North America Image Generator Market Outlook to 2030

Region:North America

Author(s):Yogita Sahu

Product Code:KROD6283

November 2024

80

About the Report

North America Image Generator Market Overview

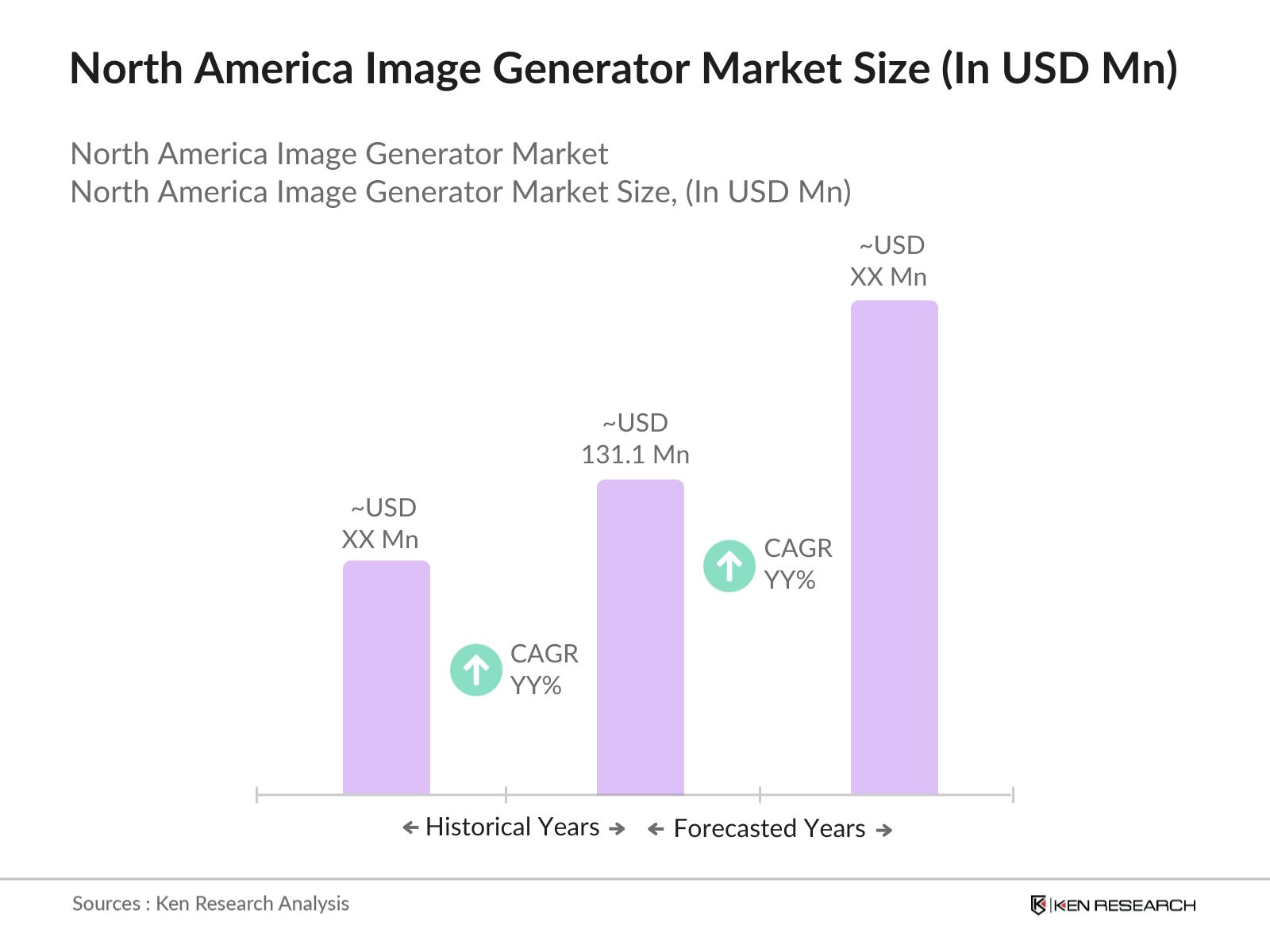

- The North America Image Generator market, valued at USD 131.1 million, is growing rapidly due to the increasing adoption of AI-based tools in content creation, digital marketing, and social media. The demand for image generation tools is primarily driven by the expanding need for creative digital content in industries like advertising, e-commerce, and gaming.

