North America Electronic Warfare Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD6183

December 2024

89

About the Report

North America Electronic Warfare Market Overview

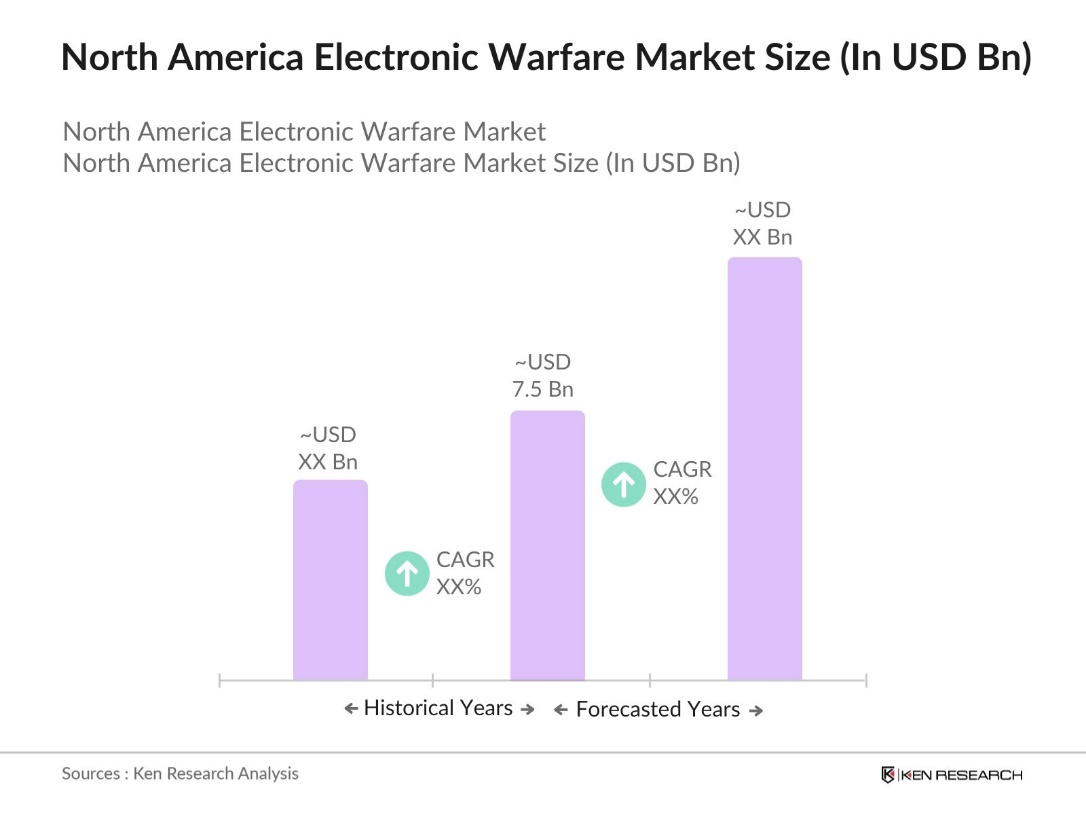

- The North America Electronic Warfare (EW) market, valued at USD 7.5 billion, has experienced steady growth driven by escalating defense expenditures and technological advancements. The increasing complexity of modern warfare necessitates sophisticated EW systems to counter diverse threats, thereby propelling market expansion.

- The United States stands as the dominant force in the North American EW market, attributed to its substantial defense budget and continuous investment in cutting-edge EW technologies. The presence of leading defense contractors and a robust military infrastructure further consolidate its leadership position.

- Export controls for EW systems have tightened, with the U.S. enforcing stricter guidelines in 2023 to prevent advanced technologies from reaching adversaries. This regulatory landscape shapes market opportunities, as companies must navigate complex compliance to engage in international contracts while securing North American technology.

