North America Industrial Automation Market Outlook to 2030

Region:North America

Author(s):Mukul

Product Code:KROD3712

October 2024

92

About the Report

North America Industrial Automation

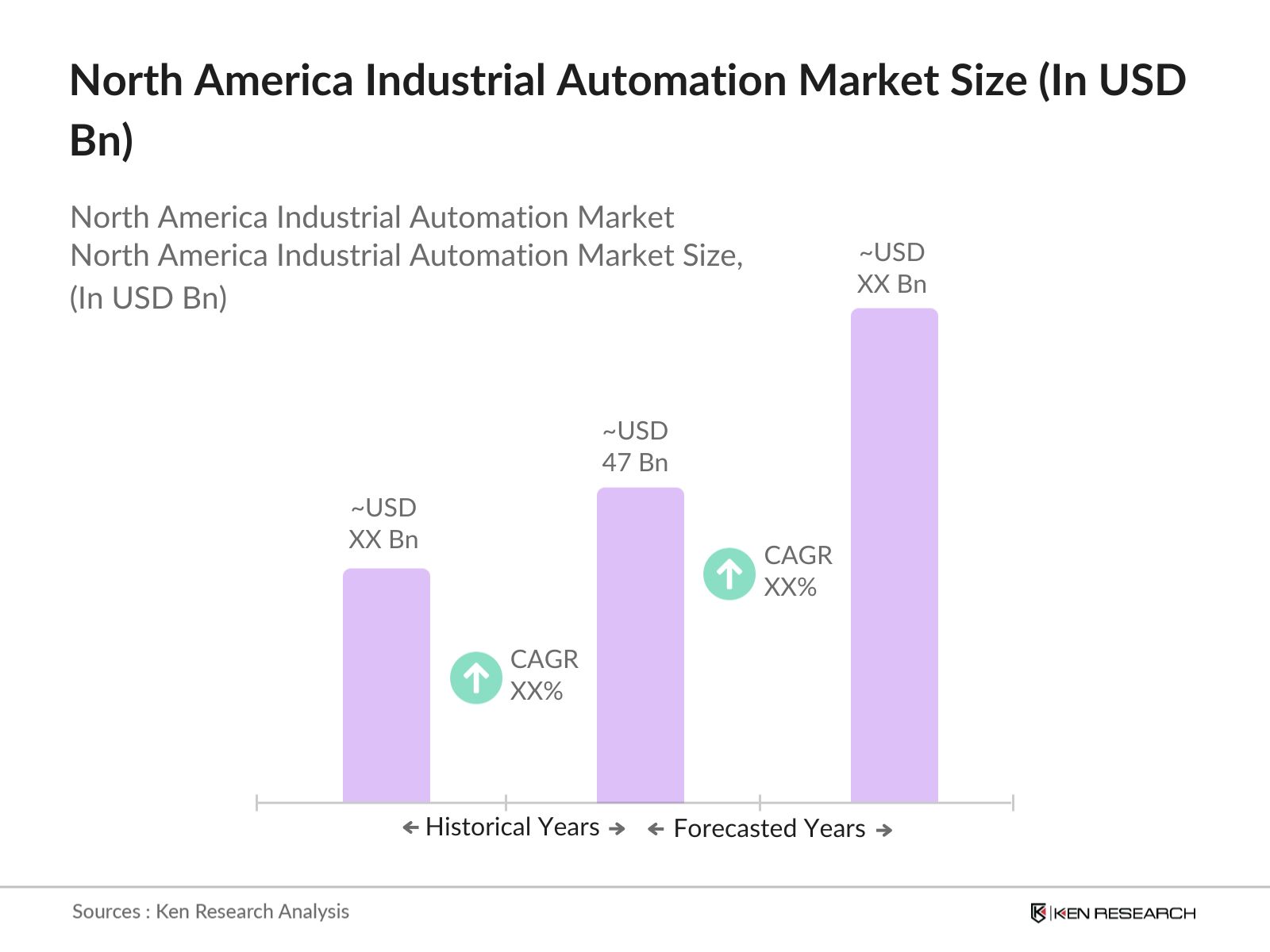

- The North America industrial automation market is a rapidly growing segment driven by increased adoption of Industry 4.0 technologies, such as robotics and advanced manufacturing solutions. The market size in 2023 is valued at USD 47 billion, attributed to the growing need for operational efficiency, real-time data monitoring, and rising demand for automated systems in industries like automotive, electronics, and healthcare. Key factors include government incentives for industrial automation and private sector investment in smart factories. Data from industry sources shows that this growth trajectory will continue with significant momentum in the upcoming years.

