North America Directed Energy Weapons Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD6857

November 2024

92

About the Report

North America Directed Energy Weapons Market Overview

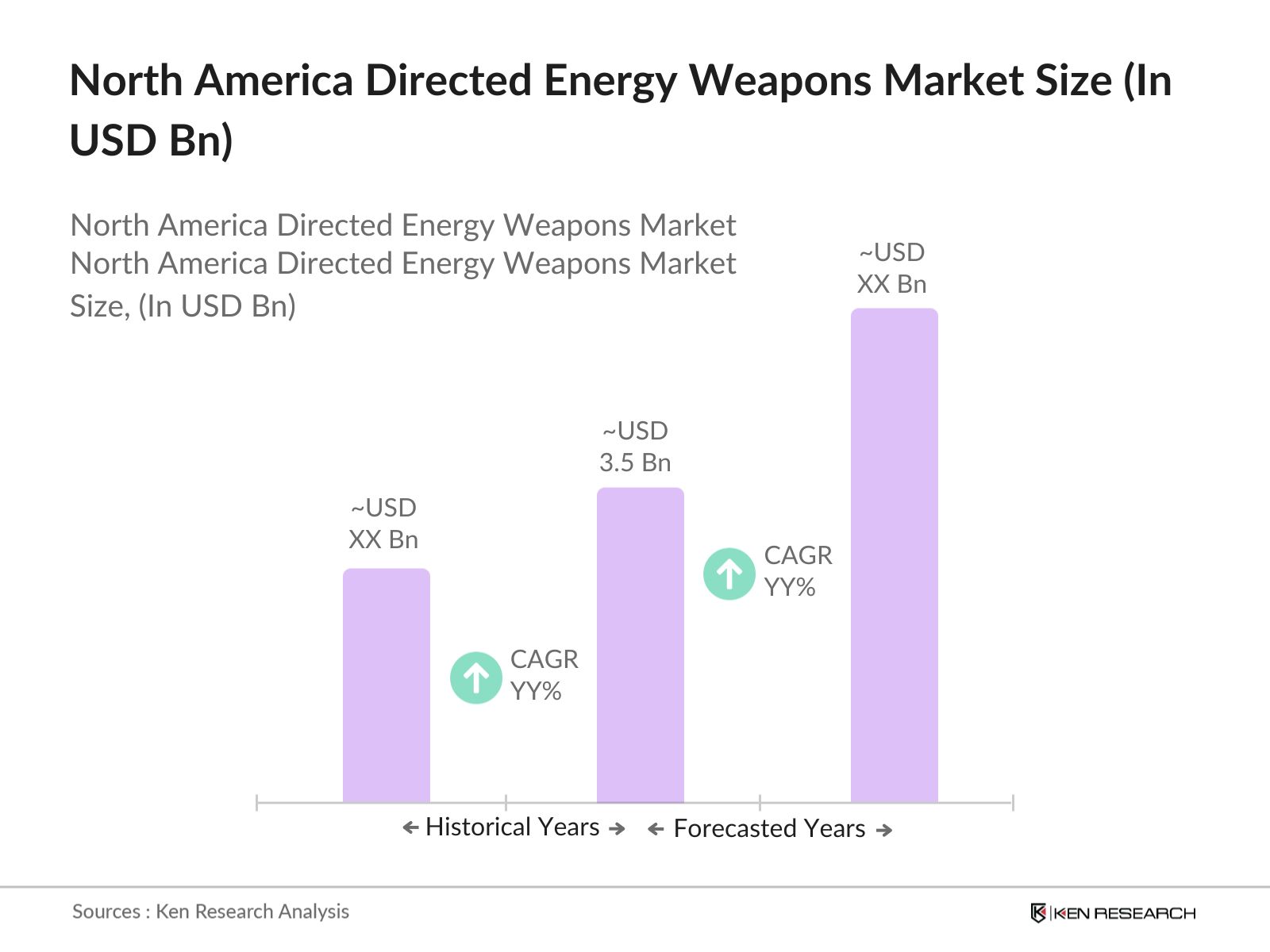

- The North America Directed Energy Weapons (DEW) Market is valued at USD 3.5 billion, reflecting a five-year historical analysis driven by significant advancements in defense technology and rising defense budgets. The demand for high-precision and non-lethal defense systems, particularly for counter-drone and missile defense operations, has spurred growth in the market.

