North America Dry Type Transformer Market Outlook to 2030

Region:North America

Author(s):Paribhasha Tiwari

Product Code:KROD4970

December 2024

90

About the Report

North America Dry Type Transformer Market Overview

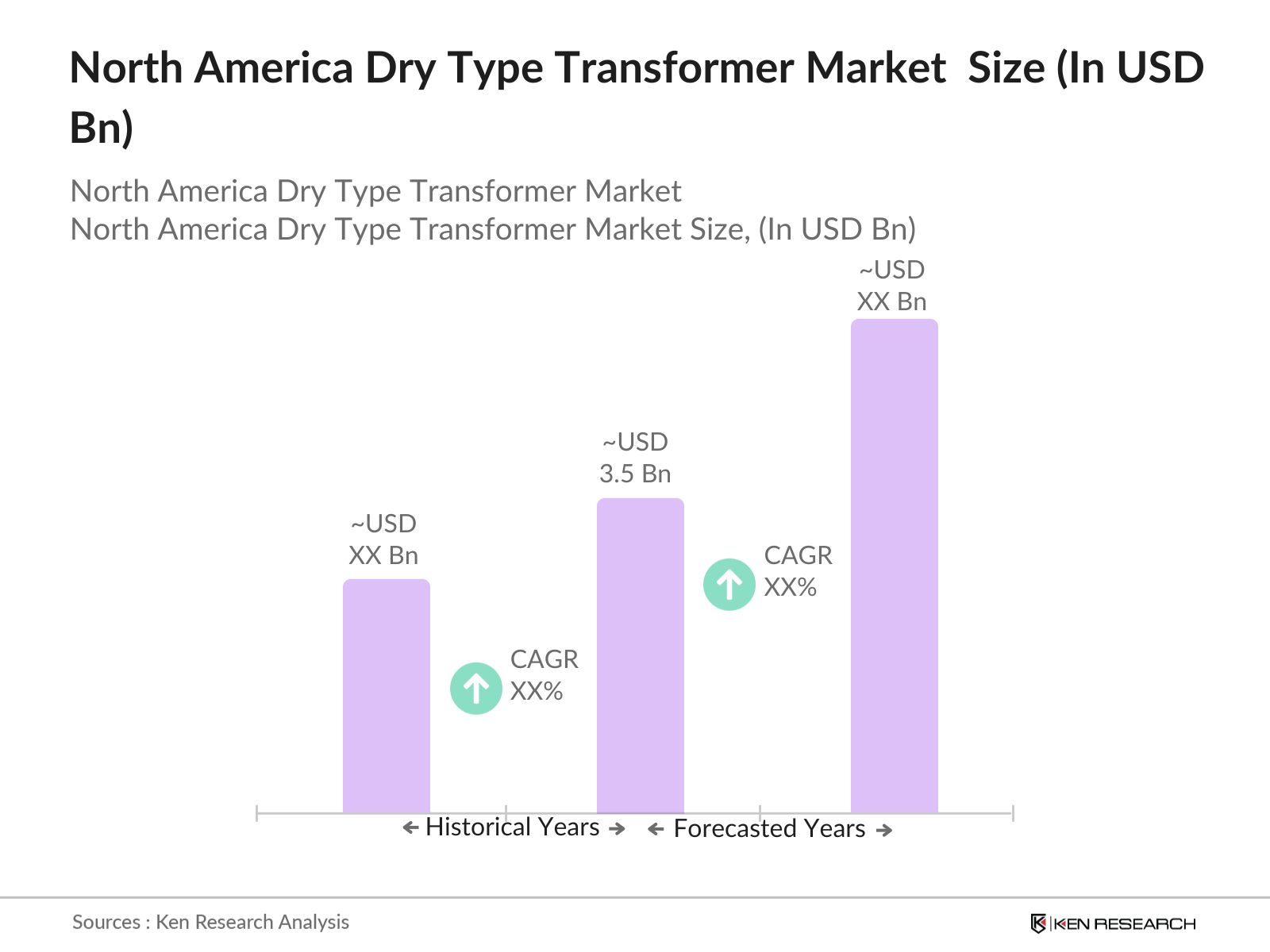

- The North America Dry Type Transformer market is valued at USD 3.5 billion, based on historical data analysis, and is driven by several key factors. The growing demand for energy-efficient solutions, alongside the rise in renewable energy installations, has significantly contributed to the market's growth. Urbanization and modernization of electrical grids, particularly in urban centers, are further fueling the need for dry type transformers, which are preferred for their reliability and low maintenance.