North America Electronic Warfare Market Segmentation

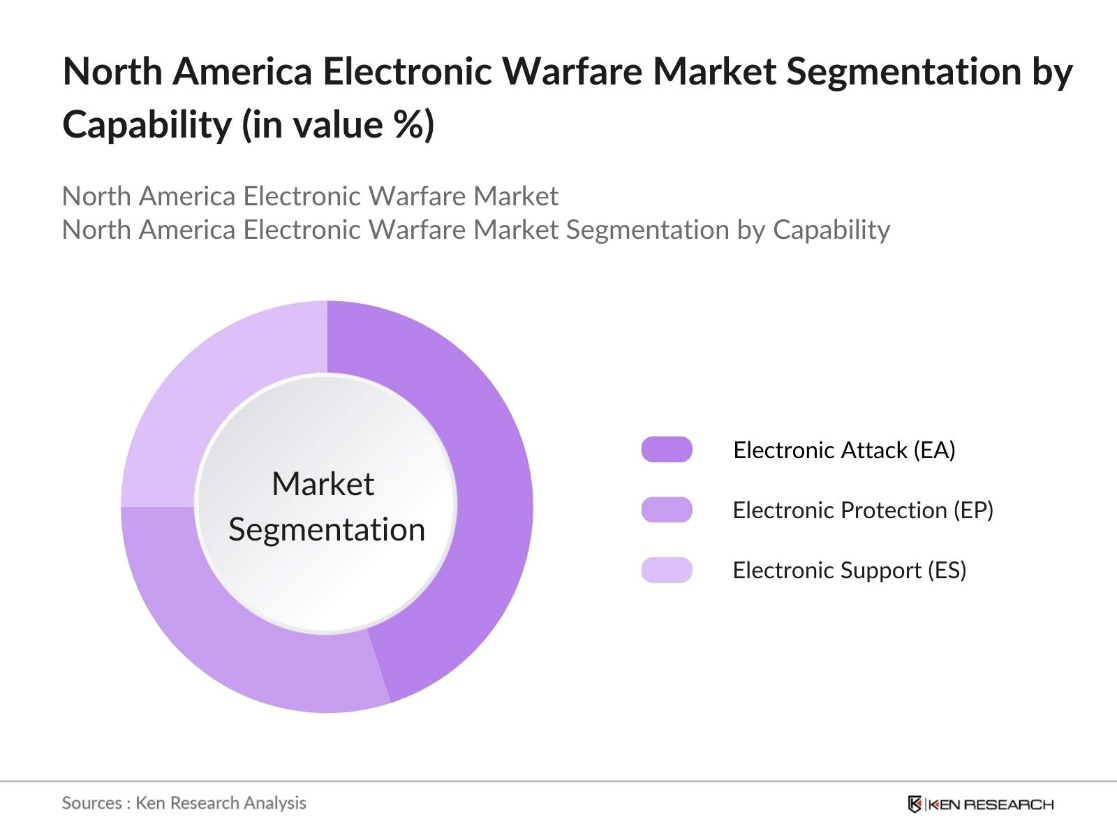

By Capability: The market is segmented by capability into Electronic Attack (EA), Electronic Protection (EP), and Electronic Support (ES). Electronic Attack holds a dominant market share due to its critical role in disrupting adversary communications and radar systems. The increasing deployment of EA systems enhances offensive capabilities, making it a pivotal component in modern military strategies.

