North America Food Technology Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD8897

Region:North America

Author(s):Vijay Kumar

Product Code:KROD8897

November 2024

99

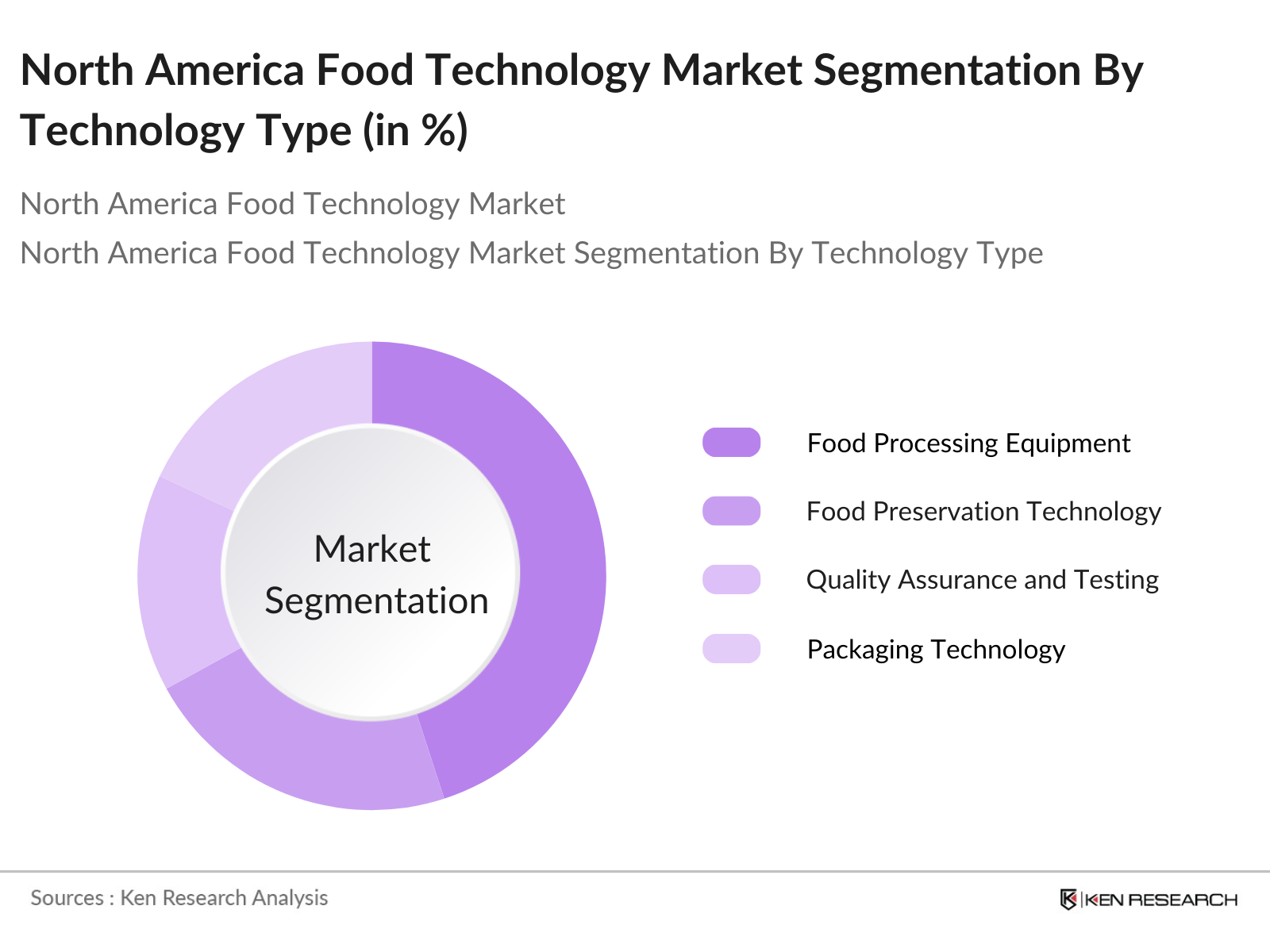

By Technology Type: The North America Food Technology market is segmented by technology type, including food processing equipment, food preservation technology, quality assurance and testing, packaging technology, and traceability solutions. Among these, food processing equipment holds the dominant market share due to its essential role in manufacturing, processing, and packaging a wide variety of food products, with innovations aimed at improving efficiency and reducing waste.