- In terms of regional dominance, the United States and Canada are leading the market due to their strong emphasis on smart grid technologies and renewable energy integration. These countries have actively invested in grid modernization projects, driving the demand for dry type transformers, especially in industrial and commercial applications. Moreover, stringent government regulations in these regions are pushing for the adoption of energy-efficient technologies, giving these nations a competitive edge in the market.

- The U.S. governments Infrastructure Investment and Jobs Act, passed in 2022, allocated $13 billion towards grid modernization and power resilience projects. This initiative is designed to upgrade the nations electrical grid to accommodate renewable energy sources, smart grid technologies, and improved power transmission. Dry-type transformers are integral to these efforts, particularly in urban areas where safety and space are critical concerns. This initiative is expected to drive the adoption of dry-type transformers across the country.

North America Dry Type Transformer Market Segmentation

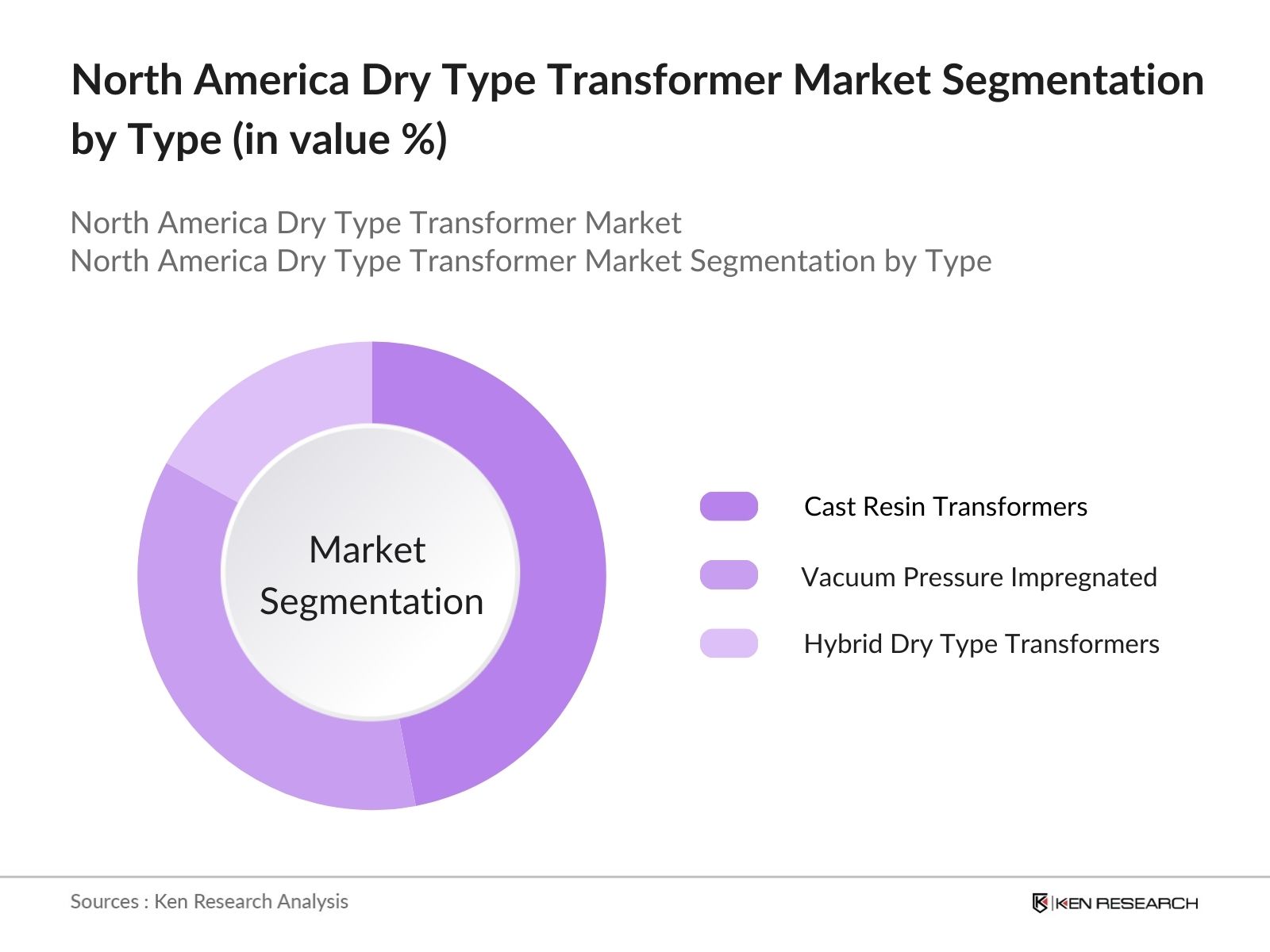

By Type: The North America Dry Type Transformer market is segmented by type into cast resin transformers, vacuum pressure impregnated (VPI) transformers, and hybrid dry type transformers. Cast resin transformers currently hold the dominant market share due to their widespread use in commercial and industrial applications. The high reliability, fire safety, and minimal environmental impact of these transformers have made them a popular choice for energy-intensive sectors such as manufacturing and renewable energy.