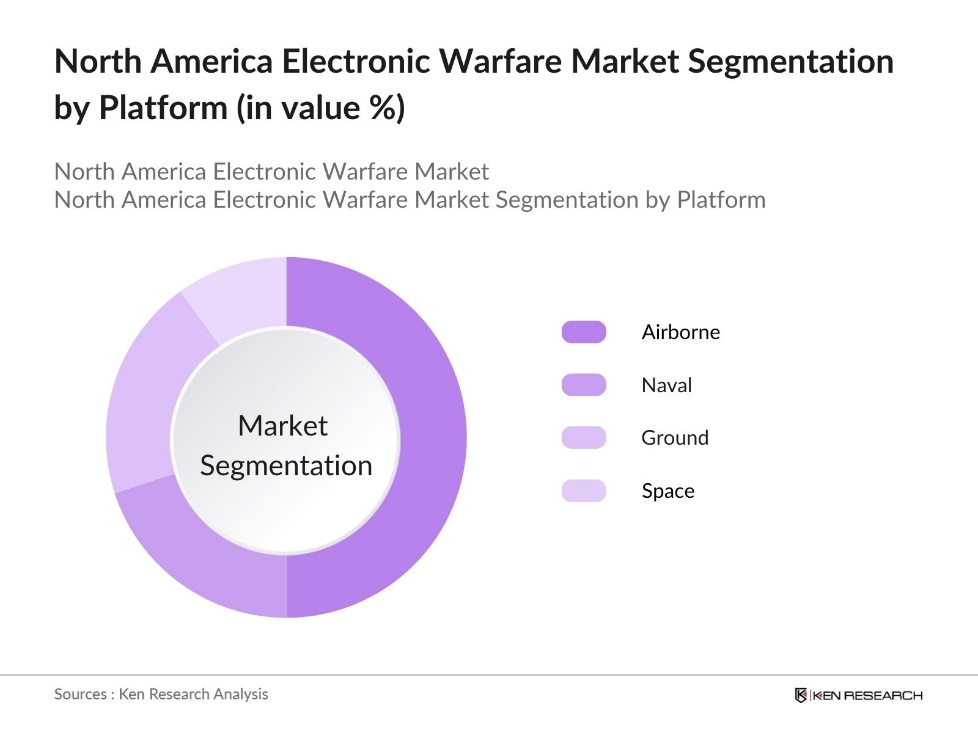

By Platform: The market is segmented by platform into Airborne, Naval, Ground, and Space. The Airborne segment leads the market, driven by the integration of advanced EW systems into aircraft to ensure air superiority and mission success. The versatility and strategic importance of airborne platforms contribute to their dominance in the EW landscape.

North America Electronic Warfare Market Competitive Landscape

The North America EW market is characterized by the presence of key players who drive innovation and maintain competitive advantage. These companies leverage extensive experience, technological expertise, and strategic partnerships to cater to the evolving defense needs.

North America Electronic Warfare Industry Analysis

Growth Drivers

- Increasing Expenditure: In 2024, the United States government allocated $842 billion to defense, marking a significant commitment to advanced military capabilities, including electronic warfare systems. This rise in defense spending provides substantial support for EW system development, procurement, and modernization, as nations address national security concerns through advanced electronic defense solutions.

- Advancements in EW Systems: North America has seen significant technological advancements in EW, with the U.S. dedicating over $50 billion in research and development for defense technologies in 2023. The DARPA has focused on enhancing EW technologies, including radar jamming and cyber-defense tools. This investment drives the adoption of modern EW solutions, incorporating innovations in signal processing and real-time data analytics, which strengthen combat readiness and strategic advantage.

- Rising Geopolitical Tensions: Growing geopolitical tensions and military activities in key regions have led the U.S. and Canada to strengthen their focus on electronic warfare (EW). By deploying EW resources strategically, they aim to address both conventional and unconventional threats, enhancing defense capabilities in high-risk areas. This proactive approach allows for improved readiness in regions with frequent military engagement, reinforcing national security measures.

Market Challenges

- High Development and Maintenance Costs: Developing and maintaining advanced EW systems involves substantial expenses due to specialized equipment and frequent technological upgrades needed to counter evolving threats. These high costs strain budget allocations, especially for countries like Canada, making it challenging to sustain state-of-the-art systems and impacting the overall pace of modernization in electronic warfare.

- Rapid Technological Obsolescence: The fast-paced technological evolution in the EW sector necessitates frequent system upgrades to stay effective. This rapid obsolescence creates challenges for North American defense budgets, as both the U.S. and Canada must allocate resources to continuously update or replace legacy systems, prioritizing modernization to keep pace with advancements.

North America Electronic Warfare Market Future Outlook

Over the next five years, the North America EW market is expected to witness significant growth, driven by continuous government support, advancements in EW technology, and increasing demand for sophisticated defense systems. The integration of artificial intelligence and machine learning into EW systems is anticipated to enhance capabilities, providing a competitive edge in modern warfare scenarios.

Market Opportunities

- Expansion into Cyber Warfare Capabilities: As cybersecurity threats grow, North American defense sectors are increasingly integrating electronic warfare (EW) with cyber warfare capabilities. This strategic expansion allows for the development of integrated cyber-electronic systems, creating comprehensive defense solutions that address complex and evolving threats, enhancing overall national security measures.

- Collaboration with Commercial Tech Firms: Collaborating with commercial tech firms enables the defense sector to incorporate advanced technologies such as AI and cloud computing into EW systems. These partnerships foster innovation by leveraging the expertise of technology companies, ensuring that EW solutions are equipped with the latest advancements to maintain operational effectiveness.

