North America Industrial Filtration Market Outlook to 2030

Region:North America

Author(s):Vijay Kumar

Product Code:KROD4968

December 2024

92

About the Report

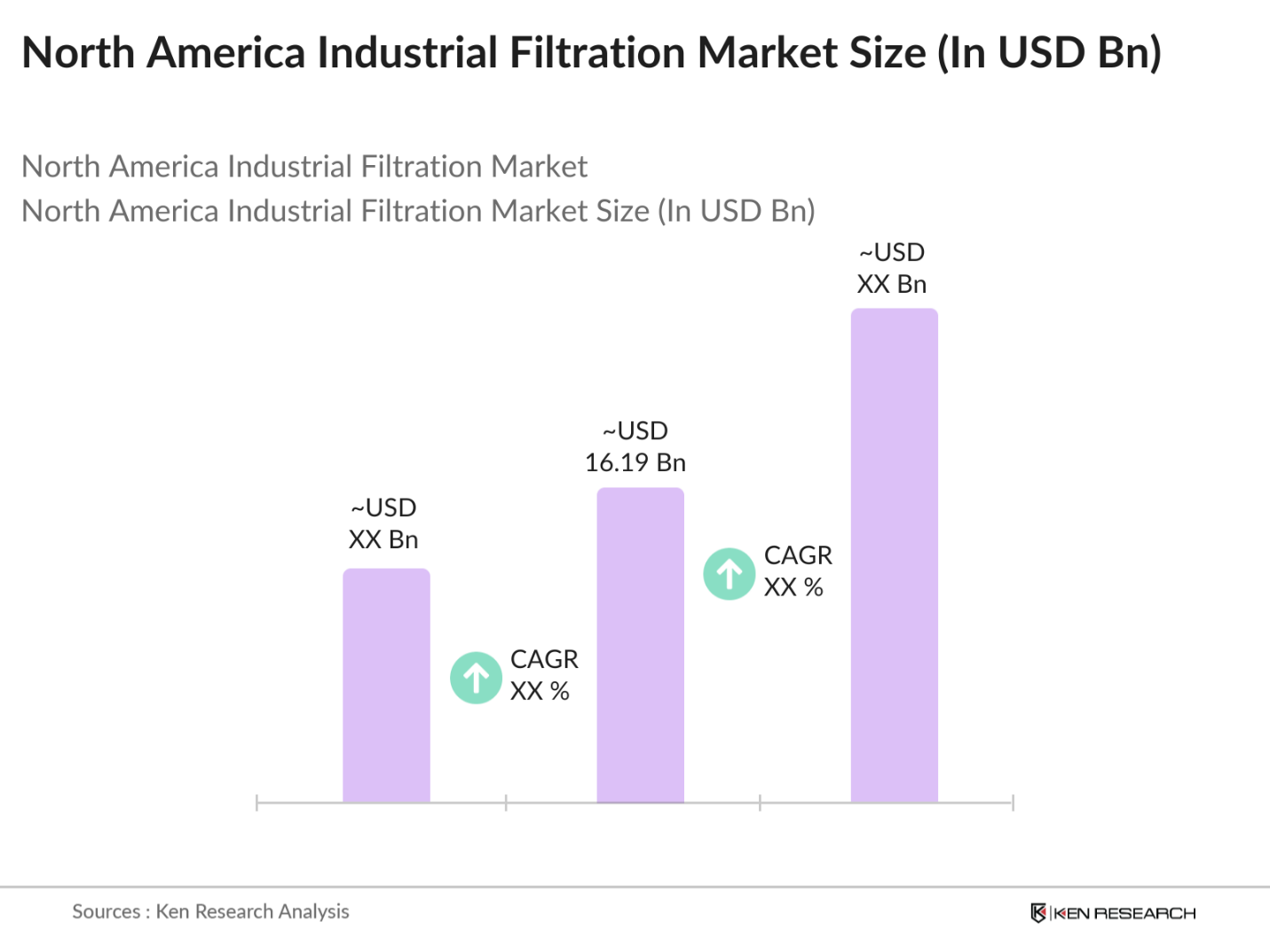

North America Industrial Filtration Market Overview

- The North America Industrial Filtration market is valued at USD 16.19 billion, based on a five-year historical analysis. This market growth is primarily driven by the increasing demand for efficient filtration systems across industries such as manufacturing, power generation, and oil & gas. The rise in regulatory requirements for pollution control and emission reductions, enforced by agencies like the Environmental Protection Agency (EPA), is also contributing to the market's expansion. Additionally, the need for improved air and water quality is boosting demand in both industrial and commercial sectors.