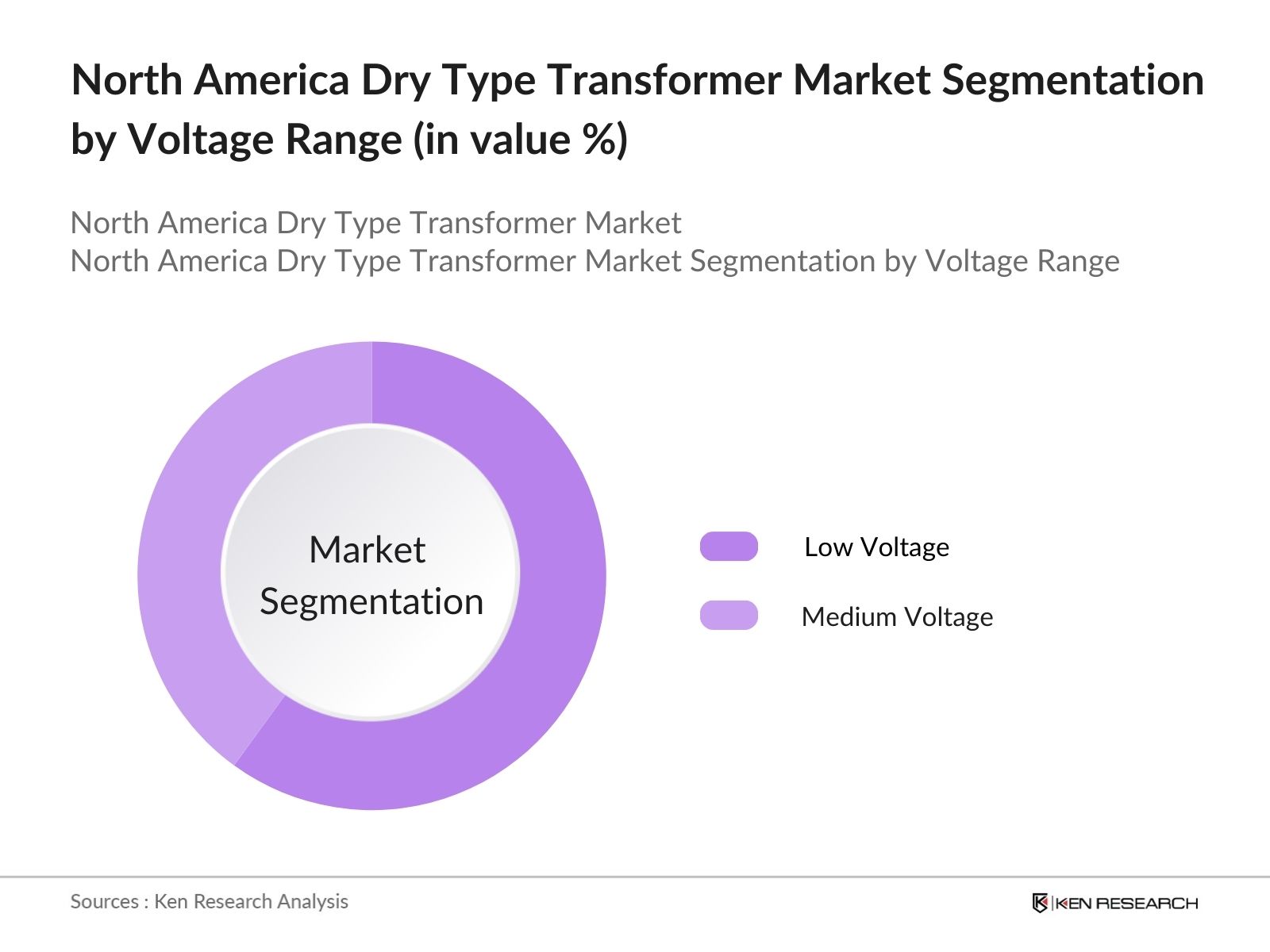

By Voltage Range: The market is also segmented by voltage range into low voltage (<36 kV) and medium voltage (36-170 kV) transformers. Low voltage transformers dominate the market, driven by their extensive application in urban infrastructure projects and commercial spaces. The growing demand for electricity distribution in urban centers is driving the growth of this segment, with applications ranging from residential complexes to data centers.

North America Dry Type Transformer Market Competitive Landscape

The North America Dry Type Transformer market is characterized by a few major players that dominate the landscape through technological advancements and extensive market presence. Key companies in this market have invested heavily in R&D to develop efficient and sustainable transformer solutions.

|

Company |

Establishment Year |

Headquarters |

Product Offerings |

Regional Presence |

R&D Investment |

Sustainability Initiatives |

Certifications & Standards |

Annual Revenue (USD) |

|

ABB Ltd. |

1988 |

Zurich, Switzerland |

- | - | - | - | - | - |

|

Siemens AG |

1847 |

Munich, Germany |

- | - | - | - | - | - |

|

Eaton Corporation |

1911 |

Dublin, Ireland |

- | - | - | - | - | - |

|

Schneider Electric SE |

1836 |

Rueil-Malmaison, France |

- | - | - | - | - | - |

|

General Electric |

1892 |

Boston, USA |

- | - | - | - | - | - |

North America Dry Type Transformer Market Analysis

Growth Drivers

- Renewable Energy Integration: The integration of renewable energy into North Americas power grid is driving demand for dry-type transformers. The United States has significantly expanded its renewable energy capacity, with over 130 GW of solar and wind power operational in 2024. According to the U.S. Energy Information Administration, renewable energy sources provided approximately 20% of the countrys electricity in 2023. Dry-type transformers play a crucial role in facilitating the connection of renewable energy sources to the grid due to their superior environmental safety and energy efficiency, making them a key component in this growing sector.

