North America Juice Concentrates Market Outlook to 2030

Region:North America

Author(s):Meenakshi Bisht

Product Code:KROD8225

December 2024

95

About the Report

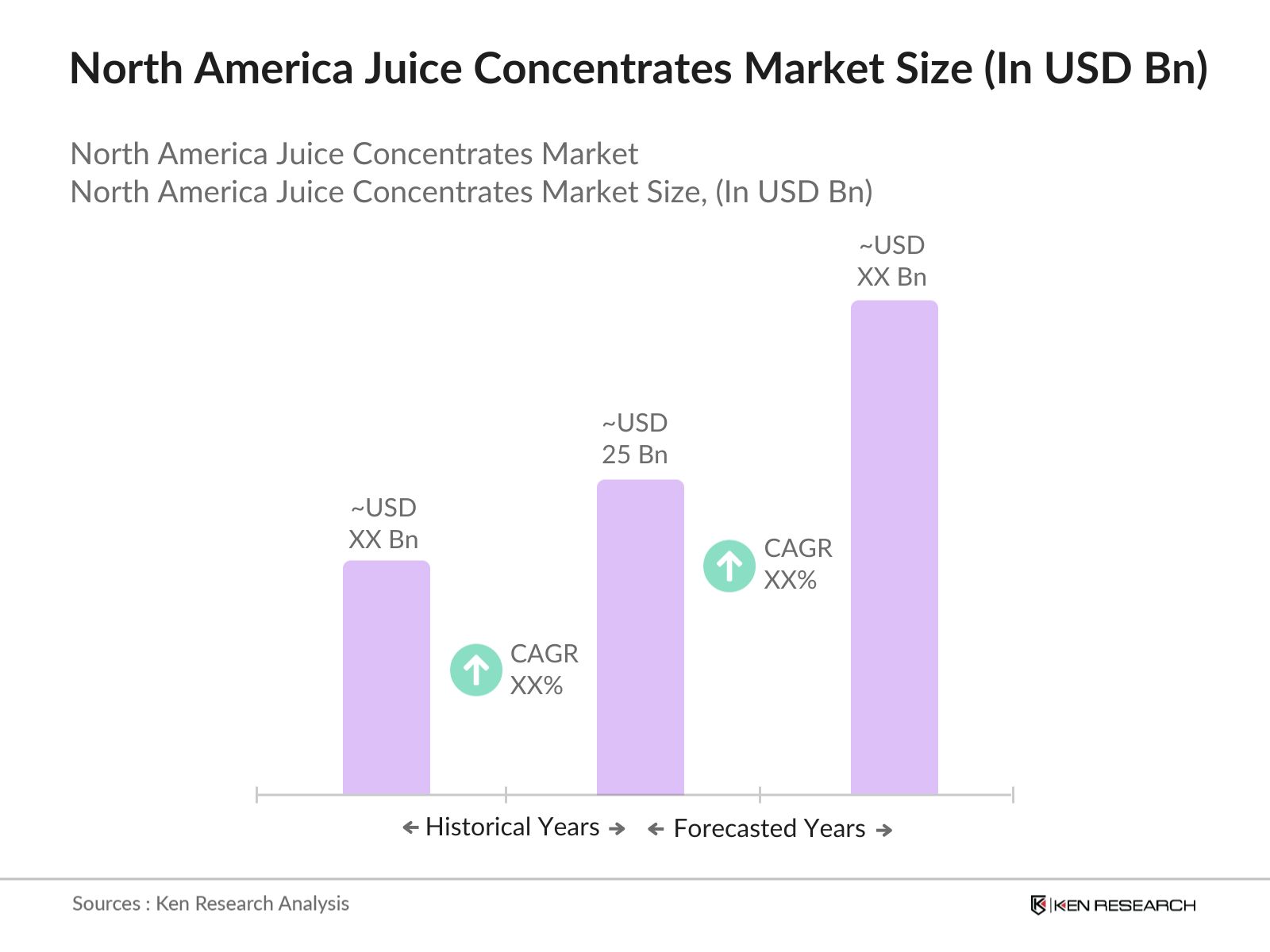

North America Juice Concentrates Market Overview

- The North America Juice Concentrates Market is valued at USD 25 billion, driven by growing consumer demand for natural, minimally processed ingredients. The preference for clean-label and natural sweeteners, along with the increasing popularity of health-conscious beverages like cold-pressed juices and functional drinks, has significantly boosted the adoption of juice concentrates. Food and beverage manufacturers are increasingly turning to juice concentrates as an alternative to artificial flavors and sweeteners, contributing to the market's steady growth.

