North America HVAC Equipment Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD4250

November 2024

91

About the Report

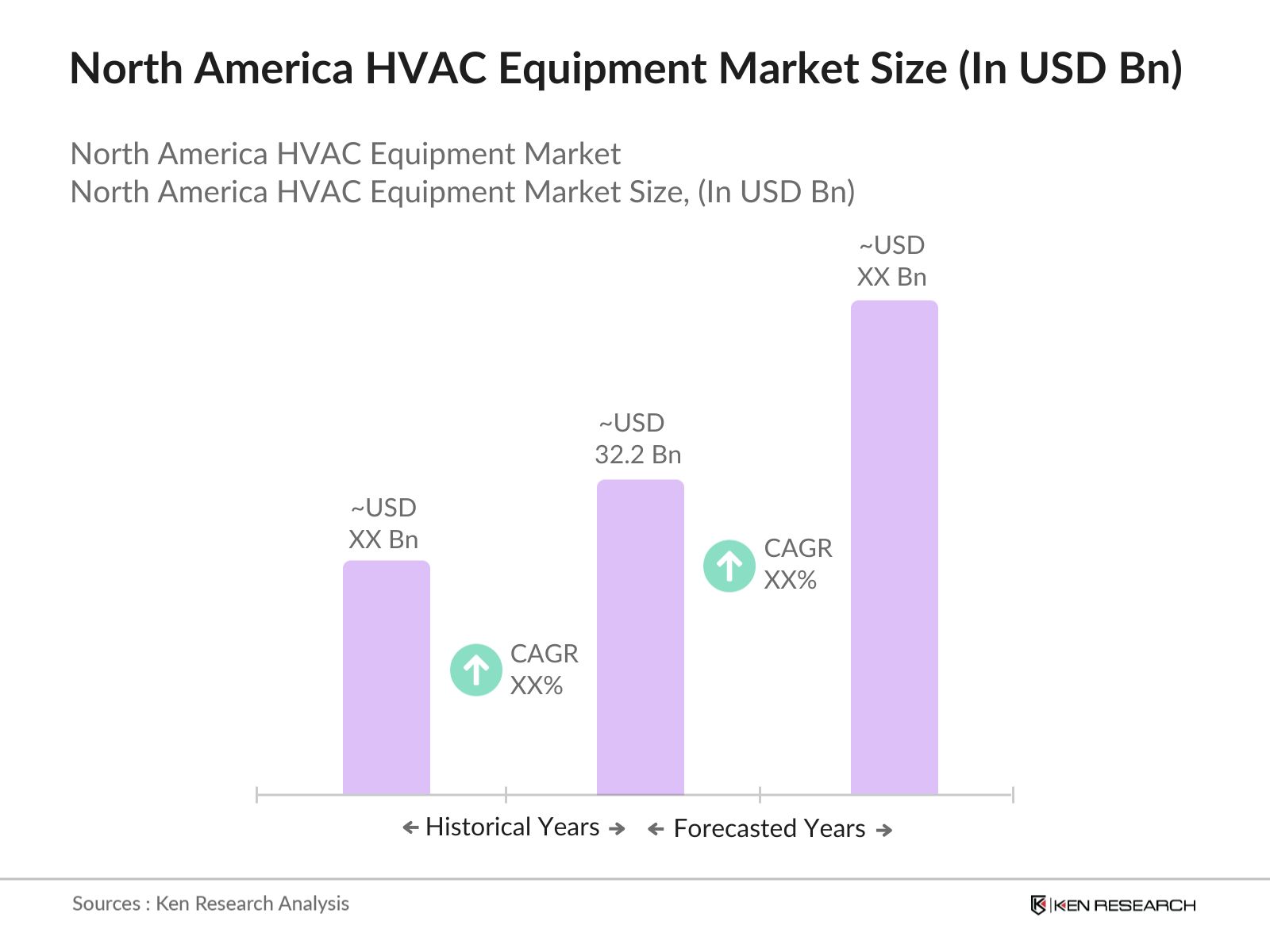

North America HVAC Equipment Market Overview

- The North American HVAC Equipment market is valued at USD 32.2 billion, based on a comprehensive five-year analysis. This market is primarily driven by the increasing demand for energy-efficient solutions and the integration of smart technologies in heating, ventilation, and air conditioning systems. The demand for HVAC systems is heightened by the growing urbanization and infrastructure development in major metropolitan areas. Additionally, the stringent environmental regulations for energy consumption are pushing manufacturers to innovate and offer more sustainable, energy-efficient products.

- In North America, the United States and Canada are the dominant countries in the HVAC market. These regions are key players due to their well-developed infrastructure, cold climates in parts of the countries, and high construction activity, both residential and commercial. The U.S. dominates due to its advanced technology adoption in smart homes and automation systems, while Canada shows significant demand for energy-efficient heating systems because of its colder climate, requiring HVAC solutions year-round.

- The EPA has introduced stringent regulations regarding the use of refrigerants in HVAC systems as part of its broader environmental protection efforts. In 2024, the agencys guidelines under the Significant New Alternatives Policy (SNAP) continue to phase out hydrofluorocarbons (HFCs), requiring the use of lower-global warming potential (GWP) refrigerants. This has prompted a shift toward environmentally friendly refrigerants such as R-32, which are now standard in new HVAC installations. The EPAs regulations are designed to align the HVAC industry with U.S. goals of reducing greenhouse gas emissions, contributing to a cleaner environment.