- Grid Modernization (Smart Grid Technologies): North Americas ongoing investment in grid modernization, particularly in smart grid technologies, is a significant growth driver for the dry-type transformer market. In 2022, the U.S. government allocated $13 billion for grid resilience and modernization projects under the Infrastructure Investment and Jobs Act. Smart grids require transformers capable of handling dynamic loads and ensuring efficient energy distribution. Dry-type transformers are increasingly favored for these applications due to their lower fire risk and ability to operate in confined spaces, which is critical in urban settings.

- Urbanization and Infrastructure Development: Urbanization and infrastructure development across North America are boosting the demand for dry-type transformers. In 2023, the U.S. Department of Transportation reported over $80 billion in infrastructure projects aimed at enhancing urban transportation and public utilities. As cities expand, the demand for reliable power distribution grows, and dry-type transformers are essential for delivering power in densely populated areas due to their compact size and reduced environmental hazards. These transformers are increasingly used in commercial buildings, airports, and public infrastructure to support urban growth.

Market Challenges

- High Installation and Maintenance Costs: The high installation and maintenance costs of dry-type transformers pose a significant challenge to market growth. While dry-type transformers offer advantages in terms of safety and environmental benefits, their initial costs are substantially higher than oil-filled alternatives. For instance, installation costs for a dry-type transformer can exceed $20,000, depending on the voltage level and application, making them less accessible for smaller utilities or companies. Maintenance, while less frequent, can also be expensive due to the specialized nature of these transformers, further contributing to the high-cost barrier.

