North America Hydrogen Market Outlook to 2030

Region:North America

Author(s):Shreya Garg

Product Code:KROD7702

December 2024

96

About the Report

North America Hydrogen Market Overview

- The North America Hydrogen Market, valued at USD 9 billion, is bolstered by a combination of public and private sector investments, emphasizing clean energy alternatives. The regions significant investment in hydrogen production facilities and infrastructure supports this growth, with substantial government incentives promoting hydrogen as a sustainable energy source. This growth is particularly accelerated by advancements in hydrogen fuel cell technology and applications across industries, from transportation to power generation.

- In North America, the United States, particularly states like California and Texas, leads the hydrogen market due to its extensive renewable energy infrastructure and proactive energy policies supporting hydrogen. Californias hydrogen refueling network and Texass industrial hydrogen production capabilities position these states as central hubs, creating a conducive environment for industry expansion. Canada also plays a vital role, driven by government initiatives and extensive natural gas resources, facilitating hydrogen production via natural gas reforming.

- Emissions mandates across North America are driving hydrogen adoption, with the U.S. setting a goal to achieve net-zero emissions by 2050. Under the Clean Air Act, the Environmental Protection Agency (EPA) has introduced stricter emissions standards, which hydrogen projects help address by offsetting industrial emissions. Canadas Clean Fuel Standard also mandates lower emissions, encouraging industries to shift to hydrogen as an alternative fuel. These regulatory frameworks promote hydrogen as part of national decarbonization strategies, directly influencing its role in emission reduction