- In North America, the United States holds a dominant position in the industrial filtration market. This dominance is attributed to the vast presence of manufacturing industries, large-scale power plants, and stringent environmental regulations that require filtration systems to meet sustainability goals. Other significant contributors include Canada, where industries like oil & gas and food processing heavily utilize filtration technology to meet operational and environmental standards. The geographic proximity of key industrial hubs ensures the continued growth of the market in these regions.

- The Clean Water Act continues to be a significant regulatory framework driving the industrial filtration market in North America. The act mandates stringent water treatment standards, impacting over 16,000 industrial facilities in the U.S. alone. These facilities rely on advanced filtration systems to comply with the legislation, which focuses on minimizing pollutants in water discharged into the environment.

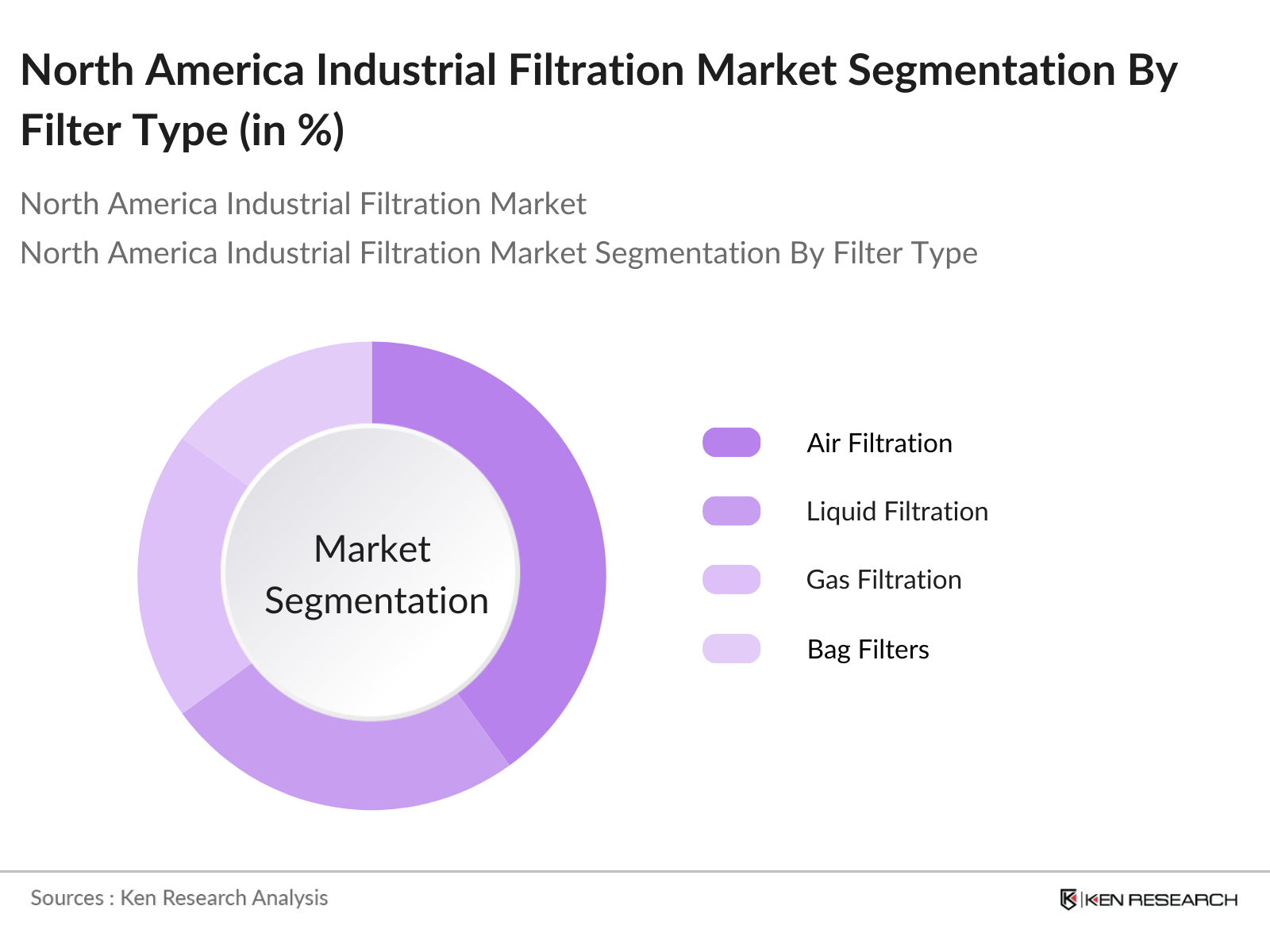

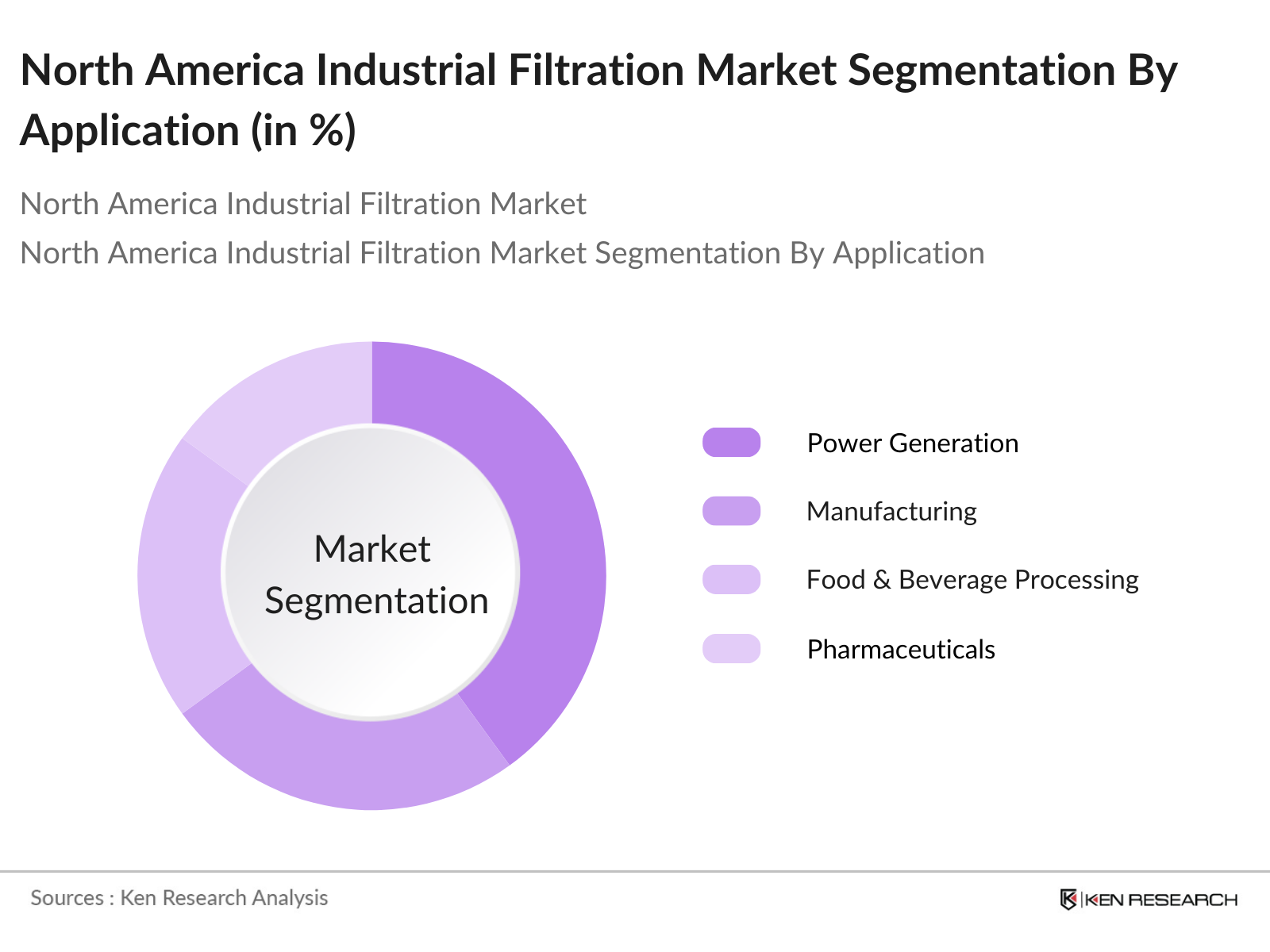

North America Industrial Filtration Market Segmentation

By Filter Type: The North America Industrial Filtration Market is segmented by filter type into air filtration, liquid filtration, gas filtration, and bag filters. Among these, air filtration dominates the market due to its widespread application in power generation, HVAC systems, and industrial manufacturing. This segment's growth is supported by stringent environmental regulations, particularly in the United States, which require industries to reduce airborne pollutants.

