North America Frozen Food Market Outlook to 2030

Region:United States

Author(s):Yogita Sahu

Product Code:KROD3692

Region:United States

Author(s):Yogita Sahu

Product Code:KROD3692

October 2024

96

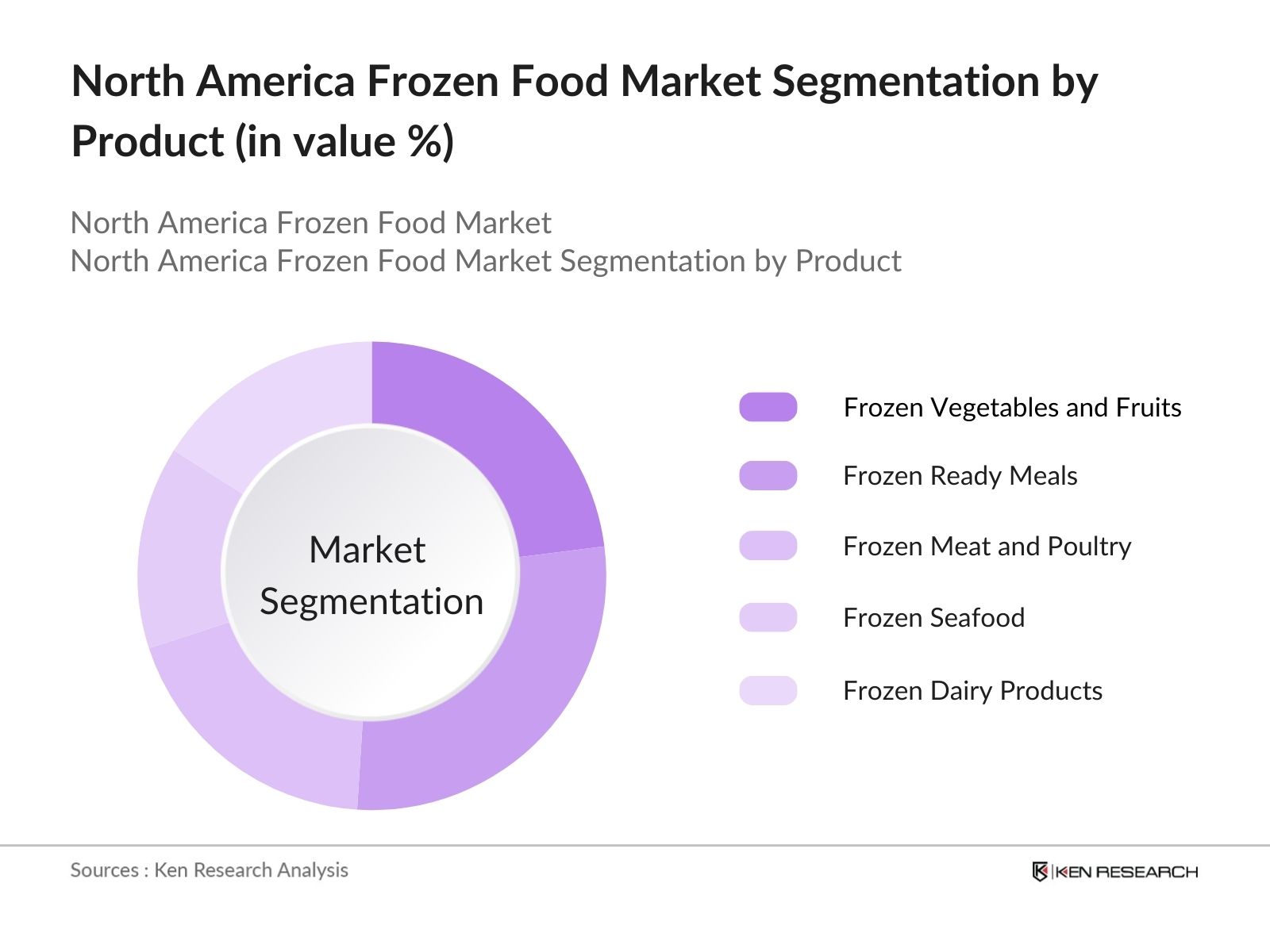

By Product Type: The market is segmented by product type into frozen vegetables and fruits, frozen ready meals, frozen meat and poultry, frozen seafood, and frozen dairy products. Recently, frozen ready meals have captured a share of the market, owing to the increasing demand for quick and easy meal options among urban populations.