North America Hydrogen Market Segmentation

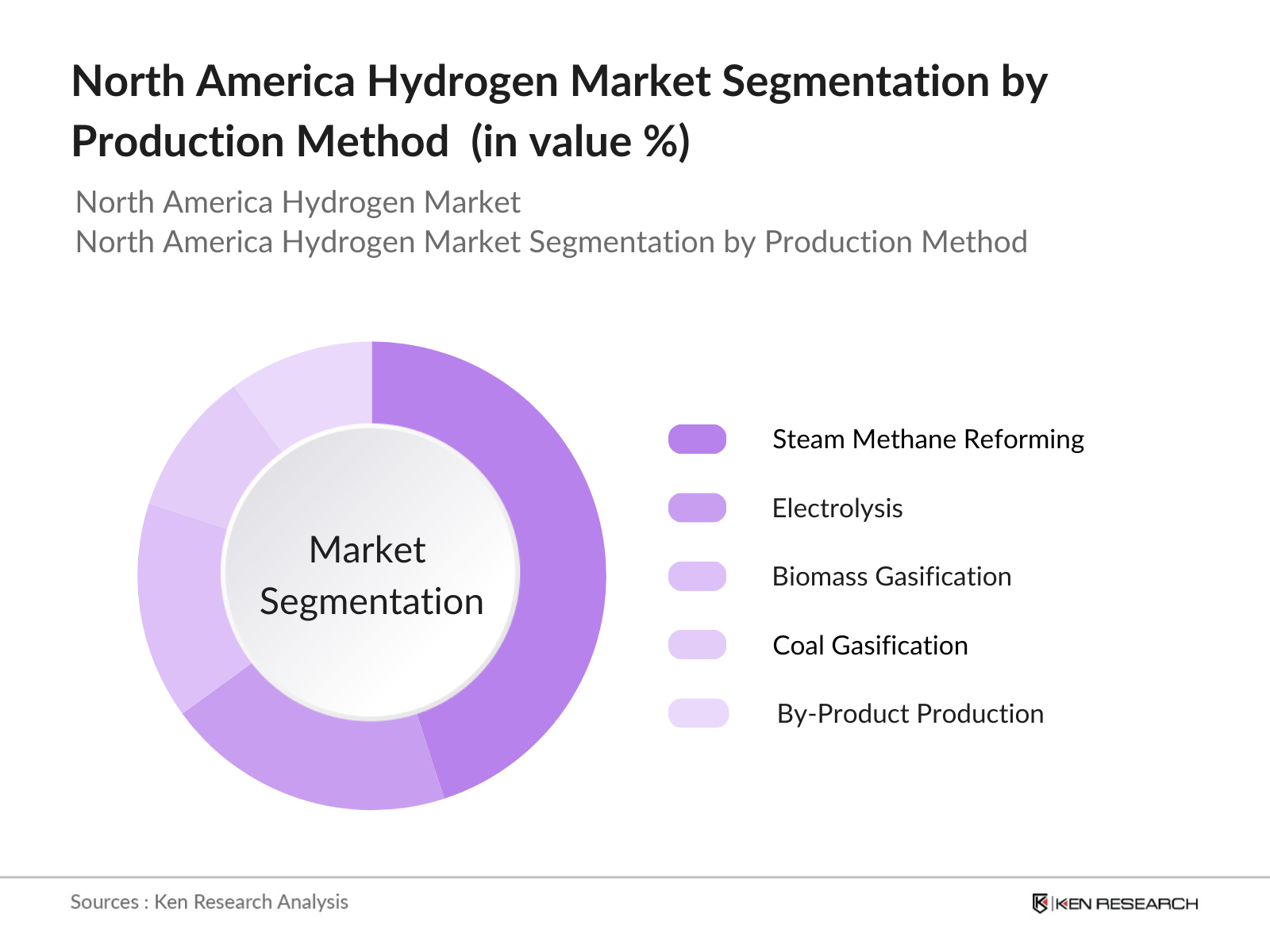

By Production Method: The Market is segmented by production method into Steam Methane Reforming, Electrolysis, Biomass Gasification, Coal Gasification, and By-Product Production. Among these, Steam Methane Reforming holds a dominant market share, primarily due to its economic viability and established infrastructure. The extensive natural gas reserves in North America make this method a cost-effective option, despite carbon emissions being a concern. Companies in the U.S. are progressively integrating carbon capture technologies with Steam Methane Reforming, reducing emissions while maintaining cost efficiency.