- The dominance of the United States in the North American industrial automation market is largely due to its well-established manufacturing base and early adoption of automation technologies. Key industrial hubs like Detroit and Silicon Valley are leading the charge in implementing advanced automation solutions, driven by the presence of major automotive and technology companies. Canada and Mexico also play significant roles, with Mexico acting as a manufacturing hub for North American industries. The geographic advantages and government policies promoting industrial innovation contribute to this dominance.

- The U.S. government provides significant financial support for automation technologies through tax credits and incentives. In 2024, the federal government earmarked $500 million for automation research grants and related tax incentives. The U.S. Department of Energy (DOE) also invested $60 million into smart manufacturing pilot projects, with the goal of reducing energy consumption by 15% across industries. The Smart Manufacturing Leadership Coalition, backed by a $200 million investment from the government, aims to boost efficiency and competitiveness by automating manufacturing processes, positioning North America as a leader in the industrial automation landscape.

North America Industrial Automation Market Segmentation

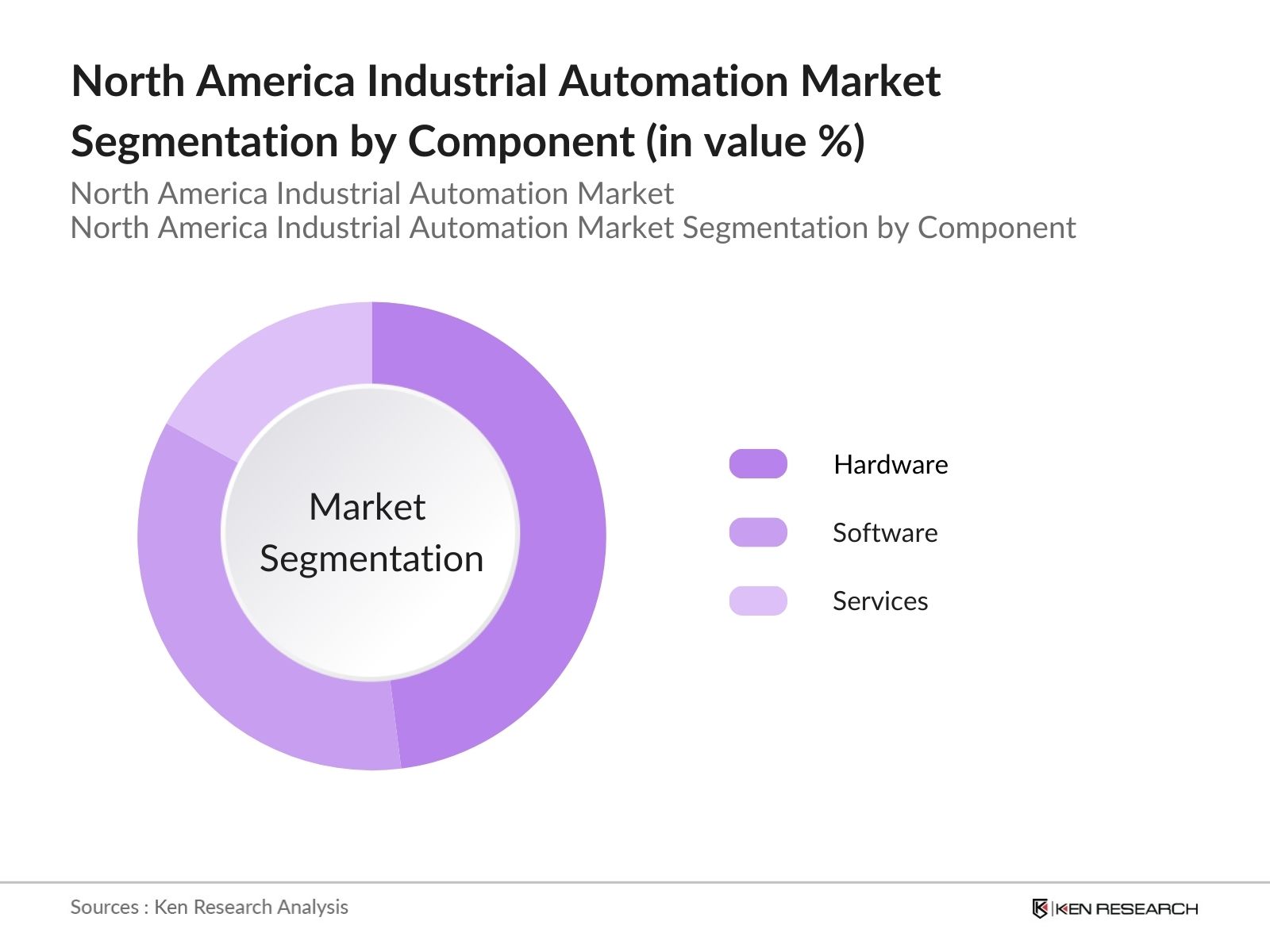

- By Component: The North America industrial automation market is segmented by component into hardware, software, and services. Recently, hardware dominated the market, driven by the increasing adoption of robotic systems, sensors, and programmable logic controllers (PLCs). This dominance is attributed to the growing integration of advanced machinery and robotics across industries, where manufacturers prioritize upgrading hardware infrastructure to enhance efficiency and reduce manual intervention.