- Major cities and countries in North America, such as the United States, dominate the Directed Energy Weapons market primarily due to their extensive defense budgets and robust military infrastructure. The United States, in particular, is a key player, with large defense contractors and significant R&D investments fostering innovation in laser and microwave-based DEW systems.

- Canada, in 2024, committed over $350 million to defense technology innovations, including directed energy weapons development. The initiative aims to bolster Canadas defense capabilities in coordination with NATO allies by enhancing research into non-lethal and precise energy-based systems for anti-drone and missile defense applications. This initiative showcases North Americas collaborative efforts in pioneering defense technology.

North America Directed Energy Weapons Market Segmentation

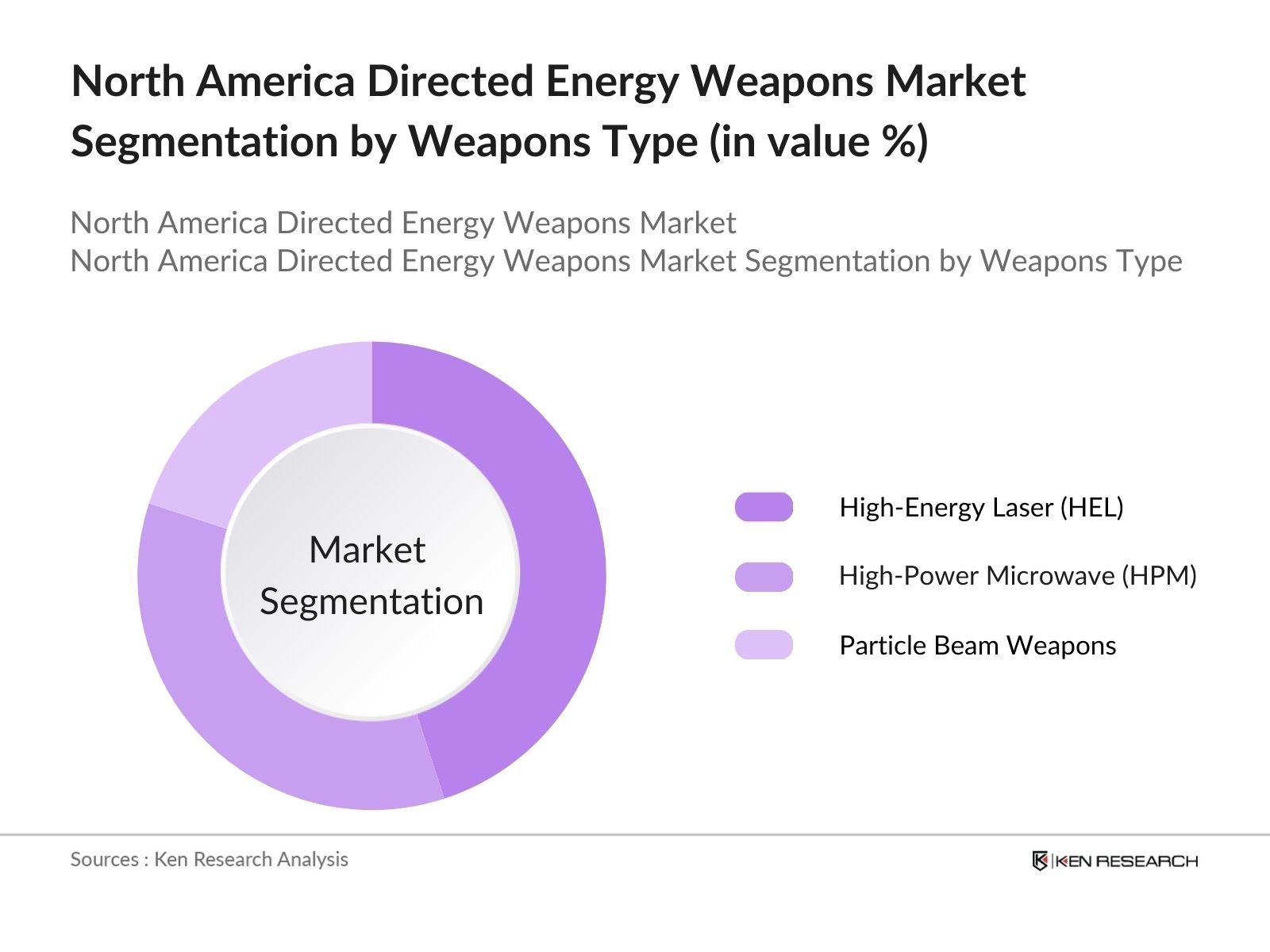

By Weapon Type: The market is segmented by weapon type into high-energy laser (HEL) weapons, high-power microwave (HPM) weapons, and particle beam weapons. High-energy laser weapons have a dominant market share due to their advanced capabilities in precision targeting and their integration into various military platforms such as naval ships and aircraft. HEL systems are preferred for their ability to provide long-range engagement while minimizing collateral damage, making them ideal for anti-drone and missile defense applications.

