North America LiDAR Market Outlook to 2030

Region:North America

Author(s):Naman Rohilla

Product Code:KROD3997

September 2024

81

About the Report

North America LiDAR Market Overview

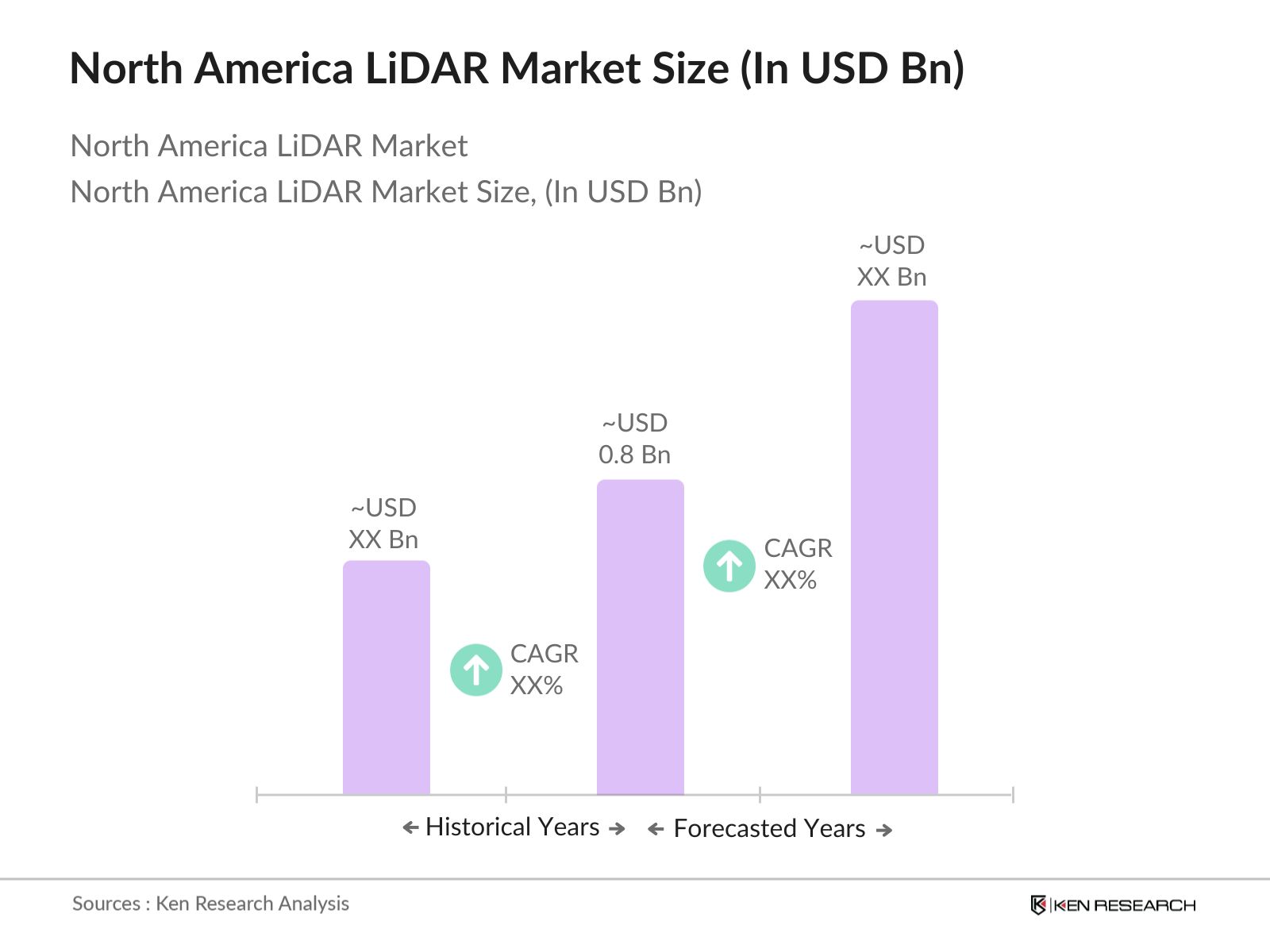

- The North America LiDAR market is valued at USD 0.8 billion, driven by the increasing adoption of autonomous vehicles, UAVs (unmanned aerial vehicles), and precision mapping technologies. The rising investments in smart city infrastructure and the growing need for accurate, real-time data for urban planning are key drivers. Technological advancements in LiDAR systems, such as enhanced accuracy and compact designs, have further catalyzed market growth, particularly in sectors like automotive, defence, and environmental monitoring.

