North America Fuel Additives Market Outlook to 2030

Region:North America

Author(s):Naman Rohilla

Product Code:KROD5304

December 2024

97

About the Report

North America Fuel Additives Market Overview

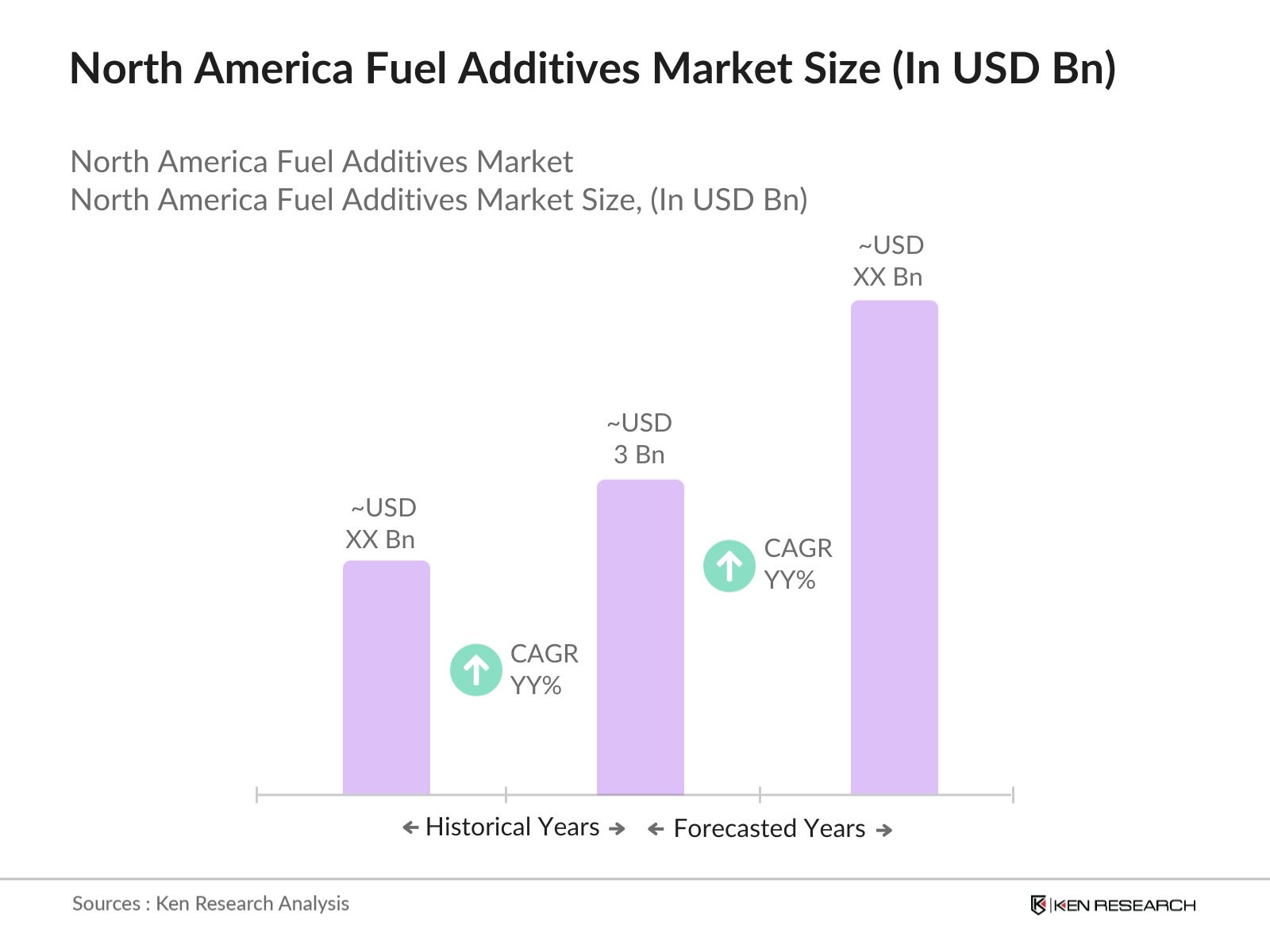

- The North America fuel additives market is valued at USD 3 billion, driven by the increasing demand for cleaner and more efficient fuels across the automotive, aviation, and marine sectors. This demand is propelled by stringent emission regulations imposed by government bodies such as the Environmental Protection Agency (EPA) and the increasing focus on reducing carbon emissions. Additionally, the rise of biofuels and advancements in additive technology are contributing to market growth, with manufacturers focusing on enhancing fuel performance while adhering to environmental standards.