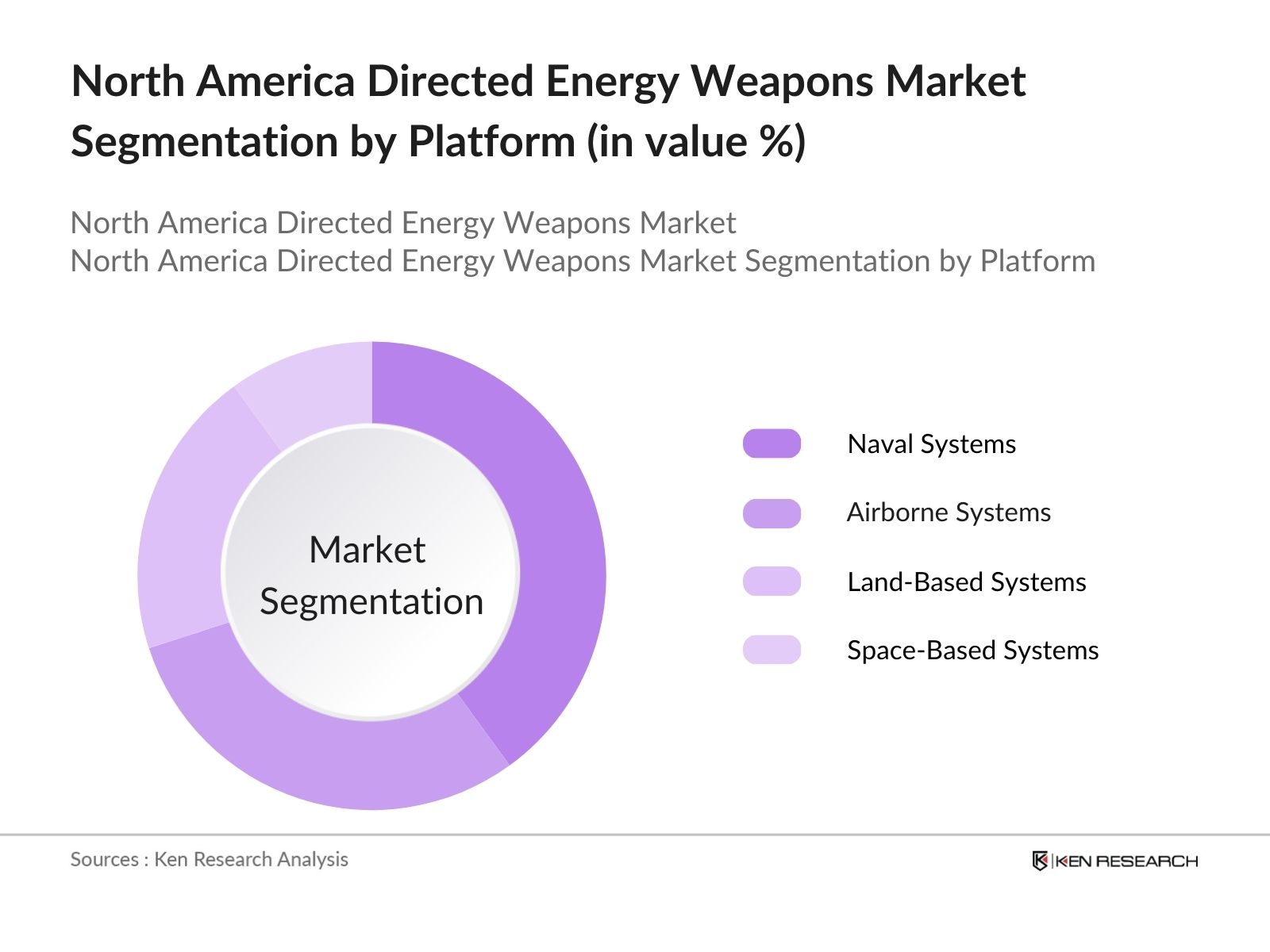

By Platform: The market is also segmented by platform into land-based systems, airborne systems, naval systems, and space-based systems. Naval systems hold a significant share of the market due to their integration with advanced targeting and defense technologies. Directed energy weapons on naval platforms offer enhanced capabilities for missile defense and counter-air threats, which is critical for the U.S. Navys strategic operations.

North America Directed Energy Weapons Market Competitive Landscape

The market is dominated by a few major players, including Lockheed Martin, Raytheon Technologies, and Northrop Grumman. These companies have established a strong foothold through significant investments in research and development, long-term government contracts, and technological innovations.

|

Company |

Establishment Year |

Headquarters |

Employees |

Defense Contracts |

R&D Spending (USD) |

Product Portfolio |

Recent Innovations |

Revenue (USD) |

|

Lockheed Martin Corporation |

1995 |

Bethesda, Maryland |

||||||

|

Raytheon Technologies |

1922 |

Waltham, Massachusetts |

||||||

|

Northrop Grumman |

1939 |

Falls Church, Virginia |

||||||

|

Boeing Defense |

1916 |

Chicago, Illinois |

||||||

|

General Atomics |

1955 |

San Diego, California |

North America Directed Energy Weapons Market Analysis

Market Growth Drivers

- Increased Defense Budget Allocation for Directed Energy Programs: The U.S. Department of Defense (DoD) allocated $67 billion in FY 2024 for advanced weapon technologies, including directed energy systems. This allocation is part of a broader effort to enhance the capabilities of next-generation weaponry for strategic defense and countering emerging threats, such as drones and hypersonic missiles. The strong financial backing from the government serves as a robust driver, with multiple contracts awarded for research, testing, and deployment of directed energy weapons.