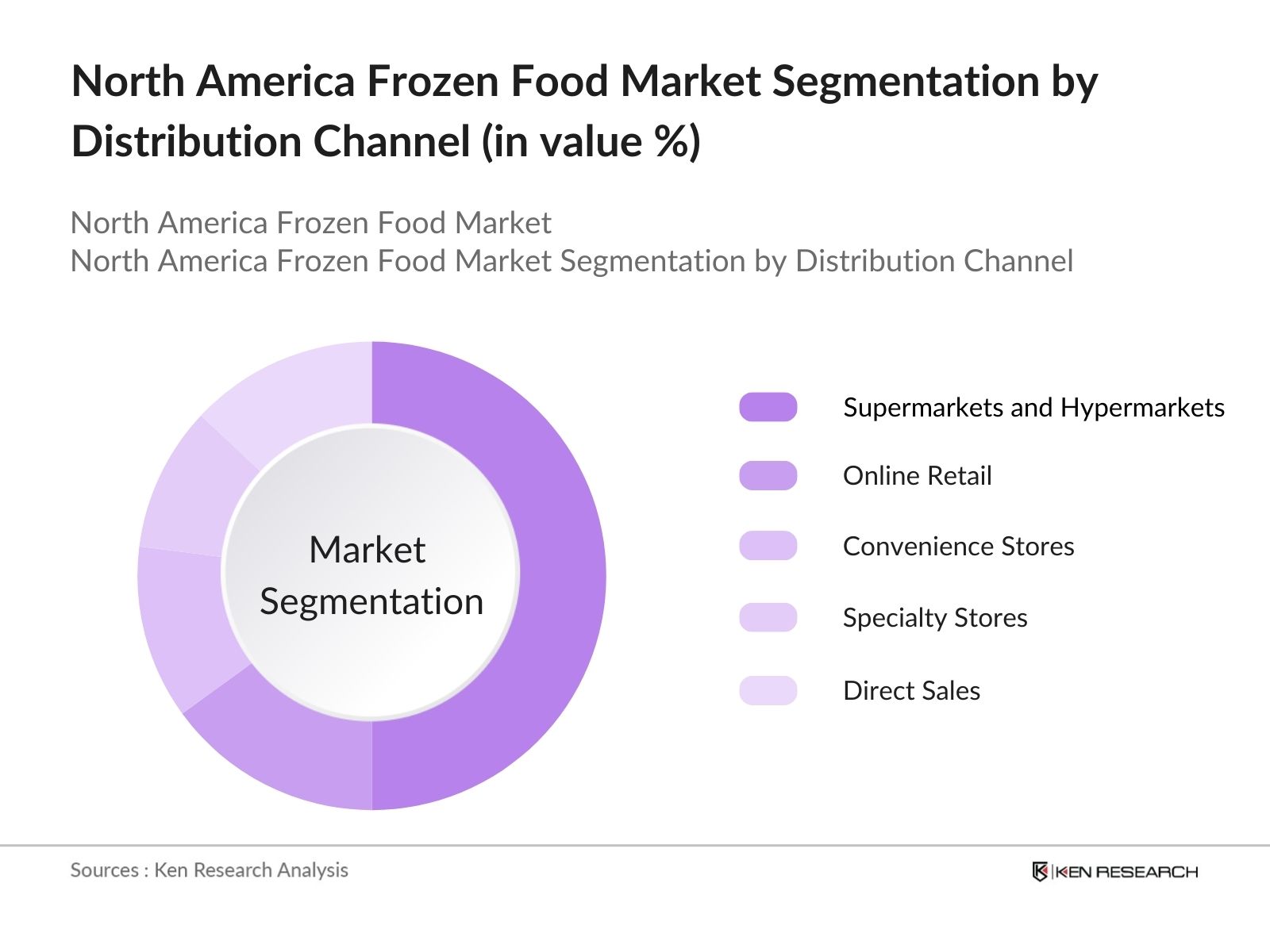

By Distribution Channel: The market is also segmented by distribution channel into supermarkets and hypermarkets, online retail, convenience stores, specialty stores, and direct sales. Supermarkets and hypermarkets hold the dominant market share due to the extensive variety of frozen food products they offer, along with their established infrastructure for frozen storage.

The market is dominated by a few major players who have established strong distribution networks, wide product portfolios, and strategic partnerships. These key players have a influence on market trends and consumer preferences.

|

Company |

Establishment Year |

Headquarters |

Revenue |

Product Range |

Sustainability Initiatives |

Distribution Network |

Strategic Collaborations |

Market Presence |

|

Nestl USA |

1866 |

Virginia, USA |

||||||

|

Conagra Brands, Inc. |

1919 |

Chicago, USA |

||||||

|

General Mills, Inc. |

1928 |

Minnesota, USA |

||||||

|

McCain Foods Limited |

1957 |

Ontario, Canada |

||||||

|

Tyson Foods, Inc. |

1935 |

Arkansas, USA |

Over the next five years, the North American frozen food industry is expected to show growth, driven by changing consumer lifestyles, innovations in food preservation technology, and increased demand for healthy and organic frozen products. Companies are likely to invest in expanding their product ranges to cater to the growing trend of plant-based and gluten-free frozen food options.