- The United States and Canada dominate the North America LiDAR market due to their strong emphasis on technological innovation and early adoption of autonomous systems. The U.S., with its large automotive sector and defence spending, leads the demand for advanced LiDAR systems. Additionally, government funding and support for smart city initiatives in Canada have boosted the market, making these countries leaders in the development and deployment of LiDAR technologies.

- LiDAR sensor calibration standards are crucial for ensuring accuracy and consistency across various applications, especially in autonomous vehicles and mapping. In 2023, the U.S. Department of Transportation established new standards for LiDAR calibration, mandating annual recalibration for all sensors used in public infrastructure projects. This regulation ensures that sensors maintain a high level of accuracy, reducing errors in critical applications such as autonomous driving.

North America LiDAR Market Segmentation

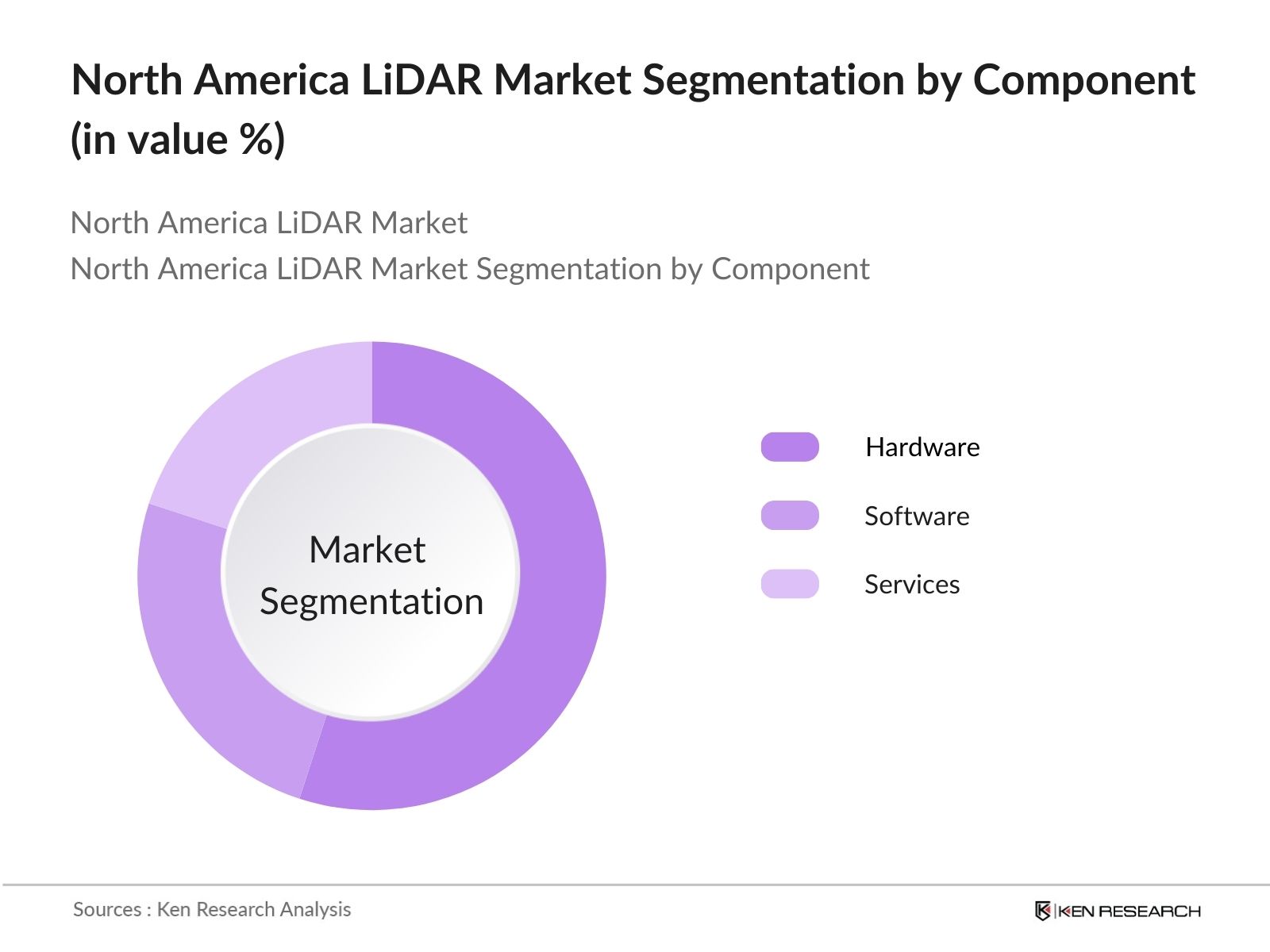

- By Component: The market is segmented by component into hardware, software, and services. Hardware, including sensors and GPS receivers, dominates the market, accounting for the largest share. This is primarily because hardware forms the backbone of LiDAR systems and is essential for data collection. The demand for high-precision hardware is also increasing due to advancements in autonomous driving and UAV mapping technologies, further solidifying this segment's dominant position in the market.