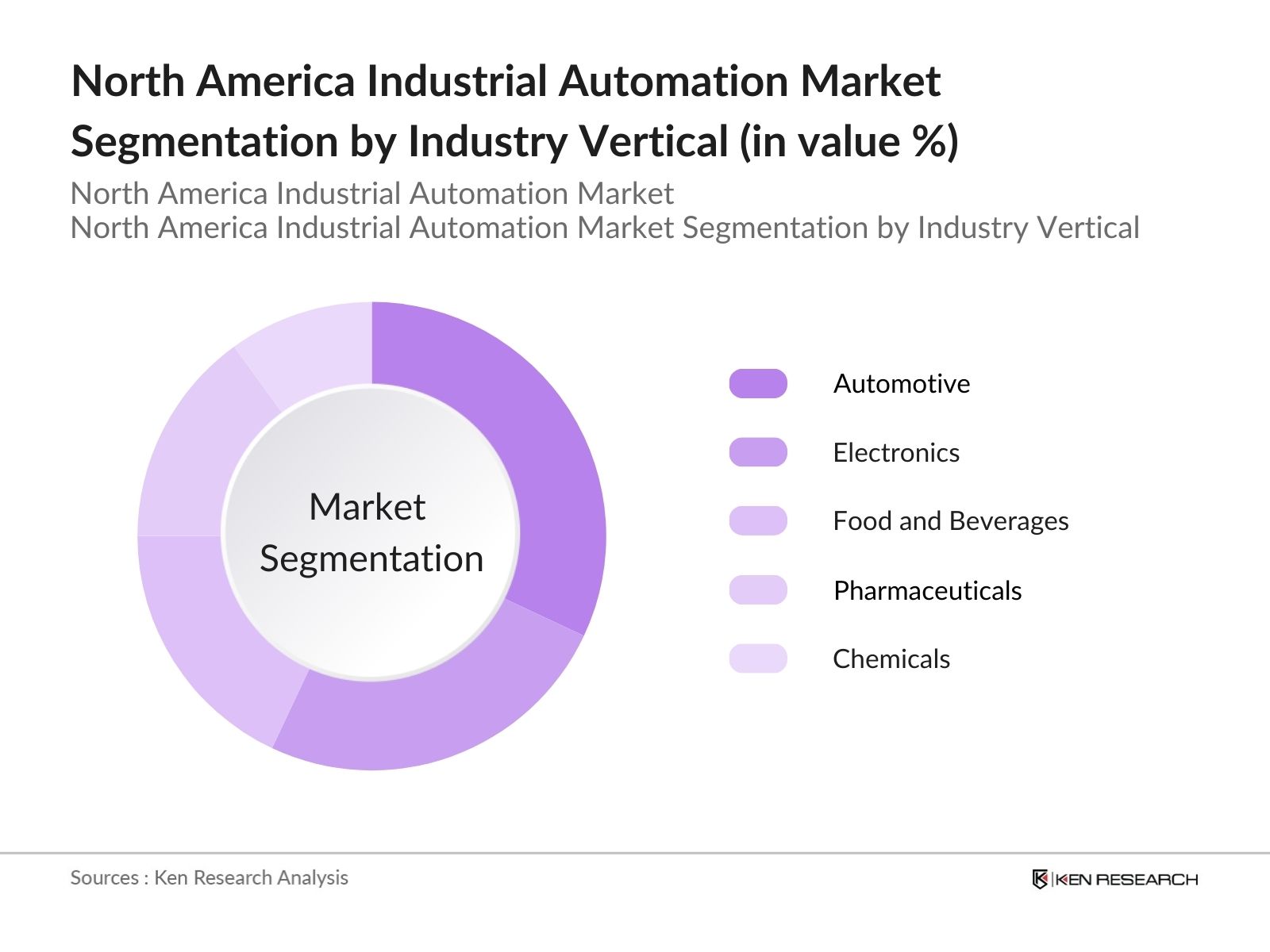

- By Industry Vertical: The industrial automation market in North America is also segmented by industry vertical into automotive, electronics, food and beverages, pharmaceuticals, and chemicals. The automotive industry dominated the market, owing to its large-scale investment in automation technologies such as robotic arms, automated production lines, and AI-driven process optimization. As one of the largest industrial sectors in North America, automotive companies have a long history of integrating automation to improve production efficiency and enhance safety standards.

North America Industrial Automation Market Competitive Landscape

The North American industrial automation market is characterized by the presence of a few dominant players, most of whom are multinational companies with large global footprints. These companies are instrumental in shaping the future of automation, offering a wide range of solutions from robotics to software integration. The competitive landscape is further consolidated by strategic partnerships and acquisitions within the sector.

|

Company Name |

Establishment Year |

Headquarters |

Global Reach |

R&D Expenditure |

Robotics Innovation |

Sustainability Initiatives |

Revenue (USD Bn) |

Patents Filed |

|

Siemens AG |

1847 |

Munich, Germany |

|

|

|

|

|

|

|

Rockwell Automation |

1903 |

Milwaukee, USA |

|

|

|

|

|

|

|

Honeywell International |

1906 |

Charlotte, USA |

|

|

|

|

|

|

|

ABB Ltd. |

1988 |

Zurich, Switzerland |

|

|

|

|

|

|

|

Mitsubishi Electric |

1921 |

Tokyo, Japan |

|

|

|

|

|

|

North America Industrial Automation Industry Analysis

North America Industrial Automation Market Growth Drivers

- Increasing Adoption of Smart Manufacturing: The integration of Industry 4.0 technologies across North American manufacturing facilities is accelerating. The U.S. industrial sector contributes over $3.8 trillion to the GDP, with a growing portion of that output driven by automation and smart factories. In 2024, over 60% of North American manufacturers are expected to adopt advanced automation, leading to an increase in productivity and efficiency. Government-backed initiatives like the Manufacturing USA Institutes, funded with $1 billion, support this transition. Advanced robotics and IoT integration in manufacturing are estimated to boost the output of smart factories by $120 billion annually by 2025.