- Increased Threat of Drone and UAV Attacks: In 2024, over 900 incidents of drone-related threats were reported across North America, prompting the need for more sophisticated defense mechanisms like directed energy weapons. Governments and defense organizations are rapidly adopting these systems to neutralize drone and UAV threats effectively. The rise in asymmetric warfare, where smaller yet potent drones can carry out attacks, creates an urgent need for real-time, energy-efficient, and precise defense solutions, which boosts the demand for directed energy technologies.

- Growing Focus on Counter Hypersonic Missiles: With 32 hypersonic missile tests being conducted globally in 2024, defense forces in North America are prioritizing the development of directed energy systems to intercept these high-speed threats. Directed energy weapons offer the advantage of engaging hypersonic threats at the speed of light, a critical factor in future missile defense strategies. The increase in hypersonic missile programs by adversary nations is pushing North America to focus on defensive solutions like high-energy lasers and microwave-based systems.

Market Challenges

- Power Generation and Storage Limitations: One of the key challenges facing directed energy weapon systems in 2024 is the availability and generation of sufficient power to operate high-energy lasers and microwave systems for extended durations. The U.S. Army's recent tests indicated that sustaining directed energy weapons for longer missions requires improved power storage solutions, which have lagged behind the technology needed for field deployment.

- Environmental and Atmospheric Interference: Weather conditions such as fog, rain, and dust can severely degrade the performance of directed energy weapons. In tests conducted by the U.S. Air Force in 2024, it was found that high-energy laser systems experienced a 30-40% drop in effectiveness in adverse weather conditions. This environmental sensitivity poses a challenge for widespread deployment, especially in maritime or desert environments where these factors are prevalent.

North America Directed Energy Weapons Market Future Outlook

Over the next five years, the North America Directed Energy Weapons industry is expected to witness substantial growth. This will be driven by the continuous innovation in high-energy laser and high-power microwave systems, supported by increasing defense budgets and growing geopolitical tensions.