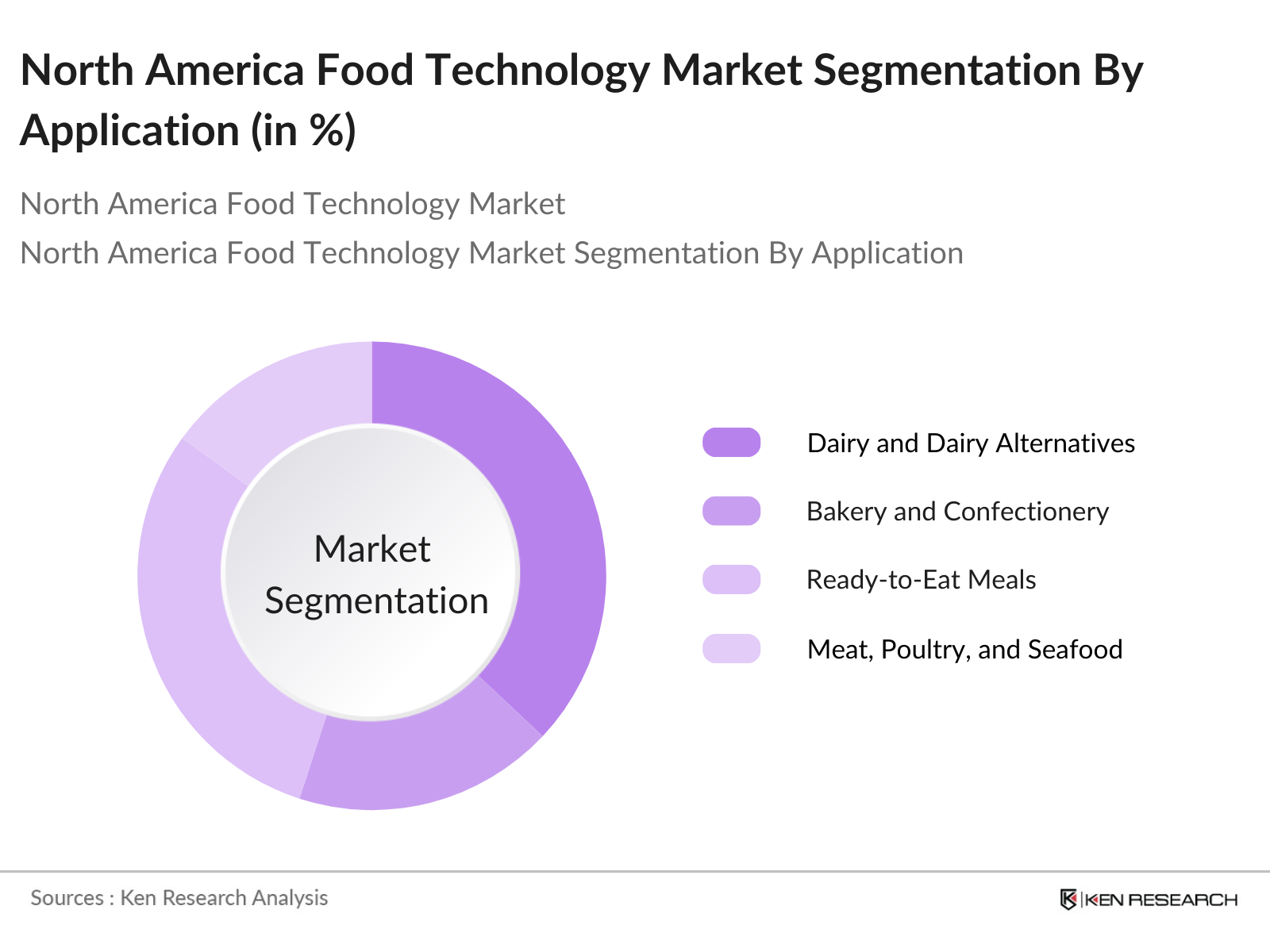

By Application: The market is segmented by application into dairy and dairy alternatives, bakery and confectionery, ready-to-eat meals, meat, poultry, and seafood, and beverages. Among these, the ready-to-eat meals segment holds the largest market share, as busy lifestyles have increased consumer demand for convenient meal options. Additionally, the availability of healthier, organic, and vegan options has expanded the consumer base, further boosting this segment's growth.

The North America Food Technology market is dominated by a few key players, with market consolidation reflecting the substantial influence of these companies in terms of resources, technology, and R&D capabilities.