- In terms of geographic dominance, the United States and Canada lead the market. The U.S. dominates due to its advanced tech infrastructure, concentration of AI research centers, and the presence of major players like OpenAI, Adobe, and NVIDIA. Canada, with its AI-friendly government policies and growing AI startup ecosystem, is also emerging as a key market.

- In 2024, the US implemented tax breaks and incentives for companies investing in digital technologies such as AI-based image generation tools. The federal government has allocated 1 billion USD in tax relief for businesses implementing innovative technologies, aiming to reduce the financial burden on enterprises and promote the adoption of cutting-edge solutions.

North America Image Generator Market Segmentation

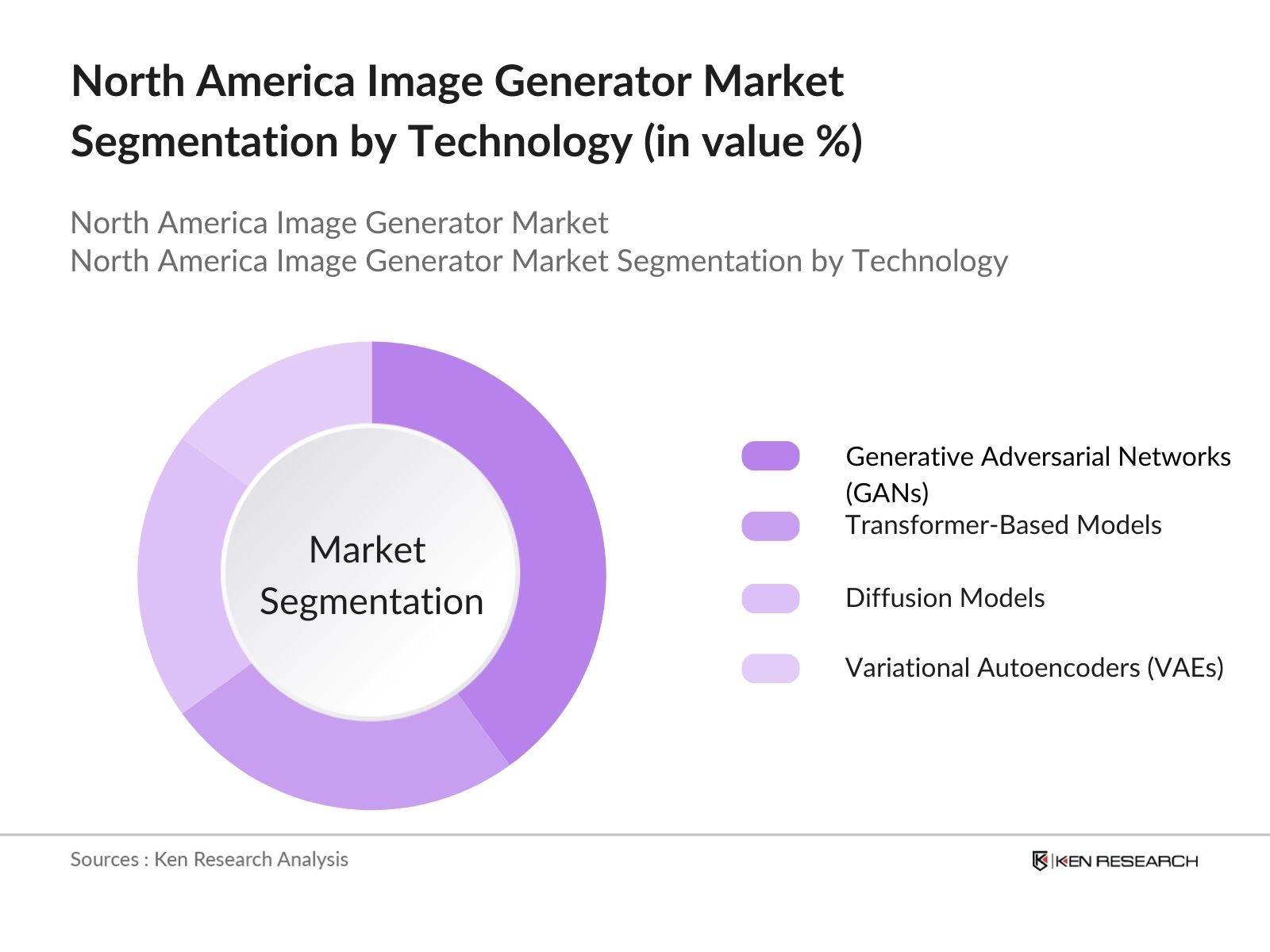

By Technology: The market is segmented by technology into Generative Adversarial Networks (GANs), Transformer-Based Models, Diffusion Models, and Variational Autoencoders (VAEs). Generative Adversarial Networks (GANs) have a dominant market share, owing to their capability of generating high-quality, realistic images. GANs are widely used in industries such as gaming, film production, and digital marketing.