- In North America, the United States and Canada dominate the juice concentrates market. The United States' dominance is due to its extensive beverage industry, high disposable income levels, and growing demand for healthier beverage options. Canada, known for its robust fruit production, particularly apples and berries, supports the availability of raw materials for juice concentrates. Both countries also benefit from well-established supply chains and a consumer base that favors convenience products, making them key players in the market.

- The FDAs guidelines on labeling, including the Nutrition Labeling and Education Act, mandate that juice concentrates disclose all ingredients and nutritional information. In 2023, the FDA released a draft Compliance Policy Guide focusing on major food allergens and their labeling requirements. This reflects an ongoing effort to clarify and enforce allergen labeling standards. Accurate labeling is crucial for consumer transparency, particularly for those with dietary restrictions.

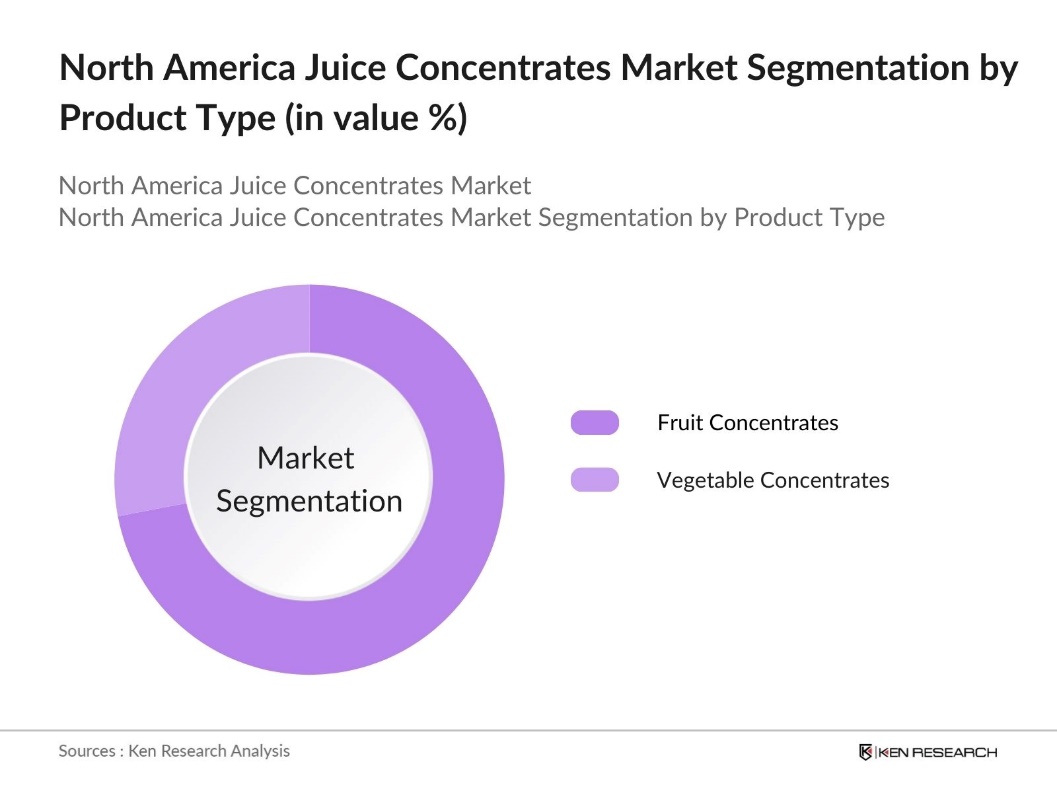

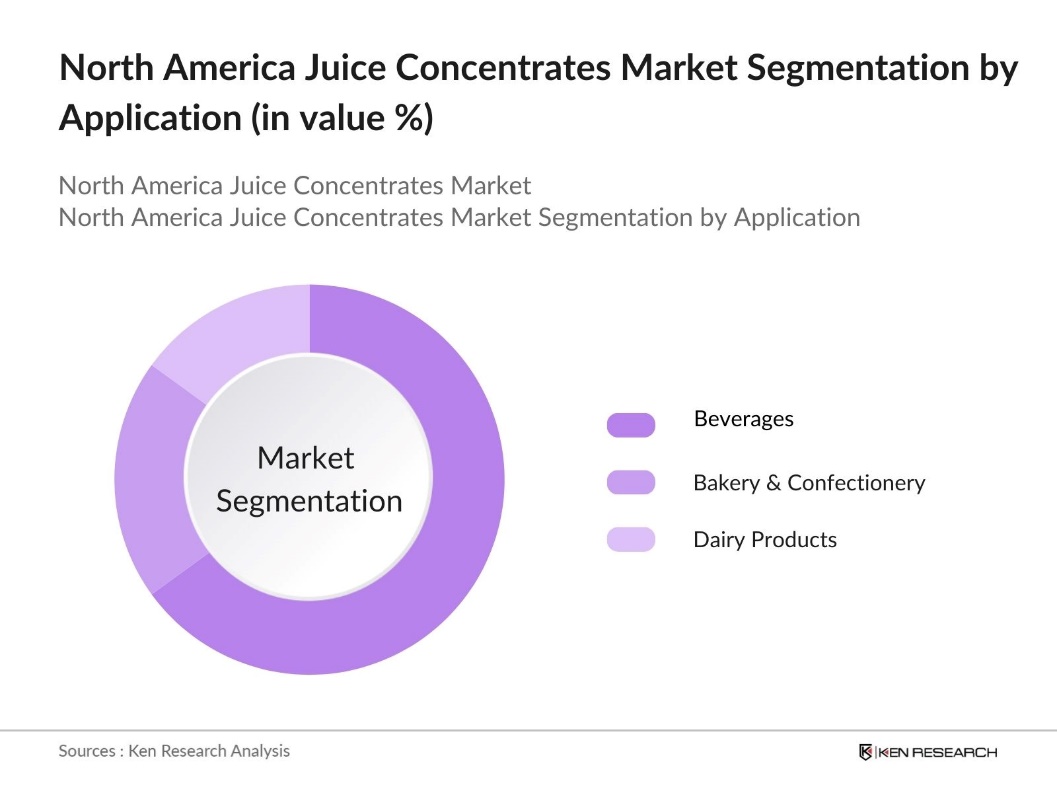

North America Juice Concentrates Market Segmentation

By Product Type: The North America Juice Concentrates market is segmented by product type into fruit concentrates and vegetable concentrates. The Fruit concentrates hold a dominant market share within this segmentation due to their wide application in beverages, bakery, and dairy products. The versatility of fruit concentrates like apple, orange, and berry in various end products, along with their natural flavoring and sweetening properties, makes them a preferred choice among manufacturers.