- In the North American region, the United States holds a dominant position due to its well-established infrastructure in the automotive and aviation sectors, coupled with a robust regulatory framework promoting the use of fuel additives to curb emissions. Cities like Houston and Chicago are key hubs in the industry, benefiting from a strong presence of refineries and fuel distribution networks. Moreover, Canada also plays a crucial role due to its increasing focus on environmental sustainability and advancements in fuel efficiency technologies.

- The U.S. Clean Air Act mandates stringent controls on vehicle emissions and fuel composition, impacting the fuel additives market. The Act requires the reduction of pollutants such as nitrogen oxides (NOx) and sulphur, which has led to the widespread adoption of sulphur-reducing additives. In 2022, the EPA reported that vehicle-related NOx emissions had decreased by 60% since the early 2000s, largely due to cleaner fuels and the use of advanced additives.

North America Fuel Additives Market Segmentation

- By Product Type: The North America fuel additives market is segmented by product type into deposit control additives, cetane improvers, lubricity improvers, corrosion inhibitors, and antioxidants. Among these, deposit control additives dominate the market due to their essential role in improving fuel performance and efficiency. These additives prevent the formation of deposits in the engine, ensuring smooth functioning and reducing maintenance costs for vehicles. The increasing demand for high-performance vehicles and stringent emission standards further drive the need for deposit control additives, making them a vital component in the fuel industry.