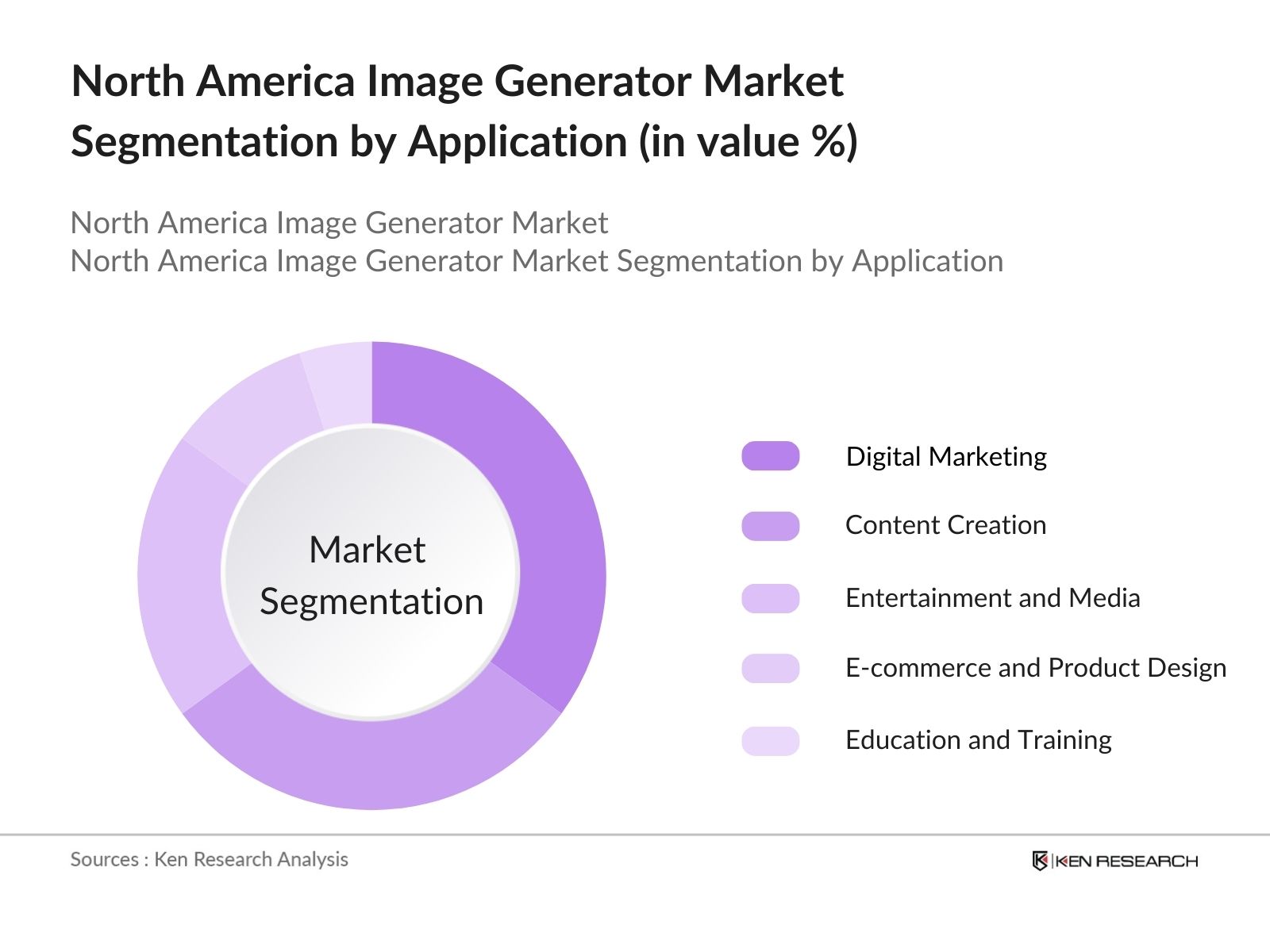

By Application: The market is also segmented by application into Digital Marketing, Content Creation, Entertainment and Media, E-commerce and Product Design, and Education and Training. Digital Marketing holds the largest market share, driven by the growing need for personalized and engaging content. AI image generators allow marketers to create unique visuals that enhance online campaigns and social media outreach.

North America Image Generator Market Competitive Landscape

The market is characterized by a competitive landscape dominated by a mix of established tech giants and innovative AI startups. Companies are focusing on integrating new AI models, expanding product portfolios, and enhancing user experience to gain a competitive edge.

|

Company Name |

Year of Establishment |

Headquarters |

Key AI Model |

R&D Investment |

Revenue (2023) |

No. of Employees |

Market Share |

Recent Acquisition |

Strategic Partnerships |

|

Adobe Inc. |

1982 |

San Jose, USA |

|||||||

|

NVIDIA Corporation |

1993 |

Santa Clara, USA |

|||||||

|

OpenAI |

2015 |

San Francisco, USA |

|||||||

|

Stability AI |

2020 |

London, UK |

|||||||

|

MidJourney |

2022 |

San Francisco, USA |

North America Image Generator Market Analysis

Market Growth Drivers

- Increased Adoption of AI and Machine Learning Tools: The integration of artificial intelligence (AI) and machine learning (ML) in image generators is rapidly transforming industries such as advertising, entertainment, and e-commerce. According to a 2024 industry report, the adoption of AI-driven image generation tools has surged by around 2.5 million units over the past two years in the US alone, due to their ability to produce hyper-realistic and customizable content at scale, which is driving demand across creative sectors.

- Expansion of Digital Content and Media Production: North America has witnessed an exponential rise in the creation of digital content, particularly in film, gaming, and advertising. By 2024, the North American media production industry is expected to generate nearly 5 billion digital assets annually, many of which rely on advanced image generation tools for design and animation. This substantial volume of content is pushing organizations to invest in automated solutions that enhance production efficiency while reducing manual labor.

- Growth of the E-Commerce Sector: In 2024, the North American e-commerce sector generated over 15 billion visual advertisements, relying heavily on automated image generation tools. As online retailers strive to enhance user experience with dynamic and engaging visual content, they are adopting these technologies at a faster rate. The shift towards hyper-targeted ads, product visualizations, and virtual try-on features is driving the adoption of high-quality image generation platforms within e-commerce giants and smaller retail businesses alike.

Market Challenges

- Ethical and Copyright Concerns: In 2024, over 300,000 legal disputes were filed in North America related to the unauthorized use of AI-generated images, highlighting the challenge of managing intellectual property rights in the digital realm. The growing use of image generators without proper licensing or attribution is raising concerns over the ethical use of such technologies, leading to more stringent legal scrutiny and compliance requirements for companies using these tools.