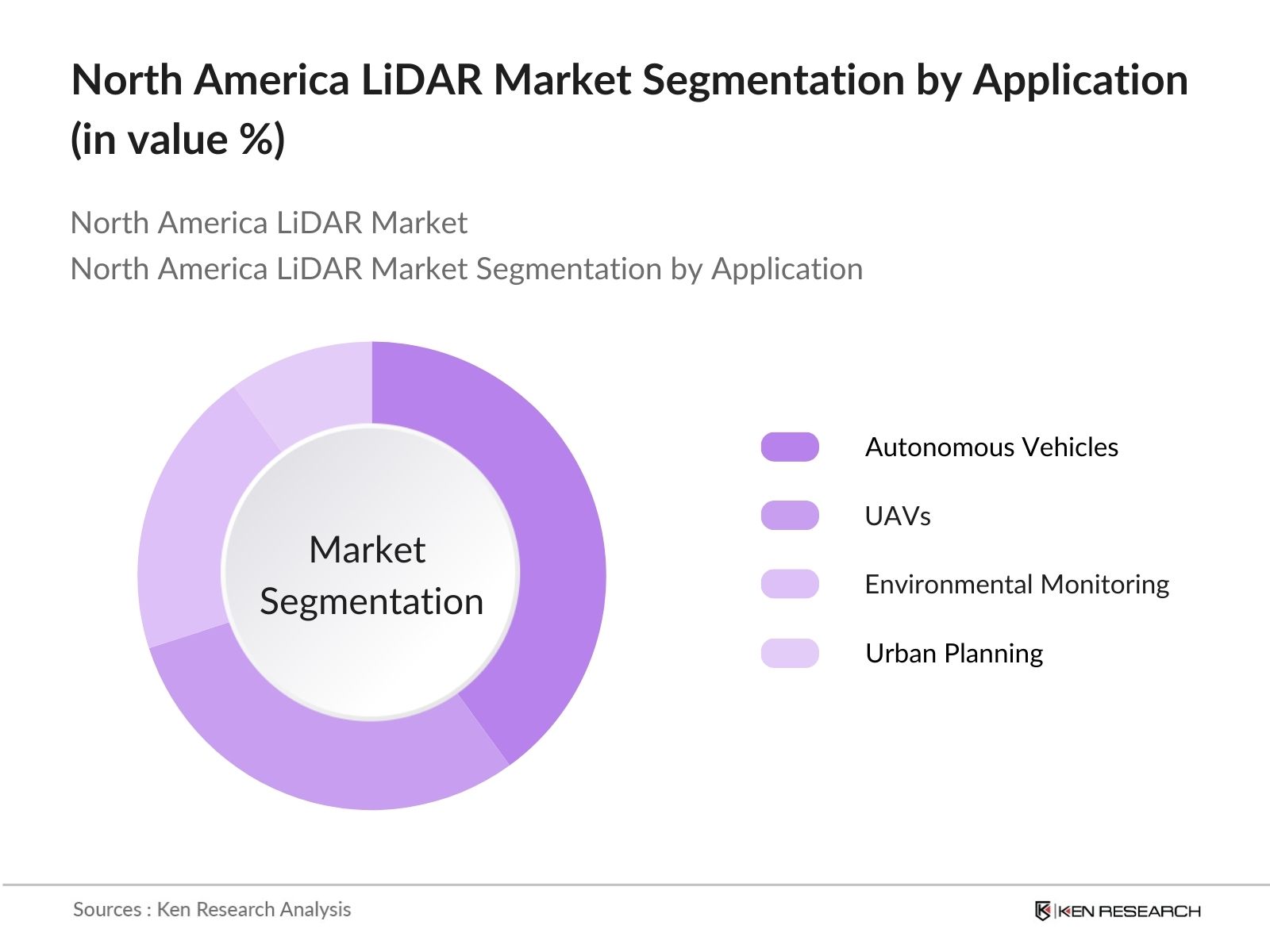

- By Application: The market is segmented by application into autonomous vehicles, UAVs, environmental monitoring, and urban planning. Autonomous vehicles hold the dominant share in this segment. The rapid development of self-driving cars and the growing investments by automotive giants in North America have propelled the demand for LiDAR systems. These systems provide real-time 3D mapping and object detection, which are critical for the safe navigation of autonomous vehicles.

North America LiDAR Market Competitive Landscape

The North America LiDAR market is dominated by a few key players who have established themselves through extensive product portfolios, technological innovations, and strategic collaborations. Companies like Velodyne and Luminar have a strong foothold in the automotive sector, while others like Trimble and Teledyne Optech focus on geospatial applications and precision mapping.

| Company Name | Establishment Year | Headquarters | Product Portfolio | Key Technologies | Core Applications | Strategic Initiatives | Market Presence | R&D and Innovation |

|---|---|---|---|---|---|---|---|---|

| Velodyne Lidar | 1983 | San Jose, USA | - | - | - | - | - | - |

| Trimble Inc. | 1978 | Sunnyvale, USA | - | - | - | - | - | - |

| Teledyne Optech | 1974 | Ontario, Canada | - | - | - | - | - | - |

| Luminar Technologies | 2012 | Orlando, USA | - | - | - | - | - | - |

| Faro Technologies | 1981 | Lake Mary, USA | - | - | - | - | - | - |

North America LiDAR Market Analysis

North America LiDAR Market Growth Drivers

- Increasing Adoption in Autonomous Vehicles: The increasing use of LiDAR (Light Detection and Ranging) technology in autonomous vehicles is driven by the demand for real-time object detection and high-precision mapping. By 2024, the United States will have over 1,400 self-driving vehicles in testing and