Scope of the Report

|

By Capability |

Electronic Attack (EA) Electronic Protection (EP) Electronic Support (ES) |

|

By Platform |

Airborne Naval Ground Space |

|

By Product Type |

EW Equipment EW Operational Support |

|

By Technology |

Radar Warning Receivers Jammers Directed Energy Weapons Anti-Radiation Missiles |

|

By Region |

United States Canada Mexico |

Products

Key Target Audience

Defense Contractors

Technology Industry

System Integrators

Defense Procurement Agencies

Military and Defense Agencies (U.S. Department of Defense)

Government and Regulatory Bodies (Federal Communications Commission)

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Lockheed Martin Corporation

Raytheon Technologies Corporation

Northrop Grumman Corporation

BAE Systems plc

L3Harris Technologies, Inc.

Boeing Defense, Space & Security

SAAB AB

Thales Group

General Dynamics Corporation

Cobham Limited

Table of Contents

1. North America Electronic Warfare Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Electronic Warfare Market Size (USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Electronic Warfare Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Defense Expenditure

3.1.2. Technological Advancements in EW Systems

3.1.3. Rising Geopolitical Tensions

3.1.4. Integration of AI and Machine Learning

3.2. Market Challenges

3.2.1. High Development and Maintenance Costs

3.2.2. Rapid Technological Obsolescence

3.2.3. Regulatory and Compliance Issues

3.3. Opportunities

3.3.1. Expansion into Cyber Warfare Capabilities

3.3.2. Collaboration with Commercial Tech Firms

3.3.3. Development of Cognitive EW Systems

3.4. Trends

3.4.1. Adoption of Open Architecture Systems

3.4.2. Miniaturization of EW Equipment

3.4.3. Increased Use of Unmanned Systems

3.5. Government Regulations

3.5.1. Defense Acquisition Policies

3.5.2. Export Control Regulations

3.5.3. Cybersecurity Standards

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. North America Electronic Warfare Market Segmentation

4.1. By Capability (Value %)

4.1.1. Electronic Attack (EA)

4.1.2. Electronic Protection (EP)

4.1.3. Electronic Support (ES)

4.2. By Platform (Value %)

4.2.1. Airborne

4.2.2. Naval

4.2.3. Ground

4.2.4. Space

4.3. By Product Type (Value %)

4.3.1. EW Equipment

4.3.2. EW Operational Support

4.4. By Technology (Value %)

4.4.1. Radar Warning Receivers

4.4.2. Jammers

4.4.3. Directed Energy Weapons

4.4.4. Anti-Radiation Missiles

4.5. By Region (Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Electronic Warfare Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Lockheed Martin Corporation

5.1.2. Raytheon Technologies Corporation

5.1.3. Northrop Grumman Corporation

5.1.4. BAE Systems plc

5.1.5. L3Harris Technologies, Inc.

5.1.6. Boeing Defense, Space & Security

5.1.7. SAAB AB

5.1.8. Thales Group

5.1.9. General Dynamics Corporation

5.1.10. Cobham Limited

5.1.11. Mercury Systems, Inc.

5.1.12. Rohde & Schwarz GmbH & Co KG

5.1.13. Leonardo S.p.A.

5.1.14. Elbit Systems Ltd.

5.1.15. Israel Aerospace Industries (IAI)

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, R&D Expenditure, Market Share, Key Contracts, Strategic Alliances)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Electronic Warfare Market Regulatory Framework

6.1. Defense Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. North America Electronic Warfare Future Market Size (USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Electronic Warfare Market Analysts Recommendations

8.1. TAM/SAM/SOM Analysis

8.2. Customer Cohort Analysis

8.3. Marketing Initiatives

8.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the North America Electronic Warfare Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the North America Electronic Warfare Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple electronic warfare system manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the North America Electronic Warfare market.

Frequently Asked Questions

01. How big is the North America Electronic Warfare Market?

The North America Electronic Warfare market is valued at USD 7.5 billion, driven by increasing defense expenditures and technological advancements.

02. What are the challenges in the North America Electronic Warfare Market?

Challenges in North America Electronic Warfare market include high development and maintenance costs, rapid technological obsolescence, and regulatory and compliance issues that can impact market growth. These challenges create barriers for smaller players and require established companies to continuously innovate.

03. Who are the major players in the North America Electronic Warfare Market?

Key players in the North America Electronic Warfare market include Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, BAE Systems plc, and L3Harris Technologies, Inc. These companies lead due to their extensive experience, innovation, and established government contracts.

04. What are the growth drivers of the North America Electronic Warfare Market?

The North America Electronic Warfare market is propelled by factors such as increasing defense budgets, advancements in EW technologies, and rising geopolitical tensions. Additionally, the integration of AI and machine learning into EW systems enhances the market's appeal.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.