By Application: The market is also segmented by application into power generation, manufacturing, food & beverage processing, pharmaceuticals, and oil & gas. The power generation sector holds the largest market share due to the increased need for filtration solutions to manage emissions and maintain the efficiency of power plants. This dominance is further driven by the sector's adoption of filtration systems to comply with strict environmental regulations, particularly regarding air pollution.

North America Industrial Filtration Market Competitive Landscape

The North America Industrial Filtration Market is dominated by a few key players with significant market presence and advanced product portfolios. These companies leverage their scale, technological innovations, and strong distribution networks to maintain competitive advantages. The North American market for industrial filtration is led by major players like Parker-Hannifin Corporation, Donaldson Company, and Eaton Corporation.

North America Industrial Filtration Industry Analysis

Growth Drivers

- Growth in Industrialization (Manufacturing, Power Generation, Oil & Gas): The industrialization of North America continues to rise, with the U.S. recording a manufacturing output of $2.3 trillion in 2022. Industrial filtration systems are critical in sectors such as power generation, which contributed over 3,900 billion kilowatt hours to the U.S. grid in 2023, and oil & gas, with production levels nearing 18 million barrels per day.

- Stringent Environmental Regulations (EPA Standards, Clean Air Act): The U.S. Environmental Protection Agency (EPA) has intensified its enforcement of air and water quality standards, including stricter limits under the Clean Air Act. Over 36,000 tons of emissions were reduced in 2023 due to regulatory compliance efforts. These regulations necessitate the adoption of advanced filtration systems to remove pollutants, positioning industrial filtration as a vital tool for businesses to avoid hefty fines and shutdowns.