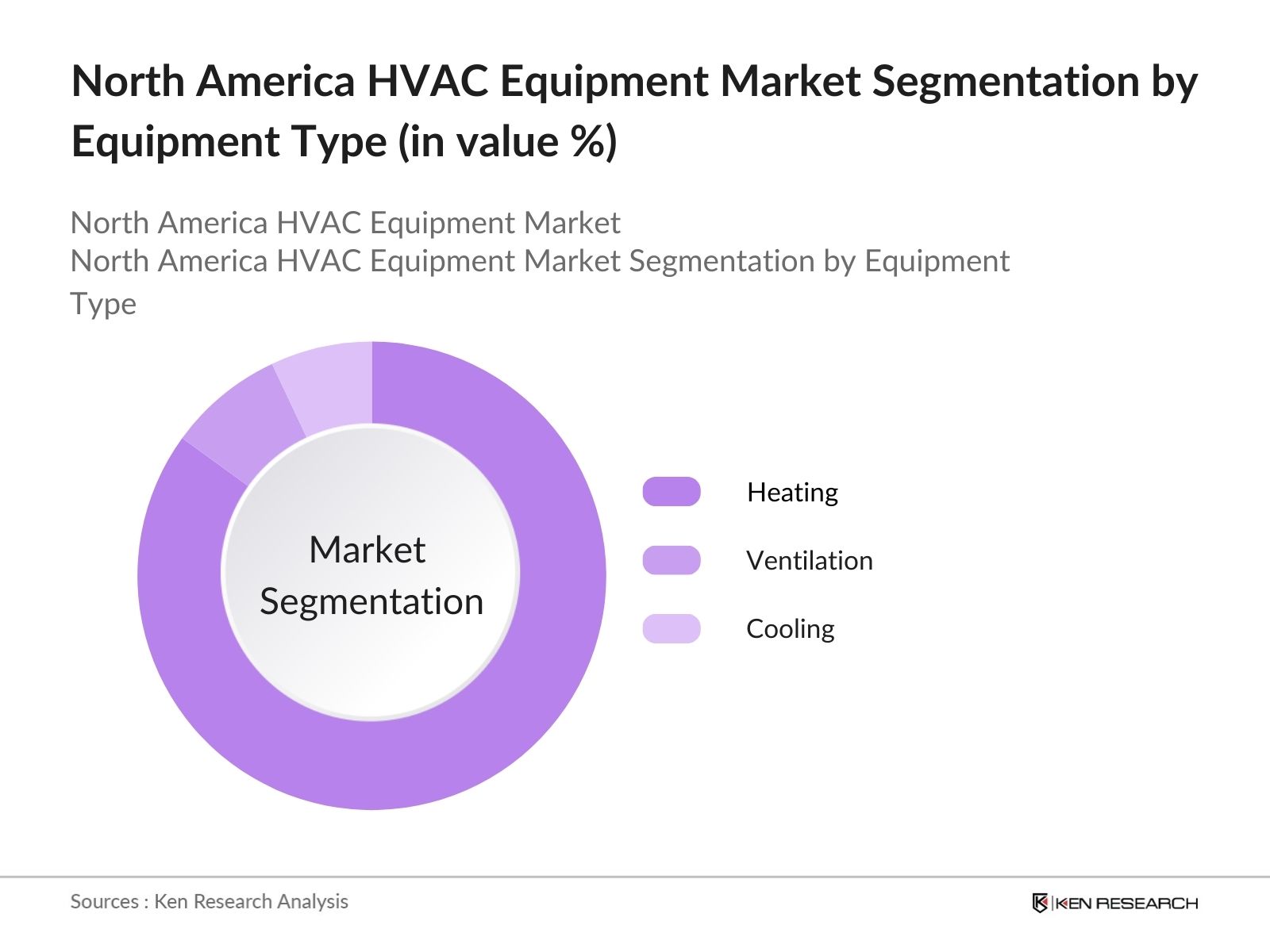

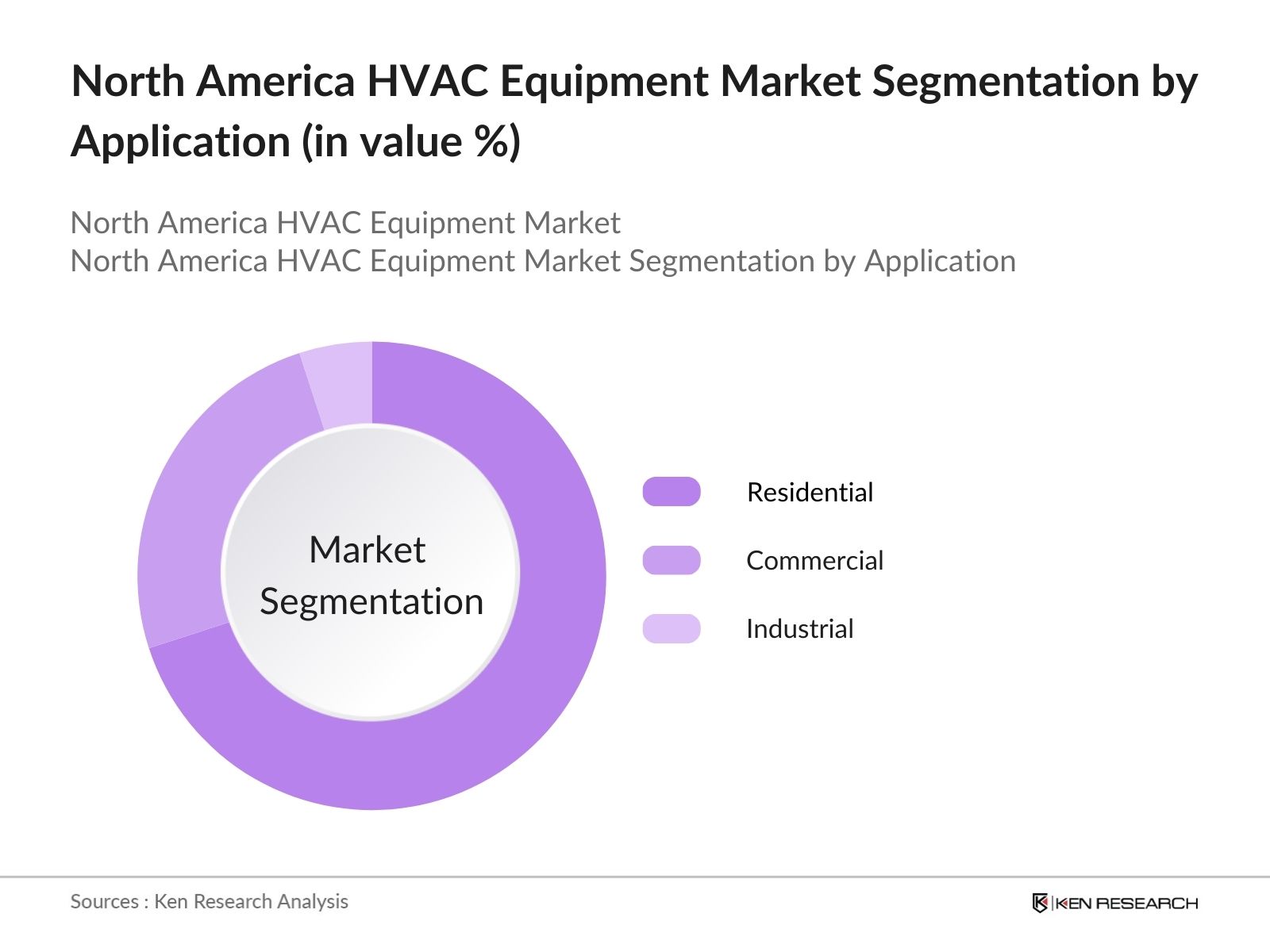

North America HVAC Equipment Market Segmentation

The North America HVAC market is segmented by equipment type and by application.

- By Equipment Type: The market is segmented by equipment type into heating, ventilation, and cooling systems. Among these, the heating segment holds the dominant market share in the region. This is largely due to the prevalence of colder climates in parts of the U.S. and Canada, which require reliable and efficient heating solutions. Gas furnaces and heat pumps have gained particular prominence due to their widespread adoption in residential buildings. Their energy efficiency, long lifespan, and ability to provide consistent heating throughout colder months make them the leading sub-segment within the HVAC market.

- By Application: The market is also segmented by application into residential, commercial, and industrial sectors. The residential sector holds the largest market share in this region, driven