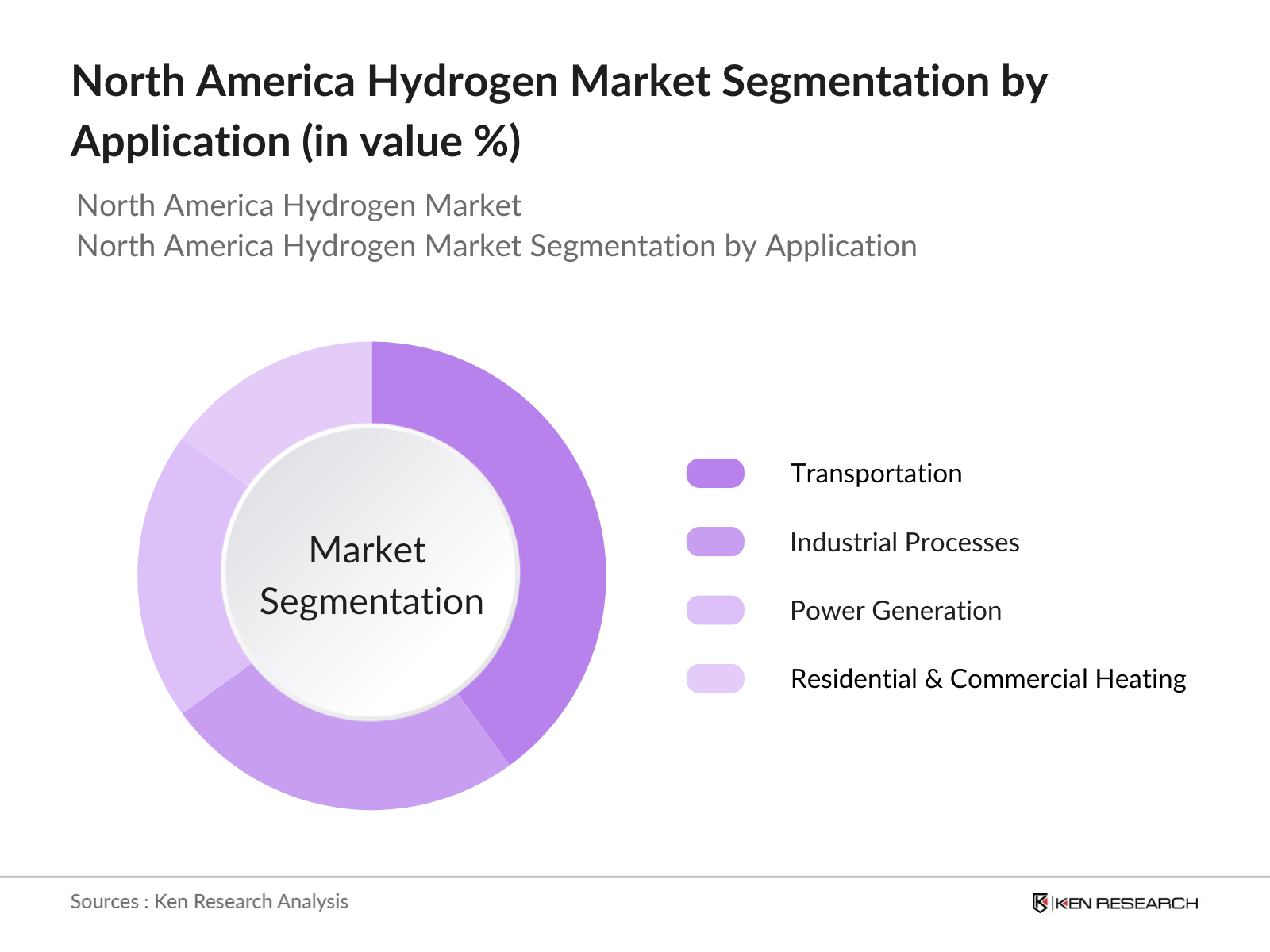

By Application: The Market is also segmented by application into Transportation, Industrial Processes, Power Generation, and Residential and Commercial Heating. The Transportation sector dominates, driven by growing investments in hydrogen fuel cell vehicles and the need for eco-friendly transportation solutions. Hydrogens high energy density and quick refueling time make it a competitive option in sectors like long-haul transportation. Prominent states like California are actively investing in hydrogen refueling stations to support this sector's growth.

North America Hydrogen Market Competitive Landscape

The North America Hydrogen Market is characterized by the presence of established energy companies and innovative players driving new hydrogen applications. Companies like Air Products & Chemicals and Linde dominate the market, leveraging extensive production facilities and partnerships across sectors. This competitive landscape is shaped by technological advancements, strategic partnerships, and focused investments in sustainable hydrogen production methods.

|

Company |

Year of Establishment |

Headquarters |

Production Capacity |

Key Partnerships |

R&D Investment |

Distribution Network |

Market Presence |

Carbon Emission Targets |

|

Air Products & Chemicals |

1940 |

Allentown, PA, USA |

||||||

|

Linde PLC |

1879 |

Dublin, Ireland |

||||||

|

Mitsubishi Power Americas |

2001 |

Lake Mary, FL, USA |

||||||

|

Plug Power Inc. |

1997 |

Latham, NY, USA |

||||||

|

Ballard Power Systems |

1979 |

Burnaby, Canada |

North America Hydrogen Industry Analysis

Growth Drivers

- Government Incentives and Subsidies: In the North America hydrogen market, government incentives and subsidies play a pivotal role in driving hydrogen adoption. The U.S. Department of Energy (DOE) allocated $9.5 billion under the Infrastructure Investment and Jobs Act to accelerate hydrogen projects across states, targeting transportation and heavy industries. Additionally, California, a leading state in hydrogen infrastructure, allocated $300 million for hydrogen fueling stations in 2023, supporting expansion across major routes. This funding has catalyzed projects aimed at establishing a hydrogen economy, with states like Texas and Louisiana also receiving funding for hydrogen hubs to bolster hydrogen production initiatives.

- Transition to Clean Energy: North Americas shift to clean energy aligns with hydrogens role as a low-emission alternative, especially in hard-to-abate sectors like transportation and heavy industry. The DOE has set an ambitious target to reduce greenhouse gas emissions by 50-52% by 2030, with hydrogen serving as a critical contributor. In Canada, hydrogen adoption is promoted under the Clean Fuel Standard, which supports investment in low-carbon fuel alternatives. These clean energy targets are pushing states to include hydrogen in their renewable energy portfolio, aiming to integrate 1 million hydrogen-powered vehicles by 2030.

- Technological Advancements in Hydrogen Production: Technological innovations, particularly in electrolyzer efficiency, are enhancing the hydrogen production landscape. In 2023, the National Renewable Energy Laboratory (NREL) reported a 20% efficiency increase in PEM electrolyzers, making green hydrogen production more viable. Furthermore, advancements in solid oxide electrolyzers have allowed for dual-use in renewable and grid-connected environments, fostering lower emissions. The U.S. Advanced Research Projects Agency-Energy (ARPA-E) has committed over $150 million to accelerate these technological improvements, potentially reducing production constraints and fostering greater scalability.

Market Challenges

- High Production Costs: The high production costs of hydrogen, especially green hydrogen, remain a challenge. As of 2024, green hydrogen production costs in North America range between $4 and $6 per kilogram, significantly higher than fossil-fuel-based hydrogen production costs. This cost disparity is a barrier for industries and consumers adopting hydrogen as an energy source. The DOE's Hydrogen Shot Initiative is actively seeking to reduce production costs by 80% to make hydrogen more competitive, targeting $1 per kilogram. However, achieving this target remains challenging, with cost reductions dependent on technological breakthroughs.