- Demand for Industrial Robots and Cobots: The demand for industrial robots in North America is projected to increase significantly, driven by sectors like automotive and electronics. As of 2024, the number of industrial robots in operation surpassed 400,000 units, a figure supported by investments in collaborative robots (cobots) designed to work alongside humans. Automotive manufacturers invested $1.7 billion into robotic systems in 2022 alone, highlighting the rapid penetration of robots. Robotics are increasingly being adopted to meet rising production demands and offset labor shortages, with over 150,000 new units expected to be operational by the end of 2024.

- Rising Focus on Energy Efficiency: Energy efficiency in manufacturing is a key priority for North America, with industrial operations accounting for approximately 30% of total U.S. energy consumption. Automation technologies that optimize energy use are seeing significant adoption. As of 2024, over $100 billion in industrial energy savings have been attributed to automation solutions such as smart grids, robotics, and IoT. The U.S. Department of Energy’s Advanced Manufacturing Office is leading efforts to promote energy-efficient technologies, providing funding for energy optimization initiatives across industries to reduce energy consumption by 25% by 2025.

North America Industrial Automation Market Restraints

- Cybersecurity Concerns in Automated Systems: Automated industrial systems are increasingly becoming targets of cyber-attacks, especially as connectivity between devices and systems grows. In 2024, over 40% of U.S. manufacturing companies reported cybersecurity breaches, impacting production and leading to losses exceeding $10 billion across the industry. The rise in IoT devices and cloud-based automation exposes systems to vulnerabilities, with a majority of manufacturers expressing concerns about the risks of data breaches and cyber-attacks. These concerns hinder the full-scale adoption of advanced automation technologies across North America’s industrial sectors.