|

Product Type |

Frozen Vegetables and Fruits |

|

Frozen Ready Meals |

|

|

Frozen Meat and Poultry |

|

|

Frozen Seafood |

|

|

Frozen Dairy Products |

|

|

Distribution Channel |

Supermarkets and Hypermarkets |

|

Online Retail |

|

|

Convenience Stores |

|

|

Specialty Stores |

|

|

Direct Sales |

|

|

Consumer Type |

Retail Consumers |

|

Foodservice and HoReCa |

|

|

Category |

Organic Frozen Foods |

|

Conventional Frozen Foods |

|

|

Region |

United States |

|

Canada |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rise in Urbanization

3.1.2. Changing Consumer Lifestyles (Convenience and Ready-to-Eat Products)

3.1.3. Increasing Demand for Organic and Gluten-Free Frozen Foods

3.1.4. Technological Advancements in Cold Storage and Freezing Techniques

3.2. Market Challenges

3.2.1. High Operational Costs of Cold Chain Logistics

3.2.2. Perceived Inferior Quality Compared to Fresh Products

3.2.3. Regulatory Compliance with Food Safety Standards

3.3. Opportunities

3.3.1. Growth of E-Commerce Platforms for Frozen Food Distribution

3.3.2. Expansion of Plant-Based Frozen Foods

3.3.3. Untapped Markets in Rural and Suburban Areas

3.4. Trends

3.4.1. Increasing Adoption of Sustainable Packaging

3.4.2. Rising Demand for International and Ethnic Frozen Foods

3.4.3. Collaboration Between Retailers and Frozen Food Producers

3.5. Government Regulation

3.5.1. FDA Regulations on Frozen Food Safety

3.5.2. Labeling Requirements for Frozen Organic Products

3.5.3. Tariffs and Trade Regulations Affecting Import and Export

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (in Value %)

4.1.1. Frozen Vegetables and Fruits

4.1.2. Frozen Ready Meals

4.1.3. Frozen Meat and Poultry

4.1.4. Frozen Seafood

4.1.5. Frozen Dairy Products

4.2. By Distribution Channel (in Value %)

4.2.1. Supermarkets and Hypermarkets

4.2.2. Online Retail

4.2.3. Convenience Stores

4.2.4. Specialty Stores

4.2.5. Direct Sales

4.3. By Consumer Type (in Value %)

4.3.1. Retail Consumers

4.3.2. Foodservice and HoReCa (Hotels, Restaurants, Cafes)

4.4. By Category (in Value %)

4.4.1. Organic Frozen Foods

4.4.2. Conventional Frozen Foods

4.5. By Region (in Value %)

4.5.1. United States

4.5.2. Canada

5.1. Detailed Profiles of Major Companies

5.1.1. Nestl USA

5.1.2. Conagra Brands, Inc.

5.1.3. General Mills, Inc.

5.1.4. Kellogg Company

5.1.5. Tyson Foods, Inc.

5.1.6. Maple Leaf Foods

5.1.7. McCain Foods Limited

5.1.8. The Kraft Heinz Company

5.1.9. Unilever PLC

5.1.10. Ajinomoto Co., Inc.

5.1.11. Amy's Kitchen, Inc.

5.1.12. JBS USA

5.1.13. Schwans Company

5.1.14. Pinnacle Foods, Inc.

5.1.15. Iceland Foods Ltd

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Revenue, Product Range, Distribution Network, Sustainability Initiatives, Strategic Collaborations, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Subsidies

5.9. Private Equity Investments

6.1. Food Safety Modernization Act (FSMA)

6.2. Import and Export Compliance

6.3. Labeling and Nutritional Guidelines for Frozen Foods

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (in Value %)

8.2. By Distribution Channel (in Value %)

8.3. By Consumer Type (in Value %)

8.4. By Category (in Value %)

8.5. By Region (in Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial phase involves mapping the entire frozen food industry ecosystem across North America. Comprehensive desk research is conducted to gather information from proprietary databases and public sources. This step helps identify key variables, including consumer preferences, supply chain factors, and regulatory requirements.

In this phase, historical data on the frozen food market is compiled to assess its growth over the last five years. The analysis includes a thorough evaluation of market penetration, competition, and evolving consumer demands, which helps to determine key growth drivers and market constraints.

To validate the gathered data, hypotheses on market trends and growth drivers are formulated and tested through interviews with key industry experts. This helps ensure the accuracy of market projections and insights into market dynamics.

The final stage involves synthesizing all the collected data into a comprehensive report. This includes detailed insights from market participants, data-driven analysis, and validation through triangulation to provide a complete and accurate overview of the North America frozen food market.