By Application: The North America Juice Concentrates market is segmented by application into beverages, bakery & confectionery, and dairy products. The beverages segment dominates the market, driven by the rising consumption of juices, smoothies, and flavored water. Juice concentrates serve as a base for these beverages, offering cost-effective production and a natural ingredient appeal. The ongoing trend of healthy and functional drinks, such as immunity-boosting juices, continues to bolster demand within this segment.

North America Juice Concentrates Market Competitive Landscape

The market is characterized by a mix of large multinational corporations and specialized regional producers. The market's competitive nature is driven by factors like product innovation, raw material sourcing capabilities, and regional expansion strategies. The leading players invest heavily in R&D to create new formulations and meet evolving consumer preferences for clean-label and organic products.

|

Company |

Establishment Year |

Headquarters |

R&D Expenditure |

Sustainability Initiatives |

Product Range |

Organic Certifications |

Distribution Network |

Revenue |

Regional Presence |

|

Archer Daniels Midland Co. |

1902 |

Chicago, USA |

|||||||

|

Ingredion Incorporated |

1906 |

Westchester, USA |

|||||||

|

Dhler GmbH |

1838 |

Darmstadt, Germany |

|||||||

|

SunOpta Inc. |

1973 |

Minnesota, USA |

|||||||

|

Kerry Group |

1972 |

Tralee, Ireland |

North America Juice Concentrates Industry Analysis

Growth Drivers

- Rise in Health-Conscious Consumers: The shift in consumer preferences towards healthier options has driven the demand for juice concentrates in North America. Around 50% of Americans reported actively trying to eat healthier in 2023, emphasizing low-sugar and natural products. This shift has influenced the beverage sector, where natural juice concentrates are perceived as healthier alternatives to synthetic sweeteners. This trend aligns with government health initiatives, encouraging natural and nutritious consumption.