deployment, requiring precise environmental data for safe navigation. LiDAR sensors enable vehicles to detect objects at distances of up to 200 meters, enhancing safety. This market growth is supported by the U.S. Department of Transportation's push for expanding autonomous vehicle testing in multiple states.

- Rising Investments in Smart City Initiatives: Governments across North America are investing heavily in smart city projects, driving demand for LiDAR technology for infrastructure mapping, traffic monitoring, and urban planning. For instance, the U.S. federal government has earmarked $165 billion for smart city infrastructure development in 2024. LiDAR systems play a crucial role in creating detailed 3D maps of urban environments, facilitating better traffic management and infrastructure maintenance.

- Demand for High-Accuracy Mapping: The need for high-accuracy mapping in industries like construction, mining, and agriculture has surged, with LiDAR technology providing detailed topographical data. The precision of LiDAR systems—capable of mapping landscapes with a vertical accuracy of 10 centimetres is essential for large-scale construction projects. In 2023, North American construction firms utilized LiDAR for nearly 1,500 infrastructure projects across the continent, ensuring higher levels of accuracy and efficiency.

North America LiDAR Market Challenges

- High Initial Equipment Cost: The initial cost of LiDAR sensors, which ranges from $4,000 to $75,000 depending on specifications, poses a challenge for widespread adoption, particularly in industries with limited budgets. This high price point is a barrier to entry for smaller businesses and government projects with limited resources. A report from the National Renewable Energy Laboratory suggests that even with the cost reductions from mass production, pricing remains an issue for smaller autonomous vehicle manufacturers.