- Limited Hydrogen Refueling Infrastructure: Despite infrastructure investments, hydrogen refueling stations remain limited in the U.S. and Canada, with only 1 hydrogen station per 100,000 square miles on average outside California. The lack of refueling stations restricts the widespread adoption of hydrogen-powered vehicles, especially in regions with limited infrastructure. For instance, the northeastern U.S. and southern Canada have fewer than 10 public refueling stations combined, creating gaps in accessibility. This limited infrastructure coverage highlights the need for further investment and cross-state collaboration to create a cohesive refueling network.

North America Hydrogen Market Future Outlook

Over the next several years, the North America Hydrogen Market is poised to witness robust growth as the focus on green hydrogen production and carbon emission reduction intensifies. Supportive regulatory frameworks, coupled with increased investments from both government and private sectors, are expected to drive the development of hydrogen infrastructure. The markets growth trajectory will also be influenced by technological advancements in hydrogen storage and transportation, enhancing its applicability across sectors.

Future Market Opportunities

- Investment in Hydrogen Fuel Cells: Hydrogen fuel cell investments are accelerating, particularly in the transportation sector, with over 10,000 fuel-cell-powered vehicles projected to be on U.S. roads by 2025. The DOE has allocated $20 million in 2023 towards fuel cell innovation, encouraging automotive companies to explore fuel cell technology in vehicles, trucks, and buses. In Canada, Ballard Power Systems leads in fuel cell manufacturing, enhancing North Americas positioning as a hydrogen technology innovator. This investment indicates a growing industry focus on hydrogen fuel cells to support clean energy targets.

- Potential for Export Markets: North Americas hydrogen production capacity positions it for export opportunities, particularly to regions with limited renewable resources. The U.S. and Canada are targeting partnerships with Japan and South Korea, where hydrogen imports are projected to play a key role in their clean energy strategies. Canadas Hydrogen Strategy aims to position the country as a global leader by 2025, planning export hubs near coastal provinces. The DOE forecasts a potential hydrogen export market worth $12 billion by leveraging North Americas renewable resources for clean hydrogen production.

Scope of the Report

|

Production Method |

Steam Methane Reforming ElectrolysisBiomass Gasification Coal Gasification By-Product Production |

|

Application |

Transportation Industrial Processes Power Generation Residential and Commercial Heating |

|

Distribution Channel |

Pipeline Compressed Gas Delivery Liquid Tanker Transport |

|

End-Use Industry |

Oil & Gas Chemicals Power & Energy Automotive |

|

Region |

United States Canada Mexico |

Products

Key Target Audience

Hydrogen Production Companies

Automotive Manufacturers

Renewable Energy Corporations

Industrial Gas Suppliers

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (U.S. Department of Energy, Natural Resources Canada)

Power Generation Firms

Transportation and Logistics Firms

Companies

Major Players

Air Products & Chemicals

Linde PLC

Mitsubishi Power Americas Inc.

Plug Power Inc.

Ballard Power Systems

Cummins Inc.

Air Liquide

Nel ASA

Engie

Chevron Corporation

Royal Dutch Shell PLC

ITM Power PLC

Bloom Energy

Siemens Energy

Toyota Motor Corporation

Table of Contents

North America Hydrogen Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate Analysis

1.4. Market Segmentation Overview

North America Hydrogen Market Size (in USD)