- Shift towards Natural Sweeteners: North America has seen a rise in the use of natural sweeteners like juice concentrates in response to declining sugar consumption. A plant-derived sweetener that is 200 to 400 times sweeter than sugar and contains no calories, making it a favorite among those looking to reduce caloric intake. This trend has been further supported by the FDA's guidelines promoting the use of natural ingredients in food products.

- Beverage Industry Growth: The beverage industry's expansion in North America has boosted the demand for juice concentrates, driven by a shift towards healthier, ready-to-drink options like fruit-based energy drinks and cold-pressed juices. This trend encourages innovation within the sector, while government support for local fruit production ensures a steady supply of raw materials, helping manufacturers meet the growing demand for high-quality juice concentrates.

Market Challenges

- Price Sensitivity: The juice concentrate market in North America is highly price-sensitive, with fluctuations in raw material costs directly impacting manufacturers. Variability in supply, often due to external factors, can affect production costs, making it challenging to maintain stable pricing. In such a competitive market, consumers are often resistant to price increases, which pressures producers to remain competitive, especially with imported concentrates influencing market dynamics.

- Quality Control Issues: Maintaining consistent quality in juice concentrates is a significant challenge, as any variation can affect taste and nutritional value. Stringent regulations require manufacturers to adhere to high safety and quality standards, ensuring proper labeling and nutrient retention. Any lapses in quality control can result in financial setbacks and harm a brands reputation, particularly as consumers increasingly prioritize transparency and ingredient sourcing.

North America Juice Concentrates Market Future Outlook

Over the next five years, the North America Juice Concentrates market is expected to experience steady growth, driven by an increasing shift towards natural and organic products. Consumer preferences for healthier beverage alternatives and clean-label ingredients are likely to continue fueling demand for juice concentrates. Additionally, the trend towards low-calorie sweeteners is expected to enhance the adoption of unsweetened juice concentrates in a range of food and beverage applications.

Market Opportunities

- Increased Demand for Organic Juice Concentrates: Consumer interest in organic juice products has grown significantly in North America, driven by preferences for pesticide-free and non-GMO options. This shift has created a strong market for organic juice concentrates, supported by organic certifications that build consumer trust. The trend reflects broader shifts towards healthier and more natural products, presenting a valuable opportunity for manufacturers to expand their offerings in the organic segment.

- Functional Juice Market Growth: The popularity of functional beverages, especially those enriched with vitamins and antioxidants, has increased, driving demand for juice concentrates. These concentrates, often used in energy drinks and immunity-boosting beverages, are seen as convenient solutions for health-conscious consumers. This trend allows manufacturers to explore innovative formulations that meet the growing preference for products with added health benefits, aligning with consumer demand for more nutritious beverage options.

Scope of the Report

|

Product Type |

Fruit Concentrates Vegetable Concentrates |

|

Application |

Beverages Bakery & Confectionery Dairy Products Sauces & Dressings |

|

Form |

Liquid Powder Frozen |

|

Ingredient Type |

Sweetened Unsweetened |

|

Region |

United States Canada Mexico |

Products

Key Target Audience

Beverage Manufacturers

Dairy Product Manufacturers

Juice Processing Equipment Manufacturers

Nutraceutical Companies

Investors and venture capital Firms

Banks and Financial Institutions

Government and Regulatory Bodies (FDA, USDA)

Companies

Players Mentioned in the Report

Archer Daniels Midland Company

Ingredion Incorporated

Dhler GmbH

Kerry Group

SunOpta Inc.

AGRANA Group

Diana Food (Symrise)

SVZ International B.V.