by high demand for smart and energy-efficient HVAC systems in homes. Increased awareness about indoor air quality and the adoption of smart home technologies are accelerating the installation of advanced HVAC systems in residential settings. Additionally, the growth in home renovations and new housing developments has further propelled this segment's dominance in the market.

North America HVAC Equipment Market Competitive Landscape

The North America HVAC equipment market is characterized by a consolidation of major global players and several domestic manufacturers. Companies in this market focus heavily on technological advancements, especially in smart HVAC systems that integrate IoT and AI for energy efficiency. The competitive landscape is dominated by established brands that have a long-standing market presence and strong distribution channels.

The North American HVAC market is dominated by companies like Carrier, Daikin, and Johnson Controls, which focus on innovation and sustainability. These companies lead the market due to their significant investments in R&D, which has allowed them to offer state-of-the-art solutions that meet growing energy efficiency and environmental compliance demands.

North America HVAC Equipment Market Analysis

Growth Drivers

- Increased Demand for Energy-Efficient Systems: The rising demand for energy-efficient HVAC systems in North America is driven by the need to reduce electricity consumption in both residential and commercial sectors. According to the U.S. Energy Information Administration (EIA), energy consumption by HVAC systems accounts for nearly 40% of total building energy use in the U.S. As of 2024, with increased urbanization, there has been a push towards more energy-efficient heating and cooling systems, especially as newer technologies like heat pumps and inverter-driven compressors reduce energy usage by 20-30%. Government incentives under the U.S. Department of Energy (DOE) continue to encourage the adoption of high-efficiency systems, making it a significant driver.