- Complex Data Processing and Analysis: LiDAR systems generate vast amounts of data up to 700,000 data points per second requiring advanced processing tools for analysis. This complex data necessitates computational power and storage solutions, increasing operational costs for companies. In 2023, North American firms reported spending an average of $150,000 annually on data processing infrastructure for large-scale LiDAR projects. The complexity of the data has delayed adoption across industries that lack the necessary analytics capabilities.

North America LiDAR Market Future Outlook

Over the next five years, the North America LiDAR market is expected to grow exponentially, driven by advancements in autonomous vehicle technology, increased adoption of UAVs for precision agriculture and mapping, and growing investments in smart city infrastructure. Government initiatives to support innovation in LiDAR technology, along with rising demand for real-time 3D data in various industries, are anticipated to further drive market expansion. Companies are also likely to focus on developing compact, cost-effective LiDAR systems to cater to a wider range of applications.

North America LiDAR Market Opportunities

- Increasing Applications in Renewable Energy Sector: LiDAR is being increasingly adopted in the renewable energy sector, particularly in wind energy for wind profiling and turbine placement. In 2023, LiDAR technology was used in over 200 wind farms across North America to optimize turbine efficiency by accurately measuring wind speeds and directions at various altitudes. The U.S. Department of Energy reported that accurate wind profiling through LiDAR has improved energy generation efficiency by up to 10%, leading to increased adoption in the renewable energy market.

- Integration with Drones for Mapping: The use of drones equipped with LiDAR technology for mapping and surveying has gained traction in 2024. Drones enable faster and more cost-effective data collection for applications such as land surveying, forestry, and agriculture. In Canada, nearly 1,000 commercial drones were equipped with LiDAR systems in 2023, covering an estimated 150,000 square kilometres of terrain. This integration allows for precise mapping in difficult-to-access areas, increasing efficiency in industries like forestry and agriculture.

Scope of the Report

| By Component |

Hardware Software Services |

| By Application |

Autonomous Vehicles UAVs Environmental Monitoring Urban Planning and Smart Cities |

| By Range |

Short Range Medium Range Long Range |

| By End-Use Industry |

Automotive Aerospace and Defense Construction Energy and Utilities |

| By Region |

United States Canada Mexico |

Products

Key Target Audience

Autonomous Vehicle Manufacturers

UAV Manufacturers

Aerospace and Defense Contractors

Banks and Financial Institutions

Smart City and Urban Planning Authorities

Environmental Monitoring Agencies

Renewable Energy Companies

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (Federal Aviation Administration, U.S. Department of Transportation)

Companies

North America LiDAR Market Major Players

Velodyne Lidar

Trimble Inc.

Teledyne Optech

Quanergy Systems

Leica Geosystems AG (Hexagon)

LeddarTech

Faro Technologies

Innoviz Technologies

Aeva Inc.

Luminar Technologies

Ouster Inc.

Geodigital International

SICK AG

RIEGL Laser Measurement Systems GmbH

Hesai Technology

Table of Contents

1. North America LiDAR Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. North America LiDAR Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. North America LiDAR Market Analysis