Ciatti Company

Lemon Concentrate

Table of Contents

1. North America Juice Concentrates Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America Juice Concentrates Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America Juice Concentrates Market Analysis

3.1. Growth Drivers (Increased consumer demand for natural products, health trends, expansion of food and beverage industry)

3.1.1. Rise in Health-Conscious Consumers

3.1.2. Shift towards Natural Sweeteners

3.1.3. Beverage Industry Growth

3.2. Market Challenges (High competition, fluctuating raw material prices, supply chain disruptions)

3.2.1. Price Sensitivity

3.2.2. Quality Control Issues

3.2.3. Environmental Sustainability Concerns

3.3. Opportunities (Innovations in product formulations, organic certifications, global export potential)

3.3.1. Increased Demand for Organic Juice Concentrates

3.3.2. Functional Juice Market Growth

3.3.3. Clean Label Trends

3.4. Trends (Sustainability initiatives, packaging innovations, consumer preference for exotic fruits)

3.4.1. Growth in Cold-Pressed Juice

3.4.2. New Packaging Technologies

3.4.3. Introduction of Exotic Fruit Juice Concentrates

3.5. Government Regulations (Food safety standards, labeling laws, import/export regulations)

3.5.1. FDA Compliance for Juice Products

3.5.2. Labeling Requirements for Concentrates

3.5.3. Tariffs on Imported Fruit Concentrates

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Farmers, manufacturers, retailers, distributors)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. North America Juice Concentrates Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Fruit Concentrates (Orange, Apple, Grape, Pineapple, Exotic Fruits)

4.1.2. Vegetable Concentrates (Carrot, Tomato, Spinach)

4.2. By Application (In Value %)

4.2.1. Beverages (Soft Drinks, Juices, Smoothies)

4.2.2. Bakery & Confectionery (Cakes, Pastries, Candies)

4.2.3. Dairy Products (Yogurt, Ice Cream)

4.2.4. Sauces & Dressings

4.3. By Form (In Value %)

4.3.1. Liquid Concentrates

4.3.2. Powder Concentrates

4.3.3. Frozen Concentrates

4.4. By Ingredient Type (In Value %)

4.4.1. Sweetened Juice Concentrates

4.4.2. Unsweetened Juice Concentrates

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America Juice Concentrates Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Archer Daniels Midland Company

5.1.2. Ingredion Incorporated

5.1.3. Dhler GmbH

5.1.4. Kerry Group

5.1.5. SunOpta Inc.

5.1.6. AGRANA Group

5.1.7. Diana Food (Symrise)

5.1.8. SVZ International B.V.

5.1.9. Ciatti Company

5.1.10. Lemon Concentrate

5.1.11. Fenco Food Machinery

5.1.12. Kanegrade Ltd

5.1.13. IPRONA AG

5.1.14. FutureCeuticals Inc.

5.1.15. Louis Dreyfus Company

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Market Share, Product Innovation, Regional Presence, Distribution Network, Sustainability Initiatives, R&D Expenditure)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product launches, expansions, partnerships)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. North America Juice Concentrates Market Regulatory Framework

6.1. Food Safety Standards

6.2. Compliance with FDA Regulations

6.3. Certification Processes (Organic, Non-GMO, Gluten-Free)

7. North America Juice Concentrates Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America Juice Concentrates Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Form (In Value %)

8.4. By Ingredient Type (In Value %)

8.5. By Region (In Value %)

9. North America Juice Concentrates Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. White Space Opportunity Analysis

9.3. Customer Cohort Analysis

9.4. Marketing Initiatives

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the North America Juice Concentrates Market. This step is supported by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary goal is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the North America Juice Concentrates Market. This includes assessing market penetration, product category performance, and the resultant revenue generation. Furthermore, an evaluation of consumer preferences and demand trends is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse range of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple juice concentrate manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the North America Juice Concentrates market.

Frequently Asked Questions

01 How big is the North America Juice Concentrates Market?

The North America Juice Concentrates Market is valued at USD 25 billion, driven by the rising demand for natural and clean-label products across the food and beverage industry.

02 What are the challenges in the North America Juice Concentrates Market?

Challenges in North America Juice Concentrates Market include the high cost of raw materials, fluctuations in agricultural yield, and stringent regulations related to product labeling and safety. Supply chain disruptions also pose risks to manufacturers.

03 Who are the major players in the North America Juice Concentrates Market?

Key players in the North America Juice Concentrates Market t include Archer Daniels Midland Company, Ingredion Incorporated, Dhler GmbH, Kerry Group, and SunOpta Inc. These companies dominate due to their extensive product portfolios and strong distribution networks.

04 What drives the demand for juice concentrates in North America?

The demand for juice concentrates is driven by a preference for natural ingredients in beverages, rising health awareness among consumers, and a shift away from artificial sweeteners.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.