- Increasing Focus on Industrial Sustainability (Waste Management, Water Reuse): North American industries have heightened their sustainability initiatives, driven by the push for cleaner production practices. In 2023, over 11 billion gallons of industrial wastewater were treated and reused in the U.S. daily. Filtration technologies play a critical role in supporting these practices by minimizing waste, enabling water reuse, and reducing reliance on fresh water resources. Businesses that adopt such measures are benefiting from reduced operational costs and increased efficiency.

Market Challenges

- High Capital Investment (Cost of Implementation, R&D Expenditure): One of the major challenges in the industrial filtration market is the significant capital investment required for the implementation of advanced systems. A 2022 study by the U.S. Department of Energy found that implementing smart filtration systems can cost over $150,000 per facility. Additionally, ongoing R&D expenses in the development of sustainable filtration technologies remain high, leading to prolonged return on investment for businesses.

- Complexity in Filtration Process (Cross-Contamination, Filtration Efficacy): Industrial filtration processes, particularly in high-risk industries such as chemicals and pharmaceuticals, face operational challenges. Cross-contamination risks and achieving filtration efficacy of 99.99% or higher are concerns for manufacturers. In 2023, over 200 contamination-related shutdowns were reported in U.S. manufacturing plants. This highlights the need for high-efficiency filtration solutions to ensure compliance with strict operational standards.