Over the next five years, the North America Food Technology market is expected to experience significant growth due to increasing consumer demand for health-conscious, plant-based, and sustainable food products. Key driving factors include continued technological advancements, a shift toward more efficient food production methods, and growing awareness of food security and sustainability.

|

Technology Type |

Food Processing Equipment Food Preservation Technology Quality Assurance and Testing Packaging Technology Traceability and Blockchain Solutions |

|

Application |

Dairy and Dairy Alternatives Bakery and Confectionery Ready-to-Eat Meals Meat, Poultry, and Seafood Beverages and Beverages Alternatives |

|

Product Innovation |

Plant-Based Foods Functional Foods Clean Label Foods Organic and non-GMO Foods |

|

End User |

Food Manufacturers Food Service Providers Retail and E-Commerce Agriculture and Food Suppliers |

|

Region |

United States Canada Mexico |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate and Key Drivers

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Major Developments and Milestones

3.1. Growth Drivers

3.1.1. Technological Advancements in Food Processing

3.1.2. Rising Demand for Sustainable and Plant-Based Alternatives

3.1.3. Increased Focus on Food Safety and Transparency

3.1.4. Growth in E-commerce and Online Food Delivery

3.2. Market Challenges

3.2.1. Regulatory Hurdles and Compliance

3.2.2. High Initial Capital Requirements

3.2.3. Limited Skilled Workforce in Emerging Tech Areas

3.3. Opportunities

3.3.1. Integration of AI and IoT in Food Production

3.3.2. Expansion of Personalized Nutrition Solutions

3.3.3. Innovations in Alternative Proteins

3.4. Key Market Trends

3.4.1. Growth of Plant-Based and Lab-Grown Meat Markets

3.4.2. Adoption of Automation and Robotics

3.4.3. Data-Driven Supply Chain Optimization

3.5. Regulatory Overview

3.5.1. FDA Compliance Requirements

3.5.2. Food Safety Modernization Act (FSMA)

3.5.3. Nutritional Labeling and Transparency Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem Overview

4.1. By Technology Type (In Value %)

4.1.1. Food Processing Equipment

4.1.2. Food Preservation Technology

4.1.3. Quality Assurance and Testing

4.1.4. Packaging Technology

4.1.5. Traceability and Blockchain Solutions

4.2. By Application (In Value %)

4.2.1. Dairy and Dairy Alternatives

4.2.2. Bakery and Confectionery

4.2.3. Ready-to-Eat Meals

4.2.4. Meat, Poultry, and Seafood

4.2.5. Beverages and Beverages Alternatives

4.3. By Product Innovation (In Value %)

4.3.1. Plant-Based Foods

4.3.2. Functional Foods

4.3.3. Clean Label Foods

4.3.4. Organic and Non-GMO Foods

4.4. By End User (In Value %)

4.4.1. Food Manufacturers

4.4.2. Food Service Providers

4.4.3. Retail and E-Commerce

4.4.4. Agriculture and Food Suppliers

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5.1. Detailed Profiles of Major Competitors

5.1.1. Cargill

5.1.2. ADM (Archer Daniels Midland)

5.1.3. Tyson Foods

5.1.4. Impossible Foods

5.1.5. Beyond Meat

5.1.6. Kelloggs (Morningstar Farms)

5.1.7. Nestl USA

5.1.8. Maple Leaf Foods

5.1.9. Ingredion Incorporated

5.1.10. PepsiCo (Quaker Foods)

5.1.11. Danone North America

5.1.12. Conagra Brands

5.1.13. General Mills

5.1.14. Unilever (Ben & Jerrys)

5.1.15. Oatly Inc.

5.2. Cross Comparison Parameters (Headquarters, Market Position, Revenue, Employee Count, Research Expenditure, Sustainability Initiatives, Product Range, Key Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment and Funding Landscape

5.7. Government Subsidies and Grants

5.8. Private Equity and Venture Capital Investments

6.1. Food Safety and Inspection Standards

6.2. Labeling and Nutritional Requirements

6.3. Environmental and Sustainability Standards

6.4. Intellectual Property and Patent Regulations

7.1. Forecasted Market Size and Growth Potential

7.2. Key Drivers of Future Market Growth

8.1. By Technology Type (In Value %)

8.2. By Application (In Value %)

8.3. By Product Innovation (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9.1. Total Addressable Market (TAM) Analysis

9.2. Segment Attractiveness Analysis

9.3. Strategic Initiatives for Market Penetration

9.4. Opportunity Analysis and Market Entry Recommendations

Disclaimer Contact UsThis initial phase constructs an ecosystem map encompassing major stakeholders in the North America Food Technology Market. Extensive desk research and analysis through proprietary databases are conducted to identify critical variables influencing market trends and challenges.

In this phase, historical data on market size, industry growth, and technology adoption is gathered. Specific market segments and sub-segments are assessed, ensuring reliability and accuracy of revenue and growth estimates across the market.

Formulated hypotheses are validated through computer-assisted telephone interviews (CATIs) with industry experts, providing direct insights on technological advancements and operational trends within the food technology sector.

