growth Drivers

3.1.1. Regulatory Compliance (E-Sign Act, UETA)

3.1.2. Increasing Adoption in BFSI

3.1.3. Digital Transformation in Enterprises

3.1.4. Demand for Remote Work Solutions

3.2. Market Challenges

3.2.1. Security Concerns and Cyber Threats

3.2.2. Initial Deployment Costs

3.2.3. Lack of Awareness in SMEs

3.2.4. Complex Regulatory Frameworks

3.3. Opportunities

3.3.1. Integration with Blockchain Technology

3.3.2. Expansion in E-Commerce and Healthcare Sectors

3.3.3. Strategic Partnerships and Collaborations

3.3.4. Rising Demand for Cloud-Based Solutions

3.4. Trends

3.4.1. Increasing Adoption of Multi-Factor Authentication

3.4.2. Rise of Paperless Workflow Solutions

3.4.3. Deployment of AI and Machine Learning in Digital Signatures

3.4.4. Growth in Mobile-Based Digital Signature Solutions

3.5. Government Regulation

3.5.1. E-Sign Act Compliance

3.5.2. UETA and Global Digital Signature Standards

3.5.3. Data Privacy Regulations (GDPR, CCPA)

3.5.4. Digital Identity Verification Initiatives

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. North America Digital Signature Market Segmentation

4.1. By Component (In Value %)

4.1.1. Software

4.1.2. Hardware

4.1.3. Services

4.2. By Deployment Type (In Value %)

4.2.1. On-Premise

4.2.2. Cloud-Based

4.3. By End-Use Industry (In Value %)

4.3.1. BFSI

4.3.2. Healthcare

4.3.3. Government

4.3.4. IT & Telecom

4.3.5. Legal & Real Estate

4.4. By Solution Type (In Value %)

4.4.1. Public Key Infrastructure (PKI)

4.4.2. Multi-Factor Authentication

4.4.3. Signature Verification

4.4.4. Identity Management

4.5. By Region (In Value %)

4.5.1. U.S.

4.5.2. Canada

5. North America Digital Signature Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Adobe Inc.

5.1.2. DocuSign, Inc.

5.1.3. OneSpan Inc.

5.1.4. Thales Group

5.1.5. SIGNiX

5.1.6. Zoho Corporation Pvt. Ltd.

5.1.7. Entrust Corporation

5.1.8. Ascertia

5.1.9. Gemalto N.V.

5.1.10. Secured Signing

5.1.11. HelloSign (Dropbox)

5.1.12. GlobalSign

5.1.13. eSignLive (Vasco Data Security)

5.1.14. DigiCert

5.1.15. IdenTrust, Inc.

5.2. Cross Comparison Parameters (Revenue, Headquarters, Inception Year, Employee Count, R&D Investments, Market Share, Service Range, Geographical Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Digital Signature Market Regulatory Framework

6.1. Compliance with National and International Standards

6.2. Certification Processes

6.3. Digital Authentication Requirements

7. North America Digital Signature Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Digital Signature Future Market Segmentation

8.1. By Component (In Value %)

8.2. By Deployment Type (In Value %)

8.3. By End-Use Industry (In Value %)

8.4. By Solution Type (In Value %)

8.5. By Region (In Value %)

9. North America Digital Signature Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the key factors influencing the North America Digital Signature market. Through extensive desk research and analysis of secondary databases, we outline the ecosystem of stakeholders and relevant trends. The main objective is to determine the core variables such as technology trends, regulatory frameworks, and adoption rates across different sectors.

Step 2: Market Analysis and Construction

In this phase, we analyze historical data related to market size, revenue streams, and end-user adoption. The assessment focuses on how market penetration has evolved over time, particularly in the BFSI and healthcare sectors, which are major drivers of growth in the digital signature market.

Step 3: Hypothesis Validation and Expert Consultation

Consultations with industry experts are conducted to validate the initial findings. We leverage direct interviews with professionals from key companies like DocuSign and Adobe to gather insights on customer preferences, technological advancements, and future growth prospects.

Step 4: Research Synthesis and Final Output

Finally, the data is synthesized to provide a detailed market report. This involves integrating both quantitative and qualitative data, ensuring a robust and accurate analysis of market dynamics. Direct feedback from leading digital signature solution providers helps verify the trends and projections included in the final report.

Frequently Asked Questions

01. How big is the North America Digital Signature Market?

The North America Digital Signature market is valued at USD 2.2 billion, driven by growing demand for secure digital transactions, regulatory compliance, and the increasing need for paperless workflows.

02. What are the challenges in the North America Digital Signature Market?

Challenges in the North America Digital Signature market include high implementation costs for smaller businesses, cybersecurity risks, and the complexity of navigating compliance with different regulations across industries.

03. Who are the major players in the North America Digital Signature Market?

Key players in the North America Digital Signature market include Adobe Inc., DocuSign, Thales Group, OneSpan Inc., and SIGNiX. These companies have established themselves due to their innovative technologies, extensive service offerings, and strong customer bases.

04. What are the growth drivers of the North America Digital Signature Market?

The North America Digital Signature market is driven by increased digital transformation initiatives, regulatory compliance requirements, and the shift towards cloud-based, remote solutions, especially in sectors such as BFSI, healthcare, and government.

05. What sectors dominate the North America Digital Signature Market?

The BFSI and healthcare sectors dominate the North America Digital Signature market due to their need for secure, authenticated documentation processes, compliance with regulations, and the growing trend towards digitization.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.