- Lack of Skilled Workforce for Advanced Automation: A significant shortage of skilled labor hampers the adoption of automation in North America. The U.S. manufacturing industry faces a gap of approximately 2.1 million workers by 2025, many of whom are needed to operate and maintain advanced automated systems. In 2024, around 70% of manufacturers cited difficulty in finding skilled workers to manage automation technologies, limiting the expansion of fully automated production lines. The lack of workforce training and upskilling programs exacerbates this challenge, with the industry calling for more vocational training initiatives.

North America Industrial Automation Market Future Outlook

Over the next five years, the North America industrial automation market is expected to grow at an accelerated pace, driven by the increasing adoption of artificial intelligence (AI) in manufacturing, the expansion of industrial IoT (IIoT) solutions, and continued government support for smart factory initiatives. Technological advancements in areas such as robotics, machine learning, and cloud computing will further catalyze the automation revolution in North America, leading to increased operational efficiency, reduced costs, and enhanced product quality across industries. As manufacturers seek to maintain competitiveness on a global scale, investment in automation will be critical to their success.

Market Opportunities

- Expansion of Industrial IoT (Internet of Things Integration): The expansion of Industrial IoT (IIoT) is revolutionizing North American manufacturing, connecting machines and systems for real-time data exchange. As of 2024, IIoT-connected devices in U.S. factories surpassed 14 million units. This expansion is being driven by government initiatives like the National Network for Manufacturing Innovation (NNMI) and private investments exceeding $200 billion in smart factories. IoT integration has the potential to reduce production downtime by 25%, while boosting operational efficiency, opening significant growth opportunities for automation companies.

- Rise of Artificial Intelligence and Machine Learning in Automation: Artificial intelligence (AI) and machine learning (ML) are transforming automation in North America. In 2024, AI-driven automation solutions are expected to reduce production defects by up to 40%. This growth is particularly evident in sectors like automotive, where AI is being used for predictive maintenance and real-time production optimization. Companies like Tesla and General Motors have adopted AI-powered robots, driving demand for intelligent systems. Government investment in AI research, including $2 billion for AI-based industrial applications, further supports the adoption of these technologies across North American industries.

Scope of the Report

|

By Component |

- Hardware |

|

- Software |

|

|

- Services |

|

|

By Industry Vertical |

- Automotive |

|

- Chemicals |

|

|

- Food and Beverages |

|

|

- Electronics and Semiconductor |

|

|

- Pharmaceuticals |

|

|

By Technology |

- Distributed Control System (DCS) |

|

- Supervisory Control and Data Acquisition (SCADA) |

|

|

- Programmable Logic Controller (PLC) |

|

|

- Human-Machine Interface (HMI) |

|

|

By End-Use |

- Discrete Manufacturing |

|

- Process Manufacturing |

|

|

- Hybrid Manufacturing |

|

|

By Region |

- United States |

|

- Canada |

|

|

- Mexico |

Products

Key Target Audience

- Automotive Manufacturers

- Pharmaceutical Companies

- Electronics and Semiconductor Manufacturers

- Food and Beverage Companies

- Chemicals Manufacturers

- Investment and Venture Capitalist Firms

- Government and Regulatory Bodies (OSHA, ISO, NIST)

- Energy and Utility Companies

Time Period Captured in the Report:

- Historical Period: 2018-2023

- Base Year: 2023

- Forecast Period: 2023-2028

Companies

- Siemens AG

- ABB Ltd.

- Honeywell International

- Rockwell Automation

- Mitsubishi Electric

- Emerson Electric

- Schneider Electric

- FANUC Corporation

- Omron Corporation

- General Electric

- KUKA AG

- Bosch Rexroth

- Parker Hannifin

- Schneider Electric SE

- Yokogawa Electric Corporation

Table of Contents

1. North America Industrial Automation Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Industrial Automation Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Industrial Automation Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Adoption of Smart Manufacturing (Industry 4.0 Integration)