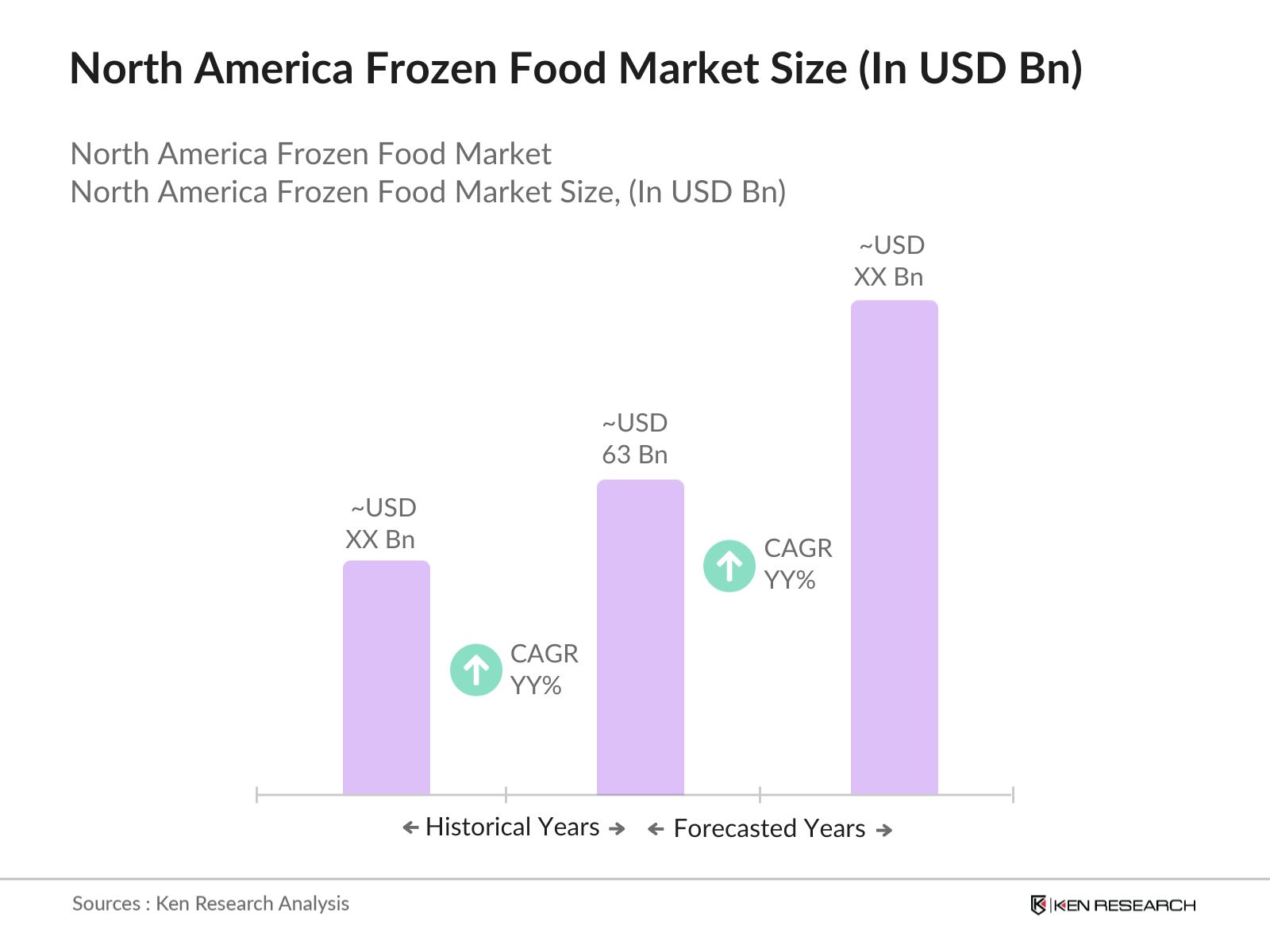

The North America frozen food market is valued at USD 63 billion, driven by increasing consumer demand for convenient, ready-to-eat meals and the growing trend towards organic and plant-based frozen products.

Challenges in the North America frozen food market include high operational costs for cold chain logistics and maintaining regulatory compliance with food safety standards. Additionally, the perception of frozen foods being of inferior quality compared to fresh products presents a hurdle.

Key players in the North America frozen food market include Nestl USA, Conagra Brands, General Mills, Tyson Foods, and McCain Foods. These companies lead the market due to their strong distribution networks and extensive product portfolios.

Growth drivers in the North America frozen food market include the increasing adoption of e-commerce for food purchasing, technological advancements in food preservation, and the rising demand for healthy and organic frozen food options.

Emerging trends in the North America frozen food market include the growing popularity of plant-based and gluten-free frozen foods, along with the use of sustainable packaging solutions. The expansion of online retail platforms is also becoming a major trend in this market.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.