- Limited Short-Circuit Strength: One of the technical challenges facing dry-type transformers is their limited short-circuit strength compared to oil-filled models. This limitation restricts their use in high-power applications where fault currents are a concern. In 2023, the U.S. Department of Energy's studies highlighted the potential for damage to dry-type transformers under high short-circuit conditions, which can lead to significant downtimes. As power grids become more complex and the load on electrical infrastructure increases, addressing the short-circuit limitations of dry-type transformers is crucial for their wider adoption.

North America Dry Type Transformer Market Future Outlook

The North America Dry Type Transformer market is expected to witness significant growth over the next five years, driven by several key factors. The increasing adoption of renewable energy sources, coupled with government incentives for smart grid technology, will propel the market forward. The rise in electric vehicle (EV) infrastructure across North America is also expected to spur demand for dry type transformers, particularly in the transportation and industrial sectors.

Market Opportunities

- Expansion of Electric Vehicle (EV) Infrastructure: The rapid expansion of electric vehicle (EV) infrastructure in North America presents a significant opportunity for the dry-type transformer market. In 2023, the U.S. government allocated $7.5 billion towards the development of a national EV charging network. Dry-type transformers, due to their reliability and reduced environmental impact, are increasingly being deployed in EV charging stations. With over 130,000 public charging stations expected to be operational by the end of 2024, dry-type transformers will play a pivotal role in supporting the electrification of transportation across the continent.

- Smart Grid Investments: Ongoing investments in smart grid technologies across North America offer promising growth opportunities for the dry-type transformer market. The U.S. Department of Energy invested $10 billion in smart grid enhancements in 2023, focusing on improving grid reliability and integrating renewable energy sources. Dry-type transformers are ideal for smart grid applications due to their energy efficiency and adaptability to variable load conditions. As utilities continue to upgrade their infrastructure, the demand for advanced transformers is set to rise, with dry-type models playing a key role in this transition.

Scope of the Report

|

By Type |

Cast Resin Transformers Vacuum Pressure Impregnated Transformers Hybrid Dry Type Transformers |

|

By Voltage Range |

Low Voltage (<36 kV) Medium Voltage (36-170 kV) |

|

By Application |

Industrial Commercial Renewable Energy |

|

By Phase |

Single-Phase Transformers Three-Phase Transformers |

|

By Region |

U.S. Canada Mexico |

Products

Key Target Audience

Transformer Manufacturers

Grid Modernization Companies

Renewable Energy Providers

Infrastructure Developers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., U.S. Department of Energy, Federal Energy Regulatory Commission)

Industrial Equipment Distributors

Electric Vehicle Charging Infrastructure Companies

Companies

Players Mentioned in the Report:

ABB Ltd.

Siemens AG

Eaton Corporation

Schneider Electric SE

General Electric

Hammond Power Solutions Inc.

Virginia Transformer Corp.

WEG Electric Corp.

TMC Transformers

CG Power and Industrial Solutions Ltd.

Table of Contents

1. North America Dry Type Transformer Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Dry Type Transformer Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Dry Type Transformer Market Analysis

3.1. Growth Drivers

3.1.1. Renewable Energy Integration

3.1.2. Grid Modernization (Smart Grid Technologies)

3.1.3. Urbanization and Infrastructure Development

3.1.4. Energy Efficiency Standards

3.2. Market Challenges

3.2.1. High Installation and Maintenance Costs

3.2.2. Limited Short-Circuit Strength

3.2.3. Supply Chain Disruptions (Raw Material Availability)

3.3. Opportunities

3.3.1. Expansion of Electric Vehicle (EV) Infrastructure

3.3.2. Smart Grid Investments

3.3.3. Technological Advancements (Nano-Crystalline Core Materials)

3.4. Trends

3.4.1. Shift towards Eco-Friendly Transformers (Low-Carbon Footprint)

3.4.2. Demand for Compact Transformers in Urban Areas

3.4.3. Digital Monitoring and Control Systems

3.5. Government Regulations and Initiatives

3.5.1. U.S. Energy Policy Act

3.5.2. Federal Energy Regulatory Commission (FERC) Standards

3.5.3. Department of Energy (DOE) Transformer Efficiency Guidelines

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. North America Dry Type Transformer Market Segmentation