Market Future Opportunities

- Directed Energy Weapons for Homeland Security: By 2028, directed energy weapons will be increasingly utilized for homeland security purposes, especially to protect critical infrastructure from drone and cyber-attacks. Governments are expected to deploy these systems at sensitive locations such as nuclear power plants, airports, and government buildings, with over 20 major installations planned by 2026 across North America.

- Development of Miniaturized Directed Energy Systems: In the coming years, there will be a shift towards the development of smaller, more portable directed energy systems. By 2027, lightweight versions of high-energy lasers will be integrated into ground vehicles and mobile units, allowing for rapid deployment in urban combat environments. This trend will revolutionize tactical military operations, with over 100 units expected to be deployed in high-risk zones by 2026.

Scope of the Report

|

Weapon Type |

High-Energy Laser (HEL) Weapons High-Power Microwave (HPM) Weapons Particle Beam Weapons |

|

Application |

Military Defense Systems Homeland Security Operations Space and Satellite Protection |

|

Technology |

Fiber Laser Technology Free Electron Laser Solid-State Laser |

|

Power Source |

Electrically Powered DEWs Chemically Powered DEWs |

|

Platform |

Land-Based Systems Airborne Systems Naval Systems Space-Based Systems |

|

Region |

North East West South |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Banks and Financial Institution

Weapon System Manufacturers

Government and Regulatory Bodies (e.g., U.S. Department of Defense, Canadian Armed Forces)

Private Equity Firms

Naval and Air Force Departments

Weapons Manufacturers

Investor and Venture Capitalist Firms

Companies

Players Mentioned in the Report:

Lockheed Martin Corporation

Raytheon Technologies

Northrop Grumman

Boeing Defense

General Atomics

BAE Systems

Leonardo DRS

L3Harris Technologies

Thales Group

Rheinmetall AG

Table of Contents

North America Directed Energy Weapons Market Overview

Definition and Scope

Market Taxonomy

Market Growth Rate (Directed Energy Technology Evolution, Deployment Rates)

Market Segmentation Overview (Weapon Type, Application, Technology, Power Source, Platform)

North America Directed Energy Weapons Market Size (In USD Bn)

Historical Market Size (Year-on-Year Weapon Deployment Data, System Sales Growth)

Year-On-Year Growth Analysis (Technological Innovation Adoption, Increasing Defense Budgets)

Key Market Developments and Milestones (Major Contracts, Breakthrough Technologies)

North America Directed Energy Weapons Market Analysis

Growth Drivers (Specific to Industry)

Increasing Defense Budget Allocations for Advanced Technologies

Rising Geopolitical Tensions Leading to Demand for Advanced Weapons

Government and Military Focus on Minimizing Collateral Damage

Favorable Regulatory Policies for Research and Development

Market Challenges (Industry-Specific Challenges)

High Development and Deployment Costs

Power Supply Constraints for Directed Energy Systems

Limited Operational Testing and Real-World Application

Opportunities (Market-Specific)

Integration into Naval and Ground Platforms

Development of Compact Power Solutions for Mobility

Rising Collaborations Between Defense Contractors and Government Agencies

Trends (Specific to DEW Adoption)

Increasing Use of High-Energy Laser Weapons for Anti-Drone Operations

Focus on Electrically Driven Weapons Over Chemical-Based Alternatives

Adoption of DEWs for Missile Defense Systems

Government Regulations (Applicable Laws and Standards)

National Defense Authorization Acts (NDAA) Policies

Export Regulations Governing Directed Energy Systems

Joint U.S.-Canada Defense Agreements Promoting Technology Sharing

SWOT Analysis (Market-Specific Metrics)

Stakeholder Ecosystem (Manufacturers, Governments, Research Institutions)

Porters Five Forces (Market-Specific Parameters: Buyer Power, Technological Substitution)

Competition Ecosystem

North America Directed Energy Weapons Market Segmentation

By Weapon Type (In Value %)

High-Energy Laser (HEL) Weapons

High-Power Microwave (HPM) Weapons

Particle Beam Weapons

By Application (In Value %)

Military Defense Systems

Homeland Security Operations

Space and Satellite Protection

By Technology (In Value %)