- Growing Adoption of Smart HVAC Technologies: Smart HVAC technologies are gaining traction due to their ability to provide greater energy savings, convenience, and system control. The integration of IoT-enabled thermostats, sensors, and machine learning in HVAC systems has been shown to reduce energy consumption by up to 10-15% compared to traditional systems. In 2024, this trend is further bolstered by the proliferation of smart building infrastructure across major urban centers in the U.S. and Canada. Moreover, state-level incentives to promote smart building technologies play a crucial role in adoption rates, with energy-saving mandates set by the DOE and EPA encouraging the shift towards smarter solutions.

- Increased Urbanization and Infrastructure Expansion: Urbanization in North America has led to significant investments in infrastructure, pushing demand for HVAC equipment in both commercial and residential sectors. According to the U.S. Census Bureau, urban population growth in the U.S. has risen by nearly 2.5 million between 2022 and 2024, prompting large-scale construction projects requiring advanced HVAC systems. Additionally, infrastructure developments such as office buildings, hospitals, and data centerseach necessitating efficient HVAC systemsare contributing to increased demand. This urbanization trend is particularly strong in states like Texas and Florida, where government-supported infrastructure projects are surging.

Market Challenges

- High Initial Setup and Installation Costs: One of the primary barriers to adopting energy-efficient and smart HVAC systems in North America is the high initial setup and installation cost. Data from the U.S. DOE indicate that installing a new energy-efficient HVAC system can cost up to $12,000 for residential buildings and even higher for commercial setups. While these costs can be offset by long-term savings on energy bills, the upfront financial burden poses a challenge, particularly for smaller businesses or homeowners with limited capital. This is further compounded by labor shortages in skilled trades, which elevate installation expenses.

- Energy Consumption Concerns in Older Systems: Older HVAC systems, particularly those over a decade old, are significantly less efficient than newer models. Data from the Environmental Protection Agency (EPA) indicates that older HVAC systems consume up to 30% more energy than energy-efficient models installed post-2020. In the U.S., buildings account for 76% of electricity use, and HVAC systems make up a considerable portion of this. With the aging HVAC infrastructure in many North American cities, energy consumption remains a pressing concern. This problem is exacerbated by the high operational costs associated with these older systems, especially in densely populated urban areas

North America HVAC Equipment Market Future Outlook

Over the next five years, the North American HVAC Equipment market is expected to experience robust growth driven by continued demand for energy-efficient systems, integration of smart technologies, and increasing government initiatives aimed at reducing carbon footprints. The rising adoption of smart home automation and AI-based energy solutions is likely to propel the market further. Increasing urbanization, coupled with a rise in infrastructure development, will continue to be key growth drivers in the HVAC industry. The market is also expected to benefit from innovations in sustainable HVAC technologies and eco-friendly refrigerants.

Market Opportunities

- Technological Advancements in HVAC Systems (IoT, AI Integration): The rapid adoption of Internet of Things (IoT) technology and artificial intelligence (AI) in HVAC systems presents a significant opportunity for market growth. In 2024, IoT-enabled HVAC systems, which allow for remote monitoring, predictive maintenance, and real-time energy usage optimization, have been deployed in over 12 million homes and commercial buildings across the U.S. AI algorithms also enable smarter HVAC control systems that can adapt to occupant behavior and weather conditions, potentially reducing energy consumption by up to 40% in some cases. This advancement aligns with the broader movement toward smart cities and smart homes across North America.

- Growth in Sustainable and Green Building Initiatives: Sustainable building practices have gained momentum across North America, providing a boost for energy-efficient HVAC solutions. According to the U.S. Green Building Council, LEED-certified buildings, which require the use of sustainable HVAC systems, have increased by 14% from 2022 to 2024. The emphasis on reducing carbon footprints, particularly in urban areas such as New York and San Francisco, has led to an uptick in demand for sustainable HVAC systems. This presents an opportunity for manufacturers and installers to capitalize on green building mandates as both commercial and residential sectors seek eco-friendly solutions.