4.1. By Type (In Value %)

4.1.1. Cast Resin Transformers

4.1.2. Vacuum Pressure Impregnated Transformers

4.1.3. Hybrid Dry Type Transformers

4.2. By Phase (In Value %)

4.2.1. Single-Phase Transformers

4.2.2. Three-Phase Transformers

4.3. By Voltage Range (In Value %)

4.3.1. Low Voltage (<36 kV)

4.3.2. Medium Voltage (36-170 kV)

4.4. By Application (In Value %)

4.4.1. Industrial

4.4.2. Commercial

4.4.3. Renewable Energy

4.5. By Region (In Value %)

4.5.1. U.S.

4.5.2. Canada

4.5.3. Mexico

5. North America Dry Type Transformer Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. ABB Ltd.

5.1.2. Eaton Corporation

5.1.3. Siemens AG

5.1.4. Schneider Electric SE

5.1.5. General Electric

5.1.6. Hammond Power Solutions Inc.

5.1.7. Virginia Transformer Corp

5.1.8. WEG Electric Corp

5.1.9. TMC Transformers

5.1.10. CG Power and Industrial Solutions Ltd.

5.1.11. Bharat Heavy Electricals Ltd.

5.1.12. Fuji Electric Co., Ltd.

5.1.13. Hitachi Energy

5.1.14. ABB Power Grids

5.1.15. Legrand

5.2. Cross Comparison Parameters

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity and Venture Capital Investments

6. North America Dry Type Transformer Market Regulatory Framework

6.1. Transformer Efficiency Standards (DOE, NEMA)

6.2. Environmental Compliance and Safety Standards

6.3. Certification Processes (ISO, UL)

7. North America Dry Type Transformer Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Dry Type Transformer Future Market Segmentation

8.1. By Type (In Value %)

8.2. By Phase (In Value %)

8.3. By Voltage Range (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. North America Dry Type Transformer Market Analysts Recommendations

9.1. Total Addressable Market (TAM) Analysis

9.2. Customer Cohort Analysis

9.3. White Space Opportunity Identification

9.4. Strategic Market Entry Recommendations

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research process begins with identifying and mapping out key stakeholders in the North America Dry Type Transformer Market. This involves conducting desk research using proprietary databases and secondary resources to gather detailed information about industry trends and market dynamics. The primary focus is on defining the variables that influence market behavior, such as government regulations, technological innovations, and customer demand.

Step 2: Market Analysis and Construction

Historical data on market performance is gathered and analyzed to assess penetration levels, revenue generation, and customer base distribution. This analysis is complemented by evaluating service quality metrics to ensure that revenue estimates are reliable and accurate. The goal is to construct a comprehensive overview of the market's past and current performance.

Step 3: Hypothesis Validation and Expert Consultation

We then develop market hypotheses based on initial findings and validate them through consultations with industry experts. These interviews are conducted using computer-assisted telephone interviewing (CATI) techniques, focusing on market practitioners' insights to refine the collected data and ensure accuracy.

Step 4: Research Synthesis and Final Output

Finally, data from manufacturers, distributors, and other stakeholders is synthesized to create a detailed market report. This includes verifying statistics through bottom-up approaches, ensuring the data is comprehensive, validated, and ready for client use.

Frequently Asked Questions

01. How big is the North America Dry Type Transformer Market?

The North America Dry Type Transformer market is valued at USD 3.5 billion, driven by the growing demand for energy-efficient and eco-friendly transformer solutions across industrial and commercial sectors.

02. What are the challenges in the North America Dry Type Transformer Market?

Challenges in the North America Dry Type Transformer market include high installation and maintenance costs, limited short-circuit strength compared to oil-immersed transformers, and supply chain disruptions impacting raw material availability.

03. Who are the major players in the North America Dry Type Transformer Market?

Key players in the North America Dry Type Transformer market include ABB Ltd., Siemens AG, Eaton Corporation, Schneider Electric SE, and General Electric. These companies dominate the market due to their extensive product portfolios, strong R&D investments, and global presence.

04. What are the growth drivers of the North America Dry Type Transformer Market?

The North America Dry Type Transformer market is driven by factors such as the integration of renewable energy sources, smart grid investments, and urbanization, all contributing to the increasing demand for dry type transformers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.