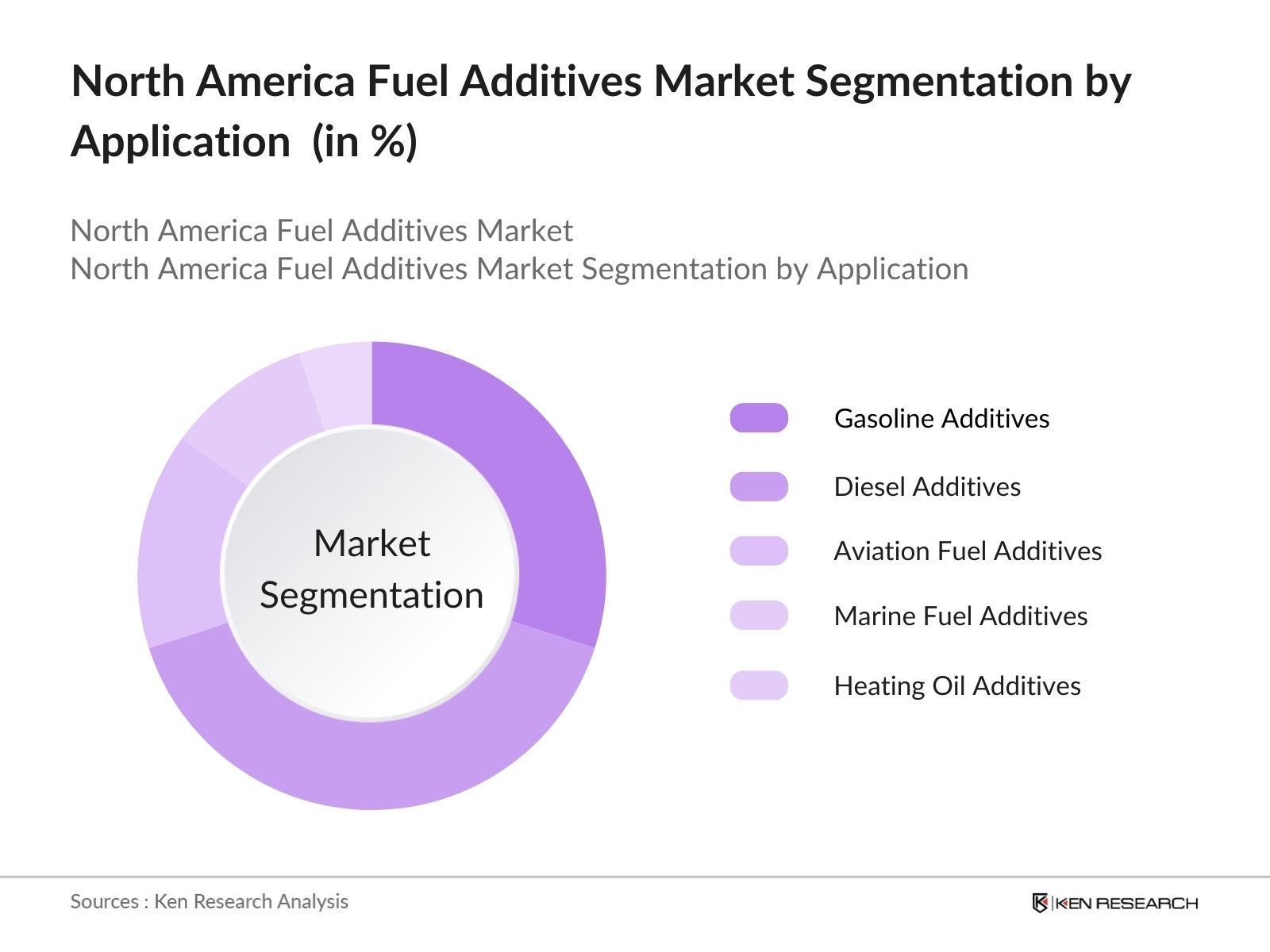

- By Application: The North America fuel additives market is segmented by application into gasoline additives, diesel additives, aviation fuel additives, marine fuel additives, and heating oil additives. Diesel additives hold a dominant market share due to the widespread use of diesel fuel in transportation and industrial sectors across North America. Diesel engines are integral to logistics and heavy machinery, and additives are essential for improving diesel quality, enhancing combustion, and reducing emissions. Additionally, government regulations aimed at lowering sulfur content in diesel fuels have further boosted the adoption of these additives.

North America Fuel Additives Market Competitive Landscape

The North American fuel additives market is characterized by the presence of both global and regional players. The market is dominated by a few key companies with strong product portfolios, technological capabilities, and extensive distribution networks. The market is competitive, with leading companies such as Afton Chemical Corporation, BASF SE, and Lubrizol Corporation at the forefront of innovation. These companies focus on enhancing product performance while meeting strict environmental regulations, maintaining a competitive edge.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

R&D Investment (USD Mn) |

Employee Count |

Geographic Reach |

Patents |

Partnerships |

Product Launches |

|

Afton Chemical Corporation |

1924 |

Richmond, USA |

- |

- |

- |

- |

- |

- |

- |

|

BASF SE |

1865 |

Ludwigshafen, Germany |

- |

- |

- |

- |

- |

- |

- |

|

Chevron Oronite Company LLC |

1917 |

San Ramon, USA |

- |

- |

- |

- |

- |

- |

- |

|

Lubrizol Corporation |

1928 |

Wickliffe, USA |

- |

- |

- |

- |

- |

- |

- |

|

Innospec Inc. |

1938 |

Englewood, USA |

- |

- |

- |

- |

- |

- |

- |

North America Fuel Additives Market Analysis

North America Fuel Additives Market Growth Drivers

- Increasing Demand for Clean and Efficient Fuels: The demand for clean and efficient fuels has been increasing across North America due to heightened concerns regarding air pollution and the environmental impacts of traditional fossil fuels. According to the U.S. Energy Information Administration (EIA), the U.S. consumed approximately 20 million barrels of petroleum per day in 2023, with a growing portion of this consumption driven by cleaner fuel options. The automotive and industrial sectors, particularly, are seeking advanced fuel additives to enhance combustion efficiency and reduce toxic emissions, contributing to the demand for fuel additives across the region.

- Expansion of the Automotive and Aviation Industry: In 2023, North America witnessed substantial growth in its automotive and aviation sectors, which directly correlates with the demand for fuel additives. Data from the International Organization of Motor Vehicle Manufacturers (OICA) shows that North American countries produced over 15 million vehicles in 2022. In the aviation sector, the U.S. Department of Transportation reported an increase in air travel demand, leading to higher jet fuel consumption and the subsequent need for performance-enhancing additives to maintain fuel efficiency and meet environmental standards.

- Focus on Reducing Carbon Footprint: There is a growing focus on reducing the carbon footprint across North America due to governmental pressure and consumer awareness. According to the World Bank, the region emitted approximately 6.7 billion metric tons of CO2 in 2022. Initiatives such as Canadas carbon pricing and the U.S. aim to achieve net-zero emissions by 2050, pushing industries to adopt fuel additives that help lower carbon emissions and meet the regions environmental targets. This focus drives the growth of the fuel additives market as companies strive to meet lower emission standards.