3.1.2. Demand for Industrial Robots and Cobots (Robotics Penetration)

3.1.3. Government Support for Automation and Efficiency (Government Incentives)

3.1.4. Rising Focus on Energy Efficiency (Energy Optimization)

3.2. Market Challenges

3.2.1. High Initial Capital Investment

3.2.2. Cybersecurity Concerns in Automated Systems

3.2.3. Lack of Skilled Workforce for Advanced Automation

3.3. Opportunities

3.3.1. Expansion of Industrial IoT (Internet of Things Integration)

3.3.2. Rise of Artificial Intelligence and Machine Learning in Automation

3.3.3. Automation in Green Manufacturing Initiatives

3.4. Trends

3.4.1. Growing Use of Predictive Maintenance (Predictive Analytics)

3.4.2. Cloud-Based Automation Solutions (Cloud Integration)

3.4.3. Autonomous Mobile Robots (AMR) and AGVs (Automated Guided Vehicles)

3.5. Government Regulations

3.5.1. North American Standards for Industrial Automation

3.5.2. Safety and Compliance Requirements (ISO and OSHA)

3.5.3. Environmental Regulations and Sustainable Practices

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces

3.9. Competitive Ecosystem

4. North America Industrial Automation Market Segmentation

4.1. By Component (In Value %)

4.1.1. Hardware

4.1.2. Software

4.1.3. Services

4.2. By Industry Vertical (In Value %)

4.2.1. Automotive

4.2.2. Chemicals

4.2.3. Food and Beverages

4.2.4. Electronics and Semiconductor

4.2.5. Pharmaceuticals

4.3. By Technology (In Value %)

4.3.1. Distributed Control System (DCS)

4.3.2. Supervisory Control and Data Acquisition (SCADA)

4.3.3. Programmable Logic Controller (PLC)

4.3.4. Human-Machine Interface (HMI)

4.4. By End-Use (In Value %)

4.4.1. Discrete Manufacturing

4.4.2. Process Manufacturing

4.4.3. Hybrid Manufacturing

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Industrial Automation Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Siemens AG

5.1.2. ABB Ltd.

5.1.3. Emerson Electric Co.

5.1.4. Honeywell International Inc.

5.1.5. Rockwell Automation

5.1.6. Schneider Electric SE

5.1.7. Mitsubishi Electric Corporation

5.1.8. Yokogawa Electric Corporation

5.1.9. Omron Corporation

5.1.10. FANUC Corporation

5.1.11. KUKA AG

5.1.12. General Electric Company

5.1.13. Bosch Rexroth AG

5.1.14. ABB Robotics

5.1.15. Parker Hannifin Corporation

5.2. Cross Comparison Parameters (Number of Patents, Robotics Deployment Rate, Automation Software Licensing, Employee Count in Automation, Global Reach, Revenue from Automation, Sustainability Initiatives, R&D Expenditure)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6. North America Industrial Automation Market Regulatory Framework

6.1. Automation Compliance Standards

6.2. Certification Requirements

6.3. Safety Protocols for Automation Systems

7. North America Industrial Automation Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Industrial Automation Future Market Segmentation

8.1. By Component (In Value %)

8.2. By Industry Vertical (In Value %)

8.3. By Technology (In Value %)

8.4. By End-Use (In Value %)

8.5. By Region (In Value %)

9. North America Industrial Automation Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first step involves developing a comprehensive ecosystem map of the North American industrial automation market, which includes key players, end-users, and technology providers. This step requires extensive desk research, utilizing a mix of secondary databases and proprietary research tools to gather industry-specific data.

Step 2: Market Analysis and Construction

In this step, historical data on market penetration, the adoption rate of automation technologies, and revenue generation metrics are analyzed. Additionally, the quality of automation solutions and their role in the overall market performance is examined to ensure reliable revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

In this phase, market hypotheses are formulated and validated through direct interviews and consultations with industry professionals. These consultations provide key insights into real-world challenges and opportunities, ensuring accurate data validation.

Step 4: Research Synthesis and Final Output

The final step involves direct engagement with companies across various industry verticals to capture a detailed view of the market, including product preferences, usage statistics, and future outlook. The integration of this data ensures the accuracy of the market forecast and analysis.

Frequently Asked Questions

01. How big is the North America Industrial Automation Market?

The North America industrial automation market is valued at USD 47 billion, driven by the adoption of robotics, Industry 4.0 technologies, and government support for manufacturing automation.

02. What are the challenges in the North America Industrial Automation Market?

Key challenges include high initial capital expenditure, cybersecurity risks in connected industrial systems, and a lack of skilled professionals capable of managing advanced automated systems.

03. Who are the major players in the North America Industrial Automation Market?

The major players include Siemens AG, ABB Ltd., Honeywell International, Rockwell Automation, and Mitsubishi Electric. These companies lead the market due to their extensive product portfolios, global reach, and significant R&D investments.

04. What are the growth drivers of the North America Industrial Automation Market?

Growth is propelled by technological advancements in robotics, IoT integration, and AI-driven process optimization. Additionally, government incentives and demand for operational efficiency further accelerate market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.