North America Industrial Filtration Market Future Outlook

Over the next five years, the North America Industrial Filtration Market is expected to experience significant growth, driven by increasing industrialization, stricter environmental regulations, and advancements in filtration technology. The shift towards more energy-efficient and sustainable filtration solutions will be a major trend, as industries look to reduce operational costs while meeting regulatory standards. Moreover, technological innovations, such as IoT-enabled filtration systems and smart monitoring devices, will further fuel market expansion by improving operational efficiency and enabling predictive maintenance.

Market Opportunities

- Growing Demand for Clean Water (Water Treatment Plants, Zero-Liquid Discharge): North America's growing demand for clean water is providing significant opportunities for the industrial filtration market. In 2023, the U.S. operated over 16,000 water treatment facilities, with new regulations encouraging the adoption of zero-liquid discharge systems. These systems rely on advanced filtration to ensure zero waste discharge into the environment. The industrial sector is seeing increased investments in filtration solutions to comply with these water conservation efforts.

- Adoption of Energy-Efficient Filtration Solutions (Low-Energy Filters, Smart Filter Media): Energy-efficient filtration technologies are gaining traction in North America, driven by a focus on reducing industrial energy consumption. The U.S. Department of Energy reported that industries could save over $10 billion annually by adopting low-energy filters and smart filter media in 2024. These technologies minimize energy consumption while maintaining high filtration efficiency, positioning them as cost-effective and environmentally responsible solutions for industries.

Scope of the Report

|

Filter Type |

Air Filtration Liquid Filtration Gas Filtration Bag Filters Cartridge Filters |

|

Application |

Power Generation Manufacturing Food & Beverage Processing Pharmaceuticals Oil & Gas |

|

Technology |

Mechanical Filtration Electrostatic Filtration Membrane Filtration Gravity Filtration |

|

Material Type |

Metal Polymer Ceramic Fiber |

|

Region |

United States Canada Mexico |

Products

Key Target Audience

Power Generation Companies

Manufacturing Industries

Food & Beverage Processing Plants

Oil & Gas Companies

Water Treatment Facilities

Government and Regulatory Bodies (Environmental Protection Agency, Department of Energy)

Investment and Venture Capitalist Firms

Industrial Equipment Manufacturers

Companies

Players Mentioned in the Report

Parker-Hannifin Corporation

Donaldson Company, Inc.

Eaton Corporation

Ahlstrom-Munksj

Camfil AB

Pall Corporation

MANN+HUMMEL Group

Filtration Group Corporation

3M

Lenntech BV

Table of Contents

1. North America Industrial Filtration Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Industrial Filtration Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Industrial Filtration Market Analysis

3.1. Growth Drivers

3.1.1. Growth in Industrialization (Manufacturing, Power Generation, Oil & Gas)

3.1.2. Stringent Environmental Regulations (EPA Standards, Clean Air Act)

3.1.3. Increasing Focus on Industrial Sustainability (Waste Management, Water Reuse)

3.1.4. Technological Advancements (Smart Filtration Systems, IoT Integration)

3.2. Market Challenges

3.2.1. High Capital Investment (Cost of Implementation, R&D Expenditure)

3.2.2. Complexity in Filtration Process (Cross-Contamination, Filtration Efficacy)

3.2.3. Maintenance and Downtime Issues (Operational Efficiency, Equipment Durability)

3.3. Opportunities

3.3.1. Growing Demand for Clean Water (Water Treatment Plants, Zero-Liquid Discharge)

3.3.2. Adoption of Energy-Efficient Filtration Solutions (Low-Energy Filters, Smart Filter Media)

3.3.3. Expansion into Emerging Markets (Mexico, Canada)

3.4. Trends

3.4.1. Adoption of Hybrid Filtration Technologies (Electrostatic, Membrane Filtration)

3.4.2. Rise of Smart Filtration Solutions (Predictive Maintenance, Automated Systems)

3.4.3. Increased Focus on Sustainability (Reusable Filters, Waste Minimization)

3.5. Government Regulations

3.5.1. Clean Water Act (Water Treatment Compliance)

3.5.2. Emission Control Standards (Air Quality Control)

3.5.3. Industrial Waste Management Policies (Wastewater, Solid Waste)

3.5.4. Government Incentives (Energy-Saving Initiatives)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (End-Users, Suppliers, Manufacturers)