Scope of the Report

|

Heating (Furnaces, Heat Pumps, Boilers) |

|

|

By Application |

Residential Commercial Industrial Institutional |

|

By Technology |

Smart HVAC Systems Traditional HVAC Systems Hybrid HVAC Systems |

|

By Distribution Channel |

Direct Sales Indirect Sales (Distributors, Retailers) |

|

By Region |

US Canada Mexico |

Products

Key Target Audience

HVAC Equipment Manufacturers

Real Estate Developers and Construction Companies

Energy Management Companies

Government and Regulatory Bodies (EPA, DOE)

Smart Home Automation Companies

Banks and Financial Institutes

Utility Service Providers

Investors and Venture Capitalist Firms

Retailers and Distributors of HVAC Systems

Companies

Major Players in the North America HVAC Market

Carrier Global Corporation

Daikin Industries Ltd.

Johnson Controls International

Lennox International Inc.

Trane Technologies Plc

Rheem Manufacturing Company

Mitsubishi Electric Corporation

York International Corporation

Nortek Global HVAC LLC

Goodman Manufacturing

Bosch Thermotechnology Corp.

Samsung HVAC

Gree Electric Appliances

Fujitsu General

Hitachi Cooling & Heating

Table of Contents

1. North America HVAC Equipment Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America HVAC Equipment Market Size (in USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America HVAC Equipment Market Analysis

3.1. Growth Drivers (Energy Efficiency, Smart Building Solutions, Replacement Demand)

3.1.1. Increased Demand for Energy-Efficient Systems

3.1.2. Growing Adoption of Smart HVAC Technologies

3.1.3. Increased Urbanization and Infrastructure Expansion

3.1.4. Replacement Demand for Old Systems

3.2. Market Challenges (High Installation Costs, Energy Consumption, Maintenance Complexity)

3.2.1. High Initial Setup and Installation Costs

3.2.2. Energy Consumption Concerns in Older Systems

3.2.3. Complex Maintenance and System Integration

3.3. Opportunities (Technological Advancements, Sustainable HVAC, Government Initiatives)

3.3.1. Technological Advancements in HVAC Systems (IoT, AI Integration)

3.3.2. Growth in Sustainable and Green Building Initiatives

3.3.3. Government Incentives for Energy-Efficient Equipment

3.4. Trends (Smart Homes, Decarbonization, AI-Driven HVAC Solutions)

3.4.1. Increased Demand for Smart Home HVAC Systems

3.4.2. Focus on Decarbonization of Heating and Cooling Solutions

3.4.3. AI-Driven HVAC Solutions for Optimized Efficiency

3.5. Government Regulations (Energy Standards, Environmental Policies)

3.5.1. U.S. Environmental Protection Agency (EPA) Regulations

3.5.2. Department of Energy (DOE) Efficiency Standards

3.5.3. LEED Certifications and Compliance

3.5.4. State-Level Building Energy Codes

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis (Bargaining Power of Buyers, Suppliers, Threat of Substitutes)

3.9. Competitive Landscape and Ecosystem

4. North America HVAC Equipment Market Segmentation

4.1. By Equipment Type (in Value %)

4.1.1. Heating (Furnaces, Heat Pumps, Boilers)

4.1.2. Ventilation (Air Purifiers, Exhaust Fans, Air Handlers)

4.1.3. Cooling (Air Conditioners, Chillers, Cooling Towers)

4.1.4. Other HVAC Systems

4.2. By Application (in Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Industrial

4.2.4. Institutional

4.3. By Technology (in Value %)

4.3.1. Smart HVAC Systems

4.3.2. Traditional HVAC Systems

4.3.3. Hybrid HVAC Systems

4.4. By Distribution Channel (in Value %)

4.4.1. Direct Sales

4.4.2. Indirect Sales (Distributors, Retailers)

4.5. By Region (in Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America HVAC Equipment Market Competitive Analysis