The final phase involves synthesizing the validated data with direct insights from industry players, verifying segment dynamics, and ensuring an accurate, comprehensive analysis of the North America Food Technology Market.

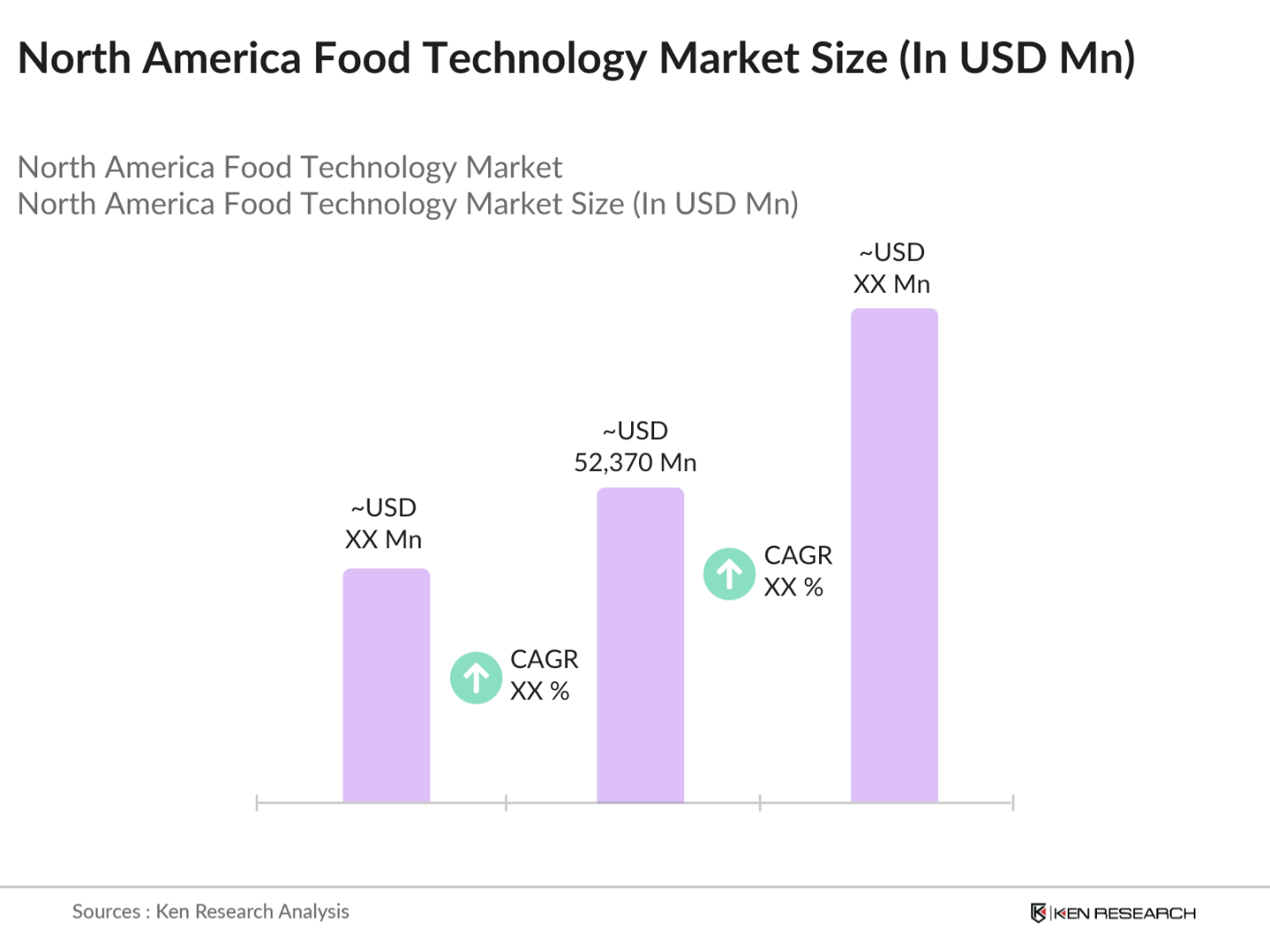

The North America Food Technology market is valued at USD 52,370 million, based on a five-year historical analysis. This market's growth is driven by rapid advancements in food processing and packaging technologies, alongside increasing consumer demand for healthier, sustainable, and convenient food options.

Challenges include regulatory compliance, high initial investment requirements, and the limited availability of skilled labor for specialized technologies.

Key players include Cargill, ADM, Tyson Foods, Beyond Meat, and Nestl USA, each dominating through innovations in food processing and sustainable product offerings.

Growth is driven by consumer interest in health-conscious diets, plant-based food options, and the adoption of advanced processing technologies aimed at enhancing food safety and sustainability.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.