- Data Privacy Regulations: The tightening of data privacy regulations in North America, including the enactment of new laws in states like California and Virginia in 2024, is presenting compliance challenges for companies using image generators that rely on user data for customization. These laws require companies to invest in more secure systems, costing the industry around 800 million annually to ensure compliance with these regulations.

North America Image Generator Market Future Outlook

Over the next five years, the North America Image Generator industry is expected to show growth, driven by the continued advancements in AI technology and its expanding applications across industries. The growing demand for personalized, AI-generated visuals in sectors like digital marketing, entertainment, and e-commerce will propel the market forward.

Future Market Opportunities

- Widespread Adoption of AI-Generated Content in Advertising: In the next five years, it is projected that the use of AI-generated visuals in advertising will grow to encompass over 80% of digital ad campaigns in North America. This shift will be driven by brands looking to increase engagement by leveraging AI-powered tools that can create hyper-personalized and dynamic content at a much faster rate than traditional design methods.

- Emergence of Regulatory Frameworks for AI-Generated Visuals: By 2029, governments in North America are expected to introduce more comprehensive regulations governing the use of AI-generated images in various industries. These regulations will likely address issues around intellectual property, data privacy, and ethical use, ensuring that the rapid growth in this sector is balanced with responsible usage and compliance.

Scope of the Report

|

By Technology |

Generative Adversarial Networks (GANs) Transformer-Based Models Diffusion Models Variational Autoencoders (VAEs) |

|

By Application |

Digital Marketing Content Creation Entertainment and Media E-commerce Education and Training |

|

By End-User Industry |

Advertising Agencies Social Media Platforms Retail and E-commerce Film and Animation Studios Independent Creators |

|

By Deployment Mode |

Cloud-Based On-Premises |

|

By Region |

United States Canada Mexico |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Banks and Financial Institution

Entertainment and Media Companies

Private Equity Firms

Government and Regulatory Bodies (Federal Trade Commission, Department of Commerce)

Investor and Venture Capitalist Firms

Cloud Service Providers

Companies

Players Mentioned in the Report:

Adobe Inc.

NVIDIA Corporation

OpenAI

Stability AI

MidJourney

Artbreeder

DeepArt.io

Runway ML

Canva

Prisma Labs

Wombo AI

DALLE by OpenAI

Jasper AI

Lensa AI

Pikazo

Table of Contents

1. North America Image Generator Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Image Generator Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Image Generator Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand for AI-Based Visual Content (Market Penetration Rate)

3.1.2. Advancements in Generative AI Technologies (R&D Investments)

3.1.3. Rising Use in Digital Marketing and E-Commerce (Adoption Rate by Industry)

3.1.4. Growth in Creative Tools Market (End-User Demand)

3.2. Market Challenges

3.2.1. High Development Costs for AI Models (Cost-Benefit Analysis)

3.2.2. Data Privacy and Copyright Concerns (Regulatory Impact)

3.2.3. Lack of Skilled Professionals in AI (Talent Availability)

3.2.4. Computational Power and Infrastructure Challenges (Cloud Infrastructure Usage)

3.3. Opportunities

3.3.1. Integration with Augmented Reality (AR) and Virtual Reality (VR) (Technological Integration)

3.3.2. Expansion into SMBs and Individual Creators Market (Market Expansion Potential)

3.3.3. Customization and Personalization Trends (Product Differentiation Opportunities)

3.4. Trends

3.4.1. Use of AI for Hyper-Realistic Visuals (Tech Advancement Impact)

3.4.2. Integration of AI Image Generators with Social Media Platforms (Platform-Specific Demand)

3.4.3. Subscription-Based Services for Generative AI Tools (Revenue Model Innovations)

3.5. Government Regulations

3.5.1. Copyright Laws Affecting AI-Generated Content (Intellectual Property Regulations)

3.5.2. Data Protection Policies for Training AI Models (Regulatory Compliance)

3.5.3. Ethical Guidelines for AI Use in Media and Creative Fields (Ethical Standards)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Developers, Creators, SaaS Providers, AI Platforms)