2.1. Historical Market Size Analysis

2.2. Key Market Developments

2.3. Regulatory Milestones

North America Hydrogen Market Analysis

3.1. Growth Drivers

3.1.1. Government Incentives and Subsidies

3.1.2. Transition to Clean Energy

3.1.3. Technological Advancements in Hydrogen Production

3.1.4. Expansion of Hydrogen Infrastructure

3.2. Market Challenges

3.2.1. High Production Costs

3.2.2. Limited Hydrogen Refueling Infrastructure

3.2.3. Storage and Transportation Barriers

3.3. Opportunities

3.3.1. Investment in Hydrogen Fuel Cells

3.3.2. Potential for Export Markets

3.3.3. Partnerships with Automotive and Power Sectors

3.4. Trends

3.4.1. Increasing Adoption of Green Hydrogen

3.4.2. Use in Industrial Applications

3.4.3. Integration with Renewable Energy Sources

3.5. Government Regulation

3.5.1. Emissions Reduction Mandates

3.5.2. Tax Credits for Hydrogen Projects

3.5.3. Standards for Hydrogen Production and Distribution

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Hydrogen Market Value Chain

North America Hydrogen Market Segmentation

4.1. By Production Method (in Value %)

4.1.1. Steam Methane Reforming

4.1.2. Electrolysis

4.1.3. Biomass Gasification

4.1.4. Coal Gasification

4.1.5. By-Product Production

4.2. By Application (in Value %)

4.2.1. Transportation

4.2.2. Industrial Processes

4.2.3. Power Generation

4.2.4. Residential and Commercial Heating

4.3. By Distribution Channel (in Value %)

4.3.1. Pipeline

4.3.2. Compressed Gas Delivery

4.3.3. Liquid Tanker Transport

4.4. By End-Use Industry (in Value %)

4.4.1. Oil & Gas

4.4.2. Chemicals

4.4.3. Power & Energy

4.4.4. Automotive

4.5. By Region (in Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

North America Hydrogen Market Competitive Landscape

5.1. Detailed Profiles of Major Companies

5.1.1. Air Products & Chemicals Inc.

5.1.2. Linde PLC

5.1.3. Mitsubishi Power Americas Inc.

5.1.4. Plug Power Inc.

5.1.5. Ballard Power Systems

5.1.6. Cummins Inc.

5.1.7. Air Liquide

5.1.8. Nel ASA

5.1.9. Engie

5.1.10. Chevron Corporation

5.1.11. Royal Dutch Shell PLC

5.1.12. ITM Power PLC

5.1.13. Bloom Energy

5.1.14. Siemens Energy

5.1.15. Toyota Motor Corporation

5.2. Cross-Comparison Parameters (Market Share, Revenue, Hydrogen Production Capacity, R&D Expenditure, Workforce Size, Regional Presence, Partnerships, Carbon Emission Reduction Targets)

5.3. Market Share Analysis by Competitor

5.4. Strategic Partnerships and Alliances

5.5. Mergers and Acquisitions

5.6. Joint Ventures in Hydrogen Technology

5.7. Recent Developments in Hydrogen Technologies

North America Hydrogen Market Regulatory Framework

6.1. Emission Standards for Hydrogen Production

6.2. Compliance with Environmental Standards

6.3. Certification Requirements for Hydrogen Fuel Cells

6.4. Incentives for Low-Carbon Hydrogen Production

North America Hydrogen Future Market Analysis

7.1. Growth Projections

7.2. Key Drivers Shaping Future Growth

North America Hydrogen Future Market Segmentation

8.1. By Production Method

8.2. By Application

8.3. By Distribution Channel

8.4. By End-Use Industry

8.5. By Region

North America Hydrogen Market Analysts Recommendations

9.1. Total Addressable Market (TAM) Analysis

9.2. Strategic Recommendations for Industry Stakeholders

9.3. Market Entry Strategies for New Players

9.4. Risk Mitigation Strategies

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial stage involves constructing a detailed overview of the North America Hydrogen Market by identifying key factors that influence hydrogen production, application, and distribution. This includes conducting in-depth desk research to capture both industry and regulatory trends.

Step 2: Market Analysis and Construction

This phase focuses on analyzing historical data to assess the markets growth trajectory. Various production methods, market applications, and associated financial metrics are examined, providing a granular view of market composition and performance.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses about the North America Hydrogen Markets future developments are validated through consultations with industry experts. These consultations offer valuable insights into operational and financial trends, supporting accurate market estimates.

Step 4: Research Synthesis and Final Output

In the final phase, comprehensive data synthesis and validation are conducted. This stage includes cross-verifying statistics through consultations with hydrogen market operators, ensuring an exhaustive and precise assessment of the North America Hydrogen Market.

Frequently Asked Questions

01. How big is the North America Hydrogen Market?

The North America Hydrogen Market, valued at USD 9 billion, is driven by a combination of government support, technological advancements, and growing applications across sectors like transportation and industrial processes.

02. What are the major challenges in the North America Hydrogen Market?

Challenges in the North America Hydrogen Market include high production costs, limited hydrogen refueling infrastructure, and complexities in hydrogen storage and transportation, which hinder wider adoption across sectors.

03. Who are the key players in the North America Hydrogen Market?

Major players in the North America Hydrogen Market include Air Products & Chemicals, Linde PLC, Mitsubishi Power Americas, Plug Power Inc., and Ballard Power Systems, leading the market with innovations in hydrogen production and application.

04. What drives the growth of the North America Hydrogen Market?

The North America Hydrogen Market is propelled by government incentives, a strong push for clean energy solutions, and the demand for sustainable energy alternatives, especially in transportation and industrial sectors.

05. How is hydrogen produced in the North America Hydrogen Market?

Hydrogen in North America is produced mainly through methods like Steam Methane Reforming, Electrolysis, and Biomass Gasification, each with varying environmental impacts and cost implications.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.