North America Fuel Additives Market Challenges

- Fluctuating Crude Oil Prices: Crude oil prices play a major role in determining the cost structure of fuel additives. According to the U.S. Energy Information Administration, crude oil prices fluctuated between $65 and $95 per barrel in 2023 due to geopolitical tensions and supply chain disruptions. These fluctuations make it challenging for manufacturers to maintain consistent pricing for fuel additives, as crude oil derivatives are key components in their production. This unpredictability affects the profitability of fuel additive manufacturers in North America.

- Environmental Impact of Certain Additives: While fuel additives improve fuel efficiency and emissions, some of them, like metallic additives, have raised concerns over environmental impacts. In 2023, the U.S. National Oceanic and Atmospheric Administration (NOAA) highlighted the negative effects of heavy metals from certain fuel additives, such as manganese-based compounds, on air quality and aquatic ecosystems. The environmental concerns surrounding these additives pose regulatory challenges and pressure on manufacturers to innovate and produce eco-friendly alternatives.

North America Fuel Additives Market Future Outlook

Over the next five years, the North America fuel additives market is expected to witness growth driven by the increased focus on reducing emissions, improving fuel efficiency, and the development of bio-based additives. Advancements in additive technology, particularly in areas such as nanotechnology and multifunctional additives, are expected to enhance the performance of fuels in both automotive and industrial applications. Furthermore, the rising adoption of electric vehicles (EVs) and hybrid vehicles may open new avenues for additive manufacturers to innovate products that cater to both traditional and alternative fuel vehicles. Overall, government regulations and the growing emphasis on sustainability will shape the future trajectory of the market.

North America Fuel Additives Market Opportunities

- Development of Bio-based Fuel Additives: The development of bio-based fuel additives is an emerging opportunity driven by North Americas focus on sustainability and reducing reliance on petrochemical derivatives. According to the U.S. Department of Agriculture, the bio-based products industry contributed $459 billion to the U.S. economy in 2022. The increased emphasis on bio-based fuels, coupled with the availability of agricultural feedstock in the region, supports the growth of bio-based fuel additives, providing a greener alternative to traditional additives and boosting market prospects.

- Rising Adoption of Electric Vehicles: Electric vehicle (EV) adoption is rising across North America, particularly in the U.S., where more than 800,000 EVs were sold in 2022, according to the U.S. Department of Energy. Although EVs reduce direct demand for traditional fuel additives, the hybrid vehicles and non-fully-electric fleet still require additives for efficiency. Additionally, advancements in battery chemistry and energy storage technology have led to a growing interest in lubricants and cooling fluids for EV batteries, creating new opportunities for additive manufacturers.

Scope of the Report

|

By Product Type |

Deposit Control Additives Cetane Improvers Lubricity Improvers Corrosion Inhibitors Antioxidants |

|

By Application |

Gasoline Additives Diesel Additives, Aviation Fuel Additives Marine Fuel Additives Heating Oil Additives |

|

By Fuel Type |

Gasoline Diesel Biofuels Jet Fuel Other Fuels |

|

By End-Use Industry |

Automotive Aviation Marine Power Generation Refining |

|

By Region |

United States Canada Mexico Rest of North America |

Products

Key Target Audience

Automotive Manufacturers

Aviation Fuel Suppliers

Marine Fuel Distributors

Fuel Refining Companies

Banks and Financial Institutions

Government and Regulatory Bodies (EPA, US Department of Energy)

Biofuel Producers

Chemical Manufacturers

Investor and Venture Capitalist Firms

Companies

Players Mentioned in the Market

Afton Chemical Corporation

BASF SE

Chevron Oronite Company LLC

Lubrizol Corporation

Innospec Inc.

Evonik Industries AG

Clariant AG

Dorf Ketal Chemicals

Infineum International Limited

TotalEnergies SE

Table of Contents

1. North America Fuel Additives Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Fuel Additives Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Fuel Additives Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand for Clean and Efficient Fuels

3.1.2. Government Regulations on Emission Control

3.1.3. Expansion of the Automotive and Aviation Industry

3.1.4. Focus on Reducing Carbon Footprint

3.2. Market Challenges

3.2.1. Fluctuating Crude Oil Prices

3.2.2. Environmental Impact of Certain Additives

3.2.3. High Production Costs for Fuel Additives

3.3. Opportunities

3.3.1. Development of Bio-based Fuel Additives

3.3.2. Rising Adoption of Electric Vehicles

3.3.3. Growing Investments in Research and Innovation

3.4. Trends

3.4.1. Adoption of Multifunctional Additives

3.4.2. Increased Use of Nanotechnology in Additive Formulation

3.4.3. Integration of Fuel Additives with Advanced Engine Technologies

3.5. Government Regulations

3.5.1. Clean Air Act Regulations

3.5.2. EPA Standards on Emissions

3.5.3. Fuel Quality Regulations

3.5.4. Incentives for Low-Emission Vehicles

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Refiners, Distributors, Automotive OEMs)