Fiber Laser Technology

Free Electron Laser

Solid-State Laser

By Power Source (In Value %)

Electrically Powered DEWs

Chemically Powered DEWs

By Platform (In Value %)

Land-Based Systems

Airborne Systems

Naval Systems

Space-Based Systems

By Region (In Value %)

North

East

West

South

North America Directed Energy Weapons Market Competitive Analysis

Detailed Profiles of Major Companies

Lockheed Martin Corporation

Raytheon Technologies

Northrop Grumman

Boeing Defense

General Atomics

BAE Systems

Leonardo DRS

L3Harris Technologies

Thales Group

Rheinmetall AG

QinetiQ Group

Elbit Systems

Textron Inc.

Dynetics, a Leidos Company

Kratos Defense & Security Solutions

Cross Comparison Parameters (Headquarters, Revenue, Market Presence, Recent Innovations, No. of Employees, Defense Contracts, R&D Spending, Product Portfolio)

Market Share Analysis (Market Leader by Category, Revenue Share)

Strategic Initiatives (Recent Developments, Innovation Focus)

Mergers and Acquisitions

Investment Analysis (Market-Specific Capital Investments)

Government Grants and Funding for Directed Energy Weapon Development

Private Equity Investments

North America Directed Energy Weapons Market Regulatory Framework

Weapon Standards for Development

Compliance Requirements in Military Applications

International Compliance and Arms Control

North America Directed Energy Weapons Future Market Size (In USD Bn)

Future Market Size Projections (Market Growth Forecasts Based on Government Spending)

Key Factors Driving Future Market Growth (New Technology Integration, Increasing Adoption for Defense)

North America Directed Energy Weapons Future Market Segmentation

By Weapon Type (In Value %)

By Application (In Value %)

By Technology (In Value %)

By Power Source (In Value %)

By Platform (In Value %)

By Region (In Value %)

North America Directed Energy Weapons Market Analysts Recommendations

TAM/SAM/SOM Analysis

Customer Cohort Analysis

Marketing Initiatives for New Technology

White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In this phase, we identify and map the key stakeholders involved in the North America Directed Energy Weapons market. By utilizing a range of secondary and proprietary databases, we gather and analyze industry-level data to define the core variables that shape the market's dynamics, such as technological trends, defense contracts, and government spending.

Step 2: Market Analysis and Construction

This step involves a detailed analysis of historical data and market penetration trends. Our team conducts a thorough assessment of weapon system deployments, government R&D investments, and defense budgets to provide an accurate representation of market growth. We focus on the performance of specific weapon types and platforms in various defense scenarios.

Step 3: Hypothesis Validation and Expert Consultation

We validate our market hypotheses through in-depth consultations with industry experts, defense contractors, and government officials. These consultations provide direct insights into the operational efficiency and financial performance of DEW systems. Our approach ensures the reliability and accuracy of our market projections.

Step 4: Research Synthesis and Final Output

The final stage involves synthesizing data from various DEW manufacturers and defense departments. This allows us to verify the market statistics derived from both top-down and bottom-up approaches. Our analysis is further refined through ongoing engagements with key market stakeholders.

Frequently Asked Questions

How big is the North America Directed Energy Weapons Market?

The North America Directed Energy Weapons market is valued at USD 3.5 billion, driven by increased defense spending and advancements in laser and microwave weapon technologies.

What are the challenges in the North America Directed Energy Weapons Market?

Challenges in this North America Directed Energy Weapons market include high development and operational costs, power supply limitations, and the need for further operational testing to ensure reliability in diverse environments.

Who are the major players in the North America Directed Energy Weapons Market?

Major players in the North America Directed Energy Weapons market include Lockheed Martin Corporation, Raytheon Technologies, Northrop Grumman, Boeing Defense, and General Atomics. These companies dominate due to their strong defense contracts and innovative DEW technologies.

What are the growth drivers of the North America Directed Energy Weapons Market?

The growth of the DEW market is driven by the increasing demand for non-lethal defense systems, rising geopolitical tensions, and the need for advanced counter-drone and missile defense technologies.

Which platform is most popular in the North America Directed Energy Weapons Market?

Naval systems hold the dominant North America Directed Energy Weapons market share due to their ability to integrate DEW technologies effectively for missile and air defense operations.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.