3.8. Porters Five Forces (Supplier Bargaining Power, Buyer Power, Competitive Rivalry)

3.9. Competition Ecosystem

4. North America Image Generator Market Segmentation

4.1. By Technology (In Value %)

4.1.1. Generative Adversarial Networks (GANs)

4.1.2. Transformer-Based Models

4.1.3. Diffusion Models

4.1.4. Variational Autoencoders (VAEs)

4.2. By Application (In Value %)

4.2.1. Digital Marketing

4.2.2. Content Creation

4.2.3. Entertainment and Media

4.2.4. E-commerce and Product Design

4.2.5. Education and Training

4.3. By End-User Industry (In Value %)

4.3.1. Advertising Agencies

4.3.2. Social Media Platforms

4.3.3. Retail and E-commerce

4.3.4. Film and Animation Studios

4.3.5. Independent Creators

4.4. By Deployment Mode (In Value %)

4.4.1. Cloud-Based

4.4.2. On-Premises

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Image Generator Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Adobe Inc.

5.1.2. NVIDIA Corporation

5.1.3. OpenAI

5.1.4. Stability AI

5.1.5. MidJourney

5.1.6. Artbreeder

5.1.7. DeepArt.io

5.1.8. Runway ML

5.1.9. Canva

5.1.10. Prisma Labs

5.1.11. Wombo AI

5.1.12. DALLE by OpenAI

5.1.13. Jasper AI

5.1.14. Lensa AI

5.1.15. Pikazo

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, AI Model Type, Product Portfolio, Strategic Partnerships, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Image Generator Market Regulatory Framework

6.1. Data Security Standards

6.2. AI Transparency and Accountability Laws

6.3. AI Content Certification Processes

7. North America Image Generator Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Image Generator Future Market Segmentation

8.1. By Technology (In Value %)

8.2. By Application (In Value %)

8.3. By End-User Industry (In Value %)

8.4. By Deployment Mode (In Value %)

8.5. By Region (In Value %)

9. North America Image Generator Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping the ecosystem of the North America Image Generator Market. Extensive desk research is conducted to gather data from secondary sources like industry reports and proprietary databases, defining key variables such as technological advancements, market demand, and revenue trends.

Step 2: Market Analysis and Construction

In this phase, historical data on market growth, penetration rates, and revenue generation is analyzed. The analysis also includes data on the competitive landscape, assessing the ratio of AI model types to their applications across industries.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses are developed and validated through interviews with industry experts. These consultations provide insights into market dynamics, revenue drivers, and future growth opportunities, helping refine the data for accuracy.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing all collected data to create a comprehensive report. Detailed insights from key industry players are incorporated to validate findings, ensuring the accuracy of market estimates.

Frequently Asked Questions

01. How big is the North America Image Generator Market?

The North America Image Generator Market is valued at USD 131.1 million, driven by the increasing adoption of AI-generated visual content across industries like digital marketing, entertainment, and e-commerce.

02. What are the challenges in the North America Image Generator Market?

Challenges in the North America Image Generator Market include high computational costs, concerns over data privacy and copyright issues, and the lack of skilled professionals in AI-related fields.

03. Who are the major players in the North America Image Generator Market?

Key players in the North America Image Generator Market include Adobe Inc., NVIDIA Corporation, OpenAI, Stability AI, and MidJourney. These companies are leading the market due to their advanced AI models and strong partnerships with tech giants.

04. What are the growth drivers of the North America Image Generator Market?

Growth drivers in the North America Image Generator Market include advancements in AI technology, increased demand for digital content creation, and the growing use of AI tools in advertising and social media platforms.

05. Which technology is dominating the North America Image Generator Market?

Generative Adversarial Networks (GANs) dominate the technology segment, as they offer superior capabilities in generating high-quality, realistic images, especially for digital marketing and entertainment applications.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.