3.8. Porters Five Forces (Supplier Power, Buyer Power, Competitive Rivalry, Threat of Substitutes, Threat of New Entrants)

3.9. Competition Ecosystem (Overview of Key Competitors, Market Positioning)

4. North America Fuel Additives Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Deposit Control Additives

4.1.2. Cetane Improvers

4.1.3. Lubricity Improvers

4.1.4. Corrosion Inhibitors

4.1.5. Antioxidants

4.2. By Application (In Value %)

4.2.1. Gasoline Additives

4.2.2. Diesel Additives

4.2.3. Aviation Fuel Additives

4.2.4. Marine Fuel Additives

4.2.5. Heating Oil Additives

4.3. By Fuel Type (In Value %)

4.3.1. Gasoline

4.3.2. Diesel

4.3.3. Biofuels

4.3.4. Jet Fuel

4.3.5. Other Fuels

4.4. By End-Use Industry (In Value %)

4.4.1. Automotive

4.4.2. Aviation

4.4.3. Marine

4.4.4. Power Generation

4.4.5. Refining

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

4.5.4. Rest of North America

5. North America Fuel Additives Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Afton Chemical Corporation

5.1.2. BASF SE

5.1.3. Chevron Oronite Company LLC

5.1.4. Lubrizol Corporation

5.1.5. Innospec Inc.

5.1.6. Evonik Industries AG

5.1.7. Clariant AG

5.1.8. Dorf Ketal Chemicals

5.1.9. Infineum International Limited

5.1.10. TotalEnergies SE

5.1.11. Baker Hughes

5.1.12. Cummins Inc.

5.1.13. Croda International Plc

5.1.14. LANXESS AG

5.1.15. Solvay S.A.

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters

5.2.3. Inception Year

5.2.4. Revenue

5.2.5. R&D Investments

5.2.6. Patent Filings

5.2.7. Geographical Reach

5.2.8. Strategic Partnerships

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Fuel Additives Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. North America Fuel Additives Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Fuel Additives Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Fuel Type (In Value %)

8.4. By End-Use Industry (In Value %)

8.5. By Region (In Value %)

9. North America Fuel Additives Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research process began by identifying key variables influencing the North America fuel additives market. This involved mapping the industrys major stakeholders, including fuel producers, distributors, and regulatory bodies. Extensive desk research was conducted using secondary databases to gather key information about market trends, growth drivers, and challenges.

Step 2: Market Analysis and Construction

This step involved compiling historical data related to fuel additive penetration across various end-use industries such as automotive, aviation, and marine. The analysis also included assessing industry-specific developments in additive technologies and regulatory impacts. A detailed examination of market revenue and product segmentation was conducted to ensure accuracy in projections.

Step 3: Hypothesis Validation and Expert Consultation

To validate the research findings, in-depth interviews were conducted with industry experts from major companies and stakeholders across the value chain. These consultations provided crucial insights into operational practices, market dynamics, and technological innovations. The information gathered from experts was used to fine-tune the market analysis.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing all the data collected and validating it against real-world applications. The research findings were cross-referenced with proprietary databases and industry reports to produce a comprehensive and accurate overview of the North America fuel additives market.

Frequently Asked Questions

01. How big is the North America Fuel Additives Market?

The North America fuel additives market was valued at USD 3 billion, driven by stringent environmental regulations and the increasing demand for cleaner fuels across key industries such as automotive, aviation, and marine.

02. What are the challenges in the North America Fuel Additives Market?

Challenges in the North America fuel additives market include fluctuating crude oil prices, environmental concerns related to certain additives, and the high production costs associated with advanced fuel additives.

03. Who are the major players in the North America Fuel Additives Market?

Key players in the North America fuel additives market include Afton Chemical Corporation, BASF SE, Chevron Oronite Company LLC, Lubrizol Corporation, and Innospec Inc., each leading in product innovation and regulatory compliance.

04. What are the growth drivers of the North America Fuel Additives Market?

The North America fuel additives market is driven by stringent emission regulations, the rising demand for fuel efficiency, and the expansion of end-use industries such as automotive and aviation. Additionally, advancements in bio-based fuel additives are contributing to market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.