3.1. Growth Drivers (Sensor accuracy, Automation, and Smart Infrastructure)

3.1.1. Increasing Adoption in Autonomous Vehicles

3.1.2. Rising Investments in Smart City Initiatives

3.1.3. Demand for High-Accuracy Mapping

3.2. Market Challenges (Hardware costs, Data Processing, and Environmental Constraints)

3.2.1. High Initial Equipment Cost

3.2.2. Complex Data Processing and Analysis

3.2.3. Performance in Poor Weather Conditions

3.3. Opportunities (LiDAR in Renewable Energy, Drones, and Advanced Analytics)

3.3.1. Increasing Applications in Renewable Energy Sector

3.3.2. Integration with Drones for Mapping

3.3.3. Expansion in Analytics and AI for LiDAR Data

3.4. Trends (Automation, Hybrid Solutions, and Compact LiDAR Systems)

3.4.1. Growing Use of LiDAR in Autonomous Driving

3.4.2. Increasing Demand for Hybrid LiDAR Solutions

3.4.3. Development of Compact and Low-Cost LiDAR Sensors

3.5. Government Regulation (Compliance, Certification, and Standards)

3.5.1. Standards for LiDAR Sensor Calibration

3.5.2. Government Policies for Autonomous Vehicle Testing

3.5.3. Regulatory Framework for Airspace Use in LiDAR Mapping

3.6. SWOT Analysis

3.7. Stake Ecosystem (Suppliers, Integrators, and End-Users)

3.7.1. Role of Suppliers in Hardware Innovation

3.7.2. Integration Challenges for Industry Participants

3.8. Porter’s Five Forces

3.9. Competition Ecosystem (Market Share, Strategic Alliances, and Innovations)

3.9.1. Strategic Collaborations among Major Players

4. North America LiDAR Market Segmentation

4.1. By Component (In Value %)

4.1.1. Hardware

4.1.2. Software

4.1.3. Services

4.2. By Application (In Value %)

4.2.1. Autonomous Vehicles

4.2.2. UAVs

4.2.3. Environmental Monitoring

4.2.4. Urban Planning and Smart Cities

4.3. By Range (In Value %)

4.3.1. Short Range

4.3.2. Medium Range

4.3.3. Long Range

4.4. By End-Use Industry (In Value %)

4.4.1. Automotive

4.4.2. Aerospace and Defense

4.4.3. Construction

4.4.4. Energy and Utilities

4.5. By Country/Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5. North America LiDAR Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Velodyne Lidar

5.1.2. Trimble Inc.

5.1.3. Teledyne Optech

5.1.4. Quanergy Systems

5.1.5. Leica Geosystems AG (Hexagon)

5.1.6. LeddarTech

5.1.7. Faro Technologies

5.1.8. Innoviz Technologies

5.1.9. Aeva Inc.

5.1.10. Luminar Technologies

5.1.11. Ouster Inc.

5.1.12. Geodigital International

5.1.13. SICK AG

5.1.14. RIEGL Laser Measurement Systems GmbH

5.1.15. Hesai Technology

5.2. Cross Comparison Parameters (Product Portfolio, R&D Investments, Market Penetration, Patents, AI Integration, Custom Solutions, Pricing, and Customer Base)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Joint Ventures, and Collaborations)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Private Equity and Venture Capital)

5.7. Government Grants and Subsidies

5.8. Innovation Focus (Product Launches, Patents, and New Technologies)

6. North America LiDAR Market Regulatory Framework

6.1. Environmental Standards and Regulations for LiDAR

6.2. Compliance Requirements for Autonomous Vehicles

6.3. Certification Processes for LiDAR Systems

7. North America LiDAR Market Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. North America LiDAR Market Future Market Segmentation

8.1. By Component (In Value %)

8.2. By Application (In Value %)

8.3. By Range (In Value %)

8.4. By End-Use Industry (In Value %)

8.5. By Country/Region (In Value %)

9. North America LiDAR Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial stage involved creating a detailed ecosystem map of the North America LiDAR market, identifying all major stakeholders, such as autonomous vehicle manufacturers and UAV companies. Desk research combined with proprietary databases was used to identify the key variables driving market growth.

Step 2: Market Analysis and Construction

This phase focused on analyzing historical data and market trends within the North America LiDAR market. This included assessing technological adoption rates, and industry penetration, and analyzing the performance of key market players to build accurate market estimates.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations were conducted through interviews with professionals in the automotive, defence, and geospatial sectors. These interviews provided critical insights into LiDAR system deployment and emerging market trends, helping validate our market hypotheses.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing the data collected from various sources and incorporating it into a comprehensive market report. LiDAR manufacturers and distributors were consulted to cross-verify the findings and refine the final report.

Frequently Asked Questions

01. How big is the North America LiDAR market?

The North America LiDAR market is valued at USD 0.8 billion, driven by the demand for precision mapping in autonomous vehicles, UAVs, and smart city projects.

02. What are the challenges in the North America LiDAR market?

Challenges in the North America LiDAR market include the high initial cost of hardware, complexity in data processing, and limitations in performance under poor weather conditions, which impact the widespread adoption of LiDAR technologies.

03. Who are the major players in the North America LiDAR market?

Key players in the North America LiDAR market include Velodyne Lidar, Trimble Inc., Teledyne Optech, Luminar Technologies, and Faro Technologies, who dominate the market due to their innovative product offerings and strategic partnerships.

04. What are the growth drivers of the North America LiDAR market?

The North America LiDAR market is driven by technological advancements in autonomous driving, increased investments in smart cities, and the growing adoption of UAVs for precision agriculture and environmental monitoring.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.