3.8. Porters Five Forces

3.9. Competitive Ecosystem

4. North America Industrial Filtration Market Segmentation

4.1. By Filter Type (In Value %)

4.1.1. Air Filtration

4.1.2. Liquid Filtration

4.1.3. Gas Filtration

4.1.4. Bag Filters

4.1.5. Cartridge Filters

4.2. By Application (In Value %)

4.2.1. Power Generation

4.2.2. Manufacturing

4.2.3. Food & Beverage Processing

4.2.4. Pharmaceuticals

4.2.5. Oil & Gas

4.3. By Technology (In Value %)

4.3.1. Mechanical Filtration

4.3.2. Electrostatic Filtration

4.3.3. Membrane Filtration

4.3.4. Gravity Filtration

4.4. By Material Type (In Value %)

4.4.1. Metal

4.4.2. Polymer

4.4.3. Ceramic

4.4.4. Fiber

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Industrial Filtration Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Parker-Hannifin Corporation

5.1.2. Donaldson Company, Inc.

5.1.3. Ahlstrom-Munksj

5.1.4. Eaton Corporation

5.1.5. Camfil AB

5.1.6. Pall Corporation

5.1.7. MANN+HUMMEL Group

5.1.8. Filtration Group Corporation

5.1.9. 3M

5.1.10. Lenntech BV

5.1.11. Lydall, Inc.

5.1.12. Cummins Filtration

5.1.13. Freudenberg Filtration Technologies

5.1.14. Pentair

5.1.15. Koch Filter Corporation

5.2. Cross Comparison Parameters (Market Share, Headquarters, Product Portfolio, Revenue, Employee Count, Manufacturing Capabilities, Global Presence, R&D Expenditure)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Industrial Filtration Market Regulatory Framework

6.1. Environmental Standards (EPA Compliance, State Regulations)

6.2. Compliance Requirements (ISO Standards, OSHA Guidelines)

6.3. Certification Processes (Energy Star, LEED Certification)

7. North America Industrial Filtration Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Industrial Filtration Future Market Segmentation

8.1. By Filter Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Material Type (In Value %)

8.5. By Region (In Value %)

9. North America Industrial Filtration Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase involves creating an ecosystem map of the North America Industrial Filtration Market. This process includes detailed desk research and analysis of multiple secondary sources, such as company reports, industry databases, and governmental publications. The key objective is to identify the primary variables influencing market growth, such as filtration efficiency, regulatory compliance, and energy consumption.

Step 2: Market Analysis and Construction

This phase involves compiling historical data on market penetration rates, revenue generation, and sales volume across various segments. The focus is on assessing key performance indicators, including the operational efficiency of filtration systems and their adoption rates across industrial sectors.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses regarding market dynamics and growth drivers are developed based on the analysis. These hypotheses are then validated through expert consultations, particularly with senior executives from major filtration companies and industry experts, to ensure data accuracy.

Step 4: Research Synthesis and Final Output

Finally, a combination of top-down and bottom-up approaches is applied to ensure the accuracy of the data. This phase includes direct engagement with filtration manufacturers, distributors, and other stakeholders to refine and validate the findings, which will be presented as part of the final market report.

Frequently Asked Questions

1. How big is the North America Industrial Filtration Market?

The North America Industrial Filtration market is valued at USD 16.19 billion, based on a five-year historical analysis. This market growth is primarily driven by the increasing demand for efficient filtration systems across industries such as manufacturing, power generation, and oil & gas.

2. What are the challenges in the North America Industrial Filtration Market?

Challenges include the high capital investment required for advanced filtration systems, complexities in managing filtration processes, and maintaining operational efficiency in harsh industrial environments.

3. Who are the major players in the North America Industrial Filtration Market?

Key players in the market include Parker-Hannifin Corporation, Donaldson Company, Eaton Corporation, and Camfil AB, among others, who dominate due to their strong distribution networks and advanced technology.

4. What drives the North America Industrial Filtration Market?

The market is driven by the growing need for efficient filtration systems across industries such as power generation, manufacturing, and food & beverage, along with stricter environmental regulations enforced by the EPA.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.