5.1. Detailed Profiles of Major Companies (No. of Employees, Headquarters, Revenue)

5.1.1. Carrier Global Corporation

5.1.2. Daikin Industries Ltd.

5.1.3. Johnson Controls International

5.1.4. Lennox International Inc.

5.1.5. Trane Technologies Plc

5.1.6. Rheem Manufacturing Company

5.1.7. Mitsubishi Electric Corporation

5.1.8. Ingersoll Rand

5.1.9. York International Corporation

5.1.10. Nortek Global HVAC LLC

5.1.11. Goodman Manufacturing

5.1.12. Bosch Thermotechnology Corp.

5.1.13. Samsung HVAC

5.1.14. Gree Electric Appliances

5.1.15. Fujitsu General

5.2. Cross Comparison Parameters (Annual Revenue, Market Share, Product Portfolio, Technology Focus, Environmental Compliance, Distribution Network, R&D Investments, Customer Base)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Funding and Grants

5.8. Private Equity and Venture Capital Investments

6. North America HVAC Equipment Market Regulatory Framework

6.1. U.S. Federal Energy Efficiency Standards

6.2. Energy Star Certification Programs

6.3. Regional HVAC Standards and Guidelines

6.4. Compliance with Environmental Standards (EPA, DOE)

7. North America HVAC Equipment Future Market Size (in USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America HVAC Equipment Future Market Segmentation

8.1. By Equipment Type (in Value %)

8.2. By Application (in Value %)

8.3. By Technology (in Value %)

8.4. By Distribution Channel (in Value %)

8.5. By Region (in Value %)

9. North America HVAC Equipment Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing and Go-To-Market Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map for the North America HVAC market. This includes identifying the major stakeholders such as manufacturers, distributors, and customers. Secondary research is conducted through government publications and proprietary databases to identify key variables such as energy efficiency trends, regulatory impacts, and technological innovations.

Step 2: Market Analysis and Construction

In this phase, historical data is compiled to assess the penetration of HVAC systems, including the balance between residential and commercial installations. The analysis further evaluates the impact of smart technology integration and sustainability measures. Revenue estimates are drawn based on the collected market data and trends.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are formulated and validated via CATIs with industry experts, including HVAC equipment manufacturers and smart home technology providers. These consultations provide real-time insights into the operational strategies of key players, including their R&D investments, technological focus, and market expansion plans.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing the insights from manufacturers, industry experts, and market data to produce a comprehensive, validated analysis of the North America HVAC Equipment market. The final output includes detailed market forecasts, trends analysis, and recommendations based on both qualitative and quantitative inputs.

Frequently Asked Questions

01. How big is the North America HVAC Equipment Market?

The North America HVAC Equipment Market is valued at USD 32.2 billion, driven by growing infrastructure projects, the adoption of energy-efficient systems, and smart home technologies.

02. What are the challenges in the North America HVAC Equipment Market?

Challenges in North America HVAC Equipment Market include high installation costs, regulatory compliance related to energy efficiency standards, and the need for skilled technicians to manage complex systems.

03. Who are the major players in the North America HVAC Equipment Market?

Key players in the North America HVAC Equipment Market include Carrier Global Corporation, Daikin Industries Ltd., Johnson Controls International, Lennox International Inc., and Trane Technologies Plc, all of which lead the market due to their technological advancements and energy-efficient product lines.

04. What are the growth drivers of the North America HVAC Equipment Market?

The North America HVAC Equipment Market is driven by factors such as increased demand for energy-efficient systems, government incentives for sustainable solutions, and advancements in smart HVAC technology

05. Which sub-segments dominate the North America HVAC market?

The heating segment, particularly gas furnaces and heat pumps, dominates due to high demand in colder climates and advancements in energy efficiency.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.